|

시장보고서

상품코드

2063345

항공기 제조 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2025-2031년)Aviation Manufacturing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2031) |

||||||

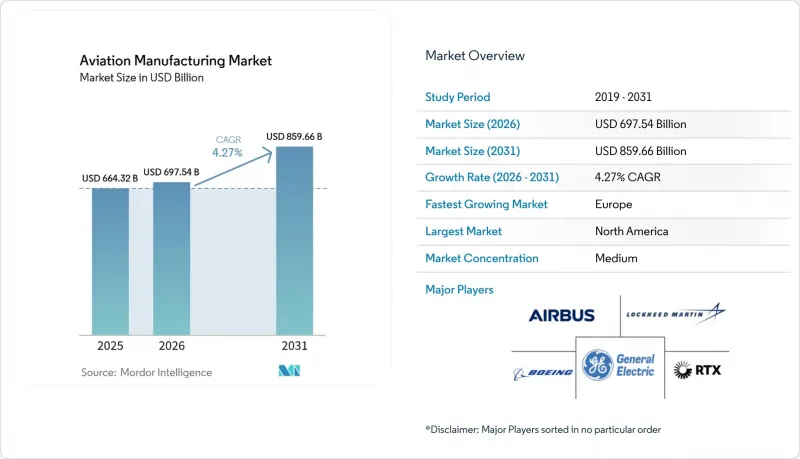

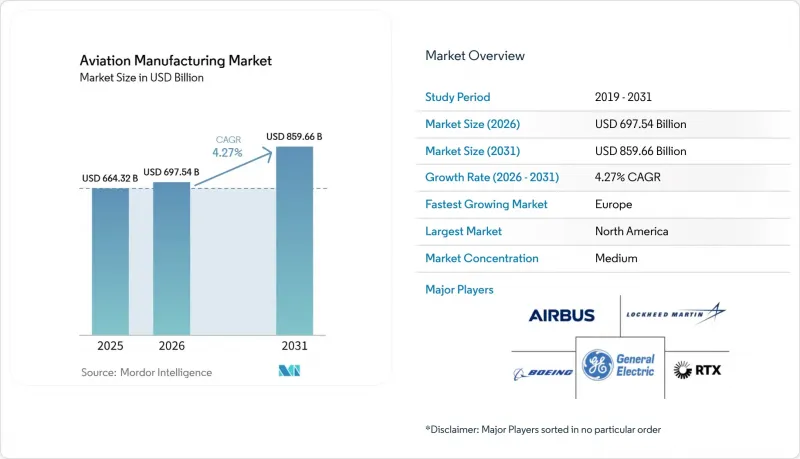

Mordor Intelligence에 의하면, 항공기 제조 시장 규모는 2025년 6,643억 2,000만 달러로 평가되었고, 2026년에는 6,975억 4,000만 달러로 추정되고, 2026-2031년 CAGR 4.27%로 성장을 지속할 전망이며, 2031년까지 8,596억 6,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 항공기 유형별(민간 항공, 군용 항공, 일반 항공), 구성 요소별(기체 구조, 추진 시스템, 아비오닉스 및 비행 제어 시스템, 객실 및 인테리어 모듈 등), 소재별(알루미늄 합금, 탄소섬유 복합재 등), 지역별(북미, 유럽 등)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 항공기 제조 시장 동향 및 인사이트

민간 항공 여행의 회복과 항공기 증강

2024년 12월까지 전 세계 여객 수송량은 2019년 수준의 94.10%까지 회복되었으며, 이에 따라 항공사들은 더욱 엄격해진 배출 규제를 충족하면서도 에너지 비용 리스크를 줄일 수 있는 연비 효율이 뛰어난 신형 제트기로의 기종 교체를 가속화하고 있습니다. 항공사들은 B737 MAX나 A320neo와 같은 협폭기체를 선호하며, 항공기 가동률을 높이고 단위 비용을 절감할 수 있는 고빈도 직항 노선망을 활용하고 있습니다. 저비용 항공사(LCC)는 지방 도시로의 노선 확장을 지속하고 있으며, 수요가 적은 노선에 적합한 100-220석급 항공기에 대한 수요를 더욱 높이고 있습니다. 향후 10년 동안 공급 물량이 부족한 상황이 지속될 것으로 보이며, 이에 따라 주요 제조업체의 가격 결정력은 유지될 것입니다. 이러한 추세가 맞물려 항공기 제조 시장의 단기적인 성장세를 뒷받침하고 있습니다.

국방 분야의 함대 현대화 프로그램

2024 회계연도 미국 예산에서 항공기 조달에 614억 달러가 배정되었습니다. 이는 12% 증가한 수치로, 공군 전력 확충에 대한 초당적인 지지가 지속되고 있음을 보여줍니다. 유럽의 '미래 전투 항공 시스템(FCAS)'과 같은 이니셔티브에서는 80억 유로(93억 6,000만 달러)가 공동 연구 개발에 투입되고 있으며, 스텔스 기술, 센서 융합, 무인기 연계 능력 향상을 통해 플랫폼의 복잡성과 사후 시장 가치를 높이고 있습니다. 아시아태평양의 동맹국들은 변화하는 안보 위협에 대응하기 위해 다목적 전투기와 해상 정찰기 도입을 서두르고 있습니다. 현대화는 신형 기체 도입에 그치지 않고, 기체 수명을 연장하고 Tier 1 및 Tier 2 공급업체의 수익원을 다각화하는 기체 중반기의 아비오닉스, 전자전(EW), 추진 시스템 업그레이드까지 확대되고 있습니다. 방위 분야에 대한 기여는 전략적 완충 역할을 하여, 민간 항공기 경기 침체기에도 항공기 제조 시장을 안정적으로 유지하고 있습니다.

항공우주용 원자재 가격 변동

에너지 부족으로 인한 제련 제약 속에서 2024년 알루미늄 현물 가격은 23% 상승했습니다. 한편, 제재 조치로 인해 러시아산 수출이 중단되면서 티타늄 공급이 부족해졌습니다. 주요 계약업체들은 장기 헤지를 활용하고 있지만, 중소규모의 2차 공급업체들은 이익률 압박에 직면해 있어 통합이나 철수를 피할 수 없는 상황입니다. 각 OEM 업체들은 듀얼 소싱, 스크랩 재활용 루프, 그리고 구조적으로 가능한 부분에 복합 소재를 통합하여 고가의 금속 사용을 줄이는 설계 변경 등의 대책을 통해 이에 대응하고 있습니다. 동적 계약 가격 인상 조항이 점차 표준화되고 있지만, 지속적인 가격 변동은 여전히 항공기 제조 시장의 단기적인 성장을 저해하고 있습니다.

부문별 분석

2025년, 민간 항공은 항공기 제조 시장 점유율 55.38%를 유지했으며, 국제 여행에 불리한 여건이 지속되는 상황에서도 그 우위를 입증했습니다. 각 항공사는 B737 MAX나 A320neo와 같은 협폭기체를 선호하며, 이러한 기종들은 직항 노선에서 높은 가동률을 보이고 있습니다. 한편, 전자상거래의 확대에 따라 화물 수익이 증가하는 가운데, 화물기로의 개조는 사업의 회복탄력성을 높이고 있습니다. 엔진 및 항공기 구조 부품 공급망의 긴장이 월간 생산량을 지속적으로 억제하고 있는 가운데, 보잉은 품질 관리를 강화하고 일정상의 위험을 줄이기 위해 스피릿 에어로시스템즈를 통합했습니다. 각 항공사가 운항 능력의 유연성을 중시하고 있어 와이드바디기 수요는 여전히 부진하지만, 스코프 조항이 완화됨에 따라 대형 리저널 제트기가 간선 노선에 진출할 수 있게 되면서 2차 OEM 제조업체의 생산 규모가 확대되고 있습니다. B737 MAX의 재인증 이후 규제 당국의 감시가 강화되면서 개발 일정은 지연되고 있지만, 더욱 엄격한 검증 절차를 통해 항공사들의 신뢰는 높아지고 있습니다.

동유럽, 인도-태평양, 중동의 지정학적 긴장이 고조되는 가운데, 군사 항공 분야에서는 다목적성을 중시하는 함대 현대화 움직임이 가속화되어 2031년까지 연평균 성장률(CAGR) 6.79%로 확대될 것으로 전망됩니다. 총 사업비가 4,000억 달러를 넘는 F-35와 같은 프로그램은 복합재 구조, 디지털 비행 제어 시스템, 그리고 민간 항공기에서 유래한 저연비 엔진을 스텔스 기술 및 전자전 용도로 응용함으로써 공군 전술의 개념을 재정의하고 있습니다. '미래 전투 항공 시스템(FCAS)'을 비롯한 국제 협력을 통해 연구 개발 부담이 분산되고, 파트너 각국의 국내 산업 참여가 정착되고 있습니다. 급유기 및 수송기를 포함한 비전투 자산의 경우, 병참의 회복탄력성이 전략적 우선순위로 부상함에 따라 꾸준한 조달이 진행되고 있습니다. 동시에, 수출 신용 지원을 통해 주요 계약업체들은 국내에서의 성공을 해외 군사 판매로 이어갈 수 있게 됩니다. 민간 제트기 생산량과 방위 분야의 수주 잔고가 가속화됨에 따라, 항공기 유형 부문은 향후 10년 동안 항공기 제조 시장의 성장을 견인할 두 가지 주요 동력이 될 것입니다.

지역별 분석

북미는 2025년 항공기 제조 시장 점유율의 40.82%를 차지한 것으로 평가되었으며, 이는 보잉의 규모, 광범위한 방산 협력사 네트워크, 그리고 탄탄한 MRO(정비·수리·오버홀) 역량을 바탕으로 하고 있습니다. 연방 정부의 수출 신용 제도와 대외 군사 판매 채널이 국제적 확장을 촉진하는 한편, 국내 생산 복귀(리쇼어링)를 뒷받침하는 인센티브가 부품의 현지 조달을 지원하고 있습니다. 캐나다는 경쟁이 치열해졌음에도 불구하고 충성도 높은 고객 기반을 유지하고 있는 봄바르디아의 프로그램을 필두로, 지역 항공기 및 비즈니스 제트기 분야에서 틈새 시장의 강점을 발휘하고 있습니다.

유럽에서는 에어버스가 단일 통로 항공기 조립 라인을 확장하고, EU의 전략적 자립 정책이 연구개발 자금을 국내 공급업체로 유도함에 따라 2031년까지 연평균 성장률(CAGR) 5.92%를 나타낼 것으로 전망됩니다. FCAS(미래 전투 항공 시스템)와 같은 공동 방위 플랫폼은 국경을 초월한 기술 교류를 촉진하고 산업 통합을 심화하고 있습니다. 독일의 엔진 기술, 프랑스의 항공전자 전문 지식, 이탈리아의 항공 구조물 전문성이 결합되어 지역 자급자족 능력을 강화하고 있습니다. 영국은 브렉시트 이후의 규제 차이에 대응하면서 전 세계 공급망을 활용하고 있습니다.

아시아태평양은 가처분 소득 증가, 공항 수용 능력의 확대, 그리고 항공 산업 지원 정부 정책에 힘입어 절대적인 수요 성장 측면에서 가장 역동적인 성장세를 보이고 있습니다. 중국의 국내 네트워크 확장이 좁은 동체 항공기의 대규모 수주를 뒷받침하는 한편, 인도의 항공사들은 막대한 수주 잔고를 확보하고 있어 인도 아대륙은 미래의 조립 거점으로서의 위상을 확립해 가고 있습니다. 일본과 한국은 고부가가치 서브시스템 수출을 유지하고 있으며, 싱가포르는 지역 내 MRO(정비·수리·오버홀) 분야에서의 리더십을 공고히 하고 있습니다. 한편, 중동의 걸프 항공사들은 지리적 요충지라는 입지를 활용해 장거리용 와이드바디 항공기를 도입하는 동시에, 보다 광범위한 항공기 제조 시장 생태계에 임베디드되는 현지 정비 센터에 투자하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.22According to Mordor Intelligence, the aviation manufacturing market size is expected to grow from USD 664.32 billion in 2025 to USD 697.54 billion in 2026 and is forecast to reach USD 859.66 billion by 2031 at a 4.27% CAGR over 2026-2031.

This report is Segmented by Aircraft Type (Commercial Aviation, Military Aviation, and General Aviation), Component (Airframe Structures, Propulsion Systems, Avionics and Flight Control Systems, Cabin and Interior Modules, and More), Material (Aluminum Alloys, Carbon Fiber Composites, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Aviation Manufacturing Market Trends and Insights

Commercial Air Travel Rebound and Fleet Expansion

Global passenger traffic recovered to 94.10% of 2019 levels by December 2024, prompting carriers to accelerate fleet replacement with newer fuel-efficient jets that cut energy cost exposure while meeting stricter emissions caps. Airlines favor narrowbody families such as the B737 MAX and A320neo, using high-frequency point-to-point networks that boost aircraft utilization and compress unit costs. Low-cost carriers (LCCs) continue to extend service into secondary cities, raising incremental demand for 100-220-seat platforms well-suited to thin routes. Delivery slots remain scarce through the decade, preserving pricing power for prime contractors. These dynamics collectively reinforce the aviation manufacturing market's short-term growth trajectory.

Defense Sector Fleet-Modernization Programs

Fiscal 2024 US appropriations allocated USD 61.4 billion to aircraft procurement, a 12% uptick that underscores sustained bipartisan support for air-power readiness. European initiatives such as the Future Combat Air System (FCAS) channel EUR 8 billion (USD 9.36 billion) into collaborative R&D, advancing stealth, sensor fusion, and unmanned teaming capabilities that elevate platform complexity and aftermarket value. Asia-Pacific allies accelerate purchases of multi-role fighters and maritime patrol aircraft to counter evolving security threats. Modernization extends beyond new frames to mid-life avionics, electronic warfare (EW), and propulsion upgrades that lengthen service life and diversify revenue for tier-1 and tier-2 suppliers. The defense contribution provides a strategic buffer, stabilizing the aviation manufacturing market during civil down-cycles.

Volatile Aerospace-Grade Raw-Material Prices

Aluminum spot prices climbed 23% in 2024 amid energy-driven smelting constraints, while titanium supply tightened after sanctions disrupted Russian exports. Prime contractors wield long-term hedges, yet smaller tier-2 vendors face margin compression that forces consolidation or exit. OEMs respond with dual-sourcing, scrap-recycling loops, and design substitutions that cut costly metals by integrating composites where structurally feasible. Dynamic contract escalation clauses have become standard, yet persistent volatility still subtracts near-term growth from the aviation manufacturing market.

Other drivers and restraints analyzed in the detailed report include:

- Additive-Manufacturing Adoption for Structural Parts

- Emerging Market Airline Fleet Growth

- Lengthy Certification and Regulatory Compliance Cycles

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Commercial aviation retained 55.38% of the aviation manufacturing market share in 2025, underscoring its dominance despite lingering international-travel headwinds. Airlines favor narrowbody families such as the B737 MAX and A320neo, which deliver high utilization on point-to-point networks, while cargo conversions add resilience as e-commerce elevates freight yields. Supply-chain tightness around engines and aerostructures continues to cap monthly output, prompting Boeing to integrate Spirit AeroSystems to boost quality control and reduce schedule risk. Widebody demand remains muted because carriers prize capacity flexibility, yet scope-clause relaxations allow larger regional jets to penetrate mainline routes, broadening production runs for secondary OEMs. Heightened regulatory scrutiny after the B737 MAX recertification extends development timelines and strengthens operator confidence through more rigorous validation protocols.

Military aviation is projected to expand at a 6.79% CAGR through 2031 as geopolitical flashpoints in Eastern Europe, the Indo-Pacific, and the Middle East spur fleet-modernization drives that emphasize multi-role versatility Programs such as the F-35, with a lifetime value topping USD 400 billion, channel composite structures, digital flight controls, and fuel-efficient engines from civil platforms into stealth and electronic-warfare applications that redefine air-power doctrine. International cooperation, exemplified by the Future Combat Air System (FCAS), spreads R&D burdens and embeds domestic industrial participation across partner nations. Non-combat assets, including tankers and transports, see steady procurement as logistics resilience becomes a strategic priority. At the same time, export credit support helps prime contractors convert domestic success into foreign military sales. The civil volume of commercial jets and the accelerating defense backlog position the aircraft-type segment as a dual-engine for the aviation manufacturing market growth through the decade.

Geography Analysis

North America commanded 40.82% of the aviation manufacturing market share in 2025, sustained by Boeing's scale, an expansive defense contractor network, and robust MRO capacity. Federal export-credit facilities and foreign-military-sales pipelines elevate international reach, while domestic reshoring incentives support component localization. Canada contributes niche strength in regional aircraft and business jets, led by Bombardier programs that retain loyal customer bases despite competitive stress.

Europe is forecasted to post a 5.92% CAGR through 2031 as Airbus expands single-aisle assembly lines and EU strategic autonomy policies channel R&D funding to indigenous suppliers. Collaborative defense platforms like the FCAS drive cross-border technology exchange and deepen industrial integration. Germany's engine competencies, France's avionics expertise, and Italy's aerostructures specialization collectively reinforce regional self-sufficiency. The UK leverages global supply links while navigating post-Brexit regulatory divergence.

Asia-Pacific registers the most dynamic absolute demand growth, driven by rising disposable incomes, airport capacity additions, and pro-aviation government policies. China's domestic network expansion underpins large narrowbody orders, while India's carriers commit to sizable backlogs, positioning the subcontinent as a future assembly hub. Japan and South Korea sustain high-value subsystem exports, and Singapore consolidates regional MRO leadership. Concurrently, Gulf carriers in the Middle East exploit geographic crossroads positioning, purchasing long-range widebodies and investing in local overhaul centers that feed into the broader aviation manufacturing market ecosystem.

- Airbus SE

- The Boeing Company

- Lockheed Martin Corporation

- RTX Corporation

- General Electric Company

- Rolls-Royce Holdings plc

- Safran SA

- Northrop Grumman Corporation

- Embraer S.A.

- Leonardo S.p.A.

- Bombardier Inc.

- Saab AB

- Mitsubishi Heavy Industries, Ltd.

- Hindustan Aeronautics Ltd.

- Kawasaki Heavy Industries, Ltd.

- AVIC SAC Commercial Aircraft Company Ltd. (Aviation Industry Corporation of China)

- Israel Aerospace Industries Ltd.

- Korea Aerospace Industries, Ltd.

- GKN Aerospace Services Limited (Melrose Industries plc)

- Eaton Corporation plc

- Parker-Hannifin Corporation

- Honeywell International Inc.

- Singapore Technologies Engineering Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Commercial air travel rebound and fleet expansion

- 4.2.2 Sustained demand for fuel-efficient, next-gen aircraft

- 4.2.3 Defense sector fleet-modernization programs

- 4.2.4 Emerging market airline fleet growth

- 4.2.5 Additive manufacturing adoption for structural parts

- 4.2.6 Supply-chain re-shoring incentives in the US/EU

- 4.3 Market Restraints

- 4.3.1 Volatile aerospace-grade raw-material prices

- 4.3.2 Lengthy certification and regulatory compliance cycles

- 4.3.3 Skilled labor shortages in advanced machining

- 4.3.4 Rising cybersecurity compliance costs across digitalized production lines

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Aircraft Type

- 5.1.1 Commercial Aviation

- 5.1.1.1 Narrowbody Aircraft

- 5.1.1.2 Widebody Aircraft

- 5.1.1.3 Regional Jets

- 5.1.2 Military Aviation

- 5.1.2.1 Combat Aircraft

- 5.1.2.2 Non-Combat Aircraft

- 5.1.2.3 Helicopters

- 5.1.3 General Aviation

- 5.1.3.1 Business Jets

- 5.1.3.2 Turboprop Aircraft

- 5.1.3.3 Piston Aircraft

- 5.1.3.4 Helicopters

- 5.1.1 Commercial Aviation

- 5.2 By Component

- 5.2.1 Airframe Structures

- 5.2.2 Propulsion Systems

- 5.2.3 Avionics and Flight Control Systems

- 5.2.4 Cabin and Interior Modules

- 5.2.5 Landing Gear and Actuation

- 5.2.6 Other Components

- 5.3 By Material

- 5.3.1 Aluminum Alloys

- 5.3.2 Carbon Fiber Composites

- 5.3.3 Titanium Alloys

- 5.3.4 High-Strength Steels

- 5.3.5 Other Materials

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 United Kingdom

- 5.4.2.2 France

- 5.4.2.3 Germany

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Russia

- 5.4.2.7 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 Australia

- 5.4.3.6 Singapore

- 5.4.3.7 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Middle East

- 5.4.5.1.1 United Arab Emirates

- 5.4.5.1.2 Saudi Arabia

- 5.4.5.1.3 Israel

- 5.4.5.1.4 Rest of Middle East

- 5.4.5.2 Africa

- 5.4.5.2.1 South Africa

- 5.4.5.2.2 Rest of Africa

- 5.4.5.1 Middle East

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Airbus SE

- 6.4.2 The Boeing Company

- 6.4.3 Lockheed Martin Corporation

- 6.4.4 RTX Corporation

- 6.4.5 General Electric Company

- 6.4.6 Rolls-Royce Holdings plc

- 6.4.7 Safran SA

- 6.4.8 Northrop Grumman Corporation

- 6.4.9 Embraer S.A.

- 6.4.10 Leonardo S.p.A.

- 6.4.11 Bombardier Inc.

- 6.4.12 Saab AB

- 6.4.13 Mitsubishi Heavy Industries, Ltd.

- 6.4.14 Hindustan Aeronautics Ltd.

- 6.4.15 Kawasaki Heavy Industries, Ltd.

- 6.4.16 AVIC SAC Commercial Aircraft Company Ltd. (Aviation Industry Corporation of China)

- 6.4.17 Israel Aerospace Industries Ltd.

- 6.4.18 Korea Aerospace Industries, Ltd.

- 6.4.19 GKN Aerospace Services Limited (Melrose Industries plc)

- 6.4.20 Eaton Corporation plc

- 6.4.21 Parker-Hannifin Corporation

- 6.4.22 Honeywell International Inc.

- 6.4.23 Singapore Technologies Engineering Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment