|

시장보고서

상품코드

2063265

고속도로 주행 보조 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Highway Driving Assist - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

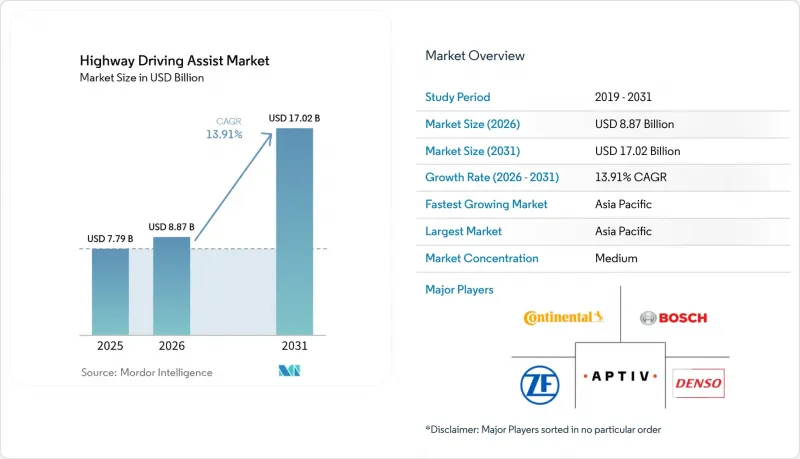

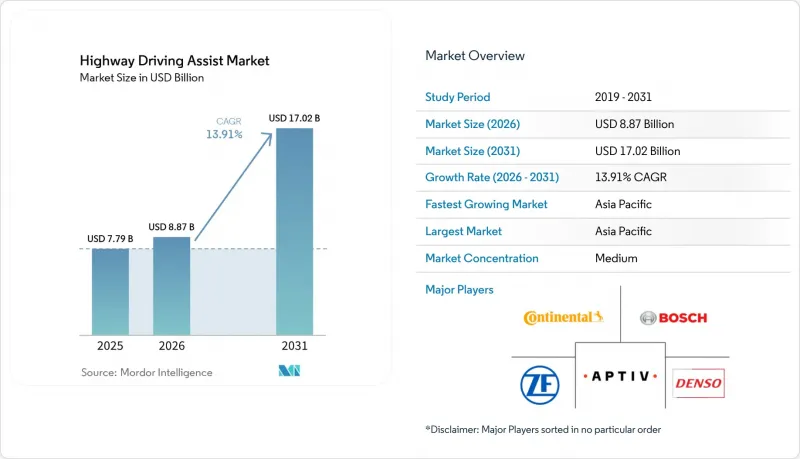

Mordor Intelligence에 의하면, 고속도로 주행 보조 시장 규모는 2025년에 77억 9,000만 달러로 평가되었습니다. 2026년에는 88억 7,000만 달러에 이르고, 2031년까지 170억 2,000만 달러에 이를 것으로 예측되며, 2026년부터 2031년에 걸쳐 CAGR은 13.91%를 나타낼 전망입니다.

본 보고서는 기술별(어댑티브 크루즈 컨트롤, 차선 유지 보조 등), 차종별(승용차, 소형 상용차 등), 구성 요소별(센서, 카메라 시스템, 제어 장치, 소프트웨어, 레이더 시스템 등), 용도별(개인 이용, 차량 관리, 라이드셰어링 서비스 등), 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 고속도로 주행 보조 시장 동향 및 인사이트

규제에 따른 안전 요건 및 NCAP 기준 상향

Euro NCAP은 2025년부터 운전자 지원 시스템에 대한 등급 평가를 시작하며, 사실상 레벨 2+ 기능을 주류 차량 모델에 도입하도록 의무화했습니다. NHTSA의 2024년부터 2033년까지의 로드맵도 비슷한 경로를 따르고 있으며, 기본적인 충돌 회피 기능 목록에 차선 유지 보조 및 어댑티브 크루즈 컨트롤을 추가하고 있습니다. 중국에서는 산업정보화부(MIIT)가 2027년을 목표로 발표한 레벨 3 규정안이 ISO 21434 및 UNECE R155의 요건을 반영하고 있어, 각국의 엔지니어링 부담을 경감시키고 있습니다. UNECE 제29 작업반은 60개 이상의 회원국에서 실시하는 형식 승인을 조화시키기 위해 레벨 3/4 프레임워크를 최종 조정 중입니다. 이러한 조치들이 맞물리면서, 고속도로 주행 보조 기능은 단순한 옵션의 편의성에서 필수적인 규정 준수 항목으로 전환되었으며, 전 세계 밸류체인 전반에 걸쳐 제품 기획 주기가 단축되고 있습니다.

자동차 제조업체의 L2/L2+ 기능 도입

각 제조업체들은 더욱 엄격한 규제가 시행되기 전에 자사 제품 라인 전체에 레벨 2 기능을 보급하기 위해 경쟁하고 있으며, 고속도로 주행 보조 기능은 프리미엄 사양에서 쇼룸의 기본 사양으로 변모하고 있습니다. 선제적으로 도입한 제조업체는 공통 플랫폼 간 소프트웨어 재사용이라는 이점을 누릴 수 있으며, 설계 주기를 처음부터 다시 시작하지 않고도 고급 플래그십 모델에서 대량 생산되는 크로스오버 차량으로 신속하게 전환할 수 있게 됩니다. 구독형 대시보드는 어떤 운전 보조 기능이 가장 높은 참여도를 이끌어내고 있는지 파악하고, 조향 및 차간 거리 제어 동작을 실시간으로 최적화하는 무선 업데이트를 유도합니다. 이러한 피드백 루프는 엔지니어링 우선순위와 소비자 경험 간의 일관성을 높여, 하드웨어 이익률이 하락하는 상황에서도 브랜드가 지속적인 디지털 수익을 확보하는 데 도움이 됩니다. 이와 동시에, 표준화된 기능 세트는 보험사에 일관된 텔레메트리 데이터를 제공하고, 할인 제도를 강화함으로써 제조업체 순정 시스템의 도입률을 더욱 촉진할 것입니다.

높은 초기 시스템 비용

센서 가격이 하락하더라도, 중복 연산 처리, 고해상도 지도, 사이버 보안 인증에 드는 총 비용은 차량 가격에 수천 달러가 추가될 가능성이 있어, 신흥 시장에서 합리적인 가격 책정을 어렵게 만들고 있습니다. 엔트리급 차량 구매자들은 편의 사양과 첨단 주행 보조 패키지 중 하나를 선택해야 하는 어려운 기로에 서는 경우가 많으며, 이로 인해 프리미엄 부문을 제외한 다른 부문에서의 보급이 더딘 임베디드니다. 차량 관리자들은 엄격한 영업이익률과 투자 효과를 저울질하며, 보험 할인이나 규제상의 우대 조치로 인해 자본 지출이 상쇄될 때까지 도입을 미루고 있습니다. 자동차 제조업체들은 기본적인 차선 유지 기능을 기본 사양으로 제공하면서, 차선 변경 기능은 유료로 제공하는 모듈식 방식을 시도하고 있지만, 이러한 계층화는 사용자 경험을 단편화시키고 마케팅을 복잡하게 만듭니다. 시스템 총비용이 일반 시장 가격대에 부합할 때까지는 지역별 도입 속도에 차이가 계속 나타날 것입니다.

부문별 분석

2025년 기준, 고속도로 주행 보조 시장의 기술 구성 비율 중 어댑티브 크루즈 컨트롤(ACC)이 38.48%를 차지했습니다. 이러한 보급은 레이더의 대중화와, 종방향 제어를 안전성의 기본 요소로 규정하는 규제 당국의 노력에 기인합니다. 각 공급업체들은 현재 이 기능을 비용 효율이 최적화된 모듈에 탑재하고 있으며, 파워트레인 및 브레이크용 ECU와 원활하게 통합되므로 대중 시장용 플랫폼에서의 통합 장벽이 낮아지고 있습니다. 이 기능이 기본 사양으로 탑재됨에 따라, 자동차 제조업체들은 마케팅의 초점을 단순한 사양에서 운전자 모니터링의 정확성과 견고한 도로 가장자리 감지 기능으로 전환하고 있습니다. 이와 동시에, 첨단 매핑 인터페이스를 통해 지속적인 클라우드 보정이 가능해져, 보급형 모델이라도 진화하는 차선 중앙 기준에 대한 준수를 유지할 수 있게 되었습니다.

자동차 차선 변경 기능은 연평균 성장률(CAGR) 17.62%로 성장하고 있으며, 이는 기술 계층 내에서 가장 빠른 성장 속도입니다. 프리미엄 등급에서는 핸즈프리 추월 및 협력적 합류 로직을 통해 차별화를 꾀하기 위해 이 기능에 의존하고 있습니다. 다중 차선 시나리오에서 횡방향 자율 주행을 검증하는 데 따르는 복잡성 때문에 안전성 주장을 유지하면서 실제 주행 거리를 줄일 수 있는 새로운 시뮬레이션 워크플로가 도입되었습니다. 클라우드 기반 소프트웨어 스택은 엣지 AI의 성숙도가 높아지면, 기본적인 차선 유지에서 예측적인 차선 선택으로의 OTA(Over-the-Air)를 통한 기능 확장도 가능하게 합니다. 그 결과, 기존 기능은 상품화가 진행되는 반면, 구독제 기능을 통해 이익률의 여지가 유지되는 양극화 경향이 나타나고 있습니다.

2025년 고속도로 주행 보조 시장 점유율에서 승용차가 68.15%를 차지했습니다. 이는 대규모 잠재 시장에서 개인 소유가 주류를 이루고 있기 때문입니다. 이 부문에서 고속도로 주행 보조 기술의 보급은 소비자들의 편의성 요구를 반영하는 한편, 위험 점수에 연동된 보험 인센티브의 확대와도 맞물려 진행되고 있습니다. 자동차 제조업체들은 이미 확립된 인포테인먼트 채널을 활용하여, 보다 고도화된 운전 지원 모드를 활성화하는 월정액 구독 서비스를 업셀링함으로써, 판매 후에도 장기간에 걸쳐 고객 참여를 유지하고 있습니다. 규제에 따라 신형 모델에 기본 ADAS 탑재가 단계적으로 의무화됨에 따라, 어떤 형태의 운전자 지원 기능에 대한 소비자의 기대도 점차 자리 잡고 있습니다. 이러한 기반이 반자율 주행 기능의 수용 확대를 위한 토대를 마련하고 있습니다.

연평균 성장률(CAGR) 14.45%로 성장하고 있는 중형 및 대형 상용차는 차량 함대의 경제성이 기술 혁신을 얼마나 가속화하는지를 보여주고 있습니다. 고속도로 주행 보조 기능은 장거리 운송 사업자에게 주요 비용 요인인 피로 관련 사고를 줄여주고, 텔레매틱스를 기반으로 한 보험료 할인 혜택을 받을 수 있는 자격을 차량에 부여합니다. 사후 장착이 가능한 센서 포드를 통해 기존 트랙터는 플랫폼을 전면적으로 재설계하지 않고도 차선 유지 기능 및 협업형 크루즈 컨트롤을 탑재할 수 있게 되어 가동 중단 시간을 줄일 수 있습니다. 자율주행 기능 덕분에 법적 안전 기준 범위 내에서 허용되는 운전 시간이 연장됨에 따라, 운전기사 부족으로 인한 압박이 이 기술의 도입을 더욱 촉진하고 있습니다. 그 결과, 각 공급업체들은 일반적인 텔레매틱스 게이트웨이와 통합 가능한 모듈식 키트를 개발하고 있으며, 고속도로 지원 기능은 총 소유 비용(TCO) 계획의 항목 중 하나가 되었습니다.

지역별 분석

아시아태평양은 2025년에 고속도로 주행 보조 시장의 36.98%를 차지했으며, 2031년까지 연평균 성장률(CAGR) 15.09%를 기록하며 가장 빠른 성장세를 보일 전망입니다. 중국 내 도로변 V2X 장치의 보급과 ISO 기준에 따른 사이버 보안 규정 준수를 통해 현지화 부담이 줄어들고, 기능 인증 절차가 신속하게 진행되고 있습니다. 일본은 고령 운전자 지원에 주력하고 있으며, 현지 자동차 제조업체들은 인구 동향의 현실에 부합하도록 운전 인계 알림 기능을 개선하고 있습니다. 한국은 전국적인 5G망을 활용해 고속도로에서의 자율주행 차량 간 협동 주행을 확대하고 있으며, 이는 인프라 구축이 보급의 기반이 됨을 보여주고 있습니다. 인도 등 신흥국에서는 국내 제조업체들이 비용 효율이 최적화된 센서군을 인기 SUV 모델에 탑재함으로써 대중 시장으로의 진출 초기 징후가 나타나고 있습니다.

북미에서는 NHTSA 주도의 규격 조화를 통해 핵심적인 운전 보조 기능이 안전 장비의 주류로 자리 잡고 있습니다. 구독 경제가 전략적 대화를 주도하고 있으며, 주요 자동차 제조업체들은 체험판에서 유료 서비스로의 전환율을 지표로 삼아 가격 체계 최적화를 추진하고 있습니다. 보험사는 차선 중앙 유지 및 운전자 모니터링 텔레메트리 데이터를 검증할 수 있는 차량에 대해 보험료를 인하하고 있으며, 이를 통해 설치율을 높이는 선순환이 이루어지고 있습니다. 캐나다 기준과의 국경을 초월한 조화를 통해 형식 인증에 따른 부담을 최소화함으로써, 북미 통합 차량 사양을 구현할 수 있게 되었습니다. 한편, 애프터마켓에서의 사후 개조가 규제 당국의 승인을 받게 됨에 따라, 구형 차량들이 고속도로 주행 보조 시장의 성장세에 동참할 수 있는 간접적인 경로가 열리고 있습니다.

유럽에서는 신차에 지능형 속도 보조 시스템(ISA) 및 차선 유지 보조 시스템(LKA)의 탑재를 의무화하는 ‘일반 안전 규정(GSR)’에 따라 진전이 나타나고 있습니다. Euro NCAP의 평가 항목이 확대됨에 따라, 제조업체들은 마케팅상의 우위를 확보하기 위해 기준 이상의 성능을 달성하도록 장려받고 있습니다. 지역 내 각 OEM 업체들은 접근이 통제된 도로에서 레벨 3 정체 대응 기능을 시범 도입하고 있습니다. 지오펜싱을 활용하여 규제 허용 범위 내에서 운영하면서, 향후 확장을 위한 이용 데이터를 수집하고 있습니다. 반도체 공급 상황과 관련된 공급망의 긴장은 국내 칩 제조업체들과의 제휴를 촉진하고, 회복탄력성에 대한 논의를 이끌어내고 있습니다. 성장률은 아시아·태평양 지역에 미치지 못하지만, 유럽의 명확한 정책이 회원국 전체에 걸친 꾸준한 확장을 뒷받침하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.22According to Mordor Intelligence, the highway driving assist market size was valued at USD 7.79 billion in 2025, is projected to reach USD 8.87 billion in 2026, and is expected to reach USD 17.02 billion by 2031, growing at a CAGR of 13.91% from 2026 to 2031.

This report is Segmented by Technology (Adaptive Cruise Control, Lane Keeping Assist, and More), Vehicle Type (Passenger Car, Light Commercial Vehicle, and More), Component (Sensors, Camera System, Control Units, Software, and Radar Systems), End-Use (Personal Use, Fleet Management, and Ride-Sharing Service), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Highway Driving Assist Market Trends and Insights

Regulatory Safety Mandates and NCAP Upgrades

Euro NCAP started grading assisted-driving systems in 2025, effectively forcing Level 2+ capability into mainstream vehicle programs. NHTSA's 2024-2033 roadmap follows a similar path by adding Lane Keeping Assist and Adaptive Cruise Control to its baseline crash-avoidance menu. In China, draft Level 3 rules issued by MIIT for 2027 mirror the requirements of ISO 21434 and UNECE R155, reducing country-specific engineering overhead. UNECE Working Party 29 is finalizing Level 3/4 frameworks to harmonize homologation across more than 60 contracting markets. Together, these measures shift highway driving assist from an optional convenience to an essential compliance item, compressing product-planning cycles across the global value chain.

Automaker Roll-out of L2/L2+ Features

Manufacturers are racing to blanket their product lines with Level 2 functionality before stricter rules take effect, turning highway-assist from a premium perk into a showroom staple. Early movers benefit from software reuse across shared platforms, enabling rapid migration from luxury flagships to high-volume crossovers without restarting design cycles from scratch. Subscription dashboards also reveal which driver-assist elements attract the most engagement, guiding over-the-air updates that refine steering and distance-keeping behavior in real time. This feedback loop tightens alignment between engineering priorities and consumer experience, helping brands secure recurring digital revenue as hardware margins erode. In parallel, standardized feature sets provide insurers with consistent telemetry, reinforcing discounts that further stimulate take rates for factory-installed systems.

High Upfront System Cost

Even with cheaper sensors, the complete bill for redundant compute, high-definition maps, and cybersecurity certification can add thousands of dollars to a vehicle, straining affordability in emerging markets. Buyers of entry trims often confront a stark choice between comfort options and advanced assist packages, which tempers penetration outside premium segments. Fleet managers weigh the investment against tight operating margins, delaying adoption until insurance discounts or regulatory credits offset capital outlay. Automakers experiment with modular offerings that keep basic lane-keeping standard while paywalling automated lane change, but this tiering fragments the user experience and complicates marketing. Until total system cost aligns with mass-market price points, rollout speed will remain uneven across regions.

Other drivers and restraints analyzed in the detailed report include:

- Falling Radar and Camera Costs

- Subscription-based HDA Service Revenues

- Cyber-security and OTA Compliance Burden

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Adaptive Cruise Control accounted for 38.48% of the technology slice of the highway driving assist market in 2025. Its ubiquity stems from radar commoditization and regulatory nudges that treat longitudinal control as a baseline safety layer. Suppliers now embed the feature in cost-optimized modules that integrate seamlessly with power-train and braking ECUs, reducing integration friction for mass-market platforms. As the function becomes standard, automakers are shifting their marketing focus away from raw specifications toward driver-monitoring fidelity and robust road-edge detection. In parallel, advanced mapping interfaces allow continuous cloud calibration, keeping even entry vehicles compliant with evolving lane-center standards.

Automated Lane Change is growing at a 17.62% CAGR, the fastest pace within the technology hierarchy. Premium trims rely on the feature to distinguish themselves through hands-free overtaking and cooperative merge logic. The complexity of validating lateral autonomy across multi-lane scenarios has prompted new simulation workflows that cut physical-drive mileage while preserving safety claims. Cloud-deployed software stacks also enable over-the-air expansion from basic lane-keeping to predictive lane selection once edge AI maturity allows. Consequently, a bifurcated pattern is emerging where legacy functions commoditize, while subscription-gated capabilities sustain margin headroom.

Passenger cars accounted for 68.15% of the highway driving assist market share in 2025, owing to the dominance of private ownership in large addressable markets. Highway driving assist adoption in this segment mirrors consumer appetite for convenience, blended with rising insurance incentives tied to risk scores. Automakers leverage established infotainment channels to upsell monthly subscriptions that unlock higher-order assist modes, maintaining engagement well past the initial sale. As regulations progressively require basic ADAS in new models, consumer expectations are also normalizing around some form of hands-on driver support. This baseline sets the stage for increased acceptance of semi-autonomous capabilities.

Medium and heavy commercial vehicles, advancing at a 14.45% CAGR, illustrate how fleet economics can accelerate technology turnover. Highway assist reduces fatigue-related incidents, a major cost factor for long-haul operators, and qualifies assets for telematics-based insurance rebates. Retrofit-ready sensor pods enable existing tractors to gain lane-keeping and cooperative cruise control without a full platform redesign, reducing downtime. Driver-shortage pressures further strengthen the case as automated functions extend allowable operating hours within legal safety envelopes. As a result, suppliers are curating modular kits that integrate with prevalent telematics gateways, turning highway assist into a line item in total-cost-of-ownership planning.

Geography Analysis

Asia-Pacific held 36.98% of the highway driving assist market in 2025 and is set to post the fastest climb at a 15.09% CAGR through 2031. China's rollout of roadside V2X units and its alignment with ISO-based cybersecurity rules reduce localization burdens and unlock rapid feature certification. Japan focuses on elderly-driver assistance, prompting local OEMs to refine takeover alerts that resonate with demographic realities. South Korea scales cooperative cruise on expressways using nationwide 5G coverage, illustrating how infrastructure readiness underpins adoption. Emerging economies such as India see early signs of mass-market penetration as domestic manufacturers integrate cost-optimized sensor suites into popular SUV lines.

North America benefits from NHTSA-driven harmonization that inserts core assist functions into the safety mainstream. Subscription economics dominate strategic dialogues, with major automakers using trial-to-paid conversion metrics to refine pricing ladders. Insurers lower premiums for vehicles that provide verifiable lane-centering and driver-monitoring telemetry, creating a virtuous feedback loop that boosts installation rates. Cross-border alignment with Canadian standards minimizes homologation overhead, enabling unified North American vehicle specifications. Meanwhile, aftermarket retrofits gain regulatory recognition, opening a secondary channel for older vehicle fleets to join the momentum of the highway driving assist market.

Europe advances under the General Safety Regulation, which mandates Intelligent Speed Assistance and Lane Keeping Assist on new vehicle types. Euro NCAP's expanded metrics spur manufacturers to exceed baseline compliance in pursuit of marketing leverage. Regional OEMs pilot Level 3 traffic-jam features on controlled-access roads, using geofencing to stay within regulatory comfort zones while collecting usage data for future expansions. Supply-chain stresses related to semiconductor availability encourage partnerships with domestic chipmakers and foster dialogue on resilience. Although growth trails Asia-Pacific, Europe's policy clarity underpins steady scale-up across member states.

- Robert Bosch

- Continental AG

- Denso Corporation

- ZF Friedrichshafen AG

- Aptiv PLC

- Valeo SA

- Mobileye Global Inc.

- Magna International

- Hyundai Mobis

- Aisin Corporation

- Autoliv Inc.

- Mando Corporation

- Infineon Technologies

- NVIDIA Corporation

- NXP Semiconductors

- Texas Instruments

- Renesas Electronics

- Hitachi Astemo

- Samsung Electronics

- Veoneer

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Regulatory Safety Mandates and NCAP Upgrades

- 4.2.2 Automaker Roll-out of L2/L2+ Features

- 4.2.3 Falling Radar and Camera Costs

- 4.2.4 Subscription-based HDA Service Revenues

- 4.2.5 5G HD-map Crowd-sourcing for Fleets

- 4.2.6 Usage-based-insurance (UBI) Incentives

- 4.3 Market Restraints

- 4.3.1 High Upfront System Cost

- 4.3.2 Cyber-security and OTA Compliance Burden

- 4.3.3 ADAS Talent Shortage Delaying Validation

- 4.3.4 Poor-weather / Lane-quality Performance Gaps

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value (USD))

- 5.1 By Technology

- 5.1.1 Adaptive Cruise Control

- 5.1.2 Lane Keeping Assist

- 5.1.3 Automated Lane Change

- 5.1.4 Traffic Jam Assist

- 5.1.5 Collision Avoidance

- 5.2 By Vehicle Type

- 5.2.1 Passenger Car

- 5.2.2 Light Commercial Vehicle

- 5.2.3 Medium and Heavy Commercial Vehicle

- 5.3 By Component

- 5.3.1 Sensors

- 5.3.2 Camera System

- 5.3.3 Control Units

- 5.3.4 Software

- 5.3.5 Radar Systems

- 5.4 By End-Use

- 5.4.1 Personal Use

- 5.4.2 Fleet Management

- 5.4.3 Ride-Sharing Service

- 5.5 Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Rest of North America

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 Spain

- 5.5.3.4 Italy

- 5.5.3.5 France

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 India

- 5.5.4.2 China

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 Turkey

- 5.5.5.4 Egypt

- 5.5.5.5 South Africa

- 5.5.5.6 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 Robert Bosch

- 6.4.2 Continental AG

- 6.4.3 Denso Corporation

- 6.4.4 ZF Friedrichshafen AG

- 6.4.5 Aptiv PLC

- 6.4.6 Valeo SA

- 6.4.7 Mobileye Global Inc.

- 6.4.8 Magna International

- 6.4.9 Hyundai Mobis

- 6.4.10 Aisin Corporation

- 6.4.11 Autoliv Inc.

- 6.4.12 Mando Corporation

- 6.4.13 Infineon Technologies

- 6.4.14 NVIDIA Corporation

- 6.4.15 NXP Semiconductors

- 6.4.16 Texas Instruments

- 6.4.17 Renesas Electronics

- 6.4.18 Hitachi Astemo

- 6.4.19 Samsung Electronics

- 6.4.20 Veoneer

7 Market Opportunities and Future Outlook

- 7.1 White-space and unmet-need assessment