|

시장보고서

상품코드

2063264

멀티 도메인 컨트롤러 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Multi Domain Controller - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

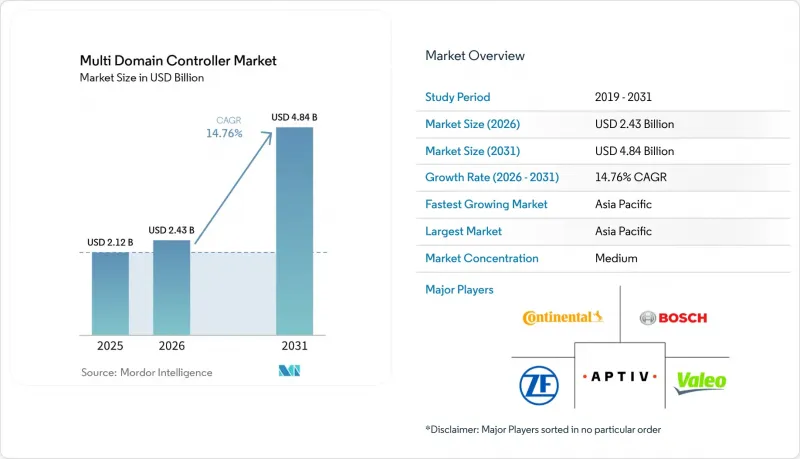

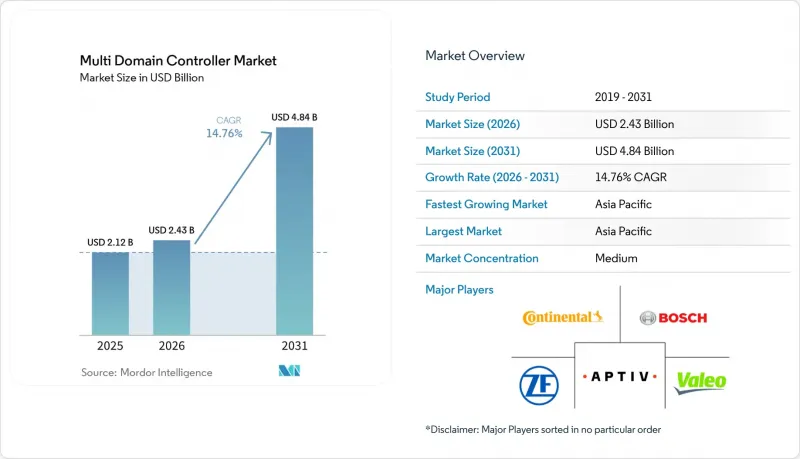

Mordor Intelligence에 의하면, 멀티 도메인 컨트롤러 시장은 2025년 21억 2,000만 달러로 평가되었습니다. 2026년 24억 3,000만 달러로 확대되어 2031년까지 48억 4,000만 달러에 이를 것으로 예측됩니다.

2026년부터 2031년까지의 연평균 성장률(CAGR)은 14.76%를 나타낼 것으로 전망됩니다.

본 보고서는 용도(ADAS 및 안전, 차체 및 편의성, 기타), 차종(승용차, 소형 상용차, 기타), 구동 방식(배터리 전기차, 하이브리드 전기차, 기타), 자율주행 수준(자율주행차 및 반자율주행차), 운영 체제(QNX, 기타), 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 멀티 도메인 컨트롤러 시장 동향 및 인사이트

ADAS 보급률 상승과 L2-L3 수준의 자율주행 확대

각 자동차 제조업체들은 레이더, 카메라, 라이다의 융합 데이터에 기반한 차선 유지, 자동 주차, 고속도로 주행 보조 기능을 표준화하고 있습니다. 집중형 컨트롤러는 개별 유닛 간의 지연을 해소하고, 메모리 및 전력 자원을 공유함으로써 재료비를 절감합니다. 퀄컴의 최신 스냅드래곤 플랫폼은 단일 보드로 주류 모델에서 핸즈프리 운전을 어떻게 지원할 수 있는지 보여줍니다. 중국과 유럽의 자동 긴급 제동 관련 규제 요건은 분산형 토폴로지에서는 충족하기 어려운 최소 연산 능력 기준을 규정하고 있습니다. 센서 스위트의 확장에 따라 대역폭 수요가 증가함에 따라, 하드웨어를 재설계하는 대신 소프트웨어를 통해 업그레이드할 수 있는 확장 가능한 컨트롤러로의 전환이 가속화되고 있습니다.

집중형 및 구역형 E/E 아키텍처로의 전환

존 설계에서는 물리적 위치를 기준으로 배선을 그룹화하여 하네스의 길이와 무게를 줄이는 동시에, 소프트웨어 수명 주기 관리를 간소화합니다. BMW의 ‘Neue Klasse’ 플랫폼은 수십 개의 레거시 유닛을, 단일 하이퍼바이저 하에서 여러 가상 머신을 호스팅하는 3개의 존 컨트롤러로 대체하고 있습니다. 각 공급업체들은 이더넷 스위칭, 전력 분배, 실시간 처리를 통합한 레퍼런스 보드를 출시하고 있으며, 이를 통해 소규모 시스템 통합사업자도 규정을 보다 신속하게 준수할 수 있게 되었습니다. 사이버 보안 로직을 소수의 노드에 집중시킴으로써, 자동차 제조업체는 침투 테스트 횟수를 줄이면서도 UNECE R155의 요건을 충족할 수 있습니다. 그 결과, 차량의 배선 재설치 없이도 향후 자율주행 기능의 업그레이드를 지원할 수 있는 재현성 있는 전기 백본이 구현됩니다.

고성능 SoC의 열 및 전력 제한

증가하는 추론 워크로드는 열을 발생시키지만, 대시보드나 엔진룸 내에서는 그 열을 방출하기 어렵습니다. 각 공급업체들은 예측 기반 스로틀링 및 첨단 냉각 소재를 채택하고 있지만, 극한의 기후 조건에서는 지속적인 최고 성능이 저하될 가능성이 있습니다. 일부 자동차 제조업체는 작업을 여러 개의 저전력 보드로 분할하고 있으며, 이로 인해 완전한 통합을 통한 비용 절감 효과가 줄어들고 있습니다. 패키징 제약은 공간과 기류가 제한된 소형차에서 가장 엄격합니다. 따라서 열 설계가 현실적인 성능 범위를 결정하게 되며, 야심 찬 단일 칩 로드맵의 진행을 지연시킬 가능성이 있습니다.

부문별 분석

2025년 기준으로 ADAS 및 안전 기능은 멀티도메인 컨트롤러 시장의 43.44%를 차지했으며, 이는 고속도로에서의 자율 주행 및 자동 주차를 뒷받침하는 계산 부하가 높은 센서 융합 및 물체 분류 워크로드의 중요성을 여실히 보여주고 있습니다. 자동차 제조업체들은 레이더, 카메라, 라이다(LiDAR)에서 들어오는 신호 간의 지연을 줄이기 위해 중앙 집중식 보드를 활용하고 있으며, 이를 통해 단일 프로세서가 여러 인식 계층을 관리할 수 있게 됩니다. 또한, 표준화된 하드웨어는 차선 유지 및 긴급 제동과 관련된 규제가 확대되는 가운데, 규제상의 우선 과제인 무선 안전 업데이트도 용이하게 해줍니다. 공급업체는 사전 인증을 완료한 기능 안전 소프트웨어를 함께 제공하기 때문에 각 브랜드는 긴 검증 주기를 반복할 필요 없이 전 세계 각지에서 제품을 출시할 수 있습니다. 현재, 경쟁사와의 차별화는 ISO 26262 ASIL-D 요건을 충족하면서 성능, 전력 소비, 비용 간의 균형을 맞추는 데 초점이 맞추어져 있습니다.

조종석용 전자기기 시장은 2031년까지 연평균 성장률(CAGR) 18.21%로 확대되고 있으며, 이는 부문 계층 중 가장 빠른 성장 속도입니다. 계기판, 인포테인먼트, 증강현실(AR) 헤드업 디스플레이가 단일 시스템 온 칩(SoC)에 통합되어 배선량이 줄어들 뿐만 아니라, 화면 간 그래픽 동기화가 가능해집니다. 하이퍼바이저가 보안상 중요한 경고 메시지와 리치 미디어를 분리함으로써, 단일 보드에서 두 가지 워크로드를 모두 법적으로 호스팅할 수 있게 됩니다. 자동차 제조업체들은 하드웨어를 재설계할 필요 없이 원격으로 새로운 사용자 경험 기능을 도입할 수 있기 때문에 이러한 여유 연산 능력을 높이 평가했습니다. 이러한 변화는 구독 수익의 잠재력을 높여주지만, 그래픽스와 ADAS 영역이 칩을 공유하는 비율이 높아짐에 따라 열 관리의 복잡성도 증가하고 있습니다.

2025년에는 승용차가 멀티도메인 컨트롤러 시장의 66.19%를 차지했습니다. 이는 생산 규모가 크다는 점과, 소형차 및 중형차에 탑재된 첨단 운전자 보조 기능에 대한 소비자 수요가 높다는 점을 반영하고 있습니다. 집중형 컴퓨팅을 통해 각 브랜드는 별도의 제어 장치를 추가하지 않고도 운전자 모니터링 카메라, 예측 유지보수 알림, 음성 제어 인포테인먼트 기능을 도입할 수 있게 됩니다. 판매 대수가 증가함에 따라 개발 비용이 수백만 대의 차량에 분산되므로, 고성능 실리콘이 신속하게 저가 시장에 보급될 수 있게 됩니다. 또한 소비자들은 스마트폰과 같은 업데이트 주기를 기대하고 있으며, 이로 인해 승용차 플랫폼은 지속적인 기능 추가가 가능한 소프트웨어 정의 아키텍처로 발전하고 있습니다. 이러한 동향은 클라우드 분석과 차량용 하드웨어 간의 긴밀한 연계를 이끌어내며, 표준화된 컨트롤러 레퍼런스 설계의 채택을 가속화하고 있습니다.

승객용 부문은 신흥 시장이 ADAS 탑재 차량으로 전환하고, 성숙 시장이 OTA(무선) 업데이트를 지원하기 위해 차량을 교체함에 따라 2026년부터 2031년까지 15.01%라는 가장 높은 연평균 성장률(CAGR)을 기록하고 있습니다. 라이드셰어링 및 카셰어링 차량을 구매하는 업체들도 원격 진단을 통해 가동 중단 시간을 줄일 수 있기 때문에 이와 유사한 하드웨어를 도입하고 있습니다. 자동차 제조업체들은 구독 서비스를 통해 단계적으로 제공되는 소프트웨어 패키지를 제공하고 있으며, 이를 통해 중앙 집중식 컨트롤러가 장기적인 수익원으로 변모하고 있습니다. 현재 경쟁사들은 비용 관리를 유지하면서 사이버 보안, 데이터 개인정보 보호, 사용자 경험 간의 균형을 맞추는 데 중점을 두고 있습니다. 각 OEM 업체들이 소프트웨어 정의 전략의 확대를 서두르는 가운데, 실리콘, 미들웨어, 클라우드 서비스를 번들로 제공할 수 있는 Tier 1 공급업체들은 실행 면에서 우위를 점하고 있습니다.

지역별 분석

아시아태평양은 멀티 도메인 컨트롤러 시장 규모의 40.34%를 차지했으며, 2031년까지 연평균 성장률(CAGR) 15.41%로 성장하며 계속해서 기술 발전의 선두를 달리고 있습니다. 중국의 자동차 제조업체들은 수출 제한을 피하기 위해 컨트롤러를 자체 개발하고 있지만, 일본과 한국의 브랜드들은 장기적인 1차 공급업체와의 파트너십에 의존하고 있습니다. 공급업체 생태계가 잘 구축되어 있어 프로토타입 비용을 절감하고 검증 과정을 신속하게 진행할 수 있으므로, 플랫폼은 더 빨리 쇼룸에 선보일 수 있습니다. 차선 유지 및 자동 제동과 관련된 정부의 규제로 인해, 보급형 모델에 대한 수요도 증가하면서 컨트롤러의 판매량은 안정적인 수준을 유지하고 있습니다. 현지 생산된 실리콘, 강력한 정책, 그리고 지원적인 자본이라는 선순환 덕분에 이 지역은 경쟁사들에 대해 확고한 우위를 유지하고 있습니다.

북미는 차량용 소프트웨어의 발상지이며, 멀티도메인 컨트롤러 시장에서 여전히 전략적 핵심 거점으로 자리 잡고 있습니다. 국내 OEM 업체들은 지각, 매핑, 운전자 모니터링을 아우르는 통합적인 연산 능력이 필요한 고속도로 자율주행 기능 업데이트를 전개하고 있습니다. 또한, 이 지역에는 소규모 브랜드에 레퍼런스 보드를 라이선스하는 스타트업 기업도 많이 존재하여 새로운 경쟁 압력을 야기하고 있습니다. NHTSA(미국 도로교통안전국)의 사이버 보안 규정안에서는 모든 프로그램에 대해 하드웨어 계층에서의 보안 부팅 및 침입 감지 기능의 탑재를 의무화하고 있으며, 이러한 기능은 중앙 집중형 플랫폼에서 가장 쉽게 구현할 수 있습니다. 카풀 및 라스트 마일 배송용 차량을 구매하는 업체들은 갓길에서 교체 가능한 컨트롤러를 원하고 있으며, 이로 인해 다양한 사후 서비스 채널이 생겨나고 있습니다.

다중 도메인 컨트롤러 시장에서 유럽이 기여하는 바는 첨단 엔지니어링 기술과 엄격한 규제 체계에 기반을 두고 있습니다. 독일과 스웨덴의 소프트웨어 정의 차량(SDV) 이니셔티브와 같은 주요 프로그램에서는 안전 관련 워크로드를 인포테인먼트 시스템과 분리하는 하이퍼바이저가 채택되어, 단일 보드에서도 엄격한 기능 안전 기준을 준수할 수 있음을 입증하고 있습니다. 책임 소재에 관한 협상으로 인한 지연으로 소비자용 제품의 출시가 늦어지고 있지만, 각 공급업체들은 구역별 하네스와 칩렛 패키지의 개선을 계속하고 있어 향후 전개는 더욱 신속하게 진행될 전망입니다. 중동의 수입업체들은 스마트 모빌리티 목표를 달성하기 위해 고급 차량 모델에 프리미엄 컨트롤러를 탑재하고 있지만, 아프리카와 남미의 일부 지역에서는 여전히 가격에 대한 민감도가 높아, 기존의 전자 제어 장치와 엔트리 레벨 도메인 보드를 결합한 저비용 하이브리드 방식을 채택하고 있습니다. 그 결과, 지역별로 계층화된 모자이크 형태의 상황이 나타나고 있지만, 전 세계의知見은 여전히 새로운 실리콘 로드맵으로 귀결되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.22According to Mordor Intelligence, the multi-domain controller market is projected to grow from USD 2.12 billion in 2025 to USD 2.43 billion in 2026, reaching USD 4.84 billion by 2031, with a CAGR of 14.76% from 2026 to 2031.

This report is Segmented by Application (ADAS and Safety, Body and Comfort, and More), Vehicle Type (Passenger Vehicle, Light Commercial Vehicle, and More), Propulsion Type (Battery Electric Vehicle, Hybrid Electric Vehicle, and More), Autonomy (Autonomous Vehicle and Semi-Autonomous Vehicle), Operating System (QNX and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Multi Domain Controller Market Trends and Insights

Rising ADAS Penetration and L2-L3 Autonomy Rollout

Automakers are standardizing lane-keeping, automated parking, and highway pilot features that rely on fused radar, camera, and lidar data. Centralized controllers eliminate latency between separate units and trim material cost by sharing memory and power resources. Qualcomm's latest Snapdragon platform shows how a single board can support hands-free driving in mainstream models. Regulatory requirements for automatic emergency braking in China and Europe lock in minimum compute thresholds that distributed topologies struggle to meet. As sensor suites expand, bandwidth demand reinforces the move to a scalable controller that can be upgraded via software rather than hardware redesign.

Shift Toward Centralized and Zonal E/E Architectures

Zonal designs group wiring by physical location, cutting harness length and weight while simplifying software life-cycle management. BMW's Neue Klasse platform replaces dozens of legacy units with three zone controllers that host multiple virtual machines under a single hypervisor. Suppliers are releasing reference boards that blend Ethernet switching, power distribution, and real-time processing, giving smaller integrators a faster route to compliance. By consolidating cybersecurity logic into a handful of nodes, automakers also meet UNECE R155 obligations with fewer penetration testing cycles. The result is a repeatable electrical backbone that supports future autonomous upgrades without re-wiring the vehicle.

Thermal-Power Limits of High-Compute SoCs

Rising inference workloads generate heat that is hard to dissipate inside dashboards and engine bays. Vendors incorporate predictive throttling and advanced cooling materials, yet sustained peak performance can still drop in extreme climates. Some automakers split tasks across multiple lower-power boards, diluting the cost savings of full consolidation. Packaging constraints are tightest in compact vehicles, where space and airflow are limited. Thermal engineering, therefore, dictates realistic performance envelopes and may slow aggressive one-chip roadmaps.

Other drivers and restraints analyzed in the detailed report include:

- OEM Push for Software-Defined Vehicles and OTA Capability

- Functional-Safety Regulation (ISO 26262, UNECE R155/156)

- Complex ASIL-D Certification Cost/Time

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

ADAS and safety accounted for 43.44% of the Multi Domain Controller market share in 2025, underscoring the compute-hungry sensor-fusion and object-classification workloads that support highway piloting and automated parking. Automakers rely on centralized boards to cut latency between radar, camera, and lidar inputs, allowing a single processor to supervise multiple perception layers. The standardized hardware also eases over-the-air safety updates, a regulatory priority as lane-keeping and emergency-braking rules widen. Suppliers bundle pre-certified functional-safety software so brands can launch across global regions without repeating long validation cycles. Competitive differentiation now centers on balancing performance, power, and cost while meeting ISO 26262 ASIL-D obligations.

Cockpit electronics is advancing at an 18.21% CAGR through 2031, the fastest pace within the segment hierarchy. Instrument clusters, infotainment, and augmented-reality head-up displays are merging onto a single system-on-chip, shrinking wiring mass and enabling synchronized graphics across screens. A hypervisor separates safety-critical telltales from rich media, allowing one board to host both workloads legally. Automakers value the extra compute headroom because it lets them deploy new user-experience features remotely rather than redesigning hardware. This shift adds subscription revenue potential yet raises thermal-management complexity as graphics and ADAS domains increasingly share silicon.

Passenger vehicles captured 66.19% of the Multi Domain Controller market share in 2025, reflecting high production scale and consumer appetite for advanced driver-assistance features in compact and midsize models. Centralized compute helps brands roll out driver-monitoring cameras, predictive maintenance alerts, and voice-controlled infotainment without adding separate control units. Higher sales volumes spread development cost across millions of cars, enabling premium silicon to reach lower price points quickly. Consumers also expect smartphone-like update cycles, which push passenger-car platforms toward software-defined architectures that permit ongoing feature drops. These dynamics forge a tight loop between cloud analytics and in-car hardware, accelerating the adoption of standardized controller reference designs.

The same passenger segment also posts the fastest 15.01% CAGR over 2026-2031, as emerging markets upgrade to ADAS-equipped vehicles and mature markets refresh fleets to enable over-the-air updates. Fleet buyers in ride-hailing and car-sharing adopt similar hardware because remote diagnostics cut downtime. Automakers offer tiered software packages unlocked by subscription, turning centralized controllers into long-term revenue engines. Competition now centers on balancing cybersecurity, data privacy, and user experience while maintaining cost discipline. Tier-one suppliers that can bundle silicon, middleware, and cloud services hold an execution edge as OEMs race to scale software-defined strategies.

Geography Analysis

Asia-Pacific accounted for 40.34% of the Multi Domain Controller market size and continues to set the technology pace, growing at 15.41% CAGR to 2031. Chinese automakers design controllers in-house to avoid export limits, while Japanese and South Korean brands rely on long-term tier-one partnerships. A dense supplier ecosystem lowers prototype costs and speeds validation, so platforms reach showrooms more quickly. Government mandates for lane-keeping and automatic braking reinforce demand even in entry vehicles, locking in steady controller volume. This virtuous cycle of local silicon, strong policy, and supportive capital keeps the region firmly in front of rivals.

North America is the historical cradle of in-vehicle software and remains a strategic pillar for the Multi Domain Controller market. Domestic original-equipment manufacturers are rolling out highway pilot updates that require unified compute across perception, mapping, and driver monitoring. The region also houses many start-ups that license reference boards to smaller brands, adding fresh competitive pressure. Cybersecurity draft rules from NHTSA require every program to embed secure boot and intrusion detection at the hardware layer, a feature most easily implemented on centralized platforms. Fleet buyers in ride-hailing and last-mile delivery demand controllers that can be swapped curbside, creating a rich after-sales channel.

Europe's contribution to the Multi Domain Controller market rests on engineering depth and a stringent regulatory framework. Flagship programs such as software-defined vehicle initiatives in Germany and Sweden showcase hypervisors that quarantine safety workloads from infotainment, demonstrating how a single board can respect strict functional-safety doctrine. Delays tied to liability negotiations slow consumer launches, yet the supplier base keeps refining zonal harnesses and chiplet packages so future rollouts will move faster. Middle-East importers layer premium controllers onto luxury models to meet smart-mobility targets, while Africa and parts of South America remain price-sensitive, adopting low-cost hybrids of legacy electronic control units and entry-level domain boards. The collective outcome is a tiered regional mosaic that still funnels global learning back into new silicon road maps.

- Continental AG

- Robert Bosch GmbH

- ZF Friedrichshafen AG

- Aptiv PLC

- Valeo SA

- BlackBerry (QNX)

- NVIDIA Corporation

- Qualcomm Technologies Inc.

- NXP Semiconductors N.V.

- Renesas Electronics Corporation

- Infineon Technologies AG

- Texas Instruments Inc.

- Visteon Corporation

- Huawei Technologies Co. Ltd.

- Magna International Inc.

- Denso Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising ADAS Penetration and L2-L3 Autonomy Rollout

- 4.2.2 Shift Toward Centralized and Zonal E/E Architectures

- 4.2.3 OEM Push for Software-Defined Vehicles and OTA Capability

- 4.2.4 Functional-Safety Regulation (ISO 26262, UNECE R155/156)

- 4.2.5 One-Board -> One-Chip Fusion of Cockpit + Driving Domains

- 4.2.6 Emergence of Automotive Chiplet And UCIe Ecosystems

- 4.3 Market Restraints

- 4.3.1 Thermal-Power Limits of High-Compute SoCs

- 4.3.2 Complex ASIL-D Certification Cost/Time

- 4.3.3 Tier-1 Vertical Integration Squeezing Smaller Suppliers

- 4.3.4 Global AI-IP Export Controls Disrupting Supply Chains

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value (USD))

- 5.1 By Application

- 5.1.1 ADAS and Safety

- 5.1.2 Body and Comfort

- 5.1.3 Cockpit Electronics

- 5.1.4 Powertrain

- 5.2 By Vehicle Type

- 5.2.1 Passenger Vehicle

- 5.2.2 Light Commercial Vehicle

- 5.2.3 Medium and Heavy Commercial Vehicle

- 5.3 By Propulsion Type

- 5.3.1 Battery Electric Vehicle

- 5.3.2 Hybrid Electric Vehicle

- 5.3.3 Plug-in Hybrid Vehicle

- 5.3.4 Internal Combustion Engine

- 5.4 By Autonomy

- 5.4.1 Autonomous Vehicle

- 5.4.2 Semi-Autonomous Vehicle

- 5.5 By Operating System

- 5.5.1 QNX

- 5.5.2 Linux

- 5.5.3 Android

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Rest of North America

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 United Kingdom

- 5.6.3.2 Germany

- 5.6.3.3 Spain

- 5.6.3.4 Italy

- 5.6.3.5 France

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 India

- 5.6.4.2 China

- 5.6.4.3 Japan

- 5.6.4.4 South Korea

- 5.6.4.5 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 United Arab Emirates

- 5.6.5.2 Saudi Arabia

- 5.6.5.3 Turkey

- 5.6.5.4 Egypt

- 5.6.5.5 South Africa

- 5.6.5.6 Rest of Middle East and Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 Continental AG

- 6.4.2 Robert Bosch GmbH

- 6.4.3 ZF Friedrichshafen AG

- 6.4.4 Aptiv PLC

- 6.4.5 Valeo SA

- 6.4.6 BlackBerry (QNX)

- 6.4.7 NVIDIA Corporation

- 6.4.8 Qualcomm Technologies Inc.

- 6.4.9 NXP Semiconductors N.V.

- 6.4.10 Renesas Electronics Corporation

- 6.4.11 Infineon Technologies AG

- 6.4.12 Texas Instruments Inc.

- 6.4.13 Visteon Corporation

- 6.4.14 Huawei Technologies Co. Ltd.

- 6.4.15 Magna International Inc.

- 6.4.16 Denso Corporation

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment