|

시장보고서

상품코드

2063404

의료기기 및 MedTech ERP(전사적 자원 계획) : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Medical Device And MedTech Enterprise Resource Planning - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

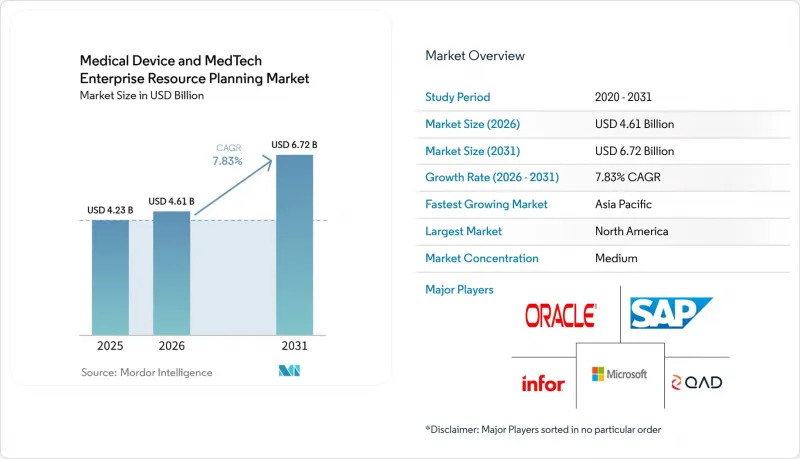

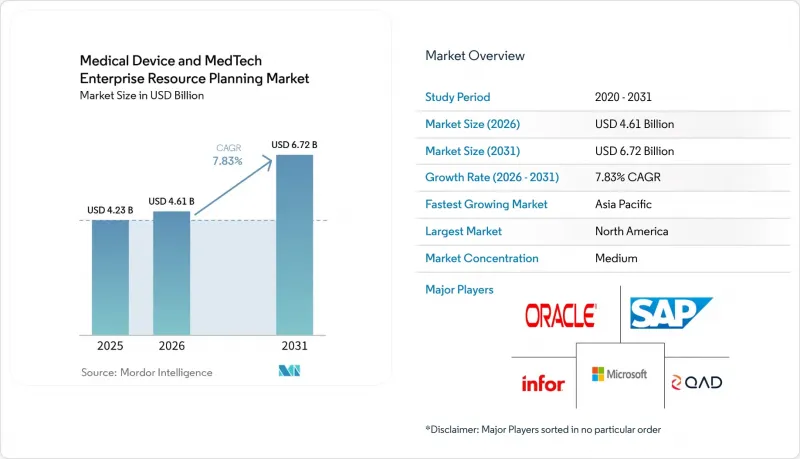

Mordor Intelligence에 의하면, 의료기기 및 MedTech ERP(전사적 자원 계획) 시장 규모는 2025년 42억 3,000만 달러로 평가되었습니다. 2026년 46억 1,000만 달러에서 2031년까지 67억 2,000만 달러로 확대되고 2026년부터 2031년까지 연평균 복합 성장률(CAGR)은 7.83%를 나타낼 것으로 예측됩니다.

본 보고서는 도입 형태(클라우드 기반, On-Premise형, 하이브리드형), 구성 요소(소프트웨어, 서비스), 조직 규모(대기업, 중소기업), 최종 사용자(의료기기 제조업체, 메드테크 서비스 제공업체 등) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 의료기기 및 MedTech ERP(전사적 자원 계획) 시장 동향과 인사이트

UDI 및 품질 규정 준수에 대한 규제 압박의 가속화

2026년 5월 28일 EUDAMED에 대한 의무 제출 기한에 따라, 제조업체는 의료기기 마스터 데이터, 사업자 등록 및 감시 보고서를 유럽 중앙 데이터베이스에 업로드해야 할 의무가 부과되었으며, 이에 따라 ERP 벤더들은 제품 수명 주기 모듈에서 직접 일련번호 및 인증서를 전송하는 네이티브 커넥터를 출시하고 있습니다. 미국에서는 2026년 2월 2일에 발효된 품질 경영 시스템 규정에 따라 컴퓨터 시스템의 검증 작업이 ISO 13485 : 2016을 준수해야 하며, ERP의 품질 워크플로우에 통합된 AI 모듈에 대한 심사가 강화되고 있습니다. 이에 대해 Oracle은 사전 검증을 거친 스크립트를 제공하는 ‘헬스 디바이스 검증 프로그램’을 도입하여, 클래스 III 의료기기 제조업체의 설치 적격성 확인 주기를 절반으로 단축했습니다. 일본 PMDA의 ISO 13485와의 조화 또한, 단일 마스터 데이터 계층 내에서 FDA, EU, 일본의 사업장 식별자를 분리할 수 있는 다지역 지원 템플릿에 대한 수요를 높이고 있습니다. 이러한 규제 요건들은 종합적으로, 분기별로 규제 당국 대응 체계를 개선할 수 있는 플랫폼에 대한 조달 결정을 뒷받침하고 있습니다.

중견 의료기기 제조업체의 클라우드 네이티브 SaaS ERP로의 전환

사용자당 월 150달러부터 시작하는 구독 요금 덕분에, 기존 On-Premise 도입에 필요했던 200만 달러 이상의 초기 투자 비용이 대폭 절감되어, 연간 매출액 5,000만 달러에서 5억 달러 규모의 기업도 의료기기 및 메드테크 ERP(전사적 자원 관리) 시장에 진출할 수 있게 되었습니다. 2025년 Microsoft Dynamics 365 도입을 통해 전자 배치 기록 및 편차 워크플로가 통합되어, 별도의 사용자 정의 코드 없이도 21 CFR Part 11을 준수할 수 있게 되었습니다. 유럽의 중견 제조업체는 미리 설정된 로트 추적 템플릿을 활용하여 최단 9개월 만에 본격적인 가동을 실현했습니다. 한편, 아시아태평양의 기업들은 중국의 데이터 보안법을 고려하여 지적재산권 데이터를 현지 데이터센터에 보관하는 하이브리드 클라우드를 선호하여 도입했습니다. 신속한 규제 대응도 또 다른 매력으로 꼽히고 있습니다. SaaS 공급업체는 분기마다 새로운 UDI 형식이나 ISO 개정판을 제공할 수 있지만, On-Premise 고객은 업그레이드를 3년마다 미루는 경우가 많습니다. 그럼에도 불구하고, 데이터 현지화에 관한 법규가 하이브리드 수요를 지속적으로 뒷받침하고 있어, 서비스 제공업체들은 현지 품질 관리 시스템과 클라우드상의 재무 장부 간에 저지연 동기화를 실현해야 하는 압박을 받고 있습니다.

높은 검증 비용 및 FDA 컴퓨터 시스템 검증 비용

FDA가 2024년에 위험 기반 컴퓨터 소프트웨어 보증(CSA)으로 전환했음에도 불구하고, 클래스 III 의료기기 제조업체들은 도입, 운영 및 성능 적합성 시험을 위해 ERP 모듈당 약 120만 달러의 예산을 여전히 책정하고 있습니다. 분기마다 클라우드 갱신이 있을 때마다 회귀 테스트 스크립트 실행, 영향 평가, 그리고 실행 완료된 테스트 기록의 보관이 필요해지면서, 릴리스 일정이 길어지고 컨설팅 비용이 증가하고 있습니다. 유럽연합(EU)도 유사한 요건을 부과하고 있으며, 감사 추적을 최대 15년간 열람 가능한 상태로 유지할 것을 요구하고 있어, 이에 따라 검증 비용이 증가하고 있습니다. 클라우드 벤더들은 현재 ‘Validation-as-a-Service(Validation-as-a-Service)’ 번들을 판매하고 있으며, Acumatica의 턴키형 문서 패키지 비용은 15만 달러이지만, 사이트별 워크플로우나 타사 시스템과의 통합을 위해서는 여전히 맞춤형 증거 생성이 필수적입니다. 매출액이 5,000만 달러인 제조업체의 경우, 이 비용은 연간 매출의 2.4%에 해당하며, 많은 중소기업이 전체 제품군 도입을 미루는 이유를 여실히 보여주고 있습니다.

부문별 분석

2025년 기준으로, 의료기기 및 메드테크(MedTech) ERP(전사적 자원 관리) 시장 점유율의 54.98%를 클라우드 도입이 차지했으며, 200만 달러 이상의 데이터센터 투자를 피하고자 하는 중견 기업 수요에 힘입어 2031년까지 연평균 성장률(CAGR) 8.43%를 나타낼 것으로 예측됩니다. 각 벤더사는 SAP의 ECC에 대한 2027년 지원 종료나 Oracle의 E-Business Suite에 대한 2030년 제공 종료와 같은 ‘지원 종료’라는 수단을 통해 고객을 SaaS 구독 모델로 유도하고 있습니다. 그렇긴 하지만, 소프트웨어 버전 관리나 맞춤형 검증 스크립트를 완벽하게 통제하고자 하는 다국적 기업들 사이에서는 On-Premise 환경 시장 규모가 계속해서 유지될 것입니다. 하이브리드 아키텍처는 중국의 ‘데이터 보안법’이나 유럽연합(EU)의 ‘GDPR(EU 개인정보보호규정)’ 적용 대상인 조직을 위한 타협안이 되어, 품질 기록을 로컬에 보관하면서 계획 엔진을 전 세계 클라우드에서 가동할 수 있게 해줍니다.

Oracle의 공정 제조용 커넥터는 제조 현장의 배치 데이터를 몇 분 간격으로 동기화하여, 과거 하이브리드 도입의 걸림돌이 되었던 지연에 대한 우려를 해소합니다. 마이크로소프트와 타사 품질 컨설턴트들은 위험 기반 검증 템플릿을 제공하고 있으며, 이를 통해 실제 가동까지 걸리는 기간을 40% 단축할 수 있어 SaaS 출시 주기에 수반되는 단점에 대한 인식이 점차 약해지고 있습니다. 그럼에도 불구하고, 분기별 기능 업데이트로 인해 제조업체는 항상 최신 버전을 사용하는 검증 팀을 유지해야 하지만, On-Premise 고객은 변경 사항을 한꺼번에 모아 수년에 걸친 단일 개선 프로젝트로 진행할 수 있습니다. 모든 도입 형태에서 구매자들은 현재 일반적인 기능 체크리스트보다 사이버 보안 체계 및 규제 당국 대응에 대한 감사 기록을 더 중요하게 여기고 있으며, 평가 기준은 규정 준수 자동화 쪽으로 전환되고 있습니다.

2025년에는 소프트웨어 라이선스와 구독이 시장 매출의 69.77%를 차지했으나, 검증의 복잡성이 증가함에 따라 서비스 부문은 연평균 성장률(CAGR) 8.23%로 성장하고 있습니다. 도입 프로젝트에는 12-18개월이 소요되며, 검증 작업이 청구 가능 시간의 최대 40%를 차지하기 때문에 제조업체들은 컴퓨터 소프트웨어 보증(CSA) 문서 작성을 생명과학 전문가에게 외주화해야 하는 상황에 처해 있습니다. 고객들이 분기별 검증, 패치 관리, 규제 모니터링 서비스를 한데 묶은 지속적인 규정 준수 계약을 채택함에 따라, 매니지드 서비스 시장은 확대되고 있습니다.

인포시스(Infosys)와 트리센티스(Tricentis)는 현재 SAP S/4HANA로 전환하는 과정에서 회귀 테스트를 자동화하고 있으며, 이를 통해 테스트 케이스 생성을 40% 줄이고 프로젝트 전체 예산을 절감하고 있습니다. 마찬가지로, 제조업체들이 멀티테넌트형 클라우드로 전환하기 전에 수십 년에 걸친 로트 추적 기록을 정리하기 위해 데이터 마이그레이션 컨설팅 사업도 호황을 누리고 있습니다. 교육 사업도 또 다른 긍정적인 요소입니다. 품질 엔지니어와 공급망 기획자는 검증 프로토콜을 위반하지 않으면서 AI가 생성한 예측 결과를 해석할 수 있도록 역량을 강화해야 합니다. AI 모듈이 추가 소프트웨어 비용 없이 통합되는 사례가 늘어남에 따라, 수익은 하류 단계의 자문, 교육, 그리고 시스템을 감사 대비 상태로 유지하기 위한 용도 관리 애드온으로 이동하고 있습니다.

지역별 분석

2025년에는 북미가 시장의 38.39%를 차지했습니다. 이는 FDA의 엄격한 감독과 다국적 의료기기 제조업체들이 밀집해 있다는 점이 뒷받침하고 있습니다. 새로운 품질 관리 시스템 규정에 따라 기업들은 ERP 관리 체계를 재검증해야 할 의무가 생겼으며, 이로 인해 ‘Validation-as-a-Service(검증 서비스)’ 계약이 확산되고 있습니다. 보스턴 사이언티픽의 액소닉스 인수 등, 합병 후의 사업 재편은 이번 인수를 통해 16곳 이상의 제조 거점을 단일 세계 원장 체계로 통합하고, 풀 스위트 S/4HANA 전환을 촉진하는 방식을 여실히 보여주고 있습니다. 캐나다와 멕시코는 미국 발주처가 요구하는 실시간 추적성 요건을 충족하기 위해 클라우드 ERP 시스템을 도입하는 니어쇼어 위탁 생산 거점으로 부상하고 있습니다.

아시아태평양은 가장 빠르게 성장하는 지역으로, 2031년까지 연평균 성장률(CAGR) 8.83%를 기록하며 성장하고 있습니다. 중국에서 클래스 III 의료기기에 대한 UDI 도입(2024년) 및 클래스 II에 대한 도입(2025년)은 국내 제조 공장에 일련번호 및 EUDAMED 형식의 커넥터 도입을 의무화하고 있으며, 유럽과 미국의 식별자 모두를 지원할 수 있는 플랫폼에 대한 투자를 촉진하고 있습니다. 인도의 ‘생산 연계형 인센티브(PLI)’ 제도에서는 IoT 대응 ERP를 도입한 공장에 대해 증분 매출의 최대 5%를 환급해 주고 있어, 신규 프로젝트에서의 도입을 가속화하고 있습니다. 한국은 센서 기반 스마트 공장에 대한 지원을 실시하고 있는 반면, 일본의 ‘사회 5.0’ 구상은 ISO 13485 인증을 목표로 하는 2차 공급업체를 대상으로 IoT와 ERP의 융합을 촉진하고 있습니다.

유럽은 여전히 큰 시장 점유율을 유지하고 있으며, 그 배경에는 의료기기 규정(MDR)과 2026년 5월로 예정된 EUDAMED 도입 기한이 있습니다. 이로 인해 수출업체들은 모두 사실상 ERP 현대화를 피할 수 없게 되었습니다. 48시간 이내에 유해사건 보고안에 대응해야 하는 제약사들은 실시간 추적성을 필수 요건으로 간주하게 되었으며, 출하 현황과 결함 발생 확률을 연계하는 AI 모듈에 대한 수요가 증가하고 있습니다. 남미, 중동 및 아프리카는 여전히 개발도상국이지만, 현지 공장이 모회사의 품질 시스템을 본받아 세계적인 브랜드로부터 우선 공급업체로서의 지위를 확보하기 위해 노력함에 따라, 도입이 착실히 진행되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.22According to Mordor Intelligence, the medical device and MedTech enterprise resource planning market size is projected to expand from USD 4.23 billion in 2025 and USD 4.61 billion in 2026 to USD 6.72 billion by 2031, registering a CAGR of 7.83% between 2026 and 2031.

This report is Segmented by Deployment Mode (Cloud-Based, On-Premise, and Hybrid), Component (Software, and Services), Organization Size (Large Enterprises, and Small and Medium Enterprises), End-User (Medical Device Manufacturers, Medtech Service Providers, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Medical Device And MedTech Enterprise Resource Planning Market Trends and Insights

Accelerating Regulatory Pressure for UDI and Quality Compliance

The May 28, 2026, deadline for mandatory EUDAMED submissions obliges manufacturers to load device master data, operator registrations, and vigilance reports into a central European database, prompting ERP vendors to release native connectors that populate serial numbers and certificates directly from product lifecycle modules. In the United States, the Quality Management System Regulation, which took effect on February 2, 2026, aligns computer system validation with ISO 13485:2016 and intensifies scrutiny of AI modules embedded in ERP quality workflows. Oracle responded with a Health Device Validation Program that ships pre-validated scripts, cutting in half the installation qualification cycles for Class III device makers. Japan's PMDA harmonization with ISO 13485 likewise boosts demand for multi-region templates capable of segregating FDA, EU, and Japanese establishment identifiers within a single master-data hierarchy. Collectively, these mandates nudge procurement decisions toward platforms that guarantee regulator-ready upgrades on a quarterly cadence.

Shift Toward Cloud-Native SaaS ERP Among Mid-Sized MedTech Firms

Subscription pricing that begins at USD 150 per user per month slashes the USD 2 million-plus capital outlay historically required for on-premise rollouts, bringing the Medical Device and MedTech enterprise resource planning market within reach of firms with USD 50 million to USD 500 million in annual sales. Microsoft's Dynamics 365 deployments during 2025 embedded electronic batch records and deviation workflows, enabling 21 CFR Part 11 compliance without custom code. European mid-sized manufacturers closed go-lives in as little as 9 months by leveraging pre-configured lot-traceability templates, while Asia-Pacific firms favored hybrid clouds that keep intellectual property data in local data centers in deference to China's Data Security Law. Rapid regulatory patching is an added lure: SaaS vendors can push new UDI formats or ISO revisions every quarter, whereas on-premises customers often defer upgrades to 3-year intervals. Even so, data-localization statutes continue to sustain hybrid demand, compelling providers to perfect low-latency synchronization between local quality systems and cloud financial ledgers.

High Validation and FDA Computer System Validation Costs

Despite the FDA's 2024 shift to risk-based Computer Software Assurance, Class III device makers still budget around USD 1.2 million per ERP module for installation, operational, and performance qualification testing. Each quarterly cloud update triggers regression scripts, impact assessments, and archival of executed test evidence, prolonging release timelines and inflating consulting fees. The European Union mirrors these demands by requiring audit trails to remain accessible for up to 15 years, driving parallel validation costs. Cloud vendors now market validation-as-a-service bundles, and Acumatica's turnkey documentation package costs USD 150,000; yet site-specific workflows and third-party integrations still mandate bespoke evidence generation. For a USD 50 million manufacturer, the expense equals 2.4% of annual revenue, underscoring why many SMEs postpone full-suite adoption.

Other drivers and restraints analyzed in the detailed report include:

- Rising Demand for Real-Time Traceability in Globalized Supply Chains

- Integration of IoT-Enabled Shop-Floor Data With ERP Platforms

- Cybersecurity Concerns Slowing Cloud ERP Adoption

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud deployments accounted for 54.98% of the Medical Device and MedTech enterprise resource planning market share in 2025 and are forecast to grow at an 8.43% CAGR through 2031, bolstered by mid-sized firms avoiding data-center investments of USD 2 million or more. Vendors are pulling end-of-support levers, SAP's 2027 sunset for ECC and Oracle's 2030 retirement of E-Business Suite, to prod customers toward SaaS subscriptions. The market size for on-premises instances will nonetheless persist among multinationals that prefer full control over software versioning and bespoke validation scripts. Hybrid architectures serve as a compromise for organizations subject to China's Data Security Law or the European Union's GDPR, allowing quality records to reside locally while planning engines run in global clouds.

Oracle's process-manufacturing connectors synchronize shop-floor batch data every few minutes, addressing latency anxieties that once hampered hybrid rollouts. Microsoft and third-party quality consultants package risk-based validation templates that reduce go-live by 40%, shrinking perceived disadvantages of SaaS release cadences. Even so, quarterly feature pushes force manufacturers to maintain evergreen validation teams, while on-premise customers can bundle changes into a single multi-year retrofit. Across all deployment types, buyers now elevate cybersecurity posture and regulator-ready audit trails above generic functionality checklists, shifting evaluation scorecards toward compliance automation.

Software licenses and subscriptions accounted for 69.77% of market revenue in 2025, yet the services category is growing at an 8.23% CAGR as validation complexity increases. Implementation projects consume 12-18 months, with validation tasks accounting for up to 40% of billable hours, pressuring manufacturers to outsource Computer Software Assurance documentation to life-sciences specialists. The market for managed services is expanding as clients adopt continuous-compliance contracts that bundle quarterly validation, patch management, and regulatory monitoring services.

Infosys and Tricentis now automate regression testing during SAP S/4HANA migrations, reducing test-case generation by 40% and trimming overall project budgets. Data-migration consultancies likewise flourish as manufacturers cleanse decades of lot-traceability records before moving to multi-tenant clouds. Training engagements are another bright spot; quality engineers and supply-chain planners require upskilling to interpret AI-generated forecasts without violating validation protocols. With AI modules increasingly embedded at no extra software charge, revenue shifts downstream to advisory, training, and application-management add-ons that keep systems audit-ready.

Geography Analysis

North America accounted for 38.39% of the market in 2025, propelled by stringent FDA oversight and a dense population of multinational device makers. The new Quality Management System Regulation obliges firms to re-validate ERP controls, spurring a wave of validation-as-a-service contracts. Post-merger consolidations, such as Boston Scientific's Axonics integration, underscore how acquisitions catalyze full-suite S/4HANA migrations that unify 16 or more manufacturing sites under a single global ledger. Canada and Mexico are emerging as nearshore contract-manufacturing hubs that install cloud ERP systems to meet the real-time traceability requirements of U.S. sponsors.

Asia-Pacific is the fastest-growing region, expanding at an 8.83% CAGR through 2031. China's phased UDI rollout for Class III devices in 2024 and Class II in 2025 obliges domestic factories to deploy serial-number and EUDAMED-style connectors, steering investment toward platforms that can align with both European and U.S. identifiers. India's Production Linked Incentive scheme reimburses up to 5% of incremental sales for plants equipped with IoT-enabled ERP, accelerating adoption among greenfield projects. South Korea subsidizes sensor-driven smart factories, while Japan's Society 5.0 agenda incentivizes IoT-ERP convergence among Tier 2 suppliers seeking ISO 13485 harmonization.

Europe maintains substantial share, anchored by the Medical Device Regulation and the May 2026 EUDAMED deadline that effectively forces ERP modernization for any exporter. Manufacturers racing to meet the 48-hour adverse-event reporting proposal now view real-time traceability as a must-have, sparking demand for AI modules that correlate shipment conditions with defect probabilities. South America and the Middle East and Africa remain nascent but show steady uptake as local plants aim to mirror parent-company quality systems and gain preferred-supplier status with global brands.

- SAP SE

- Oracle Corporation

- Microsoft Corporation

- Infor Inc.

- QAD Inc.

- Epicor Software Corporation

- Sage Group Plc

- IFS AB

- SYSPRO (Pty) Ltd.

- Plex Systems, Inc.

- Rootstock Software, Inc.

- Dassault Systemes SE

- Siemens Industry Software Inc.

- Korber Pharma Software GmbH

- Exact Holding B.V.

- Acumatica, Inc.

- Workday, Inc.

- Priority Software Ltd.

- Abas Software GmbH

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerating Regulatory Pressure for UDI and Quality Compliance

- 4.2.2 Shift Toward Cloud-native SaaS ERP Among Mid-sized MedTech Firms

- 4.2.3 Rising Demand for Real-time Traceability in Globalized Supply Chains

- 4.2.4 Integration of IoT-enabled Shop-floor Data with ERP Platforms

- 4.2.5 Surge in Post-merger System Consolidations in Medical Device Sector

- 4.2.6 Increasing Adoption of AI-driven Demand Forecasting Modules

- 4.3 Market Restraints

- 4.3.1 High Validation and FDA Computer System Validation Costs

- 4.3.2 Cybersecurity Concerns Slowing Cloud ERP Adoption

- 4.3.3 Skills Gap in ERP Data Governance within MedTech SMEs

- 4.3.4 Legacy MES-ERP Integration Complexities in Brownfield Plants

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Mode

- 5.1.1 Cloud-Based

- 5.1.2 On-Premise

- 5.1.3 Hybrid

- 5.2 By Component

- 5.2.1 Software

- 5.2.2 Services

- 5.3 By Organization Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises

- 5.4 By End-user

- 5.4.1 Medical Device Manufacturers

- 5.4.2 MedTech Service Providers

- 5.4.3 Contract Manufacturing Organizations

- 5.4.4 Clinical Research Organizations

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 Germany

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 United Arab Emirates

- 5.5.5.1.2 Saudi Arabia

- 5.5.5.1.3 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Egypt

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 SAP SE

- 6.4.2 Oracle Corporation

- 6.4.3 Microsoft Corporation

- 6.4.4 Infor Inc.

- 6.4.5 QAD Inc.

- 6.4.6 Epicor Software Corporation

- 6.4.7 Sage Group Plc

- 6.4.8 IFS AB

- 6.4.9 SYSPRO (Pty) Ltd.

- 6.4.10 Plex Systems, Inc.

- 6.4.11 Rootstock Software, Inc.

- 6.4.12 Dassault Systemes SE

- 6.4.13 Siemens Industry Software Inc.

- 6.4.14 Korber Pharma Software GmbH

- 6.4.15 Exact Holding B.V.

- 6.4.16 Acumatica, Inc.

- 6.4.17 Workday, Inc.

- 6.4.18 Priority Software Ltd.

- 6.4.19 Abas Software GmbH

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment