|

시장보고서

상품코드

2063409

북미의 항공기 제조 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)North America Aviation Manufacturing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

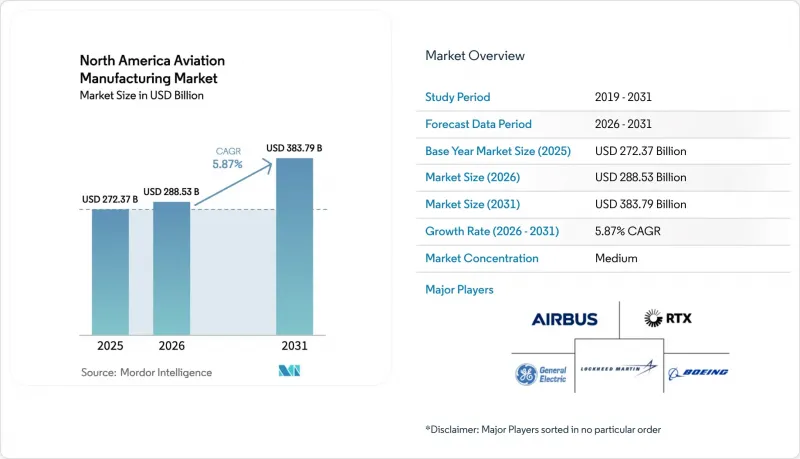

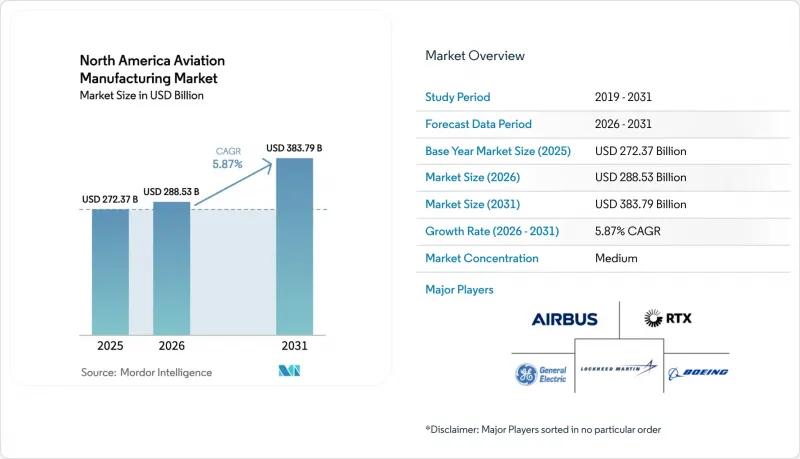

Mordor Intelligence에 의하면, 북미의 항공기 제조 시장 규모는 2025년 2,723억 7,000만 달러로 평가되었고, 2026년에는 2,885억 3,000만 달러로 추정되고, 2026-2031년 CAGR 5.87%로 성장을 지속할 전망이며, 2031년까지 3,837억 3,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 항공기 유형별(민간 항공, 군용 항공, 일반 항공), 구성 요소별(기체 구조, 추진 시스템, 항공 전자 장비 및 비행 제어 시스템 등), 소재별(알루미늄 합금, 탄소섬유 복합재, 티타늄 합금 등), 그리고 지역별(미국, 캐나다, 멕시코)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

북미의 항공기 제조 시장 동향 및 인사이트

여객 수 회복이 공급 능력 확대를 견인

북미의 항공 수요는 해당 지역의 공항과 항공사가 꾸준히 증가하는 승객 수에 맞추어 공급 능력을 조정하고 있어, 수년에 걸쳐 회복세를 보이고 있습니다. 국제공항협의회(ACI)는 2025년에 해당 지역의 여객 수가 21억 명에 달할 것으로 전망하며, 2054년까지의 장기 평균 여객 성장률을 연평균 2.3%로 예상하고 있습니다. 이를 통해 좁은 동체 항공기, 넓은 동체 항공기 및 지역 항공기를 포함한 모든 기종의 신규 항공기에 대한 수요가 유지될 것입니다. OEM 각사의 전망에 따르면, 현재 운용 중인 항공기의 상당 부분이 향후 20년 내에 교체될 것으로 예상되며, 기체 교체 추세가 이러한 수요를 더욱 부추기고 있습니다. 이를 통해 북미 항공기 제조 시장의 여러 프로그램에 걸친 생산 안정성이 뒷받침되고 있습니다. 보잉사는 향후 20년 동안 2만 1,100대의 교체 수요와 2만 2,500대의 신규 수요가 발생할 것으로 전망하고 있으며, 전 세계 항공기 보유 대수는 현재 2만 7,150대에서 2044년까지 4만 9,640대로 증가할 것으로 예측됩니다. 각 항공사는 고객의 기대와 비용 목표를 충족하기 위해 연료 효율성과 객실 업그레이드를 우선시하고 있으며, 이는 차세대 플랫폼에 대한 수주로 이어지고 있습니다. 노선 계획과 항공기 이용률의 지속적인 개선을 통해, 교체 주기를 넘어선 지속적인 수주가 뒷받침되고 있습니다. 공급업체들이 기체 구조, 엔진, 항공전자장비, 내장재 등 각 분야에서 장기 계약을 체결함에 따라, 북미 항공기 제조 시장은 이러한 수요 환경의 혜택을 누리고 있습니다.

초당적 인프라 법안이 대규모 프로젝트를 가속화합니다.

초당적 인프라 법안은 공항 현대화를 위한 다년간의 기반을 마련해 주고 있으며, 이에 따라 북미 항공 제조 시장에서 생산되는 장비 및 시스템에 대한 수요가 증가하고 있습니다. FAA는 2025년 10월에 인프라 보조금의 5차 지급을 실시했으며, 해당 법의 공항 프로그램에 따른 지금까지의 총 보조금 규모는 수십억 달러에 달하며, 활주로, 유도로, 터미널 및 비행장 시스템을 대상으로 하고 있습니다. 이러한 프로그램들은 철강 및 제조 제품의 국내 조달을 중시하며, 북미 공급업체를 우대하고 지역 내 부가가치 창출을 유지하고 있습니다. 보조금 지급 주기에 맞춘 짧은 시행 기간으로 인해 조달 및 설치 일정이 단축되어, 제트브리지, 수하물 시스템, 전원 장치, 조명 제조업체의 공장 가동률이 향상됩니다. 단계적인 자본 계획을 추진하는 공항은 제조업체, 통합업체, 서비스 제공업체에 수년에 걸친 전망을 제시합니다. 프로젝트가 계획 단계에서 건설 단계로 넘어감에 따라, 단기적인 수요 증가 효과는 항공기 측 시설 및 건축 시스템에서 가장 두드러지게 나타나며, 교육, 유지보수용 공구, 인증 지원 분야에도 파급 효과가 발생합니다.

환경 허가와 지역 사회의 반대

허가 취득 기간이 길어지면 자본 프로젝트가 지연되고, 북미 항공기 제조 시장의 안정적인 설비 수요 기반이 되는 생산 능력 확충이 미뤄질 가능성이 있습니다. 2018-2023년 미네소타주에서 보고된 우선 허가 건의 평균 처리 기간은 법정 목표를 크게 상회했으며, 대기 및 수질 관련 허가는 평균 476일이 소요되었고, 일부 신청 건의 경우 1,000일을 초과하기도 했습니다. 심사 기간이 길어지면 추가적인 자금 조달 비용이 발생하고, 프로젝트 단계 변경을 피할 수 없게 될 가능성이 있습니다. 이로 인해 제조업체의 수주 시기나 설치 시기가 변경될 것입니다. 소음 및 지역 사회에 미치는 영향에 대한 지역 사회의 피드백에 따라, 프로젝트 발주자는 설계 및 완화 조치를 조정해야 하며, 이는 시스템이나 자재의 사양 변경으로 이어질 수 있습니다. 초기 단계부터 이해관계자와의 협력을 계획하고 기초 조사를 신속하게 완료하는 프로젝트 후원자는 심사 과정에서 발생하는 수정 작업이나 미비 사항으로 인한 재심사 위험을 줄일 수 있습니다. 승인이 신속하게 이루어짐에 따라 조달 계획의 예측 가능성이 높아지며, 이는 북미 항공기 제조 시장의 모든 공급업체의 공장 일정 및 인력 계획에 있어 매우 중요합니다.

부문별 분석

2025년에는 협폭기 인도 증가와 장거리 노선 회복을 배경으로 민간 항공기가 59.76%를 차지한 것으로 평가되었으며, 북미 항공 제조 시장에서는 기체 구조, 엔진, 항공전자장비, 내장재 등 각 분야에서 안정적인 업무 흐름이 예상됩니다. 이 지역의 항공사들은 신규 도입과 병행하여 기체의 중간 수명 개조 및 객실 개조 주기를 준비하고 있으며, 이를 통해 개조(레트로핏) 및 라인핏(생산 라인에서의 개조) 시장이 활발하게 유지되고 있습니다. 수요 전망은 구형 기종의 지속적인 교체와 총 출발 편수의 꾸준한 증가를 예측하는 장기 전망에 근거하고 있으며, 이는 OEM 및 공급업체에게 향후 수년에 걸친 생산 기반을 뒷받침하고 있습니다. 또한, 기체 개량에 따라 데이터 통신(Data Comm) 및 ADS-B 장비가 표준 사양으로 적용됨에 따라, 항공전자 장비 및 연결성 업그레이드도 진행되고 있으며, 이는 북미 항공 제조 시장에서 조종실 및 통신 장비 공급업체에 대한 추가 발주로 이어지고 있습니다. 와이드바디 항공기는 현재 장거리 노선 수요 회복에 발맞추어 운용 규모가 확대되고 있는 반면, 리저널 제트기나 터보프롭 항공기는 지속적인 접근성과 유연성을 확보하기 위해 수요가 적은 노선이나 피더 네트워크를 주요 대상으로 삼고 있습니다.

군용 항공기 시장은 전투기, 수송기, 회전익기에 대한 다년간의 조달을 통해 생산이 유지될 것으로 예상에 따라, 2031년까지 연평균 성장률(CAGR) 7.98%로 확대될 전망이며, 북미 항공 제조 시장 내 군용 항공기 시장 규모 또한 예측 기간 동안 이 같은 속도로 성장할 것으로 예측됩니다. 록히드 마틴은 2025년에 역대 최다인 191대의 F-35 납품을 확정하고, 생산 로트 18 및 19와 관련된 대규모 추가 계약을 체결했습니다. 이를 통해 공급업체는 기체, 항공전자장비, 자재의 생산량을 예측할 수 있게 되었습니다. 급유기, 수송기 및 ISR(정보·감시·정찰) 플랫폼은 기동 및 감시 임무에 필수적이며, 이들이 임무 특화형 시스템 및 구조물에 대한 수요를 뒷받침하고 있습니다. 또한, 대형 수송기 및 차세대 수직 이착륙기(FVL) 솔루션의 개발이 진행됨에 따라 군용 회전익기도 현대화의 전환점을 맞이하고 있으며, 이에 따라 변속기, 블레이드 및 항공전자 장비에 대한 수요가 지속되고 있습니다. 방위 투자는 북미 항공 제조 시장의 안정적인 생산 기반을 뒷받침하며, 해당 지역의 민간 항공 산업 주기에 대한 경기 변동의 완충 역할을 수행하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.22According to Mordor Intelligence, the north america aviation manufacturing market size is expected to grow from USD 272.37 billion in 2025 to USD 288.53 billion in 2026 and is forecasted to reach USD 383.73 billion by 2031 at a 5.87% CAGR over 2026-2031.

This report is Segmented by Aircraft Type (Commercial Aviation, Military Aviation, and General Aviation), Component (Airframe Structures, Propulsion Systems, Avionics and Flight Control Systems, and More), Material (Aluminum Alloys, Carbon Fiber Composites, Titanium Alloys, and More), and Geography (United States, Canada, Mexico). The Market Forecasts are Provided in Terms of Value (USD).

North America Aviation Manufacturing Market Trends and Insights

Passenger-Traffic Rebound Driving Capacity Expansion

Air travel demand in North America is on a multi-year recovery path as airports and carriers in the region align capacity with steady passenger gains. Airports Council International projected the region to have 2.1 billion passengers in 2025 and forecast long-term average passenger growth of 2.3% annually through 2054, which sustains demand for new aircraft across narrowbody, widebody, and regional fleets. Fleet retirement dynamics enhance this pull, as OEM outlooks indicate a significant share of current aircraft will be replaced over the next 20 years, supporting multi-program production stability in the North America aviation manufacturing market. Boeing projects the need for 21,100 aircraft replacements and 22,500 new aircraft for growth over the next 20 years, with the global fleet expected to increase from 27,150 currently to 49,640 by 2044. Airlines prioritize fuel efficiency and cabin upgrades to meet customer expectations and cost objectives, which channels orders toward next-generation platforms. Continuous improvement in route planning and aircraft utilization supports sustained orders beyond replacement cycles. The North America aviation manufacturing market benefits from this demand environment as suppliers book long-dated contracts across structures, engines, avionics, and interiors.

Bipartisan Infrastructure Law Grants Accelerating Capital Projects

The Bipartisan Infrastructure Law provides a multi-year runway for airport modernization, which lifts demand for equipment and systems produced within the North America aviation manufacturing market. The FAA released a fifth tranche of infrastructure grants in October 2025, bringing total awards under the law's airport programs to date into the billions and targeting runways, taxiways, terminals, and airfield systems. These programs emphasize domestic sourcing of iron, steel, and manufactured products, favoring North American suppliers and keeping value creation in the region. Short execution windows tied to grant cycles compress procurement and installation timelines, which raises factory utilization at manufacturers of jet bridges, baggage systems, power units, and lighting. Airports advancing phased capital plans add multi-year visibility for manufacturers, integrators, and service providers. As projects move from planning to construction, the near-term lift is strongest for airside equipment and building systems, with knock-on benefits for training, maintenance tooling, and certification support.

Environmental Permitting and Community Opposition

Permitting timelines lengthen capital projects and can defer capacity additions that the North America aviation manufacturing market relies on for steady equipment demand. Reported averages for priority permits in Minnesota between 2018 and 2023 extended well beyond statutory targets, with air and water permits taking 476 days on average and some applications exceeding 1,000 days. Extended review cycles introduce additional financing costs and can shift project phasing, altering when manufacturers receive orders and when installation occurs. Community feedback on noise and local impacts requires project sponsors to adapt designs and mitigation plans, potentially changing specifications for systems and materials. Project sponsors who plan early engagement and complete baseline studies more quickly reduce the risk of rework and deficiency cycles during review. Timelier approvals support predictable procurement, which is important for factory scheduling and labor planning across suppliers in the North America aviation manufacturing market.

Other drivers and restraints analyzed in the detailed report include:

- Next-Gen Air-Traffic-Management Investments (ADS-B, SWIM)

- Sustainable-Aviation-Fuel Fueling Infrastructure Rollout

- Construction-Material Supply-Chain Bottlenecks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Commercial aviation accounted for 59.76% in 2025, on the back of rising narrowbody deliveries and a recovery in long-haul routes, and the North America aviation manufacturing market reflects steady workstreams for structures, engines, avionics, and interiors. Airlines in the region prepare for mid-life upgrades and cabin refresh cycles in parallel with new deliveries, which keep retrofit and linefit channels active. Demand visibility is reinforced by long-term forecasts that call for sustained replacement of older aircraft and ongoing growth in total departures, which supports a multi-year production runway for OEMs and suppliers. Fleet modernization also brings avionics and connectivity upgrades as Data Comm and ADS-B equipage become standard baselines, directing incremental orders to cockpit and communications providers in the North America aviation manufacturing market. Widebody platforms now move forward in line with long-haul traffic recovery, while regional jets and turboprops target thin routes and feeder networks for continued accessibility and flexibility.

Military aviation is set to expand at a 7.98% CAGR through 2031 as multi-year procurement sustains output across fighters, transports, and rotorcraft, and the North America aviation manufacturing market size for Military Aviation is projected to expand at this pace over the forecast period. Lockheed Martin confirmed delivery of a record 191 F-35 aircraft in 2025 and finalized a large follow-on contract for production Lots 18 and 19, providing suppliers with volume visibility for airframes, avionics, and materials. Tankers, transports, and ISR platforms remain integral to mobility and surveillance missions, which support demand for missionized systems and structures. Military rotorcraft also advance through modernization milestones as heavy-lift and future vertical lift solutions progress, which sustains demand for transmissions, blades, and avionics. Defense investment underpins a stable baseline of production in the North America aviation manufacturing market and provides a countercyclical buffer to commercial cycles in the region.

List of Companies Covered in this Report:

- Airbus SE

- The Boeing Company

- Lockheed Martin Corporation

- RTX Corporation

- GE Aerospace (General Electric Company)

- Rolls-Royce Holdings plc

- Safran SA

- Leonardo S.p.A.

- Bombardier Inc.

- Mitsubishi Heavy Industries, Ltd.

- Israel Aerospace Industries Ltd.

- GKN Aerospace Services Limited (Melrose Industries plc)

- Eaton Corporation plc

- Parker-Hannifin Corporation

- Honeywell International Inc.

- Singapore Technologies Engineering Ltd.

- Textron Aviation Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Passenger-traffic rebound driving capacity expansion

- 4.2.2 Bipartisan Infrastructure Law grants accelerating capital projects

- 4.2.3 E-commerce-led air-cargo boom boosting freight facilities

- 4.2.4 Electrification readiness for eVTOL and hybrid-electric aircraft

- 4.2.5 Next-gen air-traffic-management investments (ADS-B, SWIM)

- 4.2.6 Sustainable-aviation-fuel (SAF) fueling infrastructure rollout

- 4.3 Market Restraints

- 4.3.1 Budget constraints and cost overruns

- 4.3.2 Environmental permitting and community opposition

- 4.3.3 Construction-material supply-chain bottlenecks

- 4.3.4 Skilled labor shortage in airport construction trades

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Aircraft Type

- 5.1.1 Commercial Aviation

- 5.1.1.1 Narrowbody Aircraft

- 5.1.1.2 Widebody Aircraft

- 5.1.1.3 Regional Jets

- 5.1.2 Military Aviation

- 5.1.2.1 Combat Aircraft

- 5.1.2.2 Non-Combat Aircraft

- 5.1.2.3 Helicopters

- 5.1.3 General Aviation

- 5.1.3.1 Business Jets

- 5.1.3.2 Turboprop Aircraft

- 5.1.3.3 Piston Aircraft

- 5.1.3.4 Helicopters

- 5.1.1 Commercial Aviation

- 5.2 By Component

- 5.2.1 Airframe Structures

- 5.2.2 Propulsion Systems

- 5.2.3 Avionics and Flight Control Systems

- 5.2.4 Cabin and Interior Modules

- 5.2.5 Landing Gear and Actuation

- 5.2.6 Other Components

- 5.3 By Material

- 5.3.1 Aluminum Alloys

- 5.3.2 Carbon Fiber Composites

- 5.3.3 Titanium Alloys

- 5.3.4 High-Strength Steel

- 5.3.5 Other Materials

- 5.4 By Geography

- 5.4.1 United States

- 5.4.2 Canada

- 5.4.3 Mexico

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Airbus SE

- 6.4.2 The Boeing Company

- 6.4.3 Lockheed Martin Corporation

- 6.4.4 RTX Corporation

- 6.4.5 GE Aerospace (General Electric Company)

- 6.4.6 Rolls-Royce Holdings plc

- 6.4.7 Safran SA

- 6.4.8 Leonardo S.p.A.

- 6.4.9 Bombardier Inc.

- 6.4.10 Mitsubishi Heavy Industries, Ltd.

- 6.4.11 Israel Aerospace Industries Ltd.

- 6.4.12 GKN Aerospace Services Limited (Melrose Industries plc)

- 6.4.13 Eaton Corporation plc

- 6.4.14 Parker-Hannifin Corporation

- 6.4.15 Honeywell International Inc.

- 6.4.16 Singapore Technologies Engineering Ltd.

- 6.4.17 Textron Aviation Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment