|

시장보고서

상품코드

2063423

AI 통합형 ERP(전사적 자원 계획) : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)AI-Integrated Enterprise Resource Planning - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

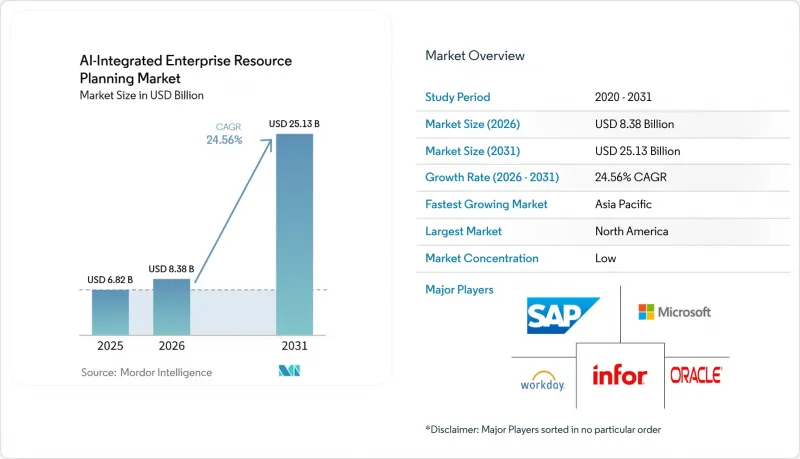

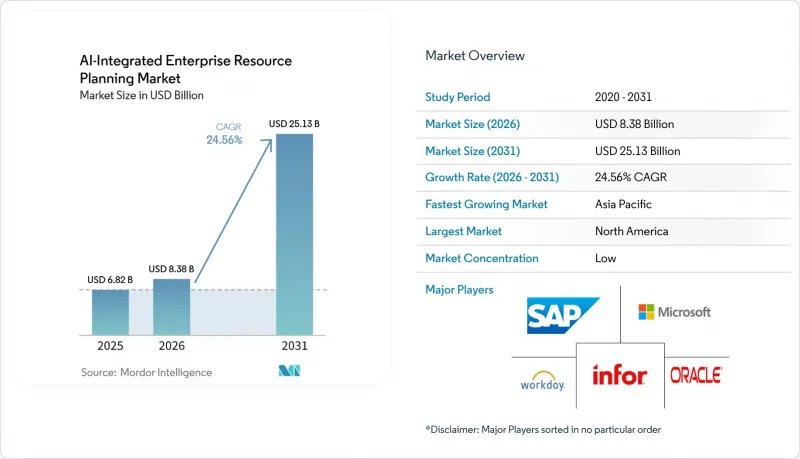

Mordor Intelligence에 의하면, AI 통합형 ERP(전사적 자원 계획) 시장 규모는 2026년 83억 8,000만 달러에서 2031년에는 251억 3,000만 달러에 이를 것으로 예측되며, 2026년부터 2031년에 걸쳐 CAGR은 24.56%를 나타낼 전망입니다.

본 보고서는 도입 모델(클라우드, On-Premise, 하이브리드), 구성 요소(소프트웨어 및 서비스), 기업 규모(대기업 및 중소기업), 업종(제조업, BFSI(은행 및 금융 및 보험), 기타), 업무 기능(재무 및 회계, 기타) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 AI 통합형 ERP(기업 자원 계획) 시장 동향과 인사이트

AI를 접목한 클라우드 네이티브 ERP로의 전환이 가속화되고 있습니다.

세계 기업들은 일반적으로 본사에서는 SAP S/4HANA나 Oracle Fusion과 같은 단일 인스턴스를 유지하면서, 자회사에는 NetSuite나 Microsoft Dynamics 365 Business Central과 같이 더 가볍고 민첩성이 뛰어난 클라우드 제품군을 도입하고 있습니다. 이러한 허브 앤 스포크형 아키텍처는 전 세계적인 재무 통합과 지역별 업무상의 유연성 사이에서 균형을 이루고 있습니다. 제조, 유통 또는 서비스 워크플로우를 패키지화한 사전 설정된 템플릿을 통해 도입이 효율화되어, 지역 법인은 4개월도 채 되지 않아 본격적인 가동을 시작할 수 있습니다. 이는 기존에 풀 스케일 전개에 보통 1년 이상이 소요되었던 점에 비추어 볼 때, 상당한 개선이라고 할 수 있습니다. 또한, 매일 밤 수행되는 동기화를 통해 이전가격 규정을 준수하는 한편, 현지 팀은 본사 차원의 변경 관리 절차를 거치지 않고도 조달 규정을 변경할 수 있는 권한을 보유하고 있습니다. 이러한 접근 방식을 통해 조직은 중앙집권적인 감독 체제를 유지하면서도 지역 차원에서의 적응성을 높일 수 있게 됩니다.

공급망 혼란 속 실시간 예측 분석에 대한 수요

제조업체와 소매업체들은 업무 효율을 높이기 위해 항만의 혼잡 상황, 기상 이상 경보, 지정학적 지표 등의 외부 신호를 계획 엔진에 직접 통합하는 움직임을 강화하고 있습니다. 이러한 예측 모델을 통해 기업은 생산 일정 변경, 화물 우회 운송, 안전 재고 재조정을 선제적으로 수행함으로써, 품절이 더 큰 혼란으로 번지는 것을 방지할 수 있습니다. 예를 들어, AI 통합형 ERP(전사적 자원 관리) 시스템과 연동된 실시간 가시화 플랫폼을 도입한 자동차 및 가전 제조업체는 계획 주기를 3분의 1로 단축하는 데 성공했습니다. 또한, 이들 기업은 긴급 배송 비용을 대폭 절감함으로써 이러한 통합이 가져다주는 구체적인 이점을 입증하고 있습니다. 이러한 새로운 시도를 통해 기존의 대시보드는 단순한 상황 설명 도구에서 벗어나, 시정 조치를 자율적으로 실행할 수 있는 첨단 처방형 엔진으로 변모했으며, 이를 통해 의사결정 프로세스가 합리화되고 공급망 전반의 회복탄력성이 향상되고 있습니다.

규제 산업 분야의 고도화된 데이터 보안 및 규정 준수 문제

의료 및 은행 업계의 사업자는 훈련 데이터가 승인된 관할 구역 내에 보관되어 있으며, 감사 추적이 GDPR(EU 개인정보보호규정), HIPAA, SOX 등의 규정을 준수하고 있음을 입증해야 합니다. 이를 통해 기밀 데이터가 안전하고 투명하게 처리될 것이 보장됩니다. 그러나 규제상의 우려를 해소하기 위해 많은 조직에서는 AI가 생성한 분개 기록과 병행하여 수동 검토를 실시했습니다. 이러한 검토 절차는 규제 당국과의 신뢰 관계를 구축하기 위한 목적이지만, AI를 통한 자동화가 약속하는 효율성 향상을 저해하는 경우가 종종 있습니다. 이러한 과제를 극복하기 위해, 새로운 페더레이티드 러닝 기술이 기밀 데이터를 관할 구역 간에 전송하지 않고도 로컬에서 모델 훈련을 가능하게 함으로써 잠재적인 해결책을 제시하고 있습니다. 그러한 가능성에도 불구하고, 페더레이티드 러닝의 대규모 도입은 여전히 제한적이며, 이를 성공적으로 운영하고 있는 엔터프라이즈 제품군은 거의 없습니다.

부문별 분석

규제 대상 기업들은 기밀 기록을 사내 방화벽 내에 보관해야 하고, 현장 설비에 대해 밀리초 단위의 응답 시간이 필요하기 때문에 On-Premise 도입은 2025년 매출의 72.13%를 차지했습니다. 그러나 클라우드 기반 AI 통합형 기업 자원 계획(ERP) 시장 규모는 2031년까지 연평균 성장률(CAGR) 25.16%로 확대될 것으로 전망됩니다. 벤더가 최첨단 코파일럿 기능을 SaaS 버전에만 제한하고 있기 때문에 재무 관리자는 핵심 원장이 On-Premise에 남아 있는 경우에도 모듈의 단계적 이전을 추진하는 경우가 많습니다.

하이브리드 방식의 접근법에서는 On-Premise 데이터 레이크와 클라우드상의 분석 샌드박스를 결합합니다. 데이터 보관에 관한 엄격한 법률이 있는 아시아 국가들의 기업에서는 개인 데이터를 자국의 클라우드에 저장하면서, AI 훈련을 위해 익명화된 데이터 세트를 전 세계 각 지역으로 전송하는 사례가 늘고 있습니다. 개념 검증(PoC)의 성공 사례가 늘어남에 따라, 경영진은 업무 시간 외에 기밀성이 높은 워크로드를 오프프레미스에서 실행하는 데 대한 거부감이 줄어들고 있으며, AI 통합형 ERP 시장 전반에서 이러한 전환 움직임이 가속화되고 있습니다.

대형 제조업체들은 독자적인 형식으로 데이터를 생성하는 프로그래머블 로직 컨트롤러(PLC)나 감시 제어 및 데이터 수집(SCADA) 시스템을 사용하고 있습니다. 이러한 시스템은 산업 공정의 자동화 및 모니터링에 필수적이지만, 생성된 데이터는 기업 자원 계획(ERP) 시스템과 호환되도록 하기 위해 종종 변환 계층이 필요합니다. 대부분의 경우, 이러한 맞춤형 코딩된 변환 레이어는 예측 유지보수 에이전트가 ERP의 작업 지시 모듈과 원활하게 통합되는 데 필수적입니다. 그러나 이러한 변환 레이어의 개발 및 유지보수에는 막대한 비용이 소요되어 통합 예산을 크게 증가시키며, 경우에 따라서는 핵심 소프트웨어 자체의 비용을 초과하기도 합니다. 또한, 시스템에 새로운 인터페이스가 도입될 때마다 보안 조치가 미흡한 연결이나 구식 프로토콜로 인해 취약점이 발생할 가능성이 있으며, 이는 사이버 보안상의 위험 요인이 될 우려가 있습니다.

이러한 과제를 해결하기 위해, 서로 다른 시스템 간의 연동을 간소화하는 솔루션으로서 로우코드 통합 허브가 등장했습니다. 이러한 허브는 대규모 맞춤형 코딩의 필요성을 줄여주어, 기업이 통합 작업을 효율화하고 관련 비용을 절감할 수 있게 해줍니다. 그러나 일부 과제를 완화하는 한편, 추가적인 라이선스 비용이나 규정 준수 및 보안을 확보하기 위한 견고한 거버넌스 프레임워크의 필요성 등, 새로운 과제도 수반합니다. 그 결과, 제조업체는 위험을 줄이면서 업무를 최적화하기 위해 기존의 맞춤형 코딩 기반 솔루션과 로우코드 플랫폼 간의 장단점을 신중하게 평가해야 합니다.

지역별 분석

북미는 2025년 매출의 37.89%를 차지했는데, 이는 공공 부문의 현대화와 소매·의료 분야의 적극적인 클라우드 전환에 힘입은 결과입니다. 미국 연방 정부의 프로그램만 해도 10년에 걸쳐 수십억 달러 규모의 계약이 체결되어 있습니다. 캐나다의 ‘클라우드 우선’ 조달 규정은 AI 통합형 전사적 자원 관리(ERP) 시장의 잠재적 규모를 더욱 확대하고, 데이터 소재지 관리를 현지화하는 컨설팅 프로젝트를 촉진하고 있습니다. 멕시코에서 일고 있는 니어쇼어링 열풍은 자동차 부품 제조업체들로 하여금 현지 공장과 미국 본사를 연결하는 2단계 아키텍처를 도입하도록 촉진하고 있습니다.

아시아태평양은 2026년부터 2031년까지 연평균 성장률(CAGR) 25.56%를 나타낼 것으로 예측되며, 이는 전 세계에서 가장 빠른 성장 속도입니다. 일본의 보조금 제도는 중소 제조업체의 라이선스 비용 부담을 경감시키고 있으며, 인도네시아의 데이터 현지화법은 전 세계 공급업체들이 국내 리전을 개설하도록 촉진하고 있고, 인도의 세무 디지털화 의무화는 중견 기업의 시스템 업그레이드를 가속화하고 있습니다. 중국의 규제상 국내 데이터센터 설치가 의무화되어 있으며, 이로 인해 전 세계 소프트웨어 공급업체와 국내 하이퍼스케일러 간의 합작 사업으로 프로젝트가 유도되고 있습니다. 호주와 한국에서는 사이버 보안 및 재해 복구 관련 인증이 중요시되고 있으며, 이에 따른 지역 예산이 더욱 확대되고 있습니다.

유럽에서는 규정 준수 규정이 세분화되어 있어 의사결정 주기가 길어지고, 성장 속도는 완만합니다. 영국에서 여러 부처에 걸쳐 진행된 SAP 전환은 부처 간 프로그램의 복잡성을 여실히 보여주고 있습니다. 독일의 제조업체들은 새로운 국경 조정 메커니즘에 맞추어 탄소 발자국을 추적하는 AI 에이전트를 도입하고 있는 반면, 프랑스의 의료 시스템에서는 로컬 호스팅이 가능해져야 비로소 클라우드 ERP가 도입되고 있습니다. 스페인과 이탈리아에서는 전자 청구서 시스템의 업그레이드가 가속화되고 있으며, 북유럽 국가들에서는 친환경 데이터센터 조달을 중시하고 있습니다. 남미, 중동 및 아프리카는 전체적으로 규모는 작지만 그 격차는 급속히 좁혀지고 있으며, 특히 정부가 세무 논리를 반영해야 하는 실시간 전자 청구서 의무화를 도입하고 있는 지역에서 이러한 현상이 두드러집니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.22According to Mordor Intelligence, the aI-integrated enterprise resource planning market size is expected to increase from USD 8.38 billion in 2026 to reach USD 25.13 billion by 2031, growing at a CAGR of 24.56% over 2026-2031.

This report is Segmented by Deployment Model (Cloud, On-Premise, and Hybrid), Component (Software and Services), Enterprise Size (Large Enterprises and Small and Medium Enterprises), Industry Vertical (Manufacturing, BFSI, and More), Business Function (Finance and Accounting, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global AI-Integrated Enterprise Resource Planning Market Trends and Insights

Accelerated Migration to Cloud-Native ERP With Embedded AI

Global corporations typically maintain a single instance of SAP S/4HANA or Oracle Fusion at their headquarters while equipping subsidiaries with lighter, more agile cloud suites such as NetSuite or Microsoft Dynamics 365 Business Central. This hub-and-spoke architecture balances global financial consolidation with localized operational flexibility. Pre-configured templates streamline deployment by packaging manufacturing, distribution, or service workflows, enabling regional entities to achieve go-live in less than 4 months. This is a significant improvement over the year or more typically required for a full-scale rollout. Additionally, nightly synchronization ensures compliance with transfer pricing regulations, while local teams retain the ability to modify procurement rules without triggering corporate-level change control processes. This approach allows organizations to maintain centralized oversight while fostering adaptability at the regional level.

Demand for Real-Time Predictive Analytics in Supply Chain Disruptions

Manufacturers and retailers are increasingly integrating external signals such as port-congestion updates, extreme-weather alerts, and geopolitical indices directly into their planning engines to enhance operational efficiency. These predictive models enable businesses to proactively reschedule production, reroute freight, and rebalance safety stock, preventing shortages from escalating into larger disruptions. For instance, automotive and consumer-electronics companies that have implemented real-time visibility platforms connected to AI-integrated enterprise resource planning market deployments have successfully reduced planning cycles by one-third. Additionally, these companies have significantly reduced expedited shipping costs, demonstrating the tangible benefits of such integrations. This emerging practice is transforming traditional dashboards from merely providing descriptive views into advanced prescriptive engines capable of autonomously executing corrective actions, thereby streamlining decision-making processes and improving overall supply chain resilience.

High Data-Security and Compliance Concerns in Regulated Industries

Healthcare and banking entities are required to demonstrate that training data remains confined within approved jurisdictions and that audit trails comply with regulations such as GDPR, HIPAA, or SOX. This ensures that sensitive data is handled securely and transparently. However, to address regulatory concerns, many organizations implement parallel manual reviews alongside AI-generated journal entries. These reviews are intended to build trust with regulators but often undermine the efficiency gains promised by AI automation. To overcome these challenges, emerging federated-learning techniques offer a potential solution by enabling local model training without transferring sensitive data across jurisdictions. Despite its promise, the adoption of federated learning at scale remains limited, as few enterprise suites have successfully operationalized it.

Other drivers and restraints analyzed in the detailed report include:

- Two-Tier ERP Adoption Among Multinational Subsidiaries

- AI-Driven Reduction in Implementation Time and Cost

- Integration Complexity With Legacy and Edge Systems

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

On-premises installations retained 72.13% of 2025 revenue because regulated enterprises keep sensitive records within corporate firewalls and require millisecond-level response times for shop-floor equipment. The AI-integrated enterprise resource planning market size for cloud deployments, however, is projected to climb at a 25.16% CAGR to 2031. Vendors reserve the most advanced copilots for SaaS editions, so financial controllers often champion gradual module migrations even when core ledgers stay on-site.

Hybrid approaches combine local data lakes with cloud analytics sandboxes. Asian organizations in countries with stringent data-residency laws increasingly store personal data on sovereign clouds while pushing anonymized datasets to global regions for AI training. As more proofs of concept succeed, boardrooms become more comfortable staging sensitive workloads off-premises during non-business hours, accelerating broader migration waves across the AI-integrated enterprise resource planning market.

Large manufacturers use programmable logic controllers (PLCs) and supervisory control and data acquisition (SCADA) systems that generate data in proprietary formats. These systems are critical for automating and monitoring industrial processes, but the data they produce often requires translation layers to be compatible with enterprise resource planning (ERP) systems. These translation layers, frequently custom-coded, are essential for enabling predictive maintenance agents to seamlessly integrate with ERP work-order modules. However, the development and maintenance of these layers can significantly increase integration budgets, often surpassing the costs of the core software itself. Additionally, each new interface introduced into the system poses a potential cybersecurity risk, as vulnerabilities can arise from poorly secured connections or outdated protocols.

To address these challenges, low-code integration hubs have emerged as a solution to simplify connecting disparate systems. These hubs reduce the need for extensive custom coding, allowing businesses to streamline integration efforts and lower associated costs. However, while they alleviate some of the pain points, they also come with their own set of challenges, including additional licensing fees and the need for robust governance frameworks to ensure compliance and security. As a result, manufacturers must carefully evaluate the trade-offs between traditional custom-coded solutions and low-code platforms to optimize their operations while mitigating risks.

Geography Analysis

North America accounted for 37.89% of 2025 revenue, driven by public-sector modernizations and aggressive cloud migrations across retail and healthcare. United States federal programs alone represent multi-billion-dollar deals that span a decade. Canadian cloud-first procurement rules further expand the addressable AI-integrated enterprise resource planning market and fuel consulting engagements that localize data-residency controls. Mexico's nearshoring boom entices automotive suppliers to adopt two-tier architectures linking local plants with U.S. headquarters.

Asia-Pacific is set to record a 25.56% CAGR from 2026-2031, the fastest pace worldwide. Japanese subsidies help small manufacturers offset license fees, Indonesian data-localization laws push global vendors to open domestic regions, and Indian tax-digitization mandates accelerate mid-market upgrades. Chinese regulations require in-country data centers, steering deals to joint ventures between global publishers and domestic hyperscalers. Australia and South Korea emphasize cybersecurity and disaster recovery certifications, further expanding regional budgets.

Europe grows more slowly because fragmented compliance rules prolong decision cycles. The United Kingdom's multi-department SAP migration illustrates the complexity of cross-agency programs. German manufacturers add AI agents to track carbon footprints in line with new border-adjustment mechanisms, while French health systems adopt cloud ERP only after local hosting becomes available. Spain and Italy accelerate e-invoicing upgrades, and the Nordics emphasize green-data-center sourcing. South America, the Middle East, and Africa collectively represent a smaller but fast-closing gap, especially where governments introduce real-time e-invoice mandates that require embedded tax logic.

- SAP SE

- Oracle Corporation

- Microsoft Corporation

- Sage Group Plc

- Infor Inc.

- Epicor Software Corporation

- Acumatica, Inc.

- Workday, Inc.

- Priority Software Ltd.

- Odoo SA

- QAD Inc.

- Ramco Systems Limited

- Plex Systems, Inc.

- SYSPRO (Pty) Ltd.

- Rootstok Software

- Deltek, Inc.

- Zoho Corporation Pvt. Ltd.

- IFS AB

- Unit4 N.V.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerated Migration to Cloud-Native ERP with Embedded AI

- 4.2.2 Demand for Real-Time Predictive Analytics in Supply Chain Disruptions

- 4.2.3 Two-Tier ERP Adoption among Multinational Subsidiaries

- 4.2.4 AI-Driven Reduction in Implementation Time and Cost

- 4.2.5 Mid-Market Appetite for Composable Low-Code ERP Modules

- 4.2.6 Government Digital Transformation Mandates and Incentives

- 4.3 Market Restraints

- 4.3.1 High Data-Security and Compliance Concerns in Regulated Industries

- 4.3.2 Integration Complexity with Legacy and Edge Systems

- 4.3.3 Shortage of AI-Skilled ERP Implementation Talent

- 4.3.4 Vendor Lock-In and Escalating Subscription Costs

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Model

- 5.1.1 Cloud

- 5.1.2 On-Premise

- 5.1.3 Hybrid

- 5.2 By Component

- 5.2.1 Software

- 5.2.2 Services

- 5.3 By Enterprise Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises

- 5.4 By Industry Vertical

- 5.4.1 Manufacturing

- 5.4.2 BFSI

- 5.4.3 Healthcare

- 5.4.4 Retail and Distribution

- 5.4.5 IT and Telecom

- 5.4.6 Government and Utilities

- 5.4.7 Other Industry Verticals

- 5.5 By Business Function

- 5.5.1 Finance and Accounting

- 5.5.2 Human Resource Management

- 5.5.3 Supply Chain and Logistics

- 5.5.4 Customer Relationship Management

- 5.5.5 Inventory and Work Order Management

- 5.5.6 Other Business Functions

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 United Kingdom

- 5.6.3.2 Germany

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 United Arab Emirates

- 5.6.5.1.2 Saudi Arabia

- 5.6.5.1.3 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Egypt

- 5.6.5.2.3 Rest of Africa

- 5.6.5.2.4 Saudi Arabia

- 5.6.5.2.5 Rest of Middle East

- 5.6.5.3 Africa

- 5.6.5.3.1 South Africa

- 5.6.5.3.2 Egypt

- 5.6.5.3.3 Rest of Africa

- 5.6.5.1 Middle East

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 SAP SE

- 6.4.2 Oracle Corporation

- 6.4.3 Microsoft Corporation

- 6.4.4 Sage Group Plc

- 6.4.5 Infor Inc.

- 6.4.6 Epicor Software Corporation

- 6.4.7 Acumatica, Inc.

- 6.4.8 Workday, Inc.

- 6.4.9 Priority Software Ltd.

- 6.4.10 Odoo SA

- 6.4.11 QAD Inc.

- 6.4.12 Ramco Systems Limited

- 6.4.13 Plex Systems, Inc.

- 6.4.14 SYSPRO (Pty) Ltd.

- 6.4.15 Rootstok Software

- 6.4.16 Deltek, Inc.

- 6.4.17 Zoho Corporation Pvt. Ltd.

- 6.4.18 IFS AB

- 6.4.19 Unit4 N.V.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment