|

시장보고서

상품코드

2063380

자동차용 디스플레이 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Automotive Display - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

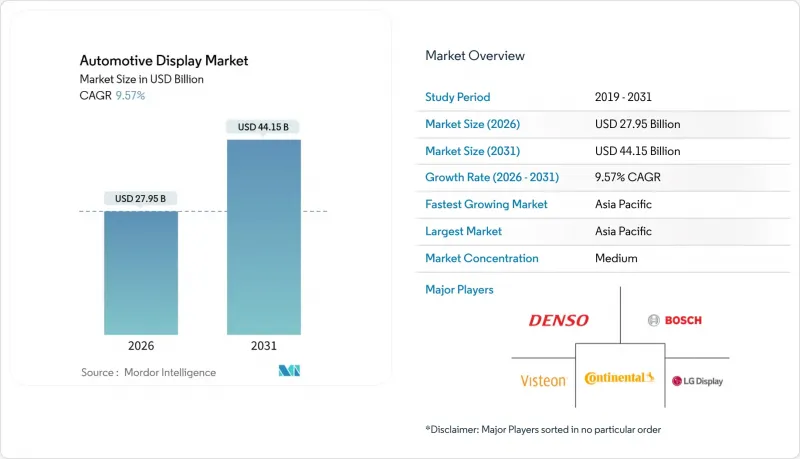

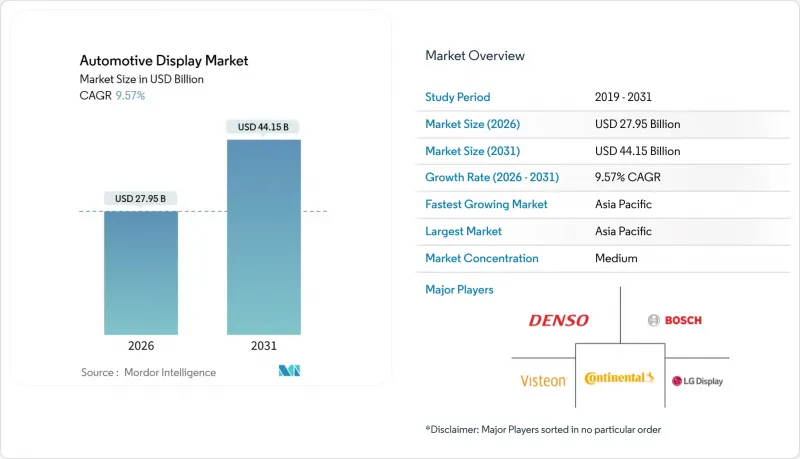

Mordor Intelligence에 의하면, 자동차용 디스플레이 시장 규모는 2026년에 279억 5,000만 달러로 평가되었고, 2031년까지 441억 5,000만 달러에 이를 것으로 예측되며, 예측 기간 중 연평균 복합 성장률(CAGR)은 9.57%로 전망됩니다.

본 보고서는 제품 유형별(센터 스택 디스플레이, 계기판 디스플레이 등), 디스플레이 기술별(액정 디스플레이(LCD), OLED 등), 차종별(승용차 및 상용차), 디스플레이 크기별(5인치 이하, 6-10인치 등) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 및 수량(대수)으로 제시되어 있습니다.

세계의 자동차용 디스플레이 시장 동향 및 인사이트

통합형 디지털 콕핏에 대한 수요 급증

자동차 제조업체들은 계기판, 인포테인먼트 시스템, 그리고 공조 제어 기능을 단일 도메인 컨트롤러에 통합하고 있으며, 이를 통해 배선량을 줄이고 대시보드 공간을 확보함으로써 자동차 디스플레이 시장에 더 큰 크기의 디스플레이를 탑재할 수 있게 하고 있습니다. 비스테온은 2025년 3분기에 첨단 디스플레이 및 SmartCore 콕핏 수주로 18억 달러를 확보하며, 통합된 하드웨어 및 소프트웨어 스택이 어떻게 조달 입찰에서 승리를 거두는지 보여주었습니다. 중국의 전기차 제조업체인 BYD, NIO, Xpeng은 12.8인치 AMOLED 계기판과 14-15인치 센터 스크린을 조합한 구성을 표준화하고 있으며, 이로 인해 전 세계 공급업체에 대한 기본 사양이 상향 조정되고 있습니다. LG전자의 'Digital Cockpit Alpha'는 POLED, LCD, AR-HUD를 통합하고, 운전자 모니터링 카메라와 연동된 통합 UI를 구현하고 있습니다. 이러한 아키텍처 전환으로 인해 공급업체 기반은 축소되는 추세입니다. 이는 UNECE R155에 기반한 펌웨어 및 사이버 보안 인증이 공급업체의 적격성을 결정하는 요인으로 점점 더 중요해지고 있기 때문입니다. AUTOSAR Adaptive R24-11은 무선(OTA) 업데이트를 더욱 효율화하여, 차량 인도 후에도 콕핏의 업데이트 주기를 지속적으로 표준화합니다.

보다 고도화된 HMI가 필요한 커넥티드카 및 전기차의 부상

전기 구동 시스템에서는 충전 상태, 회생 제동, 에너지 흐름의 시각화가 필요하지만, 자동차 디스플레이 시장에서 내연기관 차량의 계기판에는 이러한 기능이 없습니다. 중국에서는 가까운 시일 내에 전기차 생산이 크게 증가할 것으로 예상에 따라, 고해상도 회전식 디스플레이에 대한 수요가 높아지고 있습니다. ETSI 가이드라인에 따라 표준화된 5G 지원 V2X 서비스의 도입으로 인해, 협력 주행 정보를 효과적으로 표시하기 위해 HUD의 시야각 확대가 필요해지고 있습니다. Aptiv의 상용차용 통합 콕핏 컨트롤러는 텔레매틱스와 운전자 모니터링 기능을 통합하여 비용 효율적인 솔루션을 제공합니다. 뛰어난 명암비와 빠른 응답 속도를 갖춘 OLED 기술은 고가 프리미엄 전기차의 디스플레이 요구 사항을 충족합니다. 전기차와 커넥티비티 기술의 발전이 맞물려, 차량 1대당 평균 디스플레이 면적의 확대에 기여하고 있습니다.

자동차용 OLED 가격 상승

자동차용 OLED 패널은 LCD 패널에 비해 가격이 훨씬 비쌉니다. 이는 자동차용 디스플레이 시장에서 소비자용 OLED에 비해 OLED의 제조 수율이 낮다는 점을 반영한 것입니다. 또한, 과열 방지 대책으로 인해 펌웨어 오버헤드가 발생하며, 이로 인해 유효 표시 영역이 축소되어 비용이 더욱 증가합니다. LG디스플레이는 생산 비용을 대폭 절감하기 위해 조만간 가동을 시작할 것으로 예상되는 차세대 제조 시설에 막대한 투자를 하고 있습니다. 그러나 이 투자금을 회수하는 데는 수년이 걸릴 것으로 예측됩니다. 비용 프리미엄이 고급차 가격에서 차지하는 비중이 극히 적기 때문에 도입은 여전히 고급차 부문에 집중되어 있으며, 향후 몇 년간 일반 시장으로의 확산은 제한적일 것으로 예측됩니다. 게다가 LG디스플레이, 삼성디스플레이, BOE 등 공급업체의 수가 제한적이라는 점은 OEM 제조업체에게 공급량 측면에서 리스크가 되고 있습니다.

부문별 분석

2025년 기준으로 센터 스택 스크린은 자동차용 디스플레이 시장의 40.12%를 차지했으나, 유로 NCAP의 인센티브에 힘입어 헤드업 디스플레이(HUD)의 출하량은 연평균 성장률(CAGR) 10.01%로 증가하고 있습니다. 폭스바겐 ID.7에 탑재된 콘티넨탈의 AR-HUD는 운전자의 시선이 계기판으로 이동하는 시간을 단축시켜, 실질적인 안전상의 이점을 제공합니다. 기존에는 아날로그-디지털 하이브리드 방식이었던 계기판은 EU의 일반 안전 규정이 ADAS 표시를 명확히 요구하게 됨에 따라 상용차에서 12.3인치 풀 디지털화가 진행되고 있습니다.

센터 스택 시장에서는 중국 공급업체들이 10.25인치 LCD 모듈을 시장에 대량으로 공급하며 일본 및 한국 제품에 비해 상당한 가격 경쟁력을 보이고 있어, 이익률 압박에 직면해 있습니다. 그러나 유럽과 미국의 OEM 업체들은 UNECE의 사이버 보안 규정을 이유로 공급업체의 이중화에 소극적인 태도를 보이고 있습니다. 파나소닉이 스바루를 위해 개발한 시선 추적형 HUD는 동공의 확장 정도에 따라 밝기를 조절하는 기능을 갖추고 있어, 상품화가 진행되고 있는 센터 스택 시장에서 경쟁사와의 차별화를 꾀하고 있습니다. HUD 자동차용 디스플레이 시장 규모는 2030년까지 크게 확대될 것으로 예상되며, 그중에서도 AR-HUD가 가장 급격한 성장세를 보일 것으로 전망됩니다. 후석 엔터테인먼트는 여전히 틈새 시장이며, 구독료가 장벽이 되어 보급률은 낮은 수준에 머물러 있지만, BMW의 초광폭 31인치 '시어터 스크린'은 고급차에 대한 잠재적 수요가 존재함을 시사하고 있습니다.

액정 기술은 저렴한 비용과 확립된 공급망 덕분에 2025년 자동차용 디스플레이 시장에서 65.13%의 점유율을 유지했습니다. 한편, 유기EL(OLED)은 메르세데스-마이바흐의 48인치 플렉서블 대시보드와 BYD의 15인치 AMOLED 계기판 채택에 힘입어 연평균 성장률(CAGR) 10.64%로 성장하고 있습니다. OLED에 비해 훨씬 저렴한 비용으로 고해상도를 구현하는 LTPS-LCD는 2026년까지 자동차용 LCD 생산에서 상당한 점유율을 차지할 것으로 예측됩니다.

AUO가 곧 출하를 시작할 다수의 존을 갖춘 첨단 패널이 보여주듯이, Mini-LED는 일시적인 고대비 솔루션으로 기능합니다. 한편, Micro-LED는 아직 상용화 전 단계에 있지만, 현재의 대량 전사 수율로는 자동차 업계에서 요구하는 엄격한 기준을 충족하지 못하는 결함이 발생하고 있습니다. 따라서 기술적 계층 구조 측면에서 볼 때, LCD는 주류 플랫폼용, OLED는 고급차용, Mini-LED는 타협안으로 자리매김하고 있으며, Micro-LED는 2028년 이후에 성숙기에 접어들 것으로 예측됩니다.

지역별 분석

아시아태평양은 2025년에 자동차용 디스플레이 시장 점유율의 46.33%를 차지하며 1위를 차지한 것으로 평가되었으며, 2031년까지 연평균 성장률(CAGR) 12.05%로 성장할 것으로 전망됩니다. 중국 내 전기차의 급증은 콕핏 기술의 눈부신 발전을 이끌고 있으며, 회전식 스크린이나 AR-HUD와 같은 혁신적인 기술이 주목받고 있습니다. 주요 디스플레이 제조업체들은 국내 OEM 업체들이 유럽 및 미국 공급망에서 볼 수 있는 수준을 상회하는 견고한 재고 완충 장치를 유지할 수 있도록 생산 능력에 대한 대규모 투자를 진행하고 있습니다. 한편, 일본의 기존 기업들은 스마트폰 시장에서 중국 경쟁사들에게 시장 점유율을 빼앗긴 후, 자동차용 디스플레이로 사업 방향을 전환하고 있습니다. 이러한 전략적 전환에는 시장 내 입지를 회복하기 위한 제휴도 수반되고 있습니다. 한국에서는 지속적인 공급망 문제에 대응하기 위해 주요 자동차 브랜드를 대상으로 디스플레이 생산의 수직 통합이 추진되고 있습니다.

유럽과 북미에서는 자동차 판매량 증가세가 둔화되고 있지만, 첨단 기능의 도입은 빠르게 진행되고 있습니다. 유럽의 규제 기준에 따라 비용 증가가 따르지만, 주요 자동차 라인업 전반에 걸쳐 AR-HUD 통합이 진행되고 있습니다. 또한, 사이버 보안 규제로 인해 공급망 환경이 재편되면서, 필요한 인증을 갖추지 못한 신규 진출기업들의 경우 통합 과정이 더욱 복잡해지고 있습니다. 북미에서는 이와 유사한 규제 정책이 존재하지 않기 때문에 해당 기능의 도입이 유럽에 비해 뒤처져 있습니다. 그러나 고급 자동차 브랜드들은 유럽의 기준에 부합하기 위해 첨단 디스플레이 기술을 도입하고 있습니다.

남미, 중동 및 아프리카의 신흥 시장에는 성장 기회가 있습니다. 남미에서는 합리적인 가격의 안드로이드 헤드 유닛이 애프터마켓에 진출하면서 사후 장착 시장의 활기가 더해지고 있지만, 규제상의 문제로 인해 보급은 제한적입니다. 중동에서는 수입 고급차에 고급 디스플레이가 선호되지만, 차량의 기본 크기가 작기 때문에 시장 규모 확대에는 한계가 있습니다. 튀르키예에서는 유럽의 안전 기준을 충족하도록 상용차 생산을 조정하고 있는 반면, 남아프리카공화국에서는 높은 관세로 인해 도입이 프리미엄 부문으로 제한되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.22According to Mordor Intelligence, the automotive display market size stood at USD 27.95 billion in 2026 and is forecast to reach USD 44.15 billion by 2031, translating into a 9.57% CAGR during the forecast period.

This report is Segmented by Product Type (Center Stack Display, Instrument Cluster Display, and More), Display Technology (Liquid Crystal Display (LCD), Organic Light-Emitting Diode (OLED), and More), Vehicle Type (Passenger Cars and Commercial Vehicles), Display Size (≤5-Inch, 6-10 Inch, and More), and Geography. Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

Global Automotive Display Market Trends and Insights

Soaring Demand for Integrated Digital Cockpits

Automakers are consolidating instrument clusters, infotainment systems, and climate controls into single domain controllers, reducing wiring mass and freeing up dashboard real estate for larger displays in the automotive display market. Visteon secured USD 1.8 billion in advanced display and SmartCore cockpit orders during Q3 2025, demonstrating how integrated hardware-software stacks win sourcing bids. Chinese EV makers BYD, NIO, and Xpeng have normalized 12.8-inch AMOLED clusters paired with 14-15-inch center screens, raising the baseline specification for global suppliers. LG Electronics' Digital Cockpit Alpha fuses POLED, LCD, and AR-HUD into a unified UI linked to driver-monitoring cameras. The architecture shift compresses the supply base because firmware and cybersecurity credentials under UNECE R155 increasingly define vendor eligibility. AUTOSAR Adaptive R24-11 further streamlines over-the-air (OTA) updates, standardizing cockpit refresh cycles well beyond vehicle delivery.

Rise of Connected and Electric Vehicles Needing Richer HMI

Electric drivetrains require visualizations of charging status, regenerative braking, and energy flow, which are absent in internal-combustion dashboards within the automotive display market. China is expected to significantly increase EV production in the near future, boosting the demand for high-resolution rotating displays. The adoption of 5G-enabled V2X services, standardized under ETSI guidelines, is driving the need for expanded HUD fields of view to effectively display cooperative-driving information. Aptiv's Integrated Cockpit Controller for commercial vehicles integrates telematics and driver monitoring, offering cost-efficient solutions. OLED technology, with its superior contrast ratio and rapid response time, addresses the visualization requirements of premium EVs in the higher price segment. Together, advancements in EVs and connectivity are contributing to an increase in the average display area per vehicle.

Premium Pricing of Automotive-Grade OLEDs

Automotive OLED panels are significantly more expensive than their LCD counterparts, reflecting lower manufacturing yields for OLEDs compared to consumer OLEDs within the automotive display market. Additionally, burn-in mitigation introduces firmware overhead, which reduces the usable area and further increases costs. LG Display is investing heavily in its next-generation manufacturing facility, which is expected to become operational in the near future, aiming to significantly reduce production costs. However, the return on this investment is anticipated to take several years. Since the cost premium represents a small fraction of a luxury car's price, adoption remains concentrated in the luxury segment, with limited penetration in the mass market expected over the next several years. Moreover, the limited number of suppliers, including LG Display, Samsung Display, and BOE, poses volume risks for OEMs.

Other drivers and restraints analyzed in the detailed report include:

- OEM Push for Larger Pillar-to-Pillar Screens

- Rapid Cost-Down of High-Brightness Automotive LCDs

- Glass and Semiconductor Supply Volatility

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Center stack screens held a 40.12% share of the automotive display market in 2025; however, Head-Up Display (HUD) shipments are rising at a 10.01% CAGR, driven by Euro NCAP incentives. Continental's AR-HUD on the Volkswagen ID.7 shortens dashboard glance time, adding tangible safety benefits . Instrument clusters, historically analog-digital hybrids, are undergoing 12.3-inch full-digital upgrades in commercial vehicles as EU General Safety Rules demand clear ADAS readouts.

Center stacks face margin compression as Chinese suppliers flood the market with 10.25-inch LCD modules, offering a significant discount to Japanese and Korean units. However, Western OEMs hesitate to dual-source due to UNECE cybersecurity stipulations. Panasonic's eye-tracking HUD for Subaru adapts brightness to pupil dilation, differentiating itself from competitors in an increasingly commoditized center-stack space. The automotive display market size for HUDs is forecast to expand significantly by 2030, with AR-HUD capturing the steepest curve. Rear-seat entertainment remains a niche market, with lower adoption rates restrained by subscription costs, but ultra-wide 31-inch Theatre Screens from BMW suggest pent-up demand for luxury.

Liquid crystal technology maintained a 65.13% share of the automotive display market in 2025, due to its low cost and established supply chain. Organic Light-Emitting Diode (OLED), however, is expanding at 10.64% CAGR, buoyed by Mercedes-Maybach's 48-inch flexible dash and BYD's adoption of 15-inch AMOLED clusters. By delivering high resolutions at a significantly lower cost compared to OLED, LTPS-LCD is expected to dominate a substantial share of the automotive LCD output by 2026.

Mini-LED serves as a temporary high-contrast solution, as demonstrated by AUO's advanced panel featuring numerous zones set to ship soon. While Micro-LED is still in its pre-commercial phase, its current mass-transfer yields result in defects that do not meet the stringent standards required in the automotive industry. Thus, the technological hierarchy positions LCDs for mainstream platforms, OLEDs for luxury cabins, mini-LEDs as a compromise, and anticipates micro-LEDs to mature post-2028.

Geography Analysis

The Asia-Pacific region led with a 46.33% automotive display market share in 2025 and is projected to expand at a 12.05% CAGR through 2031. China's EV surge is driving significant advancements in cockpit technology, with innovations such as rotating screens and AR-HUDs gaining traction. Leading display manufacturers are heavily investing in production capacities to ensure domestic OEMs maintain robust inventory buffers, surpassing the norms seen in Western supply chains. Meanwhile, Japan's established players are shifting their focus to vehicle displays after losing ground in the smartphone market to Chinese competitors. This strategic pivot is accompanied by partnerships aimed at revitalizing their market presence. In South Korea, efforts are underway to vertically integrate display production for key automotive brands, addressing ongoing supply chain challenges.

Europe and North America are witnessing slower growth in vehicle units, but are rapidly adopting advanced features. Regulatory standards in Europe are driving the integration of AR-HUDs across major automotive line-ups, despite the associated cost premiums. Cybersecurity regulations are also reshaping the supplier landscape, increasing the complexity of integration for new entrants without the necessary certifications. In North America, feature adoption lags behind Europe due to the absence of similar regulatory policies. However, premium automotive brands are incorporating advanced display technologies to align with European benchmarks.

Emerging markets in South America and the Middle East & Africa present growth opportunities. In South America, retrofitting activities are gaining momentum as affordable Android head units enter the aftermarket space, although regulatory challenges limit broader adoption. In the Middle East, there is a preference for premium displays in luxury imports, but smaller vehicle bases constrain scalability. Turkey is adapting its commercial vehicle production to meet European safety standards, while in South Africa, high tariffs are restricting adoption to premium segments.

- LG Display Co., Ltd.

- Samsung Display Co., Ltd.

- Robert Bosch GmbH

- Continental AG

- Denso Corporation

- Visteon Corporation

- Panasonic Automotive Systems Co., Ltd.

- Nippon Seiki Co., Ltd.

- AUO Corporation

- Japan Display Inc.

- Sharp Corporation

- BOE Technology Group Co., Ltd.

- Hyundai Mobis Co., Ltd.

- Valeo SA

- Tianma Microelectronics Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Drivers

- 4.1.1 Soaring Demand for Integrated Digital Cockpits

- 4.1.2 Rise of Connected and Electric Vehicles Needing Richer HMI

- 4.1.3 OEM Push for Larger Pillar-to-Pillar Screens

- 4.1.4 Rapid Cost-Down of High-Brightness Automotive LCDs

- 4.1.5 NCAP Distraction-Score Rules Accelerating HUD Fitment

- 4.1.6 Software-Defined Vehicle OTA UX Refresh Cycles

- 4.2 Market Restraints

- 4.2.1 Premium Pricing of Automotive-Grade OLEDs

- 4.2.2 Glass and Semiconductor Supply Volatility

- 4.2.3 Rising Cyber-Security Compliance Costs

- 4.2.4 Reliability Issues with Large Flexible Displays

- 4.3 Value/Supply-Chain Analysis

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value (USD) and Volume (Units))

- 5.1 By Product Type

- 5.1.1 Center Stack Display

- 5.1.2 Instrument Cluster Display

- 5.1.3 Head-Up Display

- 5.1.4 Rear-Seat Entertainment Display

- 5.2 By Display Technology

- 5.2.1 Liquid Crystal Display (LCD)

- 5.2.2 Organic Light-Emitting Diode (OLED)

- 5.2.3 MiniLED / MicroLED

- 5.3 By Vehicle Type

- 5.3.1 Passenger Cars

- 5.3.2 Commercial Vehicles

- 5.4 By Display Size

- 5.4.1 Less than equal to 5-inch

- 5.4.2 6 to 10 inch

- 5.4.3 Above 10 inch

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Rest of North America

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 Egypt

- 5.5.5.4 Turkey

- 5.5.5.5 South Africa

- 5.5.5.6 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 LG Display Co., Ltd.

- 6.4.2 Samsung Display Co., Ltd.

- 6.4.3 Robert Bosch GmbH

- 6.4.4 Continental AG

- 6.4.5 Denso Corporation

- 6.4.6 Visteon Corporation

- 6.4.7 Panasonic Automotive Systems Co., Ltd.

- 6.4.8 Nippon Seiki Co., Ltd.

- 6.4.9 AUO Corporation

- 6.4.10 Japan Display Inc.

- 6.4.11 Sharp Corporation

- 6.4.12 BOE Technology Group Co., Ltd.

- 6.4.13 Hyundai Mobis Co., Ltd.

- 6.4.14 Valeo SA

- 6.4.15 Tianma Microelectronics Co., Ltd.

7 Market Opportunities & Future Outlook

- 7.1 Growing AR-HUD Monetization Potential

- 7.2 MicroLED Roadmaps Promise 30% Power Savings

- 7.3 Over-the-air Subscription Models for Display-Based Features

- 7.4 China-Centric Cockpit-Display Supply Chain Localization

- 7.5 Aftermarket Retrofit Demand for Screens Above 12-inch in Developing Markets