|

시장보고서

상품코드

2063410

남미의 공급망 컨설팅 서비스 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)South America Supply Chain Consulting Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

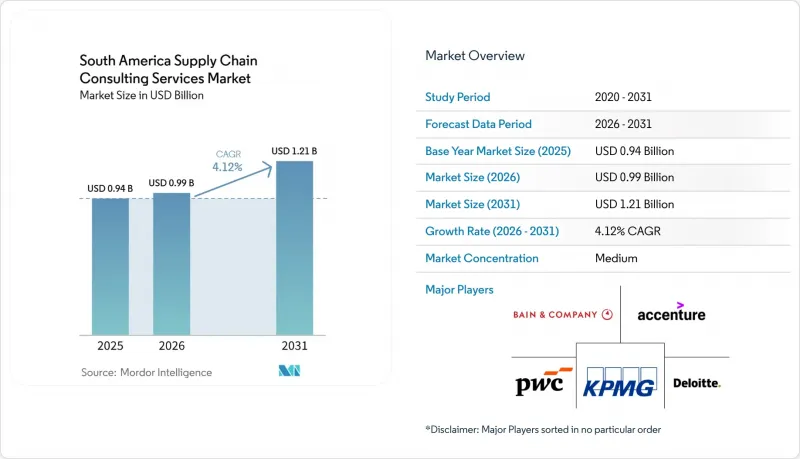

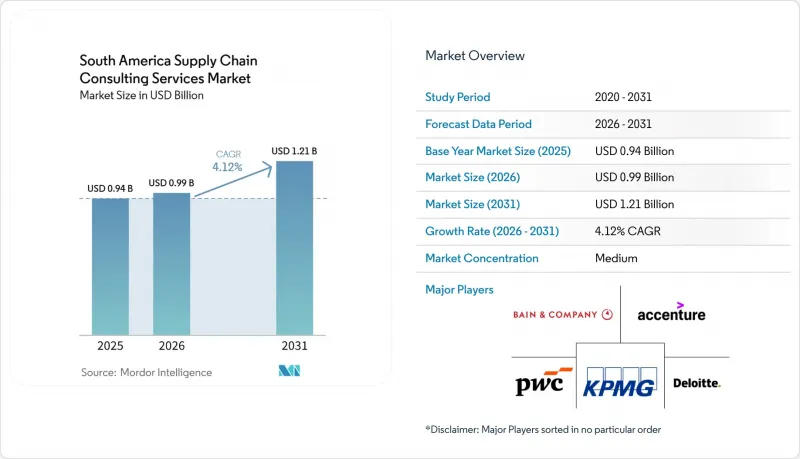

Mordor Intelligence에 의하면, 남미의 공급망 컨설팅 서비스 시장 규모는 2025년에 9억 4,100만 달러로 평가되었고, 2026년 9억 8,700만 달러로 추정되고, 2031년까지 12억 800만 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 4.12%를 나타낼 전망입니다.

본 보고서는 서비스 유형별(공급망 전략 및 네트워크 설계, 조달 및 소싱 등), 최종 사용자 산업별(소매 및 전자상거래, 제조업 등), 컨설팅 방식별(프로젝트 기반 컨설팅, 매니지드 서비스 등), 조직 규모별(대기업, 중소기업) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제공됩니다.

남미의 공급망 컨설팅 서비스 시장 동향 및 인사이트

디지털 공급망 혁신의 도입 확대

기업들은 분산된 ERP, 조달, 물류 시스템을 프로세스 오케스트레이션 및 예측 분석을 위한 AI가 통합된 클라우드 플랫폼 위에 통합하고 있습니다. 연간 지출액이 140억 달러에 달하는 20개 이상의 구매 도구를 Coupa 플랫폼 아래 통합하는 Vale의 프로그램은 자산이 풍부한 대기업들이 시범 프로젝트에서 본격적인 대규모 실행 단계로 넘어가고 있음을 보여줍니다. 제약 회사인 우니아오 키미카(Uniao Quimica)도 SAP Ariba를 활용해 비슷한 길을 걷고 있으며, 지능형 제안 평가 기능을 추가한 시스템의 2026년 5월 가동을 목표로 하고 있습니다. 또한, 이 지역에서는 에이전트형 AI 실험도 진행 중이며, YPF와 Globant는 조달 및 재고 관리 워크플로우 전반에 46개의 디지털 에이전트를 도입하여 직원들이 전략적 소싱 업무에 전념할 수 있도록 하고 있습니다. 많은 기업이 데이터 아키텍처 설계, 프로세스 재설계 및 변경 관리 프로그램 실행에 있어 외부 지원이 필요하기 때문에 컨설팅 기업들은 그 혜택을 누리고 있습니다.

기업 전체 차원에서의 비용 최적화의 필요성

이 지역의 물류 비효율성은 여전히 수익성을 구조적으로 압박하고 있으며, 비용은 선진국 경제의 거의 2배에 달할 전망입니다. 아마존 브라질이 시나리오 모델링을 위해 Optilogic사의 Cosmic Frog를 도입한 것과 같은 사례는 화주들이 속도, 서비스, 비용 간의 상충 관계를 정량화하고 있음을 보여줍니다. 소매 기업 경영진을 대상으로 한 조사에 따르면, 무역 관련 비용이 상승할 경우 66%가 네트워크 재구축이나 공급업체 다각화를 계획하고 있으며, 이는 네트워크 설계 및 재고 최적화에 중점을 둔 컨설팅 프로젝트의 견실한 수주 파이프라인으로 이어지고 있습니다. 미주개발은행(IDB)은 디지털화를 통해 물류 비용을 최대 15%까지 절감할 수 있을 것으로 추정하고 있으며, 이는 컨설턴트가 계약을 성사시키기 위해 제시하는 구체적인 ROI(투자 수익률) 주장을 뒷받침하고 있습니다.

숙련된 공급망 전문가의 부족

OECD 조사에 따르면, 중소기업은 자동화 위험이 높은 일상 업무의 상당 부분을 담당하고 있음에도 불구하고, 고도의 교육 프로그램에 대한 접근성이 부족하여 데이터 분석 및 공정 엔지니어링 분야의 인력 부족 현상이 발생하고 있습니다. KPMG는 브라질과 아르헨티나 전역에서 인력 부족으로 인해 프로젝트 기간이 연장되고 일당 비용이 상승함에 따라, 컨설팅 프로젝트의 확장성이 제한될 것이라고 경고하고 있습니다. 이를 완화하기 위해 각 기업은 역량 개발을 위한 부트캠프를 시작하거나, 대학과 제휴하여 주니어 애널리스트를 위한 양성 프로그램을 마련하고 있습니다.

부문별 분석

2025년, 디지털 공급망 전환은 남미 공급망 컨설팅 서비스 시장 점유율의 21.78%를 차지했으며, 기업들이 종단간 가시성과 AI 기반 의사결정 엔진을 우선시하고 있음을 여실히 보여주었습니다. 발레(Vale)사가 90개 이상의 내부 통제를 자동화하는 프로그램은 수년에 걸친 디지털화 노력의 규모를 잘 보여줍니다. 아마존 브라질의 실시간 네트워크 트윈은 물류 시나리오를 지속적으로 테스트하며 수요를 더욱 촉진하고 있습니다. 지속가능성 및 친환경 공급망 관련 활동은 규모는 작지만, 2031년까지 연평균 성장률(CAGR) 7.31%로 확대되고 있습니다. 이는 국채형 그린본드의 수익과 브라질 레알 표시 세액 공제가 탈탄소화 로드맵의 자금원이 되고 있기 때문입니다. 이에 따라 각 컨설팅 기업들은 탄소 회계 모듈을 핵심 혁신 업무에 통합함으로써 투자 회수 기간을 단축하는 동시에, ESG 관련 서비스 분야의 남미 공급망 컨설팅 서비스 시장 규모를 확대되고 있습니다.

이 두 가지 가장 빠르게 성장하는 분야 외에도, 네트워크 설계와 조달 최적화는 여전히 수요가 끊이지 않는 분야입니다. IDB가 예측한 780억 달러 규모의 수출 증가 가능성은 사업 거점 분석의 업데이트를 촉진하고 있는 반면, YPF의 에이전트형 AI 실험은 자율적인 공급업체 평가로의 전환을 시사하고 있습니다. 서비스 구성은 리스크 및 복원력 모델링을 통해 보완되고 있으며, 고객들은 사이버, 기후, 지정학적 스트레스 테스트를 통합한 디지털 트윈의 도입을 요구하고 있습니다. 이러한 성장은 남미공급망 컨설팅 서비스 시장이 분절화된 자문 서비스에서 통합 플랫폼을 활용한 솔루션으로 지속적으로 진화하고 있음을 보여줍니다.

2025년, 제조업은 남미 공급망 컨설팅 서비스 시장의 35.59%를 차지했으며, 이는 복잡한 자동차 및 광업 밸류체인에 힘입은 결과였습니다. 브라질의 자동차 부품 매출액은 2024년에 2,591억 레알(508억 달러)에 달했으며, 이에 따라 공급업체의 합리화 및 패키지 재설계에 관한 컨설팅 프로젝트가 잇달아 진행되었습니다. 주요 광업 기업들은 처리 능력 향상과 디지털 허가 취득을 추구하고 있으며, 공급망의 디지털화를 점점 더 적극적으로 도입하고 있는 페루의 515억 5,000만 달러 규모 프로젝트 파이프라인이 그 대표적인 사례입니다. 에너지 및 유틸리티 부문은 규모는 작지만 연평균 성장률(CAGR) 6.02%로 가장 빠르게 성장하고 있는 분야입니다. 이는 국제재생에너지기구(IRENA)가 2050년까지 연간 5,000억 달러의 재생에너지 투자가 필요할 것으로 예측하고 있기 때문입니다. 이러한 성장에 힘입어, 송전망 물류, 전해조 조달, 수소 회랑 계획에 특화된 남미공급망 컨설팅 서비스 시장 규모가 확대되고 있습니다.

소매 및 전자상거래 분야의 사업들은 물류 센터 확충이라는 흐름에 편승하고 있습니다. CEVA가 운영하는 6만 7,000제곱미터 규모의 아마존 물류 센터(하루 13만 5,000개의 물품을 처리 가능)는 옴니채널 브랜드가 프로세스 설계와 창고 자동화를 필요로 하는 규모가 얼마나 큰지를 보여줍니다. 제약, 식품, 음료 기업들도 마찬가지로 콜드체인의 현대화, 재생 소재 함유율 관련 규정 준수, 시리얼화 통합을 위해 컨설턴트를 채용하고 있습니다. 고객층의 다양화는 상품 시장의 경기 사이클이 둔화되더라도 견고한 수익 기반을 뒷받침하는 요인이 됩니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.22According to Mordor Intelligence, the south america supply chain consulting services market size was valued at USD 0.941 billion in 2025 and estimated to grow from USD 0.987 billion in 2026 to reach USD 1.208 billion by 2031, at a CAGR of 4.12% during the forecast period (2026-2031).

This report is Segmented by Service Type (Supply Chain Strategy and Network Design, Procurement and Sourcing, and More), End-User Industry (Retail and Ecommerce, Manufacturing, and More), Consulting Approach (Project-Based Consulting, Managed Services, and More), Organization Size (Large Enterprises, Smes), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

South America Supply Chain Consulting Services Market Trends and Insights

Rising Adoption of Digital Supply Chain Transformation

Enterprises are consolidating fragmented ERP, procurement, and logistics systems onto cloud platforms that embed AI for process orchestration and predictive analytics. Vale's program to unify more than 20 purchasing tools under Coupa, covering USD 14 billion in annual spend, showcases how large asset-heavy firms are moving from pilot projects to scaled execution. Pharmaceutical manufacturer Uniao Quimica is following a similar path with SAP Ariba, targeting a May 2026 go-live that adds intelligent proposal evaluation. The region is also experimenting with agentic AI, as YPF and Globant deployed 46 digital agents across procurement and inventory workflows, freeing staff for strategic sourcing. Consulting firms benefit because most enterprises need external support to blueprint data architecture, redesign processes, and run change-management programs.

Need for Cost Optimization Across Enterprises

Regional logistics inefficiencies remain a structural drain on profitability, with costs sitting at almost double those in developed economies. Platform deployments such as Amazon Brazil's use of Optilogic's Cosmic Frog for scenario modeling illustrate how shippers are quantifying trade-offs among speed, service, and cost. Surveys of retail executives indicate that 66% plan to reconfigure their networks or diversify suppliers if trade-related costs rise, feeding a robust pipeline of consulting engagements focused on network design and inventory rightsizing. The Inter-American Development Bank estimates digitalization can shave up to 15% off logistics costs, underscoring the tangible ROI narrative that consultants use to close deals.

Shortage of Skilled Supply Chain Professionals

OECD research shows that SMEs perform most routine tasks at high risk of automation yet lack access to advanced training programs, leaving a gap in data analytics and process-engineering talent. KPMG warns that staffing constraints lengthen project timelines and raise day rates across Brazil and Argentina, limiting the scalability of consulting engagements. To mitigate, firms are launching capacity-building boot camps and partnering with universities to create feeder programs for junior analysts.

Other drivers and restraints analyzed in the detailed report include:

- Nearshoring Trends Driving Regional Supply Chain Reconfiguration

- Government Incentives for Green Logistics Initiatives

- High Consulting Fees for Small and Medium Enterprises

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Digital Supply Chain Transformation captured 21.78% of the South America supply chain consulting services market share in 2025, underscoring companies' prioritization of end-to-end visibility and AI-driven decision engines. Vale's program to automate more than 90 internal controls underscores the scale of multi-year digital mandates. Demand is reinforced by Amazon Brazil's real-time network twin, which continuously tests fulfillment scenarios. Sustainability and Green Supply Chain mandates, although smaller, are expanding at a 7.31% CAGR to 2031 as sovereign green-bond proceeds and BRL-denominated tax credits finance decarbonization roadmaps. Consultants are thus integrating carbon accounting modules into core transformation work, shortening payback horizons and widening the South America supply chain consulting services market size for ESG-linked offerings.

Beyond the two fastest-moving areas, network design and procurement optimization remain evergreen lines. IDB's projection of a potential USD 78 billion export uplift drives renewals of footprint analyses, while YPF's agentic AI experiment signals a pivot toward autonomous supplier evaluation. The service mix is rounded out by risk and resilience modeling, with clients requesting digital twins that overlay cyber, climate, and geopolitical stress tests. These expansions illustrate how the South America supply chain consulting services market continues to evolve from siloed advisory toward integrated, platform-enabled solutions.

Manufacturing commanded 35.59% of the South America supply chain consulting services market in 2025, led by complex automotive and mining value chains. Brazil's auto-parts revenue reached BRL 259.1 billion (USD 50.8 billion) in 2024, drawing consulting assignments in supplier rationalization and packaging redesign. Mining majors seek throughput gains and digital permitting, illustrated by Peru's USD 51.55 billion project pipeline that increasingly embeds supply-chain digitization. Energy and utilities, while smaller, is the fastest-growing vertical at 6.02% CAGR as IRENA forecasts USD 500 billion in annual renewable investment needs through 2050. This growth enlarges the South America supply chain consulting services market size devoted to grid logistics, electrolyser sourcing, and hydrogen corridor planning.

Retail and e-commerce engagements are riding a wave of fulfillment-center expansion. CEVA's 67,000 square-meter Amazon site, capable of 135,000 daily packages, showcases the scale at which omnichannel brands require process mapping and warehouse automation. Pharma, food, and beverage firms are likewise hiring consultants to modernize cold chains, comply with recycled-content mandates, and integrate serialization. The broadening client mix underpins a resilient revenue base even when commodity cycles soften.

