|

시장보고서

상품코드

2063369

육우 사료 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Beef Cattle Feed - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

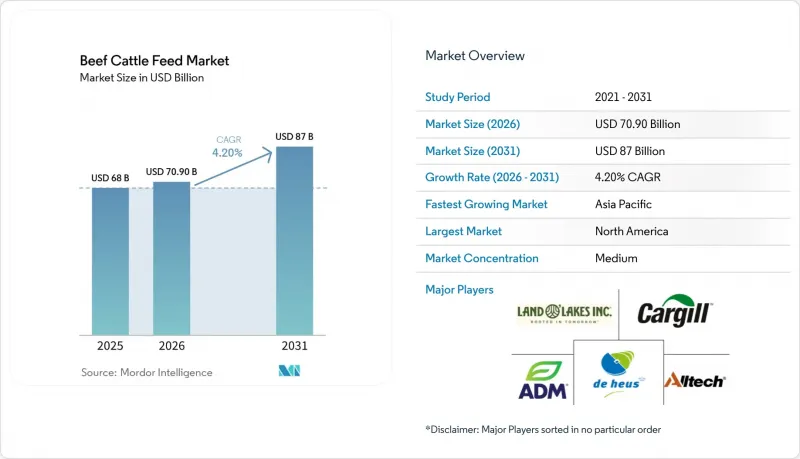

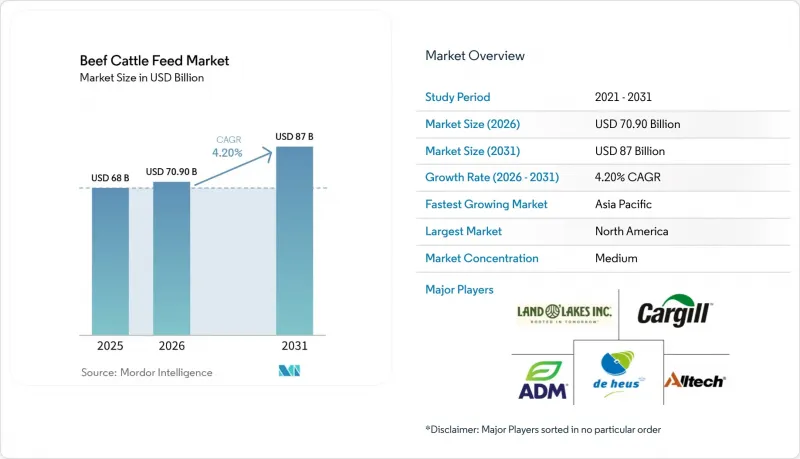

Mordor Intelligence에 의하면, 육우 사료 시장 규모는 2025년 680억 달러로 평가되었습니다. 2026년에는 709억 달러로 확대되어 예측 기간(2026-2031년) CAGR은 4.2%를 나타내, 2031년까지 870억 달러에 이를 것으로 예측됩니다.

본 보고서는 원료별(옥수수, 대두박, 유지종자박, 기타), 형태별(펠렛, 크럼블, 기타), 사료 유형별(완전 사료, 농축 사료, 기타), 기능성 첨가제별(아미노산, 비타민·미네랄, 아미노산, 기타), 지역(북미, 유럽, 아시아태평양, 남미, 기타)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 육우 사료 시장 동향 및 인사이트

고단백 쇠고기에 대한 수요가 상업용 사료의 도입을 촉진하고 있습니다.

소고기 단백질에 대한 전 세계적 수요가 육우 사료 시장의 물량 성장을 계속해서 견인하고 있습니다. OECD-FAO의 예측에 따르면, 전 세계 육류 소비량은 2033년까지 12% 증가할 것으로 추정되며, 소득 증가와 식습관의 변화를 배경으로 남아시아와 동남아시아가 주요 수요 거점으로 부상하고 있습니다. 이러한 수요 증가는 특정 국가들의 사육 두수 증가로 이어질 뿐만 아니라, 생산자들이 더 높은 도축 중량과 더 안정적인 도체 품질을 추구하도록 촉진하고 있습니다. 그 결과, 고에너지 사료의 중요성이 점점 더 커지고 있으며, 육우 사료 시장에서 기존의 저투입형 사료 시스템을 대신해 옥수수, 유지종자박, 생산성 향상 보조제의 사용이 확대되고 있습니다. 이러한 추세는 소 사육 두수가 감소 압력을 받고 있는 지역에서도 두드러지는데, 이는 비육 관리를 강화함으로써 사육 두수의 감소를 상쇄하고 있기 때문입니다. 올텍(Alltech, Inc.)의 보고서에 따르면, 북미와 유럽의 소 사육 두수가 감소하고 있음에도 불구하고, 2024년부터 2025년에 걸쳐 전 세계 육우 사료 취급량은 0.5% 증가했습니다. 이러한 추세는 육우 사료 시장에서 상업용 사료의 도입이 꾸준히 증가하고 있음을 보여주며, 생산성 향상은 단순히 사육 두수의 확대뿐만 아니라 비육 효율과 사료의 품질에 의해 점점 더 주도되고 있음을 시사합니다.

항생제를 사용하지 않은 쇠고기의 프리미엄화가 특수 첨가물 수요를 가속화

항생제 미사용 및 ‘평생 항생제 미사용’ 프로그램은 북미, 유럽, 아시아태평양, 특히 일본의 주요 소매 및 외식 산업 공급망 전반에 걸쳐 표준화되고 있습니다. 이에 따라, 약용 성장 촉진제를 사용하지 않고 장내 환경의 건강과 생산성을 지원하는 프로바이오틱스, 직접 투여용 미생물 제제, 효모 배양물, 유기산, 식물성 첨가물에 대한 수요가 육우 사료 시장에서 증가하고 있습니다. 또한, 바이어들은 추적 가능성, 원료의 특정, 배합의 일관성을 중시하며, 범용 제품보다 특수한 원료를 선호하는 경향이 강해지고 있습니다. 그 결과, 입증된 효능과 확실한 문서화를 갖춘 공급업체가 육우 사료 시장에서 그 중요성이 커지고 있습니다. 예를 들어, 2024년 5월, 올텍(Alltech)사는 메탄 감축용 카본 트러스트(Carbon Trust) 인증 사료 첨가제 ‘아고린 루미난(Agolin Luminan)’의 북미 판매를 시작했습니다. 이 제품은 클린 라벨 축산 프로그램을 지원하며, 생산자와 구매자 모두에게 검증된 지속가능성 관련 주장을 강화하는 것이었습니다. 프리미엄 쇠고기의 판매 채널이 확대됨에 따라, 추적 가능성이 제한적인 범용 첨가제보다 검증된 특수 영양 제품의 중요성이 더욱 커질 것으로 예측됩니다.

옥수수와 대두박의 가격 변동이 사료 마진을 압박하고 있습니다.

원자재 가격 변동은 육우 사료 시장의 수익성에 있어 여전히 큰 과제로 남아 있습니다. 옥수수와 대두박은 비육 사료 비용의 55%에서 65%를 차지하고 있어, 가격이 조금만 상승해도 생산자의 이익률을 압박하고, 고부가가치 영양 제품에 대한 지출을 억제할 가능성이 있습니다. 2026년 3월, 중동의 지정학적 긴장으로 인해 디젤 연료, 전력, 운송 비용이 상승하면서 사료 시장 상황이 더욱 악화되었습니다. 또한, 이 협회는 유럽연합(EU)의 리신 공급량의 95% 이상과 비타민 공급량의 60%에서 70%를 수입에 의존하고 있어, 생산자들은 아시아공급망 혼란에 취약한 입장에 놓여 있다고 지적했습니다. 원가 상승은 이미 전 세계 육류 가격에 영향을 미치고 있습니다. 유엔 식량농업기구(FAO)의 쇠고기 가격 지수는 2025년 10월 사상 최고치를 기록하며, 2024년 1월 수준보다 28% 상승했습니다. 사료 비용이 급등하는 가운데, 육우 사료 시장의 구매자들은 특수 영양 솔루션 도입을 미루고 혼합 사료의 가격 경쟁력을 유지하는 데 주력하는 경우가 많기 때문에 곡물 및 유지종자의 가격 변동은 전 세계적으로 지속적인 수익률에 대한 위험 요인으로 작용하고 있습니다.

부문별 분석

2025년, 옥수수는 육우 사료 시장 규모의 42.5%를 차지했으며, 높은 에너지 밀도와 북미 및 남미의 비육 시스템 전반에 걸친 광범위한 공급 가능성 덕분에 비육용 혼합 사료 시장에서 주도적인 위치를 유지했습니다. 대두박은 기존 유채종자를 통해 영양분을 공급하는 고생산성 비육 프로그램에서 여전히 주요 단백질 공급원으로 자리매김하고 있습니다. 한편, 독일에서 2025년에 실시된 모니터링 결과에 따르면, 유채유 압착 찌꺼기가 대두를 사용하지 않고도 고생산성 소 사료를 완전히 충당할 수 있는 것으로 나타났으며, 이는 유전자 변형 성분 미사용 및 산림 파괴 방지 기준을 준수하는 사료 옵션에 대한 수요를 뒷받침하고 있습니다. 밀과 유지종자 케이크도 여전히 중요한 에너지원 및 단백질원으로 기능하고 있으며, 특히 유지종자 케이크는 저탄소 사료 전략에서 주목을 받고 있습니다.

곤충 단백질 분말 시장은 2031년까지 연평균 성장률(CAGR) 14.2%를 나타낼 것으로 예측되며, 육우 사료 시장에서 가장 빠르게 성장하는 원료 부문이 될 전망입니다. 중국의 2025-2026년 사료 산업 보고서에서는 대두박에 대한 의존도를 낮추기 위해 곤충과 단세포 단백질에 대한 관심이 높아지고 있다는 점이 강조되었습니다. 그러나 그 보급 확대는 여전히 유럽연합(EU), 일본, 한국의 규제 당국의 승인에 달려 있습니다. 요소, 증류박, 농업 제품 등을 포함한 기타 원료는 비용 중심 시장에서 여전히 중요한 위치를 차지하고 있으며, 옥수수가 지배적인 지위를 유지하고 있음에도 불구하고 원료의 조합은 다양화되고 있습니다.

2025년 사료 유형별 시장 점유율에서 육우 사료의 52.0%를 배합사료가 차지했습니다. 이는 대규모 상업용 비육 목장에서 턴키 방식의 사육 솔루션에 대한 수요가 높음을 반영하고 있습니다. 이러한 우위는 대규모 비육 사업에서 노동력을 절감하고 변동성을 낮춤으로써 뒷받침되고 있습니다. 농축 사료는 생산자가 자체 재배한 곡물과 함께 사용하는 비육 전·육성 단계의 시스템에서 계속해서 중요한 역할을 수행하고 있는 반면, 보충제는 특정 영양 관리가 필요한 방목형 및 어미소와 송아지 사육 사업에서 널리 사용되고 있습니다.

프리믹스와 특수 첨가제는 2031년까지 연평균 성장률(CAGR) 6.8%를 기록하며, 육우 사료 시장 전체의 성장률을 상회할 것으로 전망됩니다. 이러한 추세는 배합 사료가 여전히 주류를 이루고 있는 한편, 보다 모듈화되고 맞춤형 영양 시스템으로의 점진적인 전환을 보여주고 있습니다. 대규모 업체들 사이에서 각 단계마다 완제품 사료에 의존하기보다는 고성능 프리믹스 플랫폼을 도입하여 최종 배합을 자체적으로 수립하는 추세가 늘어나고 있습니다. 이러한 접근 방식을 통해 비육 목장은 자사의 곡물을 보다 효율적으로 활용할 수 있을 뿐만 아니라, 육우 사료 시장의 첨가제 및 프리믹스 공급업체에게는 직접 판매 기회가 확대될 것입니다.

지역별 분석

북미는 전 세계 육우 사료 시장을 주도하며, 2025년에는 매출의 33%를 차지해 지역별 최대 점유율을 기록했습니다. 미국은 해당 지역 내 매출의 대부분을 차지하며, 대규모 비육장 시스템과 통합적인 사료 관리를 통해 계속해서 수요의 기반이 되었습니다. 미국 내 비육우 총 도축 두수의 12%에서 15%를 젖소에서 유래한 육우가 차지하고 있으며, 이는 신생 송아지와 비육기에 특화된 영양 프로그램의 필요성을 여실히 보여주고 있습니다. 캐나다는 앨버타주의 비육장 중심의 비육 및 수출 관련 쇠고기 생산 시스템에 힘입어, 해당 지역에서 2위 시장을 유지해 왔습니다. 멕시코 시장은 2025년 스크류웜 문제로 인한 미국 국경 폐쇄 이후, 100만 마리 이상의 보류 소가 국내 사료 수요를 증가시켜 비용 부담을 가중시킨 탓에 공급이 미미했습니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR)이 5.4%를 나타낼 것으로 예측되며, 육우 사료 시장에서 가장 빠르게 성장하는 지역이 될 것으로 전망됩니다. 2025년, 중국은 주요 국가 중 하나였으며, 같은 기간 반추동물용 사료 생산량은 1.8% 증가했습니다. 인도는 브랜드 사료의 채택 확대에 힘입어, 해당 지역에서 가장 빠르게 성장하는 국가 시장이 될 것으로 예측됩니다. 호주 및 뉴질랜드는 수출 지향형 쇠고기 생산 시스템과 첨단 사육 기술의 혜택을 누리고 있지만, 그 규모가 비교적 작기 때문에 지역 전체 매출 성장에 기여하는 정도는 제한적입니다.

튀르키예는 시장 성장의 주요 견인차인 반면, 남아프리카공화국, 사우디아라비아, 이집트는 시판 사료의 도입과 새로운 지역 생산 능력에 대한 투자에 힘입어 빠르게 성장하는 국가별 시장으로 부상하고 있습니다. 유럽의 육우 사료 시장의 성장은 메탄 감축 첨가제의 사용과 동물 복지 기준 강화를 촉진하는 ‘팜 투 포크(Farm to Fork)’ 환경 정책에 힘입고 있습니다. 서유럽 국가들에서는 질소 배출 목표를 달성하기 위해 사료 검사 프로토콜을 정비하고 저단백 사료를 도입하는 움직임이 활발히 진행되고 있습니다. 동유럽은 생산자들이 경영의 현대화를 추진하고 유럽연합(EU)공급망에 통합됨에 따라 계속해서 중요한 성장 지역으로 자리매김하고 있습니다. 한편, 브렉시트 이후 규제 차이로 인해 규정 준수 업무의 복잡성이 커지는 반면, 원료 조달 및 배합 유연성 측면에서의 혁신도 촉진되고 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.24According to Mordor Intelligence, the beef cattle feed market size is projected to increase from USD 68.0 billion in 2025 to USD 70.9 billion in 2026 and is forecast to reach USD 87.0 billion by 2031 at 4.2% CAGR over the forecast period (2026-2031).

This report is Segmented by Ingredient (Corn, Soybean Meal, Oilseed Cakes, and More ), by Form (Pellets, Crumbles, and More), by Feed Type (complete Feed, Concentrates, and More), by Functional Additive (Amino Acids, Vitamins and Minerals, Amino Acids, and More), and by Geography (North America, Europe, Asia-Pacific, South America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Beef Cattle Feed Market Trends and Insights

Protein-Dense Beef Demand Supporting Commercial Feed Adoption

Global demand for beef protein continues to drive volume growth in the beef cattle feed market. According to OECD-FAO projections, global meat consumption is estimated to increase by 12% by 2033, with South and Southeast Asia as key demand centers driven by rising incomes and changing dietary preferences. This growing demand is not only leading to an increase in animal numbers in certain countries but is also encouraging producers to aim for heavier slaughter weights and more consistent carcass performance. As a result, higher-energy rations are becoming increasingly important, boosting the use of corn, oilseed cakes, and performance supplements over traditional low-input forage systems in the beef cattle feed market. This trend is evident even in regions where cattle inventories are under pressure, as intensified finishing practices have compensated for herd reductions. Alltech, Inc. reported that global beef feed tonnage increased by 0.5% from 2024 to 2025, despite declining cattle inventories in North America and Europe. This pattern highlights the resilience of commercial feed adoption in the beef cattle feed market, as production gains are increasingly driven by finishing efficiency and ration quality rather than herd expansion alone.

Antibiotic-Free Beef Premiums Accelerating Specialty Additive Demand

Antibiotic-free and no-antibiotics-ever programs are becoming standard across major retail and foodservice supply chains in North America, Europe, and Asia-Pacific, especially Japan. This has increased demand for probiotics, direct-fed microbials, yeast cultures, organic acids, and phytogenics in the beef cattle feed market that support gut health and performance without medicated growth promoters. Buyers also prioritize traceability, ingredient identity, and formulation consistency, increasing preference for specialty inputs over generic products. As a result, suppliers offering proven efficacy and strong documentation are gaining importance in the beef cattle feed market. For example, in May 2024, Alltech, Inc. began North American distribution of Agolin Ruminant, a Carbon Trust-certified feed additive for methane reduction. The product supported cleaner-label livestock programs and strengthened verified sustainability claims for producers and buyers. As premium beef channels expand, documented specialty nutrition is anticipated to gain further importance over generic additives with limited traceability.

Corn and Soybean Meal Price Volatility Pressuring Feed Margins

Raw material price volatility remains a significant challenge to profitability in the beef cattle feed market. Corn and soybean meal constitute 55% to 65% of finishing ration costs, meaning even slight price increases can erode producer margins and constrain spending on premium nutrition products. In March 2026, the geopolitical tensions in the Middle East led to higher diesel, electricity, and shipping costs, further straining feed economics. Additionally, the association noted that the European Union relies on imports for over 95% of its lysine supply and 60% to 70% of its vitamin supply, leaving producers vulnerable to disruptions in Asian supply chains. Rising input costs are already impacting global meat prices. The Food and Agriculture Organization (FAO) beef price index reached a record high in October 2025, up 28% from January 2024 levels. As feed costs escalate, buyers in the beef cattle feed market often delay adopting specialty nutrition solutions and focus on maintaining ration affordability, making grain and oilseed price volatility a persistent margin risk globally.

Other drivers and restraints analyzed in the detailed report include:

- Methane-Reduction Compliance Increasing Demand for Functional Feed Solutions

- Precision Ration Formulation Improving Feed Efficiency and Weight Gain

- Additive Approval and Antibiotic-Use Restrictions Slowing Product Rollouts

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Corn accounted for 42.5% of the beef cattle feed market size in 2025, maintaining its leading position in finishing rations due to its high energy density and broad availability across North American and South American feedlot systems. Soybean meal remained the primary protein source for high-performance finishing programs using conventional oilseed supplementation. At the same time, Germany's 2025 monitoring results showed that rapeseed extraction meal could fully support high-performance cattle rations without soy, supporting demand for GMO-free and deforestation-compliant feed options. Wheat and oilseed cakes also continue to serve as important energy and protein inputs, with oilseed cakes gaining attention for lower-carbon ration strategies.

Insect protein meal is projected to grow at a 14.2% CAGR through 2031, making it the fastest-growing ingredient segment in the beef cattle feed market. China's 2025-2026 feed industry commentary highlighted an increasing focus on insect and single-cell proteins to reduce dependence on soybean meal. However, wider adoption still depends on regulatory approvals in the European Union, Japan, and South Korea. Other ingredients, including urea, distillers' grains, and agricultural by-products, remain important in cost-sensitive markets, broadening the ingredient mix even as corn retains its dominant position.

Complete feed accounted for 52.0% of the beef cattle feed market share by feed type in 2025, reflecting strong demand for turnkey feeding solutions in large commercial feedlots. Its dominance is driven by lower labor requirements and reduced variability in high-volume finishing operations. Concentrates continue to play an important role in stocker and backgrounding systems, where producers combine them with farm grain, while supplements remain widely used in pasture-based and cow-calf operations that require targeted nutrition.

Premixes and specialty additives are projected to grow at a 6.8% CAGR through 2031, outpacing the overall beef cattle feed market. This trend indicates a gradual shift toward more modular and customized nutrition systems, even as complete feed remains the dominant format. An increasing number of larger operators are acquiring high-performance premix platforms and formulating final rations internally, instead of relying on fully finished feed for every stage. This approach enables feedlots to utilize their own grain more efficiently while expanding direct sales opportunities for additive and premix suppliers in the beef cattle feed market.

Geography Analysis

North America led the global beef cattle feed market, accounting for 33% of revenue in 2025 and the largest share among regions. The United States accounted for significant regional revenue and continued to anchor demand through large feedlot systems and integrated ration management. Beef-on-dairy cattle accounted for 12% to 15% of total United States fed cattle slaughter, underscoring the need for specialized neonatal and finishing nutrition programs. Canada remained the second-largest market in the region, supported by feedlot-intensive finishing in Alberta and export-linked beef production systems. Mexico's market tightened after the 2025 United States border closure related to screwworm, because more than 1 million retained cattle increased domestic feed demand and lifted cost pressure.

Asia-Pacific is projected to be the fastest-growing region in the beef cattle feed market, with a 5.4% CAGR projected through 2031. In 2025, China was a major country, with its ruminant feed output increasing by 1.8% during the historical period. India is anticipated to be the fastest-growing country market in the region, driven by the increasing adoption of branded compound feeds. Australia and New Zealand benefit from export-oriented beef systems and advanced feeding practices; however, their smaller scale limits their overall contribution to regional revenue growth.

Turkey is a major contributor to market growth, while South Africa, Saudi Arabia, and Egypt are emerging as faster-growing country markets, supported by the adoption of commercial feed and investments in new regional production capacities. European growth in the beef cattle feed market is supported by Farm to Fork environmental policies that encourage methane-reducing additives and stronger animal welfare standards. Western European countries are advancing feed-testing protocols and adopting low-protein diets to meet nitrogen-emission targets. Eastern Europe remains a key growth area as producers modernize operations and integrate with European Union supply chains. Meanwhile, post-Brexit regulatory divergence has increased compliance complexity while also encouraging innovation in ingredient sourcing and formulation flexibility.

- Cargill, Incorporated

- Archer Daniels Midland

- Land O'Lakes (Purina Animal Nutrition)

- Alltech Inc

- De Heus Animal Nutrition B.V.

- Nutreco N.V. (SHV Holdings)

- Charoen Pokphand Foods PCL

- ForFarmers N.V.

- Kent Nutrition Group (Kent Corporation)

- Elanco Animal Health Incorporated (Eli Lilly and Company)

- Kalmbach Feeds Inc

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Protein-dense beef demand supporting commercial feed adoption

- 4.2.2 Antibiotic-free beef premiums accelerating specialty additive demand

- 4.2.3 Methane-reduction compliance increasing demand for functional feed solutions

- 4.2.4 Precision ration formulation improving feed efficiency and weight gain

- 4.2.5 Carbon-credit monetization encouraging low-emission feed programs

- 4.2.6 Hindgut and rumen stability needs in high-grain finishing systems

- 4.3 Market Restraints

- 4.3.1 Corn and soybean meal price volatility pressuring feed margins

- 4.3.2 Additive approval and antibiotic-use restrictions slowing product rollouts

- 4.3.3 Cultivated-meat investment affecting long-term beef demand planning

- 4.3.4 Storage and handling variability reducing specialty feed performance

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Bargaining Power of Buyers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value in USD)

- 5.1 By Ingredient

- 5.1.1 Corn

- 5.1.2 Soybean Meal

- 5.1.3 Wheat

- 5.1.4 Oilseed Cakes

- 5.1.5 Insect Protein Meal

- 5.1.6 Others

- 5.2 By Form

- 5.2.1 Pellets

- 5.2.2 Mash

- 5.2.3 Crumbles

- 5.2.4 Liquid Supplements

- 5.3 By Feed Type

- 5.3.1 Complete Feed

- 5.3.2 Concentrates

- 5.3.3 Supplements

- 5.3.4 Premixes and Specialty Additives

- 5.4 By Functional Additive

- 5.4.1 Amino Acids

- 5.4.2 Vitamins and Minerals

- 5.4.3 Probiotics and Yeast

- 5.4.4 Organic Acids and Enzymes

- 5.4.5 Other Functional Additives

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.1.4 Rest of North America

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 France

- 5.5.3.3 United Kingdom

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 Australia

- 5.5.4.5 New Zealand

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 Turkey

- 5.5.5.3 United Arab Emirates

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Egypt

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Overview, Market Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Cargill, Incorporated

- 6.4.2 Archer Daniels Midland

- 6.4.3 Land O'Lakes (Purina Animal Nutrition)

- 6.4.4 Alltech Inc

- 6.4.5 De Heus Animal Nutrition B.V.

- 6.4.6 Nutreco N.V. (SHV Holdings)

- 6.4.7 Charoen Pokphand Foods PCL

- 6.4.8 ForFarmers N.V.

- 6.4.9 Kent Nutrition Group (Kent Corporation)

- 6.4.10 Elanco Animal Health Incorporated (Eli Lilly and Company)

- 6.4.11 Kalmbach Feeds Inc