|

시장보고서

상품코드

2063411

아시아태평양의 항공기 제조 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Asia-Pacific Aviation Manufacturing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

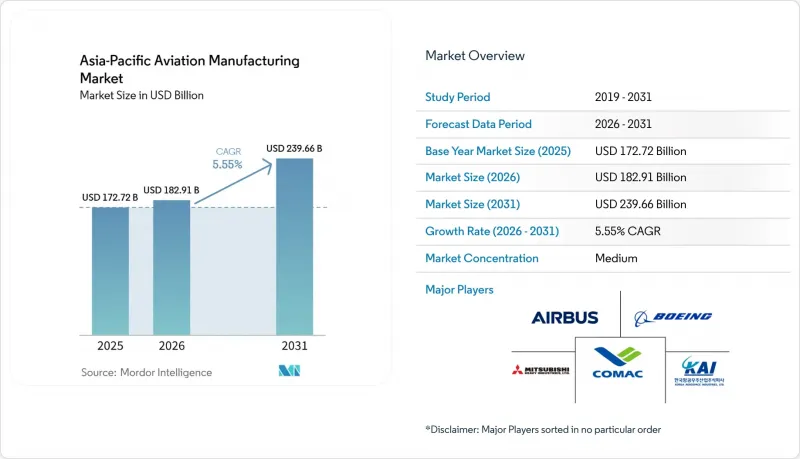

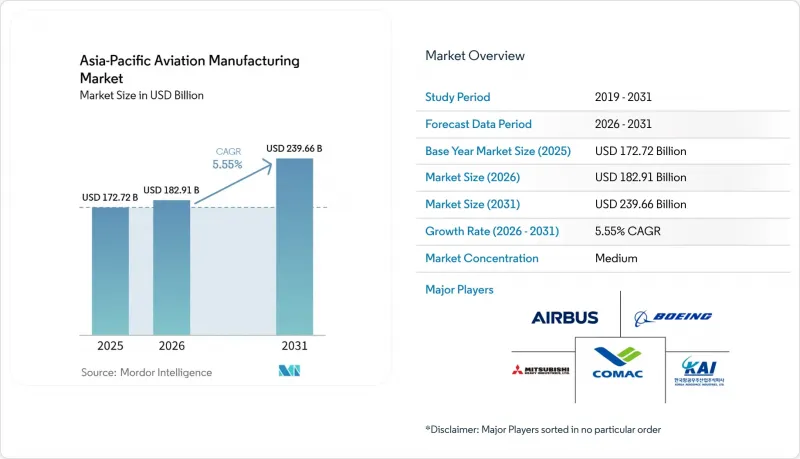

Mordor Intelligence에 의하면, 아시아태평양의 항공기 제조 시장 규모는 2025년 1,727억 2,000만 달러로 평가되었고, 2026년에는 1,829억 1,000만 달러로 추정되고, 2026-2031년 CAGR 5.55%로 성장을 지속할 전망이며, 2031년까지 2,396억 6,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 항공기 유형별(민간 항공, 군용 항공, 일반 항공), 구성 요소별(기체 구조, 추진 시스템, 아비오닉스 및 비행 제어 시스템, 객실 및 내장 모듈 등), 소재별(알루미늄 합금, 탄소섬유 복합재 등), 지역별(중국 등)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

아시아태평양의 항공기 제조 시장 동향 및 인사이트

민간 항공 여행의 회복이 OEM의 미결제 수주량을 끌어올리고 있습니다.

2025년, 아시아태평양 항공사들의 여객 킬로미터 매출은 전년 대비 9.3% 증가하여 세계 다른 지역을 앞질렀으며, 이는 단일 통로 항공기의 꾸준한 생산을 뒷받침하는 결과였습니다. 에어버스는 2024년 766대에 이어 2025년에는 793대를 인도했으며, 각 항공사가 운항 능력을 회복함에 따라 단일 통로 항공기 인도의 대부분이 아시아태평양 항공사를 대상으로 이루어졌습니다. 보잉은 성장과 교체 수요가 모두 뒷받침하는 형태로, 해당 지역에서의 대규모 조달이 지속될 것으로 전망하고 있습니다. 인도의 항공사는 A320neo 시리즈 전체에 대한 인도 물량을 확보한 주요 계약을 바탕으로 수주 잔고를 지속적으로 확대하고 있으며, 이 수주 잔고는 향후 10년에 걸쳐 이어지고 있습니다. 탑승률 회복과 납품 물량 제한이 맞물리면서 미결 주문량이 견조한 추세를 보이고 있으며, 특정 사양에 대한 가격 결정력을 강화하고 있습니다.

아시아태평양 LCC의 협폭기 수주 급증

LCC(저비용 항공사)는 단일 통로 항공기의 경제성을 살려 직항 노선을 빈번하게 운항하는 방식을 우선시함으로써, 남아시아 및 동남아시아 내 여객 수송 구조를 일신했습니다. A320neo 및 B737 MAX 시리즈는 연료 소비량과 좌석당 정비 비용을 절감합니다. 이는 LCC의 가동률 목표와 부합하며, 운항 횟수가 많은 국내선 및 지역 노선의 현금 비용 상황을 개선할 것입니다. 인도 및 동남아시아의 주요 저비용 항공사(LCC)들의 기단 확대는 일일 블록 시간이 늘어남에 따라 랜딩 기어, 브레이크, 항공전자 장비용 예비 부품에 대한 수요도 증가시키고 있습니다. 신형 기종으로 인한 운항 비용 절감과 신뢰성 향상 덕분에 지방 도시 간 연결성이 더욱 현실화되었으며, 공항 인프라가 아직 구축 단계에 있는 상황에서도 추가 발주를 뒷받침하고 있습니다. 조달 속도는 여전히 엔진 공급 상황과 정비 공장의 가동 능력에 좌우되고 있지만, 협폭기(narrow-body)에 대한 구조적인 수요는 아시아태평양의 항공기 제조 시장을 지속적으로 지탱하고 있습니다.

LEAP 및 PW-GTF 엔진의 만성적인 공급 부족

플랫 앤드 휘트니(P&W)사의 PW1100G 엔진에서 발생한 분말 금속 이상과 관련된 점검으로 인해 항공기 운항 중단이 계속되고 있으며, 이로 인해 항공기 가동률이 제한되고 있습니다. 이 회사는 시정 조치의 장기화와 막대한 현금 비용 발생 가능성을 시사하고 있습니다. 각 항공사는 운항 중단으로 인한 손실을 보고하고 있으며, OEM의 지원 패키지에는 현행 점검 체제 하에서의 보상액 및 수리 비용 규모가 반영되어 있습니다. CFM의 LEAP 시리즈 역시 독자적인 생산 능력의 제약과 정비 공장으로의 반입 압박에 직면해 있어, 이로 인해 정비 기간이 계속 길어지고 있으며, 일정을 유지하기 위해서는 더 많은 예비 부품을 확보해야 하는 상황입니다. 이러한 역풍으로 인해 신형 협폭기체의 단기 인도 계획은 정체 상태에 접어들었고, 구형 기체의 퇴역이 지연되면서 지출은 정비 및 부품 수명 연장으로 전환되고 있습니다. 따라서 아시아태평양의 항공기 제조 시장은 단기적인 판매량보다 신뢰성과 애프터마켓 대응을 우선시하는 더욱 까다로운 공급 환경 속에서 성장하고 있습니다.

부문별 분석

2025년 기준으로 민간 항공은 아시아태평양 항공기 제조 시장 규모의 59.76%를 차지했으며, 이는 지역별 제조 일정에 있어 협폭기 프로그램이 차지하는 비중을 반영한 것입니다. 군사 항공 시장은 각국 정부가 장기적인 전력 정비 수요에 부합하는 전투기, 수송기, 회전익기의 조달 체계를 구축하고 있어, 2031년까지 연평균 성장률(CAGR) 7.76%로 확대될 것으로 전망됩니다. 민간 항공 분야에서는 일반적인 장거리 비행과 국내선 및 지역 노선에서의 빈번한 운항이 갖는 경제성 덕분에, 여전히 단일 통로 항공기 프로그램이 핵심을 이루고 있습니다. 광동체 항공기의 비중은 장거리 수요가 광동체 항공기 활용을 뒷받침하는 지역에 집중되어 있으며, 동북아시아의 항공사 및 오세아니아의 운항 사업자들은 대륙 간 노선을 위해 꾸준한 도입을 이어가고 있습니다.

방위 분야의 현대화로 인해 군사 부문의 장기적인 전망이 밝습니다. 이는 플랫폼 업데이트와 기체 수 확대가 수년에 걸쳐 단계적으로 이루어지기 때문입니다. 공군이 다목적 전투기의 교체 및 초계, 수송 임무용 전용기 도입을 추진하는 가운데, 금속, 복합재료, 항공전자기기, 액추에이터 등공급업체들은 플랫폼 간 공통성 덕분에 혜택을 보고 있습니다. 민간 항공 분야에서는 예측 가능한 비행 시간 프로파일과 신형 엔진 옵션을 통한 운항 경제성 향상으로 인해 협폭기(나로우바디)의 우위가 유지되고 있습니다. 아시아태평양의 항공기 제조 업계는 방위 분야의 안정성에 의존하여 민간 분야의 변동을 완화함으로써 이러한 경기 사이클의 균형을 지속적으로 유지하고 있습니다. 한편, 비즈니스 항공 및 일반 항공의 점진적인 성장은 하류 수요에 다양성을 가져오고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.22According to Mordor Intelligence, the asia-Pacific aviation manufacturing market size is expected to grow from USD 172.72 billion in 2025 to USD 182.91 billion in 2026 and is forecast to reach USD 239.66 billion by 2031 at a 5.55% CAGR over 2026-2031.

This report is Segmented by Aircraft Type (Commercial Aviation, Military Aviation, and General Aviation), Component (Airframe Structures, Propulsion Systems, Avionics and Flight Control Systems, Cabin and Interior Modules, and More), Material (Aluminum Alloys, Carbon Fiber Composites, and More), and Geography (China, and More). The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific Aviation Manufacturing Market Trends and Insights

Commercial Air-Travel Rebound Fuels OEM Backlogs

Asia-Pacific carriers posted a 9.3% year-over-year increase in revenue passenger kilometers in 2025, outpacing other global regions and reinforcing the case for steady single-aisle output. Airbus delivered 793 aircraft in 2025 after 766 in 2024, and a significant portion of the single-aisle flow went to Asia-Pacific operators as airlines restored capacity. Boeing projects sustained large-scale procurement in the region, with growth and replacement both supporting demand. India's carriers continue to expand their order books, which stretch into the next decade, building on headline commitments that locked in delivery slots across the A320neo family. The combination of restored load factors and constrained deliveries keeps backlogs firm and strengthens pricing power for selected configurations.

Surge in Asia-Pacific Low-Cost-Carrier Narrowbody Orders

Low-cost carriers have reshaped traffic within South and Southeast Asia by prioritizing high-frequency point-to-point routes that favor single-aisle economics. The A320neo and B737 MAX families deliver lower fuel burn and per-seat maintenance costs, which align with LCC utilization targets and improve cash-cost positions on dense domestic and regional pairs. Expanded fleets at leading LCCs in India and Southeast Asia also elevate demand for landing gear, brakes, and avionics spares as utilization extends daily block hours. Secondary-city connectivity is becoming more viable as new aircraft reduce trip costs and improve reliability, supporting incremental orders even as airport infrastructure is still maturing. Procurement pacing remains tethered to engine availability and shop-visit capacity, while the structural demand for narrowbody aircraft continues to underpin the Asia-Pacific aviation manufacturing market.

Chronic LEAP and PW-GTF Engine Shortages

Pratt & Whitney's PW1100G inspections related to powder-metal anomalies continue to ground aircraft and constrain fleet availability, with the company signaling extended remediation timelines and material cash costs. Airlines have reported losses linked to aircraft-on-ground events, and OEM support packages reflect the magnitude of compensation and repair expense under current inspection regimes. CFM LEAP families face their own throughput constraints and shop-visit pressures, which keep turnaround times elevated and require more spares coverage to maintain schedules. These headwinds cap near-term delivery profiles for new narrowbodies and delay retirement of older fleets, which redistributes spend toward maintenance and component life extensions. The Asia-Pacific aviation manufacturing market, therefore, grows amid tighter supply conditions that prioritize reliability and aftermarket readiness over short-term volume.

Other drivers and restraints analyzed in the detailed report include:

- Government Offsets/Local-Content Mandates

- Regional Push for SAF-Ready Production Lines

- Skilled-Labor Gaps in Composite Lay-Up and Automation

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Commercial aviation accounted for 59.76% of the Asia-Pacific aviation manufacturing market size in 2025, reflecting the weight of narrowbody programs in regional build schedules. Military aviation is projected to expand at 7.76% CAGR to 2031 as governments anchor procurement pipelines for combat aircraft, transports, and rotorcraft that align with long-term readiness needs. Within commercial, single-aisle programs remain the backbone due to typical stage lengths and the economics of high-frequency service across domestic and regional routes. The widebody mix remains concentrated in areas where long-haul demand supports dual-aisle utilization, with Northeast Asian carriers and operators in Oceania maintaining steady intake for intercontinental networks.

Defense modernization gives the military segment durable visibility because platform updates and fleet expansions are sequenced over many years. As air forces refresh multi-role fighters and add missionized aircraft for patrol and lift, suppliers across metals, composites, avionics, and actuation benefit from cross-platform commonality. On the civil side, narrowbody dominance holds given predictable block-hour profiles and improved operating economics of new engine options. The Asia-Pacific aviation manufacturing industry continues to balance these cycles by relying on defense stability to smooth commercial variability, while incremental growth in business and general aviation adds diversity to downstream demand.

List of Companies Covered in this Report:

- Airbus SE

- The Boeing Company

- Commercial Aircraft Corporation of China, Ltd. (COMAC)

- Mitsubishi Heavy Industries, Ltd.

- Hindustan Aeronautics Ltd.

- Korea Aerospace Industries, Ltd.

- Kawasaki Heavy Industries, Ltd.

- AVIC SAC Commercial Aircraft Company Ltd. (Aviation Industry Corporation of China)

- Safran SA

- Singapore Technologies Engineering Ltd.

- TATA Advanced Systems Ltd

- Eaton Corporation plc

- GKN Aerospace Services Limited (Melrose Industries plc)

- Honeywell International Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Commercial air-travel rebound fuels OEM backlogs

- 4.2.2 Surge in Asia-Pacific low-cost-carrier narrowbody orders

- 4.2.3 Government offsets/local-content mandates

- 4.2.4 Regional push for SAF-ready production lines

- 4.2.5 Additive-manufacturing hubs in China, Japan and Australia

- 4.2.6 ASEAN defense modernization accelerating twin-use plants

- 4.3 Market Restraints

- 4.3.1 Chronic LEAP and PW-GTF engine shortages

- 4.3.2 Skilled-labour gaps in composite lay-up and automation

- 4.3.3 Lengthy bilateral certification for COMAC, KAI, HAL types

- 4.3.4 Cyber-security and ITAR compliance cost spike for suppliers

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Aircraft Type

- 5.1.1 Commercial Aviation

- 5.1.1.1 Narrowbody Aircraft

- 5.1.1.2 Widebody Aircraft

- 5.1.1.3 Regional Jets

- 5.1.2 Military Aviation

- 5.1.2.1 Combat Aircraft

- 5.1.2.2 Non-Combat Aircraft

- 5.1.2.3 Helicopters

- 5.1.3 General Aviation

- 5.1.3.1 Business Jets

- 5.1.3.2 Turboprop Aircraft

- 5.1.3.3 Piston Aircraft

- 5.1.3.4 Helicopters

- 5.1.1 Commercial Aviation

- 5.2 By Component

- 5.2.1 Airframe Structures

- 5.2.2 Propulsion Systems

- 5.2.3 Avionics and Flight Control Systems

- 5.2.4 Cabin and Interior Modules

- 5.2.5 Landing Gear and Actuation

- 5.2.6 Other Components

- 5.3 By Material

- 5.3.1 Aluminum Alloys

- 5.3.2 Carbon Fiber Composites

- 5.3.3 Titanium Alloys

- 5.3.4 High-Strength Steels

- 5.3.5 Other Materials

- 5.4 By Geography

- 5.4.1 China

- 5.4.2 India

- 5.4.3 Japan

- 5.4.4 South Korea

- 5.4.5 Australia

- 5.4.6 Singapore

- 5.4.7 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Airbus SE

- 6.4.2 The Boeing Company

- 6.4.3 Commercial Aircraft Corporation of China, Ltd. (COMAC)

- 6.4.4 Mitsubishi Heavy Industries, Ltd.

- 6.4.5 Hindustan Aeronautics Ltd.

- 6.4.6 Korea Aerospace Industries, Ltd.

- 6.4.7 Kawasaki Heavy Industries, Ltd.

- 6.4.8 AVIC SAC Commercial Aircraft Company Ltd. (Aviation Industry Corporation of China)

- 6.4.9 Safran SA

- 6.4.10 Singapore Technologies Engineering Ltd.

- 6.4.11 TATA Advanced Systems Ltd

- 6.4.12 Eaton Corporation plc

- 6.4.13 GKN Aerospace Services Limited (Melrose Industries plc)

- 6.4.14 Honeywell International Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment