|

시장보고서

상품코드

2063347

젖소 사료 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Dairy Cattle Feed - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

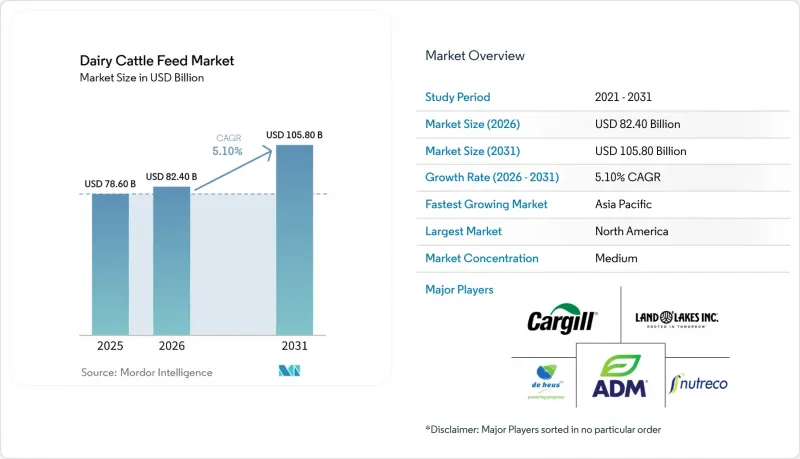

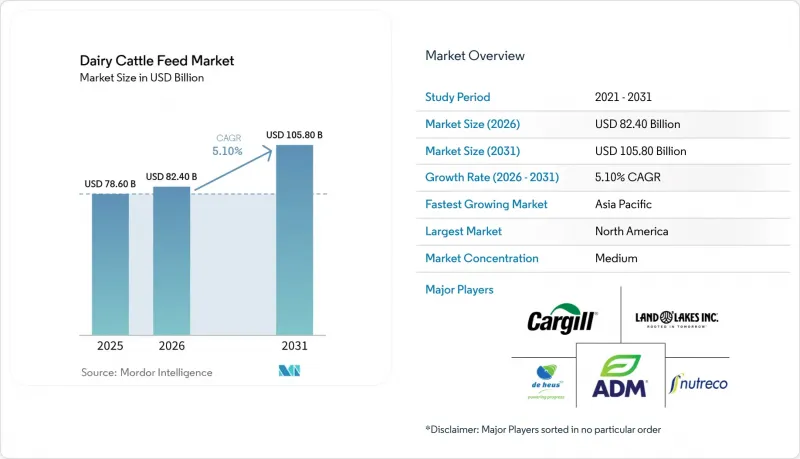

Mordor Intelligence에 의하면, 젖소 사료 시장 규모는 2025년 786억 달러로 평가되었습니다. 2026년에는 824억 달러, 2031년까지 1,058억 달러로 확대되고 2026-2031년 CAGR은 5.1%를 나타낼 전망입니다.

본 보고서는 사료 유형(에너지 사료, 단백질 사료, 미네랄, 비타민, 기타), 형태별(펠렛, 크럼블, 매시, 기타), 원료별(옥수수, 대두박, 밀, 기타), 생애주기 단계별(송아지용 스타터, 비육용 암소, 기타), 지역별(북미, 남미, 유럽, 기타)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 젖소 사료 시장 동향 및 인사이트

신흥국에서의 낙농장 집약화 추세

인도에서 젖소 사육이 확대되면서, 소 무리의 생산성 향상과 체계적인 사료 급여 관행에 힘입어 반추동물용 및 육우용 사료 수요가 증가하고 있습니다. 인도 정부에 따르면, 2024-25년도 우유 생산량은 2억 4,787만 톤으로, 2023-24년도의 2억 3,930만 톤에 비해 3.58% 증가했습니다. 이는 조직형 낙농 시스템의 확대와 사육 규모 확대를 반영한 것입니다. 이러한 성장은 생산성 수준을 유지하기 위해서는 영양 균형이 잡힌 반추동물용 사료가 필요함을 보여줍니다. 낙농장이 사료 관리 방식을 강화한 상업적 운영 방식으로 전환함에 따라, 혼합 소 사료의 사용이 증가할 것으로 예상되며, 이는 젖소 사료 시장의 지속적인 성장을 뒷받침할 것입니다.

정밀 사료 공급 소프트웨어 및 IoT 사료 센서 도입

미국 국립보건원(NIH)의 연구에 따르면, 낙농장의 확대와 사육 규모 증가로 인해 가축 모니터링이 복잡해지고 있으며, 그 결과 건강, 복지, 생산성과 관련된 문제가 발생하고 있습니다. 이 연구에서는 정밀 축산(PLF)이 센서를 활용해 개별 가축을 실시간으로 모니터링함으로써, 소 무리 관리의 개선과 생산성 최적화를 촉진하고 있다는 점을 강조하고 있습니다. 이러한 시스템에는 클라우드 컴퓨팅과 머신러닝을 포함한 IoT 기술이 통합되어 있어, 낙농 경영에서 데이터 기반의 의사 결정을 가능하게 합니다.

사료 원료에 대한 식물 검역상의 수입 장벽 강화

점점 더 엄격해지는 식물 검역 규제로 인해 사료 원료의 세계 무역이 제한되고 있으며, 이는 젖소 사료 시장공급 상황에 중대한 영향을 미치고 있습니다. 미국 농무부의 보고서에 따르면, 유럽연합(EU)이 제안하고 있는 농약 잔류 기준 강화 조치는 연간 54억 달러를 넘는 농산물 수출에 영향을 미칠 가능성이 있습니다. 이러한 규제 조치는 규정 준수 비용을 증가시키고, 수출업체 시장 접근을 제한합니다. 그 결과, 사료 제조업체들은 공급 차질과 가격 문제에 직면해 있으며, 조달처의 다각화와 유연한 조달 방식의 중요성이 부각되고 있습니다.

부문별 분석

2025년에는 에너지 사료가 젖소 사료 시장 점유율의 40%를 차지하며 최대 비중을 기록했으나, 2026년부터 2031년에 걸쳐서는 기능성 첨가제 시장이 연평균 성장률(CAGR) 8.9%로 가장 빠르게 확대되고 있습니다. 생산자들은 3-니트로옥시프로판올에 대한 관심을 높이고 있는데, 이는 이 첨가제에 대한 투자가 탄소 크레딧이나 메탄 관련 유제품 과세 감면을 통해 상쇄될 수 있기 때문입니다. 에너지 사료는 규모 면에서 여전히 젖소 사료 시장을 독점하고 있지만, 사료 제조업체들이 프로바이오틱스, 생효모, 보호 아미노산에 예산을 할당함에 따라 그 점유율은 서서히 감소하고 있습니다. 루멘(반추위)의 미생물군집 조절에 초점을 맞춘 스타트업이, 그동안 약용 클램블이 주도해 온 시장에 진출하고 있습니다.

실제 배합 설계에서는 단백질 이용 효율을 높이기 위해 효소나 직접 투여용 미생물 제제가 코팅 메티오닌과 결합되어 있습니다. 규제 당국이 처방전 같은 마케팅 전략을 용인한다면, 기능성 첨가제는 상당한 시장 점유율을 확보할 가능성이 있습니다. 에너지 사료는 여전히 중요한 구성 요소이지만, 옥수수 가격이 수출 가격 수준에 도달할 경우 현지 곡물 제품으로 전환될 것으로 예측됩니다. 이러한 추세는 젖소 사료 시장이 단순한 열량 함량에서 영양 밀도로 전환되고 있음을 보여줍니다.

2025년에는 펠릿이 젖소 사료 시장 점유율에서 46%로 가장 높은 비중을 차지했으나, 2036년부터 2031년에 걸쳐서는 총혼합사료(TMR) 시장 규모가 연평균 성장률(CAGR) 9.7%라는 가장 빠른 속도로 확대되고 있습니다. 사료를 고정밀도로 계량, 혼합, 공급하는 로봇 믹서가 젖소 사료 시장의 발전을 주도하고 있습니다. 대규모 목장에서는 만성적인 인력 부족으로 인한 인력 배치 문제를 해결하기 위해 TMR(토탈 믹스드레이션) 로봇에 대한 의존도가 높아지고 있습니다. 그 결과, 특히 에너지 효율의 향상이 탄소 스코어카드 개선에 기여함에 따라, 우유 구매자들의 관심을 끌고 있는 지역에서 TMR 성분 시장이 확대되고 있습니다.

송아지나 초산우 사료의 경우, 크럼블이나 매시 사료에 대한 수요는 안정적이지만, 그 성장세는 제한적입니다. 한편, 중성 세제 섬유(NDF)나 전분 함량 등의 상세한 데이터를 클라우드 기반 대시보드로 전송하는 첨단 TMR 영양 센서의 도입으로, 사료는 데이터 기반 제품으로 변모하고 있습니다. 물리적 사료 배합과 이에 수반되는 데이터 분석을 모두 제공할 수 있는 사료 공장은 이처럼 진화하는 시장에서 큰 이점을 누릴 수 있는 위치에 있습니다.

지역별 분석

2025년에는 북미가 젖소 사료 시장 점유율의 29%를 차지했습니다. 캘리포니아주, 위스콘신주, 아이다호주, 텍사스주 등은 토탈 믹스드 레이션(TMR) 도입 지원 및 클라우드 기반 분석을 제공하는 지역 밀착형 사료 제조업체들의 지원을 받아 중요한 수요 거점으로 자리 잡고 있습니다. 캐나다의 할당 제도는 우유 거래의 결제를 안정화시켜, 결과적으로 사료 예산의 균형을 도모하고 있습니다. 한편, 멕시코는 미국산 잉여 원자재와의 지리적 근접성을 활용하여 강력한 국경 간 물류 네트워크를 구축하고 있습니다. 2026년 2월에 출범한 아처 다니엘스 미들랜드(ADM)와 올텍(Alltech)의 합작 사업체인 ‘아크라로스(Akralos)’는 해당 지역이 사업 규모 확대와 기술 서비스 통합에 주력하고 있음을 보여줍니다.

아시아태평양 시장은 2026년부터 2031년까지 연평균 성장률(CAGR) 7.4%를 나타낼 것으로 예측되며, 가장 빠르게 성장하는 지역이 될 전망입니다. 콜드체인 인프라 및 유전자형 분석을 지원하는 정부의 이니셔티브에 힘입어 사료의 사양 요건에 대한 수요가 증가하고 있습니다. 이러한 프로그램들은 사료 생산의 효율과 품질을 향상시키고, 지속적으로 발전하는 산업 기준을 준수하기 위한 것입니다. 호주와 일본은 성숙한 시장으로 간주되지만, 지속가능성에 대한 소비자의 기대에 부응하는 사료의 추적 가능성 및 기능성 첨가물에 대한 수요는 여전히 강하며, 이는 투명성과 환경적 책임에 대한 중요성이 높아지고 있음을 반영하고 있습니다.

유럽에서는 낙농 생산의 정체, 엄격한 기후 정책, 식물성 대체품과의 경쟁과 같은 과제에 직면해 있습니다. 탄소 발자국에 대한 고려와 잔류 기준이 원료 선정에 영향을 미치고 있어, 지역산 곡물의 활용과 산림 파괴가 없는 대두에 대한 인증 취득이 촉진되고 있습니다. 폴란드에서 ForFarmers가 최근 펼친 활동에서 알 수 있듯이, 동유럽은 여전히 유망한 확장 지역입니다. 남미는 목초 기반 시스템이 주는 비용 면에서의 이점을 누리고 있지만, 수출 기회를 잡기 위해 사육용 사료의 도입을 확대되고 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.24According to Mordor Intelligence, the dairy cattle feed market size is projected to grow from USD 78.6 billion in 2025 to USD 82.4 billion in 2026 and USD 105.8 billion by 2031, with a CAGR of 5.1% from 2026 to 2031.

This report is Segmented by Feed Type (Energy Feed, Protein Feed, Minerals, Vitamins, and More), by Form (Pellets, Crumbles, Mash, and More), by Ingredient Source (Corn, Soybean Meal, Wheat, and More), by Lifecycle Stage (Calf Starter, Heifer Grower, and More), and by Geography (North America, South America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Dairy Cattle Feed Market Trends and Insights

Growing Intensification of Dairy Farms in Emerging Economies

The growth of dairy cattle farming in India is increasing the demand for ruminant and compound cattle feed, driven by rising herd productivity and structured feeding practices. According to the Government of India, milk production totaled 247.87 million metric tons in 2024-25, a 3.58% increase from 239.30 million metric tons in 2023-24, reflecting the expansion of organized dairy systems and larger herd sizes. This growth underscores the need for nutritionally balanced ruminant feed to maintain productivity levels. As dairy farms transition to commercial operations with enhanced feed management practices, the use of formulated cattle feed is projected to increase, supporting sustained growth in the dairy cattle feed market.

Adoption of Precision-Feeding Software and IoT Ration Sensors

According to a study by the National Institutes of Health, the growth of dairy farms and larger herd sizes have increased the complexity of animal monitoring, resulting in challenges related to health, welfare, and productivity. The study emphasizes that precision livestock farming (PLF) employs sensors to monitor individual animals in real time, facilitating improved herd management and performance optimization. These systems incorporate IoT technologies, including cloud computing and machine learning, to enable data-driven decision-making in dairy operations.

Escalating Phytosanitary Import Barriers on Feed Ingredients

Increasingly stringent phytosanitary regulations are restricting global trade in feed ingredients, significantly affecting the supply availability for the dairy cattle feed market. The United States Department of Agriculture reports that the European Union's proposed stricter pesticide residue limits could impact agricultural exports worth over USD 5.4 billion annually . These regulatory measures raise compliance costs and restrict market access for exporters. Consequently, feed manufacturers encounter supply disruptions and price challenges, emphasizing the importance of diversified sourcing strategies and flexible procurement practices.

Other drivers and restraints analyzed in the detailed report include:

- Surge in Functional Dairy Demand for A2 and Lactose-free Products

- Volatility-Hedging Contracts for Feed Corn and Soybean Meal

- Antibiotic-Use Scrutiny Tightening Medicated-Feed Approvals

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Energy feed led with the largest 40% of the dairy cattle feed market share in 2025, while the functional additives market size is advancing at the fastest 8.9% CAGR from 2026 to 2031. Producers are increasingly focusing on 3-nitrooxypropanol, as an investment in this additive can be offset through carbon credits and reduced methane-related milk levies. While energy feeds continue to dominate the dairy cattle feed market in terms of size, their share is gradually declining as feed mills allocate budgets toward probiotics, live yeast, and protected amino acids. Start-ups focusing on rumen microbiome modulation are entering a space previously dominated by medicated crumbles.

In practical ration formulation, enzymes and direct-fed microbials are combined with coated methionine to enhance protein efficiency. Functional additives could capture a significant market share if regulatory bodies accept prescription-like marketing strategies. Energy feeds will remain a key component, but are projected to shift toward local grain by-products when corn prices reach export-parity levels. This trend underscores the dairy cattle feed market's transition toward nutrient density over simple calorie content.

Pellets held the largest 46% of the dairy cattle feed market share in 2025, whereas the total mixed ration (TMR) market size is expanding at the fastest 9.7% CAGR from 2036 to 2031. Robotic mixers that weigh, blend, and deliver feed with high precision are driving advancements in the dairy cattle feed market. Large herds increasingly rely on Total Mixed Ration (TMR) robots to address staffing challenges caused by persistent labor shortages. As a result, the market for TMR components is expanding, particularly in regions where energy efficiency contributes to improved carbon scorecards, attracting interest from milk buyers.

While demand for crumble and mash feed remains steady in calf and heifer diets, its growth is limited. Conversely, the introduction of advanced TMR nutrient sensors, which transmit detailed data such as Neutral Detergent Fiber (NDF) and starch content to cloud-based dashboards, is transforming feed into a data-driven product. Feed mills capable of providing both the physical feed blend and accompanying data insights are positioned to benefit significantly in this evolving market.

Geography Analysis

North America is projected to account for 29% of the dairy cattle feed market share in 2025. States such as California, Wisconsin, Idaho, and Texas represent significant demand centers, supported by regional mills that provide Total Mixed Ration (TMR) startups and cloud-based analytics. Canada's quota system stabilizes milk payments, which in turn balances feed budgets. Meanwhile, Mexico leverages its proximity to surplus ingredients from the United States, fostering a strong cross-border logistics network. Archer-Daniels-Midland Company (ADM) and Alltech, Inc. Akralos venture, launched in February 2026, highlights the region's focus on scaling operations and integrating technical services.

The Asia-Pacific market is projected to grow at a 7.4% CAGR from 2026 to 2031, making it the fastest-growing region. Government initiatives supporting cold-chain infrastructure and genotyping are increasing the demand for higher feed specification requirements. These programs aim to enhance the efficiency and quality of feed production, ensuring compliance with evolving industry standards. Although Australia and Japan are regarded as mature markets, they maintain a strong demand for feed traceability and functional additives that meet consumer expectations for sustainability, reflecting a growing emphasis on transparency and environmental responsibility.

Europe is navigating challenges such as stagnant milk production, stringent climate policies, and competition from plant-based alternatives. Carbon footprint considerations and residue limits are influencing ingredient choices, encouraging the use of regional grains and deforestation-free soy certifications. Eastern Europe remains a promising area for expansion, as demonstrated by ForFarmers' recent activities in Poland. South America benefits from cost advantages associated with pasture-based systems but is increasingly adopting confinement diets to capture export opportunities.

- Cargill, Incorporated

- Archer-Daniels-Midland Company (ADM)

- Nutreco N.V. (SHV Holdings N.V.)

- Land O'Lakes, Inc.

- De Heus Voeders B.V.

- ForFarmers N.V.

- Lallemand Inc.

- Alltech, Inc.

- Evonik Industries AG

- BASF SE

- DSM-Firmenich AG

- Godrej Agrovet Limited

- Royal Agrifirm Group (Cooperatie Koninklijke Agrifirm U.A.)

- Kent Nutrition Group, Inc. (Kent Corporation)

- Ridley Corporation Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing intensification of dairy farms in emerging economies

- 4.2.2 Adoption of precision-feeding software and IoT ration sensors

- 4.2.3 Surge in functional dairy demand for A2 and lactose-free products

- 4.2.4 Volatility-hedging contracts for feed corn and soybean meal

- 4.2.5 Carbon-credit programs rewarding low-methane dairy herds

- 4.2.6 On-farm insect bioconversion of manure into high-protein feed

- 4.3 Market Restraints

- 4.3.1 Escalating phytosanitary import barriers on feed ingredients

- 4.3.2 Antibiotic-use scrutiny tightening medicated-feed approvals

- 4.3.3 Margin squeeze from alternative milk uptake

- 4.3.4 Smallholder credit limitations in Africa and South Asia

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porters Five Forces Analysis

- 4.6.1 Intensity of Competitive Rivalry

- 4.6.2 Threat of New Entrants

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Bargaining Power of Buyers

- 4.6.5 Threat of Substitutes

5 Market Size and Growth Forecasts (Value)

- 5.1 By Feed Type

- 5.1.1 Energy Feed

- 5.1.2 Protein Feed

- 5.1.3 Minerals

- 5.1.4 Vitamins

- 5.1.5 Functional Additives

- 5.1.6 Others

- 5.2 By Form

- 5.2.1 Pellets

- 5.2.2 Crumbles

- 5.2.3 Mash

- 5.2.4 Total Mixed Ration (TMR)

- 5.2.5 Others

- 5.3 By Ingredient Source

- 5.3.1 Corn

- 5.3.2 Soybean Meal

- 5.3.3 Wheat

- 5.3.4 Alfalfa

- 5.3.5 Others

- 5.4 By Lifecycle Stage

- 5.4.1 Calf Starter

- 5.4.2 Heifer Grower

- 5.4.3 Lactating Cow Ration

- 5.4.4 Dry Cow Ration

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.1.4 Rest of North America

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 France

- 5.5.3.3 Russia

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 United Kingdom

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Australia

- 5.5.4.4 Japan

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Egypt

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Cargill, Incorporated

- 6.4.2 Archer-Daniels-Midland Company (ADM)

- 6.4.3 Nutreco N.V. (SHV Holdings N.V.)

- 6.4.4 Land O'Lakes, Inc.

- 6.4.5 De Heus Voeders B.V.

- 6.4.6 ForFarmers N.V.

- 6.4.7 Lallemand Inc.

- 6.4.8 Alltech, Inc.

- 6.4.9 Evonik Industries AG

- 6.4.10 BASF SE

- 6.4.11 DSM-Firmenich AG

- 6.4.12 Godrej Agrovet Limited

- 6.4.13 Royal Agrifirm Group (Cooperatie Koninklijke Agrifirm U.A.)

- 6.4.14 Kent Nutrition Group, Inc. (Kent Corporation)

- 6.4.15 Ridley Corporation Limited