|

시장보고서

상품코드

2062468

유기 바이오가스 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Organic Biogas - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

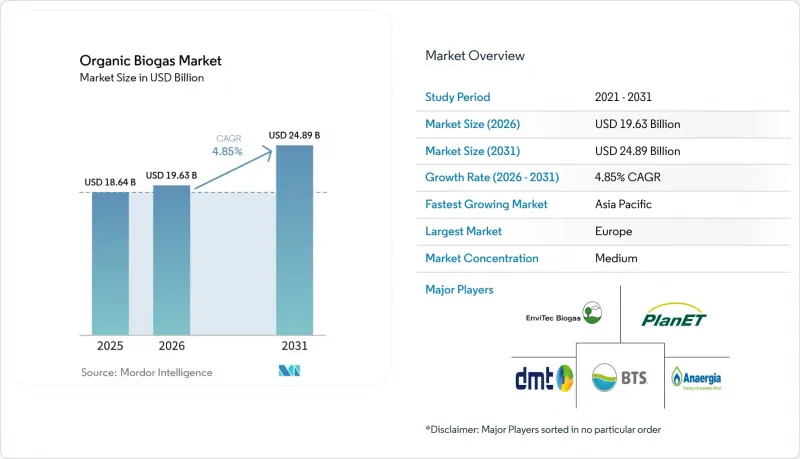

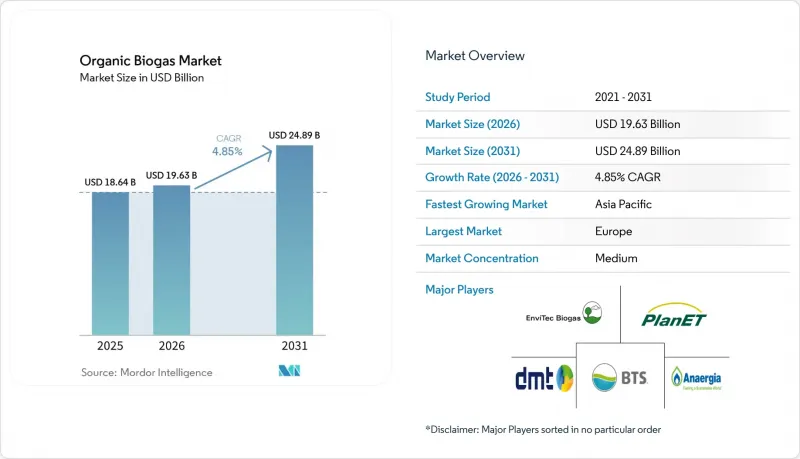

Mordor Intelligence에 의하면, 유기 바이오가스 시장 규모는 2025년에 186억 4,000만 달러로 평가되었고, 2026년에 196억 3,000만 달러로 추정되고, 2031년까지 248억 9,000만 달러에 이를 것으로 예측되며, 2026-2031년 CAGR 4.85%로 성장할 전망입니다.

본 보고서는 원료별(농업 잔여물 등), 기술별(습식 혐기성 소화 등), 플랜트 규모별(농장 규모, 중규모 등), 용도별(발전 등), 최종 사용자 부문별(지방 자치 단체 등) 및 지역별(북미, 유럽, 아시아태평양, 남미, 중동 및 아프리카)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 유기 바이오가스 시장 동향 및 분석

정부의 인센티브와 재생에너지 목표

투자 적격 수준의 명확한 정책이 유기 바이오가스 시장의 기반이 되고 있습니다. 미국의 RNG 인센티브법은 발전 사업자를 도매 전력 가격 변동으로부터 보호하기 위한 생산 세액 공제를 규정하고 있습니다. 브라질의 2025년 바이오메탄법은 가스 공급업체에 2026년부터 배출량을 10% 감축할 것을 의무화하고 있으며, 이에 따라 저탄소 분자 구매 의무가 즉시 강화됩니다. 덴마크의 배출량 70% 감축법은 국내 원료 잠재력의 거의 전부를 흡수하는 '바이오메탄 우선' 전력망 전략을 추진하고 있습니다. 인도의 SATAT 제도는 국내 바이오 CNG 플랜트의 규모 확대를 가능하게 하는 구매 보장을 제공함으로써, 2030년까지 수요를 40배로 늘리는 것을 촉진하고 있습니다. 이러한 일관된 조치 덕분에 금융 관계자들은 15년의 회수 기간을 가진 수 메가와트 규모의 시설을 지원할 수 있다는 자신감을 갖게 되었습니다.

유기성 폐기물 발생량 증가와 매립 금지 의무

도시 지역의 폐기물 처리비 인상과 메탄 감축 목표가 도시 지역 유기성 바이오가스 시장의 성장을 가속하고 있습니다. 최신 소화조는 식품 폐기물에서 생화학적 산소 요구량(BOD)의 95%를 제거하는 동시에, 제거된 화학적 산소 요구량(COD) 1그램당 0.292리터의 메탄을 생성합니다. 하수처리장에 병설된 혐기성 막 생물반응기는 고농도의 유기물을 처리하여 전력망 공급 기준에 부합하는 바이오메탄을 생산합니다. 전형적인 대도시권 프로젝트의 경우, 소화 잔여물 비료와 탄소 크레딧을 통해 수익을 창출함으로써 6년 이내에 설비 투자 비용을 회수할 수 있습니다. 도시 지역의 원료는 품질이 안정적이기 때문에 대규모 시설 건설이 가능하며, 계절적 제약을 받는 농업 잔여물과 비교할 때 단위 비용 절감과 수익성 향상을 도모할 수 있습니다.

혐기성 소화 설비의 높은 초기 설비 투자(CAPEX)

유틸리티급 소화조는 1MW당 300만-800만 달러의 비용이 듭니다. 이는 맞춤형 전처리, 바이오가스 정제 및 악취 관리 시스템을 반영한 것입니다. EnviTec사가 포레스트와 프리드랜드에서 진행한 5,000만 유로 규모의 설비 현대화를 통해 가스 정제 능력은 두 배로 늘어났지만, 이는 경험이 풍부한 사업자에게도 자본 측면에서 높은 장벽이 됨을 보여줍니다. 금융 기관들은 기술적 리스크를 이유로 들지만, 자산군의 성숙도와 95%의 가동률 실적을 바탕으로 선진국 시장에서는 프로젝트 파이낸싱 확보가 점점 더 수월해지고 있는 반면, 신흥 지역에서는 여전히 차입 자금 조달에 제약이 있습니다.

부문별 분석

2025년, 농업 잔여물은 유기성 바이오가스 시장 점유율의 34.1%를 차지했습니다. 반면, 식품 폐기물은 지자체의 폐기물 감축 의무를 충족시키고 있으며, 연평균 6.7%의 성장률을 기록하고 있어 프로젝트의 내부수익률(IRR)을 높이는 확실한 수익원을 제공합니다.

EU 지역 내에서만 해도, 지자체의 가정별 수거 프로그램을 통해 연간 1,800만 톤의 식품 폐기물이 수거되고 있으며, 고에너지 원료가 소화조로 보내져 톤당 520 Nm³의 바이오가스가 생산되고 있습니다. 이는 일반적인 작물 잔여물보다 약 45% 더 많은 수치입니다. 캘리포니아주의 낙농업 부문도 비슷한 성장세를 보이고 있습니다. 2024년에는 1,230만 톤의 가축 분뇨가 소화조에 투입되어 6억 2,000만 달러 상당의 RNG 크레딧을 창출했으며, 이는 젖소 800마리 미만의 목장에서 발생하는 우유 판매 수익을 상회했습니다. 하수 슬러지 시장의 경우, 독일이 2029년부터 대규모 시설에서의 토양 살포를 금지할 예정이므로 시장이 축소될 것으로 예측됩니다.

습식 CSTR은 운영 신뢰성과 기존 투자로 인해 여전히 52.3%의 시장 점유율을 차지하고 있지만, 건식 소화는 물 사용량을 70% 절감하고 설치 면적을 40% 축소할 수 있다는 장점을 바탕으로 연간 7.1%의 성장률을 기록하고 있습니다. DRANCO사의 고형분 함량이 높은 플랜트는 체류 시간을 21일로 단축할 수 있어, 설비 투자를 비례적으로 늘리지 않고도 처리 능력을 향상시킬 수 있습니다.

2단계 공동 소화 설계는 지질이 풍부한 폐기물에서 메탄 수율을 향상시킵니다. 그러나 1MW 규모의 설비의 경우, 이에 120만 달러의 추가 비용이 소요됩니다. 한편, 라그나형 시스템은 비용 대비 효과가 뛰어나 열대 지역의 축산 거점에서 선호되고 있습니다. 그러나 평균적인 메탄 누출이 문제로 지적되면서, 기후 변화 대책으로서의 신뢰성이 위협받고 있습니다. 2025년, 능동 흡입식 막 커버의 도입으로 이 메탄 누출이 감소했습니다. 그러나 신용 확보가 어려운 시장에서는 이러한 기술 혁신으로 인해 투자 회수 기간이 1년 이상 길어지고 말았습니다.

지역별 분석

유럽은 2025년 매출의 41.2%를 차지했으며, 독일의 9,500개 플랜트와 덴마크의 세계 최고 수준인 바이오메탄 송전망 도입률 28%가 그 기반이 되고 있습니다. 원료 공급원이 포화 상태이며, 바이에른주 등 일부 지역에서는 계통 연계 대기 기간이 18개월에 달하고 있습니다. 북유럽 국가들에서는 운송용 연료의 30%를 재생에너지로 충당해야 한다는 의무 규정과 바이오 LNG의 조기 도입에 힘입어 성장이 두드러지고 있습니다.

아시아태평양은 2031년까지 연평균 6.4%의 성장률을 기록할 전망이며, 유기 바이오가스 시장에서 가장 빠르게 성장하는 지역이 될 것으로 전망됩니다. 중국의 500억 위안 규모의 농촌용 소화조 기금과 인도의 5,000개 플랜트라는 SATAT 목표가 추진력을 뒷받침하고 있지만, 부지 확보에 대한 우려와 임베디드 가격을 둘러싼 분쟁으로 인해 실행은 지연되고 있습니다. 일본은 2024년 식품재활용법 개정 이후 틈새 시장의 선두주자로 부상하고 있으며, 동남아시아의 성장은 팜유 폐수 처리 시설 프로젝트를 통해 뒷받침되고 있습니다.

북미에서는 캘리포니아주가 LCFS를 통해 RNG 수요를 주도하고 있으며, 캐나다의 주별 탄소세는 브리티시컬럼비아주와 퀘벡주에서 10여 건의 신규 프로젝트를 촉발하고 있습니다. 멕시코에서는 파이프라인 접근성이 제한적이기 때문에 주로 식품 공장에서의 현장 증기 이용을 목적으로 설비 용량이 증가하고 있습니다. 남미 및 중동 및 아프리카은 여전히 규모는 작지만, 브라질 설탕 산업의 시범 프로젝트와 UAE의 폐기물 발전 시설 건설이 진행되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.22According to Mordor Intelligence, the organic biogas market size is projected to be USD 18.64 billion in 2025, USD 19.63 billion in 2026, and reach USD 24.89 billion by 2031, growing at a CAGR of 4.85% from 2026 to 2031.

This report is Segmented by Feedstock (Agricultural Residues, and More), Technology (Wet Anaerobic Digestion, and More), Plant Scale (Farm-Scale, Medium, and More), Application (Electricity Generation and More), End-User Sector (Municipal Utilities, and More), and Geography (North America, Europe, Asia-Pacific, South America, Middle East and Africa). Market Forecasts are Provided in Terms of Value (USD).

Global Organic Biogas Market Trends and Insights

Government Incentives & Renewable-Energy Targets

Investment-grade policy clarity underpins the organic biogas market. The US RNG Incentive Act anchors production tax credits that insulate developers from wholesale power volatility. Brazil's 2025 biomethane statute obliges gas suppliers to cut emissions 10% from 2026, immediately sharpening purchase obligations for low-carbon molecules. Denmark's 70% emission-reduction law executes a biomethane-first grid strategy that absorbs nearly all domestic feedstock potential. India's SATAT scheme provides offtake guarantees that scale domestic bio-CNG plants, fostering a forty-fold demand rise by FY 2030.Such aligned measures give financiers confidence to back multimegawatt facilities with 15-year paybacks.

Rising Organic-Waste Generation & Landfill-Diversion Mandates

Municipal tipping-fee escalation and methane-abatement goals propel organic biogas market growth in cities. Advanced digesters now remove 95% biochemical oxygen demand from food waste while yielding 0.292 L methane per gram of chemical oxygen demand removed.Anaerobic membrane bioreactors co-located at wastewater plants treat high-strength organics and generate grid-quality biomethane streams. Typical metropolitan projects repay capital within six years once digestate fertilizer and carbon credits are monetized. Urban feedstock consistency enables larger facilities, lowering unit costs and boosting profitability relative to seasonally constrained farm residues.

High Upfront CAPEX of Anaerobic-Digestion Plants

Utility-scale digesters cost USD 3-8 million per MW, reflecting bespoke preprocessing, biogas upgrading, and odor management systems. EnviTec's EUR 50 million upgrades at Forst and Friedland double gas-upgrading capacity yet illustrate steep capital hurdles even for experienced operators. Although lenders cite technology risk, asset-class maturity, and 95% uptime records increasingly secure project finance in developed markets, while emerging regions still face constrained debt availability.

Other drivers and restraints analyzed in the detailed report include:

- Decarbonization Mandates for Transportation Bio-Fuels

- Carbon-Negative Bio-Fertilizer Demand

- Grid-Injection Bottlenecks & Gas-Quality Compliance Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Agricultural residues retained 34.1% of the organic biogas market share in 2025. In contrast, food waste meets municipal diversion mandates and is expanding at 6.7% annually, delivering reliable gate fees that improve project IRRs.

Municipal curbside programs are diverting 18 million tons of food waste per year within the EU alone, funneling high-energy substrates into digesters that realize 520 Nm3 of biogas per ton, roughly 45% more than average crop residues. California's dairy sector illustrates parallel momentum: 12.3 million tons of manure fed to digesters in 2024 generated RNG credits worth USD 620 million, surpassing farm milk revenue for herds under 800 cows. The sewage sludge market is expected to decline after Germany bans land application from large plants in 2029.

Wet CSTR continues to dominate with 52.3% share because of operational reliability and legacy investments, yet dry digestion is growing 7.1% per year by leveraging 70% lower water use and 40% smaller footprint. A DRANCO high-solids plant can reduce retention time to 21 days, boosting throughput without proportional capex.

Two-stage co-digestion designs boost methane yields from lipid-rich waste. However, this comes at an added cost of USD 1.2 million for a 1 MW setup. While Laguna-type systems are favored in tropical livestock hubs for their cost-effectiveness, they face scrutiny due to an average methane slip, jeopardizing their climate credentials. In 2025, the introduction of active-suction membrane covers reduced this slip. Yet, in markets where credit is hard to come by, this innovation has pushed the payback period out by over a year.

Geography Analysis

Europe maintained 41.2% of 2025 revenue, anchored by Germany's 9,500 plants and Denmark's world-leading 28% biomethane grid penetration. Feedstock sources mature, and interconnection queues stretch to 18 months in regions such as Bavaria. Nordic countries are experiencing growth, driven by a 30% renewable transport fuel mandate and the early adoption of bio-LNG.

Asia-Pacific will expand 6.4% annually through 2031, making it the fastest-growing region in the organic biogas market. China's CNY 50 billion rural-digester fund and India's 5,000-plant SATAT target underpin momentum, though execution lags amid land fears and offtake-price disputes. Japan is emerging as a niche leader post-2024 Food Recycling Law amendments, and Southeast Asian growth is backed by palm-effluent lagoon projects.

In North America, California drives RNG demand via LCFS, while Canada's provincial carbon taxes have triggered a dozen new projects in British Columbia and Quebec. Mexico adds capacity mainly for on-site steam in food factories because of limited pipeline access. South America and the Middle East & Africa remain small but are logging pilot projects in Brazil's sugar sector and the UAE's waste-to-energy build-out.

- EnviTec Biogas AG

- PlanET Biogas Group

- BTS Biogas SRL

- BioConstruct GmbH

- Scandinavian Biogas

- Nature Energy Biogas

- Bright Biomethane

- Anaergia Inc.

- Hitachi Zosen Inova

- Future Biogas

- Gasum Oy

- Agraferm GmbH

- DMT Environmental Technology

- Schmack Biogas GmbH

- Veolia Environnement

- Air Liquide Biogas Solutions

- ENGIE Biomethane

- Clean Energy Fuels Corp.

- Wartsila (Puregas Solutions)

- Gazpack BV

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Government incentives & renewable-energy targets

- 4.2.2 Rising organic-waste generation & landfill-diversion mandates

- 4.2.3 Decarbonisation mandates for transportation bio-fuels (RNG / Bio-CNG)

- 4.2.4 Carbon-negative bio-fertiliser demand (digestate valorisation)

- 4.2.5 Corporate RNG procurement via virtual pipelines & certificates

- 4.2.6 Bio-LNG demand for emerging green maritime corridors

- 4.3 Market Restraints

- 4.3.1 High upfront CAPEX of anaerobic-digestion plants

- 4.3.2 Feedstock supply-chain seasonality & logistics complexity

- 4.3.3 Grid-injection bottlenecks & gas-quality compliance costs

- 4.3.4 Local opposition due to odour / heavy-vehicle traffic (NIMBY)

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porters Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Feedstock

- 5.1.1 Agricultural Residues

- 5.1.2 Animal Manure

- 5.1.3 Food and Kitchen Waste

- 5.1.4 Sewage Sludge

- 5.1.5 Industrial Organic Waste

- 5.1.6 Energy Crops (e.g., maize silage, sorghum)

- 5.2 By Technology

- 5.2.1 Wet Anaerobic Digestion (CSTR)

- 5.2.2 Dry/High-Solids Digestion

- 5.2.3 Two-Stage/Co-digestion Systems

- 5.2.4 Lagoon/Covered-lagoon AD

- 5.3 By Plant Scale

- 5.3.1 Farm-scale (Below 250 kW)

- 5.3.2 Medium (250 kW to1 MW)

- 5.3.3 Utility-scale (Above 1 MW)

- 5.4 By Application

- 5.4.1 Electricity Generation

- 5.4.2 Heat Only

- 5.4.3 Combined Heat and Power (CHP)

- 5.4.4 Vehicle Fuel (Bio-CNG/Bio-LNG)

- 5.4.5 Pipeline RNG Injection

- 5.4.6 Industrial Steam / Process Heat

- 5.5 By End-User Sector

- 5.5.1 Municipal Utilities

- 5.5.2 Agriculture and Livestock Farms

- 5.5.3 Food and Beverage Manufacturers

- 5.5.4 Waste-management Companies

- 5.5.5 Transport Fuel Distributors

- 5.5.6 Others

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 United Kingdom

- 5.6.2.2 Germany

- 5.6.2.3 France

- 5.6.2.4 Spain

- 5.6.2.5 Nordic Countries

- 5.6.2.6 Russia

- 5.6.2.7 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 South Korea

- 5.6.3.5 ASEAN Countries

- 5.6.3.6 Australia and New Zealand

- 5.6.3.7 Rest of Asia-Pacific

- 5.6.4 South America

- 5.6.4.1 Brazil

- 5.6.4.2 Argentina

- 5.6.4.3 Colombia

- 5.6.4.4 Rest of South America

- 5.6.5 Middle East and Africa

- 5.6.5.1 United Arab Emirates

- 5.6.5.2 Saudi Arabia

- 5.6.5.3 South Africa

- 5.6.5.4 Egypt

- 5.6.5.5 Rest of Middle East and Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 EnviTec Biogas AG

- 6.4.2 PlanET Biogas Group

- 6.4.3 BTS Biogas SRL

- 6.4.4 BioConstruct GmbH

- 6.4.5 Scandinavian Biogas

- 6.4.6 Nature Energy Biogas

- 6.4.7 Bright Biomethane

- 6.4.8 Anaergia Inc.

- 6.4.9 Hitachi Zosen Inova

- 6.4.10 Future Biogas

- 6.4.11 Gasum Oy

- 6.4.12 Agraferm GmbH

- 6.4.13 DMT Environmental Technology

- 6.4.14 Schmack Biogas GmbH

- 6.4.15 Veolia Environnement

- 6.4.16 Air Liquide Biogas Solutions

- 6.4.17 ENGIE Biomethane

- 6.4.18 Clean Energy Fuels Corp.

- 6.4.19 Wartsila (Puregas Solutions)

- 6.4.20 Gazpack BV

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment

- 7.2 Emerging Financing Models (green bonds, blended finance)

- 7.3 Circular-economy Integration Opportunities

- 7.4 Digestate-based Biofertiliser Commercialisation

- 7.5 Pathways to Negative-emission Credits