List of Companies Covered in this Report:

- Accenture plc

- Deloitte Touche Tohmatsu Ltd

- KPMG International Ltd

- PricewaterhouseCoopers International Ltd

- Bain & Company Inc.

- Boston Consulting Group Inc.

- McKinsey & Company Inc.

- Ernst & Young Global Ltd

- International Business Machines Corporation (IBM Consulting)

- Capgemini SE

- Genpact Limited

- Chainalytics LLC

- NTT DATA Corporation

- Oliver Wyman Inc.

- AlixPartners LLP

- Kearney

- Infosys Limited

- Tata Consultancy Services Limited

- GEP Worldwide

- Alvarez & Marsal Holdings LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Adoption of Digital Supply Chain Transformation

- 4.2.2 Need for Cost Optimization Across Enterprises

- 4.2.3 Increasing Complexity of Regional Trade Regulations

- 4.2.4 Nearshoring Trends Driving Regional Supply Chain Reconfiguration

- 4.2.5 Rapid Growth of E-commerce Fulfillment Hubs in Secondary Cities

- 4.2.6 Government Incentives for Green Logistics Initiatives

- 4.3 Market Restraints

- 4.3.1 Shortage of Skilled Supply Chain Professionals

- 4.3.2 High Consulting Fees for Small and Medium Enterprises

- 4.3.3 Political Instability Affecting Long-Term Consulting Contracts

- 4.3.4 Fragmented Infrastructure Limiting Consulting Implementation ROI

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Ecosystem Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Buyers

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Service Type

- 5.1.1 Supply Chain Strategy and Network Design

- 5.1.2 Procurement and Sourcing

- 5.1.3 Logistics and Distribution Optimization

- 5.1.4 Inventory and Demand Planning

- 5.1.5 Digital Supply Chain Transformation

- 5.1.6 Sustainability and Green Supply Chain

- 5.1.7 Risk and Resilience Consulting

- 5.1.8 Other Service Types

- 5.2 By End-User Industry

- 5.2.1 Retail and E-commerce

- 5.2.2 Manufacturing

- 5.2.3 Food and Beverage

- 5.2.4 Healthcare and Pharmaceuticals

- 5.2.5 Automotive

- 5.2.6 Consumer Packaged Goods

- 5.2.7 Energy and Utilities

- 5.2.8 Other End-User Industries

- 5.3 By Consulting Approach

- 5.3.1 Project-Based Consulting

- 5.3.2 Managed Services

- 5.3.3 Training and Capacity Building

- 5.3.4 Advisory and Benchmarking

- 5.3.5 Other Consulting Approaches

- 5.4 By Organization Size

- 5.4.1 Large Enterprises

- 5.4.2 Small and Medium Enterprises

- 5.5 By Geography

- 5.5.1 Brazil

- 5.5.2 Argentina

- 5.5.3 Colombia

- 5.5.4 Chile

- 5.5.5 Peru

- 5.5.6 Rest of South America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Accenture plc

- 6.4.2 Deloitte Touche Tohmatsu Ltd

- 6.4.3 KPMG International Ltd

- 6.4.4 PricewaterhouseCoopers International Ltd

- 6.4.5 Bain & Company Inc.

- 6.4.6 Boston Consulting Group Inc.

- 6.4.7 McKinsey & Company Inc.

- 6.4.8 Ernst & Young Global Ltd

- 6.4.9 International Business Machines Corporation (IBM Consulting)

- 6.4.10 Capgemini SE

- 6.4.11 Genpact Limited

- 6.4.12 Chainalytics LLC

- 6.4.13 NTT DATA Corporation

- 6.4.14 Oliver Wyman Inc.

- 6.4.15 AlixPartners LLP

- 6.4.16 Kearney

- 6.4.17 Infosys Limited

- 6.4.18 Tata Consultancy Services Limited

- 6.4.19 GEP Worldwide

- 6.4.20 Alvarez & Marsal Holdings LLC

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment