|

시장보고서

상품코드

2073237

육우용 사료 첨가제 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Beef Cattle Feed Additives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

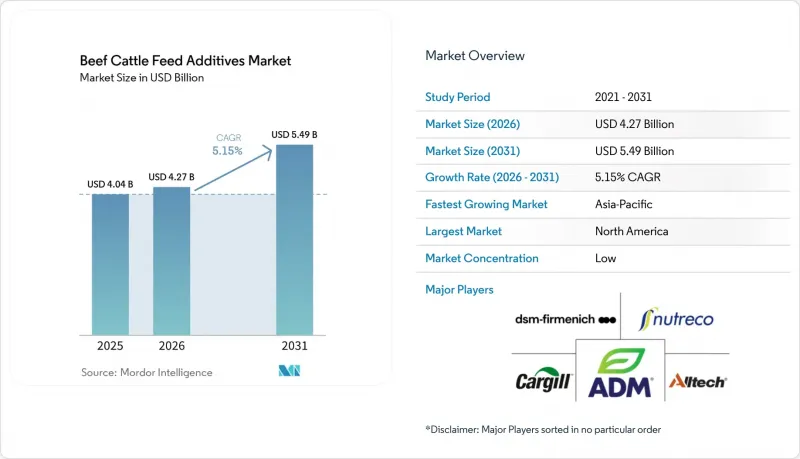

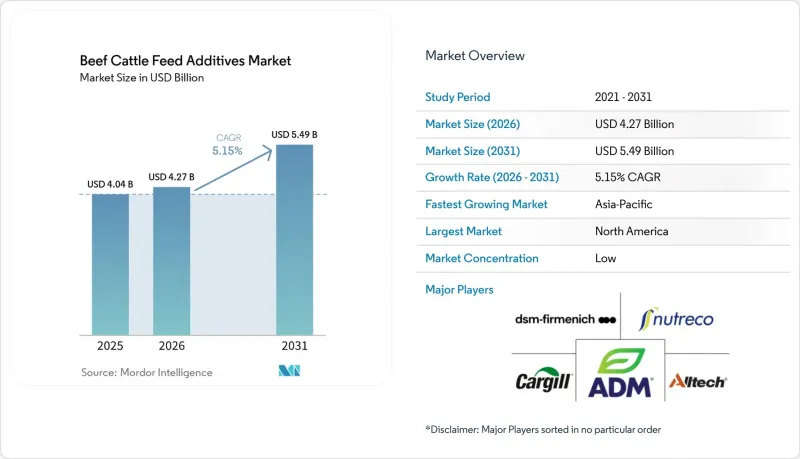

Mordor Intelligence에 의하면, 육우용 사료 첨가제 시장 규모는 2025년 40억 4,000만 달러에서 2026년에는 42억 7,000만 달러로 확대되어 2026년부터 2031년까지 CAGR 5.15%로 성장을 지속하여, 2031년까지 54억 9,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 첨가제의 유형(산미제, 항생제, 항산화제, 아미노산, 결합제, 효소, 향미료 및 감미료, 미네랄, 미코톡신 해독제 등), 형태(건조제 및 액체), 그리고 지역(북미, 남미, 유럽, 아시아태평양, 중동 및 아프리카)별로 분류되어 있습니다. 시장 전망은 금액 및 수량 기준으로 제시되어 있습니다.

세계 육우용 사료 첨가제 시장 동향과 인사이트

사료 전환율과 일일 증체량 향상을 추구하는 상업용 비육장 수요

대규모 비육장 시스템은 그 경제성이 측정 가능한 사료 효율과 체중 증가에 달려 있기 때문에 육우용 사료 첨가제 시장에서 여전히 가장 안정적인 수요 기반을 형성하고 있습니다. 2025년, 세계자원연구소(WRI)는 메탄 저감 사료 첨가제가 상업적으로 가장 발전된 가축 배출 저감 기술 중 하나이며, 평균 약 30%의 메탄 저감 효과를 보이며, 통제된 조건에서는 90% 이상의 저감 효과를 달성하는 기술도 있다고 보고했습니다. 이러한 이용 수준은 주요 집약적 사육 시스템에서 성능 향상을 위한 첨가제가 단순한 선택 사항이 아니라 운영상 필수품으로 취급되고 있음을 보여줍니다. 곡물 가격이 상승하면 사료 전환율이 조금만 개선되어도 경제적 가치가 더욱 뚜렷해지며, 이익률 압박 속에서도 수요의 견조함을 유지하는 데 도움이 됩니다. 이와 같은 논리에 따라, 현재 남미의 집약적 사육 시스템에서도 도입이 확대되고 있으며, 현지 비육 경제성을 바탕으로 고농축 사료 급여 프로그램의 유효성을 검증하는 생산자들이 늘어나고 있습니다.

항생제 계열 성장 촉진제에서 장내 환경 개선용 첨가제로의 전환

규제 대상인 축산 시스템에서 항생제계 성장 촉진제 사용 중단이 진행되고 있는 것이 시장에 긍정적인 영향을 미치고 있습니다. 이러한 변화에 따라 상업적 구매자들은 입식기 및 비육기 동안 사료 섭취량의 안정성과 장 기능을 지원할 수 있는 프로바이오틱스, 프리바이오틱스, 유기산 및 효모 유래 성분으로 관심을 돌리고 있습니다. 실제로는 많은 생산자들이 단순히 한 가지 항생제 제품을 다른 제품으로 대체하고 있는 것은 아닙니다. 대신, 다양한 소화기 계통 및 건강상의 요구를 충족시키기 위해 여러 유형의 첨가제를 결합한 다층적인 프로그램을 도입하고 있습니다. 미국 내 "일반적으로 안전하다고 인정되는(GRAS)" 루트 나 유럽식품안전청(EFSA)의 승인 심사 등 공인된 승인 절차를 거친 제품은 구매자들이 문서화된 규정 준수를 더욱 중요하게 여기기 때문에 시장에서 입지가 강화되고 있습니다. 이러한 선별 효과로 인해 규제 대응 노하우가 풍부한 대형 공급업체들이 우위를 점하게 되었으며, 육우용 사료 첨가제 시장 전체의 평균적인 기술 수준이 향상되고 있습니다.

엄격한 승인 및 잔류 기준 준수에 따른 부담

엄격한 승인 절차로 인해 새로운 생물 유래 제품이나 특수 제품의 상용화가 상당히 지연되고 있습니다. 미국에서는 식품의약국(FDA)이 약용 사료 배합물에 대해 “신규 동물용 의약품 허가 신청(NADA)” 프로세스를 채택하고 있으며, 이 과정이 완료되기까지는 보통 3년에서 5년이 소요됩니다. 유럽연합(EU)에서는 규정(EC) 제1831/2003호에 따라 동물의 건강, 인간의 건강 및 환경에 미치는 영향을 포괄하는 안전성 평가가 의무화되어 있으며, 엄격한 심사 기준이 유지되고 있습니다. 수출 시장은 이 과정을 더욱 복잡하게 만들고 있습니다. 일본, 한국 또는 유럽연합(EU) 등의 지역으로 수출하는 생산자는 가장 엄격한 잔류 기준을 준수해야 하기 때문입니다. 그 결과, 육우용 사료 첨가제 시장에서는 제품 개발 주기가 빠른 기업보다 규제 대응 능력이 탄탄한 기업이 유리한 경향을 보입니다.

부문별 분석

2025년, 아미노산은 육우용 사료 첨가제 시장 점유율의 20.8%를 차지하며 가장 큰 비중을 차지하는 첨가제 유형이 되었습니다. 이 위상은 비육, 육성 및 어미소와 송아지 사육 시스템 전반에 걸쳐, 단백질 효율, 무지방 조직 축적 및 질소 이용의 최적화 측면에서 아미노산이 수행하는 명확한 역할을 반영하고 있습니다. 가장 빠르게 성장하고 있는 첨가제 유형은 항산화제로, 사료의 저장 기간이 길어지고 고에너지 사료 배합으로 인해 산화 위험이 높아짐에 따라, 2026년부터 2031년까지 연평균 성장률(CAGR) 6.7%로 확대될 것으로 예측됩니다. 또한, 육우용 사료 첨가제 시장에서는 수출에 민감한 용도 분야에서 토코페롤이나 구연산 등의 천연 항산화 시스템에 대한 무역상의 선호도가 높아지고 있습니다. 이러한 수요 패턴에 따라 아미노산은 여전히 생산성 향상 프로그램의 핵심을 차지하고 있는 한편, 품질을 중시하는 사료 공급 시스템에서는 항산화제의 사용 확대 속도가 가속화되고 있습니다.

육우용 사료 첨가제 업계 전반에서 프로바이오틱스와 프리바이오틱스는 장내 환경의 안정화가 건강 관리 비용 절감과 밀접한 관련이 있는 도입 및 전환 프로그램에서 더욱 중요한 역할을 담당하고 있습니다. 구매자들이 항생제 투여 후 관리 과정에서 보다 종합적인 소화기 계통 지원을 원하고 있기 때문에 단일 균주 제품보다 다중 균주 제품의 매력이 높아지고 있습니다. 또한, 효모 제품도 틈새 시장의 보조적 역할에서 벗어나, 루멘의 pH 균형과 섬유질 이용률 향상이 요구되는 비육용 사료에 정기적으로 배합되는 등 그 위상을 확대되고 있습니다. 유럽연합 집행위원회는 2025년, Saccharomyces cerevisiae CNCM I-4407을 비육우용 사료 첨가제로 승인했습니다. 이는 규제 시장에서 생효모 시스템의 상업적 입지를 강화하는 것입니다. 육우용 사료 첨가제 시장에서는 여전히 미네랄과 비타민이 기초적인 카테고리로서 중요하지만, 성장의 비중은 사료 배합의 안정성, 장 건강, 그리고 사료 보존 문제를 보다 직접적으로 해결하는 제품으로 점차 이동하고 있습니다.

지역별 분석

2025년, 북미는 육우용 사료 첨가제 시장 점유율의 59.1%를 차지하며 최대 지역 부문이 되었습니다. 이 지역의 위상은 고농축 비육 사료에서 여러 유형의 첨가제가 이미 표준으로 자리 잡은 미국의 비육장 모델이 지닌 기술적 선진성을 반영하고 있습니다. 현재 북미의 육우용 사료 첨가제 시장은 메탄 감축 프로그램, 아미노산의 정밀한 사용, 그리고 질병 발생률 감소 및 도체 품질 향상을 목표로 하는 사육 초기 단계용 장 건강 제품에 대한 수요에 힘입어 성장하고 있습니다. 주요 상업용 시스템에서 핵심적인 성능 향상 첨가제의 도입률이 이미 높은 수준에 이르렀기 때문에 성장률은 다른 성장세가 빠른 지역에 비해 완만한 수준에 그칠 것으로 전망됩니다. 이 지역에서 향후 가치 창출은 단순한 판매량 확대보다는 보다 확실한 실증 데이터를 갖춘 프리미엄 제품을 통해 이루어질 가능성이 높을 것입니다.

남미는 소 사육 두수가 많고, 첨가제 보급률에도 아직 성장 여지가 있어, 육우용 사료 첨가제 시장에서 여전히 성장률이 가장 높은 신흥 지역으로 자리 잡고 있습니다. 2024년부터 2025년까지 브라질의 소 사육 두수는 2억 2,000만 마리를 넘어섰으며, 이는 이 지역의 규모와 장기적인 첨가제 수요 측면에서 차지하는 중요성을 입증했습니다. 성장 잠재력이 가장 높은 곳은 체계적인 사료 공급과 보다 일관된 영양 관리가 필요한 폐쇄형 또는 반집약형 비육 시스템에서 사육되는 소의 수가 증가하고 있는 지역입니다. 2024년, DSM-Firmenich는 브라질 세테 라고아스에 새로운 동물사료 생산 시설을 개장했습니다. 이 시설은 육우 및 젖소를 위한 사료 첨가제를 연간 10만 메트르톤 생산할 수 있는 능력을 갖추고 있으며, 브라질의 반추동물 영양 밸류체인에 대한 업계 투자를 강화하는 동시에, 상업적 육우 시스템 전반에 걸친 향후 첨가제 보급을 뒷받침하고 있습니다. 아르헨티나에서도 수요가 뒷받침되고 있습니다. 이는 구리, 아연, 셀레늄 결핍이 송아지의 생산성을 현저히 저하시킬 가능성이 있는 사육 시스템에서 생산자들이 보다 목표가 명확한 미네랄 보충 프로그램을 채택하고 있기 때문입니다.

유럽은 육우용 사료 첨가제 시장에서 성숙기에 접어든 분야이면서도 여전히 전문성이 높은 분야이며, 수요는 규제 대상인 효모 제품, 식물 유래 성분, 아미노산 및 메탄 관련 솔루션에 집중되어 있습니다. 아시아태평양은 가장 빠르게 성장하는 지역 부문으로, 중국 및 인근 시장의 비육 농장 확대와 규제 현대화에 힘입어 2026년부터 2031년까지 연평균 성장률(CAGR) 5.9%로 성장할 것으로 전망됩니다. 중국에서는 2026년 1월, 육용 비육우용 토탈 믹스드 레이션(TMR) 프로그램에서 구아니디노초산의 승인 용도가 확대되었습니다. 이는 지속적으로 성장하고 있는 상업적 시스템에서 생산성 향상을 위한 첨가제에 대한 공공 지원이 이루어졌음을 보여주는 사례입니다. De Heus Animal Nutrition B.V.는 동남아시아 및 사하라 이남 아프리카 전역에서 사업을 전개하고 있으며, 이들 지역에서는 소 사육 두수 증가와 사료의 현대화에 따라 보다 체계적인 첨가제 프로그램에 대한 초기 단계 수요가 발생하고 있습니다. 중동은 육우용 사료 첨가제 시장에 독특한 기회를 제공합니다. 열 스트레스, 수입 사료에 대한 의존도, 장기간의 저장 주기가 항산화제, 산미제, 미네랄 프리믹스의 안정적인 사용을 촉진하고 있기 때문입니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.07.07According to Mordor Intelligence, the beef cattle feed additives market size is projected to grow from USD 4.04 billion in 2025 to USD 4.27 billion in 2026 and is forecast to reach USD 5.49 billion by 2031 at 5.15% CAGR over 2026-2031.

This report is Segmented by Additive Type (Acidifiers, Antibiotics, Antioxidants, Amino Acids, Binders, Enzymes, Flavors and Sweeteners, Minerals, Mycotoxin Detoxifiers, and More), by Form (Dry and Liquid), and by Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value and Volume.

Global Beef Cattle Feed Additives Market Trends and Insights

Commercial Feedlot Demand for Better Feed Conversion and Daily Gain

Large feedlot systems remain the most stable demand base in the beef cattle feed additives market because their economics depend on measurable feed efficiency and weight gain. In 2025, the World Resources Institute (WRI) reported that methane-inhibiting feed additives are among the most commercially advanced livestock emission-reduction technologies, with average methane reductions of around 30% and some technologies achieving reductions exceeding 90% under controlled conditions. That level of use shows that performance additives in major confinement systems are treated as operating necessities rather than optional inputs. When grain costs rise, the financial value of even modest improvements in feed conversion becomes more apparent, helping keep demand resilient amid margin pressure. The same logic is now strengthening adoption in South American confinement systems, where more producers are validating high-concentrate feeding programs against local finishing economics.

Shift from Antibiotic Growth Promoters to Gut-Health Additives

The market is benefiting from the move away from antibiotic growth promoters in regulated livestock systems. This change is pushing commercial buyers toward probiotics, prebiotics, organic acids, and yeast derivatives that can support intake stability and gut function in receiving and finishing phases. In practice, many producers are not substituting one antibiotic product for another. Instead, they implement layered programs that incorporate multiple additive types to address various digestive and health needs. Products that move through recognized approval pathways, such as the Generally Recognized as Safe (GRAS) route in the United States and authorization reviews under the European Food Safety Authority (EFSA), gain stronger commercial traction because buyers place greater value on documented compliance. That sorting effect favors larger suppliers with regulatory depth and raises the average technical standard across the beef cattle feed additives market.

Tight Approval and Residue-Compliance Burden

The stringent approval processes significantly slow the commercialization of new biological and specialty products. In the United States, the Food and Drug Administration (FDA) employs the New Animal Drug Application (NADA) process for medicated feed combinations, which typically takes 3 to 5 years to complete. In the European Union, Regulation (EC) No 1831/2003 mandates safety evaluations covering animal health, human health, and environmental impact, maintaining a high review standard. Export markets further complicate the process, as producers exporting to regions such as Japan, South Korea, or the European Union must comply with the strictest residue limits. Consequently, the beef cattle feed additives market tends to favor companies with robust regulatory capabilities over those with faster product development cycles.

Other drivers and restraints analyzed in the detailed report include:

- Higher Mycotoxin and Forage Variability in Beef Rations

- Carbon-Insetting Demand for Methane-Reducing Additives

- Limited Grazing-System Fit for Some Methane Inhibitors

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Amino acids accounted for 20.8% of the beef cattle feed additives market share in 2025, making them the largest additive type. Their position reflects a clear role in protein efficiency, lean tissue deposition, and nitrogen use optimization across finishing, growing, and cow-calf systems. The fastest-growing additive type is antioxidants, which are projected to expand at a 6.7% CAGR during 2026-2031 as feed storage periods lengthen and higher-energy rations increase oxidation risk. The beef cattle feed additives market is also seeing stronger trade preference for natural antioxidant systems, such as tocopherols and citric acid, in export-sensitive applications. That demand pattern keeps amino acids central to performance programs while giving antioxidants a faster expansion path in more quality-conscious feeding systems.

Within the broader beef cattle feed additives industry, probiotics and prebiotics are gaining a stronger role in receiving and transition programs, where gut stability is closely tied to health cost control. Multi-strain formats are becoming more attractive than single-strain products because buyers want broader digestive support in post-antibiotic management. Yeast products are also advancing from a niche support role to a more regular inclusion in feedlot diets that need rumen pH balance and stronger fiber utilization. The European Commission authorized Saccharomyces cerevisiae CNCM I-4407 as a feed additive for cattle for fattening in 2025, which supports the commercial standing of live yeast systems in regulated markets. The beef cattle feed additives market still relies on minerals and vitamins as foundational categories, but the growth mix is shifting toward products that solve ration stability, gut health, and feed preservation issues more directly.

Complete Report Scope:

- By Additive

- Acidifiers

- Lactic Acid

- Propionic Acid

- Fumaric Acid

- Other Acidifiers

- Antibiotics

- Tetracyclines

- Penicillins

- Tylosin

- Bacitracin

- Other Antibiotics

- Antioxidants

- Butylated Hydroxyanisole (BHA)

- Butylated Hydroxytoluene (BHT)

- Ethoxyquin

- Propyl Gallate

- Tocopherols

- Citric Acid

- Other Antioxidants

- Amino Acids

- Lysine

- Tryptophan

- Methionine

- Threonine

- Other Amino Acid

- Binders

- Natural Binders

- Synthetic Binders

- Enzymes

- Carbohydrases

- Phytases

- Other Enzymes

- Flavors and Sweeteners

- Flavors

- Sweeteners

- Minerals

- Macrominerals

- Microminerals

- Mycotoxin Detoxifiers

- Binders

- Biotransformers

- Phytogenics

- Herbs & Spices

- Essential Oil

- Other Phytogenics

- Pigments

- Carotenoids

- Curcumin & Spirulina

- Prebiotics

- Inulin

- Fructo Oligosaccharides

- Galacto Oligosaccharides

- Xylo Oligosaccharides

- Lactulose

- Mannan Oligosaccharides

- Other Prebiotics

- Probiotics

- Lactobacilli

- Bifidobacteria

- Streptococcus

- Pediococcus

- Enterococcus

- Other Probiotics

- Vitamins

- Vitamin A

- Vitamin B

- Vitamin C

- Vitamin E

- Other Vitamins

- Yeast

- Live Yeast

- Spent Yeast

- Torula Dried Yeast

- Selenium Yeast

- Whey Yeast

- Yeast Derivatives

- Acidifiers

- By Form

- Dry

- Liquid

- By Geography

- North America

- United States

- Canada

- Mexico

- Rest of North America

- South America

- Brazil

- Argentina

- Chile

- Rest of South America

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- New Zealand

- South Korea

- Indonesia

- Thailand

- Vietnam

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- Turkey

- Iran

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Kenya

- Rest of Africa

- North America

Geography Analysis

North America held 59.1% of the beef cattle feed additives market share in 2025, which made it the largest regional segment. The region's position reflects the technical intensity of the United States feedlot model, where multiple additive classes are already standard in high-concentrate finishing rations. The beef cattle feed additives market in North America is now driven by demand for methane-reduction programs, precision amino acid use, and gut-health products for the receiving phase that address morbidity and carcass-quality goals. Growth will likely stay moderate compared with faster regions because baseline adoption of core performance additives is already high in the most commercial systems. Future value creation in this region is likely to come more from premium products with stronger documentation than from simple volume expansion.

South America remains the highest-growth emerging region in the beef cattle feed additives market, as its cattle base is large and additive penetration still has room to grow. Brazil's cattle herd exceeded 220 million head during the 2024-2025 period, confirming the region's scale and its relevance to long-term additive demand. The growth case is strongest where more cattle are moving through confinement or semi-intensive finishing systems that require structured feeding and more consistent nutritional intervention. In 2024, DSM-Firmenich inaugurated a new animal nutrition facility in Sete Lagoas, Brazil, with the capacity to produce 100,000 metric tons of supplements annually for beef and dairy cattle, reinforcing industry investment in the Brazilian ruminant nutrition value chain and supporting future additive penetration across commercial beef systems. Argentina also supports demand because producers are using more targeted mineral programs in systems where deficiencies in copper, zinc, and selenium can materially reduce calf performance.

Europe remains a mature but specialized part of the beef cattle feed additives market, with demand centered on regulated yeast products, phytogenics, amino acids, and methane-related solutions. Asia-Pacific is the fastest regional segment and is projected to expand at 5.9% CAGR during 2026-2031, supported by feedlot growth and regulatory modernization in China and nearby markets. China expanded the approved use of guanidinoacetic acid for beef fattening cattle in Total Mixed Ration (TMR) programs in January 2026, which shows official support for performance additives in a growing commercial system. De Heus Animal Nutrition B.V. maintains operations across Southeast Asia and Sub-Saharan Africa, where cattle population growth and feed modernization are creating early-stage demand for more formal additive programs. The Middle East presents a distinct opportunity set for the beef cattle feed additives market, as heat stress, reliance on imported feed, and long storage cycles support steady use of antioxidants, acidifiers, and mineral premixes.

- Cargill, Incorporated

- Archer Daniels Midland Company

- Nutreco N.V. (SHV Holdings N.V.)

- DSM-Firmenich AG

- Alltech, Inc.

- Kemin Industries, Inc.

- BASF SE

- Evonik Industries AG

- Elanco Animal Health Incorporated

- Novus International, Inc.

- Bluestar Adisseo Company

- Lallemand Inc.

- Zinpro Corporation

- Land O'Lakes, Inc.

- De Heus Animal Nutrition B.V. (Royal De Heus)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Commercial feedlot demand for better feed conversion and daily gain

- 4.2.2 Shift from antibiotic growth promoters to gut-health additives

- 4.2.3 Higher mycotoxin and forage variability in beef rations

- 4.2.4 Precision mineral and amino acid supplementation adoption

- 4.2.5 Carbon-insetting demand for methane-reducing additives

- 4.2.6 Byproduct-rich rations need more stabilizing additives

- 4.3 Market Restraints

- 4.3.1 Tight approval and residue-compliance burden

- 4.3.2 Volatile input costs for vitamins amino acids and fermentation products

- 4.3.3 Limited grazing-system fit for some methane inhibitors

- 4.3.4 Weak on-farm data capture slows return on investment validation

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Bargaining Power of Buyers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value and Volume)

- 5.1 By Additive

- 5.1.1 Acidifiers

- 5.1.1.1 Lactic Acid

- 5.1.1.2 Propionic Acid

- 5.1.1.3 Fumaric Acid

- 5.1.1.4 Other Acidifiers

- 5.1.2 Antibiotics

- 5.1.2.1 Tetracyclines

- 5.1.2.2 Penicillins

- 5.1.2.3 Tylosin

- 5.1.2.4 Bacitracin

- 5.1.2.5 Other Antibiotics

- 5.1.3 Antioxidants

- 5.1.3.1 Butylated Hydroxyanisole (BHA)

- 5.1.3.2 Butylated Hydroxytoluene (BHT)

- 5.1.3.3 Ethoxyquin

- 5.1.3.4 Propyl Gallate

- 5.1.3.5 Tocopherols

- 5.1.3.6 Citric Acid

- 5.1.3.7 Other Antioxidants

- 5.1.4 Amino Acids

- 5.1.4.1 Lysine

- 5.1.4.2 Tryptophan

- 5.1.4.3 Methionine

- 5.1.4.4 Threonine

- 5.1.4.5 Other Amino Acid

- 5.1.5 Binders

- 5.1.5.1 Natural Binders

- 5.1.5.2 Synthetic Binders

- 5.1.6 Enzymes

- 5.1.6.1 Carbohydrases

- 5.1.6.2 Phytases

- 5.1.6.3 Other Enzymes

- 5.1.7 Flavors and Sweeteners

- 5.1.7.1 Flavors

- 5.1.7.2 Sweeteners

- 5.1.8 Minerals

- 5.1.8.1 Macrominerals

- 5.1.8.2 Microminerals

- 5.1.9 Mycotoxin Detoxifiers

- 5.1.9.1 Binders

- 5.1.9.2 Biotransformers

- 5.1.10 Phytogenics

- 5.1.10.1 Herbs & Spices

- 5.1.10.2 Essential Oil

- 5.1.10.3 Other Phytogenics

- 5.1.11 Pigments

- 5.1.11.1 Carotenoids

- 5.1.11.2 Curcumin & Spirulina

- 5.1.12 Prebiotics

- 5.1.12.1 Inulin

- 5.1.12.2 Fructo Oligosaccharides

- 5.1.12.3 Galacto Oligosaccharides

- 5.1.12.4 Xylo Oligosaccharides

- 5.1.12.5 Lactulose

- 5.1.12.6 Mannan Oligosaccharides

- 5.1.12.7 Other Prebiotics

- 5.1.13 Probiotics

- 5.1.13.1 Lactobacilli

- 5.1.13.2 Bifidobacteria

- 5.1.13.3 Streptococcus

- 5.1.13.4 Pediococcus

- 5.1.13.5 Enterococcus

- 5.1.13.6 Other Probiotics

- 5.1.14 Vitamins

- 5.1.14.1 Vitamin A

- 5.1.14.2 Vitamin B

- 5.1.14.3 Vitamin C

- 5.1.14.4 Vitamin E

- 5.1.14.5 Other Vitamins

- 5.1.15 Yeast

- 5.1.15.1 Live Yeast

- 5.1.15.2 Spent Yeast

- 5.1.15.3 Torula Dried Yeast

- 5.1.15.4 Selenium Yeast

- 5.1.15.5 Whey Yeast

- 5.1.15.6 Yeast Derivatives

- 5.1.1 Acidifiers

- 5.2 By Form

- 5.2.1 Dry

- 5.2.2 Liquid

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.1.4 Rest of North America

- 5.3.2 South America

- 5.3.2.1 Brazil

- 5.3.2.2 Argentina

- 5.3.2.3 Chile

- 5.3.2.4 Rest of South America

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 France

- 5.3.3.3 United Kingdom

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Netherlands

- 5.3.3.7 Russia

- 5.3.3.8 Rest of Europe

- 5.3.4 Asia-Pacific

- 5.3.4.1 China

- 5.3.4.2 India

- 5.3.4.3 Japan

- 5.3.4.4 Australia

- 5.3.4.5 New Zealand

- 5.3.4.6 South Korea

- 5.3.4.7 Indonesia

- 5.3.4.8 Thailand

- 5.3.4.9 Vietnam

- 5.3.4.10 Rest of Asia-Pacific

- 5.3.5 Middle East

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 Turkey

- 5.3.5.3 Iran

- 5.3.5.4 United Arab Emirates

- 5.3.5.5 Rest of Middle East

- 5.3.6 Africa

- 5.3.6.1 South Africa

- 5.3.6.2 Egypt

- 5.3.6.3 Kenya

- 5.3.6.4 Rest of Africa

- 5.3.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Cargill, Incorporated

- 6.4.2 Archer Daniels Midland Company

- 6.4.3 Nutreco N.V. (SHV Holdings N.V.)

- 6.4.4 DSM-Firmenich AG

- 6.4.5 Alltech, Inc.

- 6.4.6 Kemin Industries, Inc.

- 6.4.7 BASF SE

- 6.4.8 Evonik Industries AG

- 6.4.9 Elanco Animal Health Incorporated

- 6.4.10 Novus International, Inc.

- 6.4.11 Bluestar Adisseo Company

- 6.4.12 Lallemand Inc.

- 6.4.13 Zinpro Corporation

- 6.4.14 Land O'Lakes, Inc.

- 6.4.15 De Heus Animal Nutrition B.V. (Royal De Heus)