|

시장보고서

상품코드

2073581

아시아태평양의 전략 컨설팅 서비스 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Asia Pacific Strategic Consulting Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

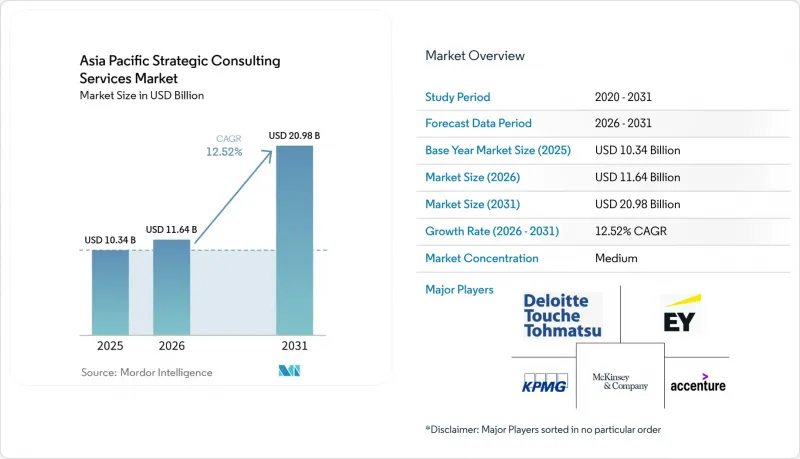

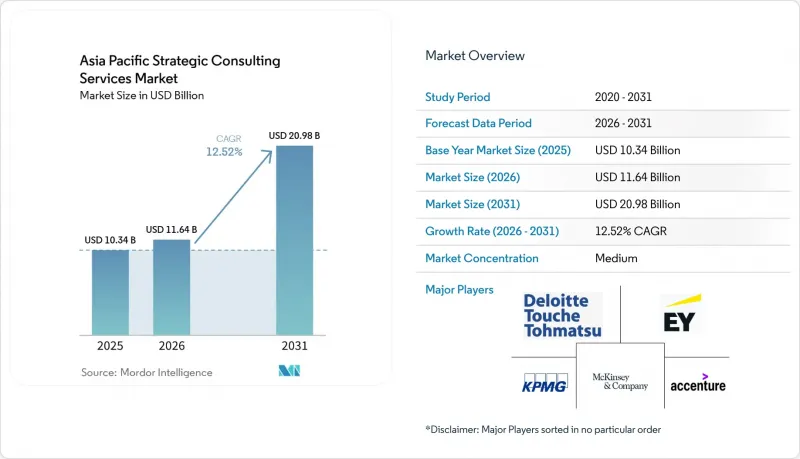

Mordor Intelligence에 의하면, 2026년 아시아태평양의 전략 컨설팅 서비스 시장 규모는 116억 4,000만 달러에 달할 것으로 예상되고, 2025년 103억 4,000만 달러에서 확대해, 2031년에는 209억 8,000만 달러에 이를 것으로 예측됩니다.

2026년부터 2031년까지의 연평균 성장률(CAGR)은 12.52%를 나타낼 것으로 전망됩니다.

본 보고서는 서비스 유형(기업 전략, 디지털 전략 등), 최종 사용자 산업(금융 서비스, 소매 및 소비재 등), 기업 규모(대기업, 중소기업), 제공 모델(온사이트 컨설팅, 원격/가상 컨설팅 등) 및 지역별로 분류되어 있습니다. 시장 전망치는 금액(달러)으로 표시되어 있습니다.

아시아태평양의 전략 컨설팅 서비스 시장 동향 및 인사이트

아시아태평양을 휩쓸고 있는 디지털 전환의 물결

이 지역의 기업들은 팬데믹으로 인한 혼란을 계기로 디지털 관련 지출을 가속화하고 있으며, 기존에 오프라인으로 운영되던 조직의 44%가 2025년까지 비자동화 프로세스의 절반 이상을 자동화할 계획을 세웠습니다. 컨설팅 기업들은 프로젝트의 전체 라이프사이클에 AI를 접목함으로써 이러한 기회를 포착하고, 가동률을 최대 50%까지 향상시키는 동시에 데이터가 풍부한 전략 스프린트를 실현하여 프로젝트 기간을 단축하고 있습니다. 규제 당국도 수요를 창출하고 있습니다. 싱가포르 금융관리청은 이행 계획 지침을 발표했으며, 일본 금융청은 체계적인 자문 지원을 장려하는 AI 활용 프레임워크를 공표했습니다. 고객사가 전문가를 다수 보유한 팀을 선호함에 따라, 각 기업은 피라미드형에서 다이아몬드형 인력 구성으로 전환하고 있으며, 중견 인력과 전문가 채용을 확대함과 동시에 아시아태평양의 전략 컨설팅 서비스 시장 전체의 인재 경제 구조를 재정의하고 있습니다.

국경을 초월한 M&A 및 사업 재편 사례의 급증

공급망의 다양화와 지정학적 재편으로 인해, 2024년 해당 지역의 거래 건수는 수년 만에 최고 수준을 기록하며, 거래 전략 업무에 활기를 불어넣었습니다. 서로 다른 규제 기준과 국가 안보 심사에 대응해야 하는 복잡성 때문에 현지에서 확실한 실적을 쌓고 협업 도구 세트를 갖춘 자문 팀에게는 분명한 경쟁 우위가 생기고 있습니다. IBM이 HashiCorp를 64억 달러에 인수한 것과 같은 기술 주도형 인수는 소프트웨어 역량이 기업 가치 평가 기준에 미치는 영향을 여실히 보여주고 있습니다. 한편, 리스크 완화 전략과 관련된 스핀오프 및 커브아웃은 사업 재편 프로젝트의 파이프라인을 더욱 확대시키고 있습니다. 그 결과, 각 컨설팅 기업들은 거시적인 위험 신호를 아세안, 일본, 호주 전역의 이사회 차원의 행동 계획으로 전환하는 지정학적 전략 팀을 공식적으로 구성했습니다.

대기업 고객들 사이에서 가격에 대한 민감도가 높아지고 있습니다.

경영진급 바이어들은 거시경제의 불확실성에 대응하여 요금 체계 재협상을 추진하고 있으며, 성과 기반 가격 책정 및 프로젝트 주기 단축으로 전환하고 있습니다. 이에 각 기업은 상세한 ROI 기준치와 AI를 활용한 전달 가속화 기술을 바탕으로 한 정액제 모델로 대응하고 있으며, 이를 통해 복합 단가가 하락하더라도 이익률을 유지하고 있습니다. 전문 인력 확보가 중요시됨에 따라, 신입 인력에 대한 수요는 더욱 줄어들고, 중견 인력 확보 경쟁이 치열해지는 한편, 프리랜서 마켓플레이스에 인력을 공급하는 OB 네트워크가 육성되고 있습니다.

부문별 분석

디지털 전략 부문은 2025년 아시아태평양의 전략 컨설팅 서비스 시장 규모에서 27.20%를 차지하며, 기업의 변혁 프로그램에서 계속해서 핵심적인 역할을 했습니다. 이러한 우위는 정량화 가능한 수익 증대와 비용 효율화를 가져오는 AI 통합, 데이터 현대화, 그리고 플랫폼형 비즈니스 모델의 확대에 기인합니다. ESG 및 지속가능성 컨설팅 시장은 현재 규모는 작지만 연평균 성장률(CAGR) 13.05%로 성장을 지속하고, 있으며, 공시 의무에 따라 환경 지표가 이사회 안건으로 상정됨에 따라 기존 기업 전략 예산을 점차 잠식해 나갈 것으로 예측됩니다. M&A 전략은 공급망 및 지정학적 재편의 흐름을 타고, 통합적인 거래 전략에 대한 수요를 촉진하고 있습니다. 리스크 및 컴플라이언스 업무는 아시아태평양 각 관할 구역에서 강화되고 있는 자금세탁 방지 기준, 사이버 규제, 디지털 주권법에 힘입어 견조한 성장세를 유지하고 있습니다.

각 서비스 제공업체들은 업계 고유의 가속화 도구와 인사이트 확보까지 걸리는 시간을 단축하는 독자적인 데이터 자산을 활용하여 타사와의 차별화를 꾀하고 있습니다. 예를 들어, 탄소 회계 플랫폼은 ESG 관련 활동에 통합되고 있으며, 디지털 트윈은 제조 전략 수립을 가속화하고 있습니다. 이러한 도구들은 구독 및 관리형 서비스 모델을 통해 지속적인 수익원을 창출하며, 수익 구조를 순수한 시간 및 자재비 기반의 청구 방식에서 점차 전환시키고 있습니다. 이와 동시에, 아시아태평양의 전략 컨설팅 서비스 시장에서는 디지털 전략 및 지속가능성이라는 틈새 분야에서 프리미엄 가격 책정과 브랜드 정체성을 유지하기 위해 컨설팅 기업들이 전문 부티크 회사를 분사시키는 움직임이 나타나고 있습니다.

2025년, 은행, 보험사, 자본 시장 사업자들이 디지털 혁신과 규제의 틈새를 교묘히 헤쳐 나가는 가운데, 금융기관은 아시아태평양의 전략 컨설팅 서비스 시장 점유율의 24.12%를 차지했습니다. 핀테크와의 제휴, 오픈 뱅킹 인터페이스, 그리고 임베디드 금융 생태계에는 기술, 업무, 규정 준수 각 영역을 통합한 치밀한 전환 계획이 필요합니다. 한편, 생명과학 및 헬스케어 분야는 인구 동향의 변화, 원격의료의 보급, 생명공학에 대한 투자 확대를 배경으로 연평균 성장률(CAGR) 13.70%를 기록하며 성장세를 가속화하고 있습니다. TMT(기술·미디어·통신) 기업들은 5G 지원 플랫폼, AI를 활용한 컨텐츠 생성, 데이터 개인정보 보호 요건에 대한 지침을 계속해서 요구하고 있으며, 제조업 고객들은 탈탄소화 단계별 목표를 반영한 인더스트리 4.0 로드맵을 요구하고 있습니다.

분야별 전문화에 따라 서비스 제공 팀의 역할이 재정의되고 있습니다. 예를 들어, 임상 연구와 데이터 사이언스, 혹은 결제 업무와 사이버 보안과 같은 두 분야에 정통한 컨설턴트는 현재 고액의 보수를 받고 있습니다. 정부 기관 고객들은 스마트시티 및 공공재정 혁신 프로젝트를 선별적으로 발주하고 있지만, 예산 제약으로 인해 전반적인 성장은 제한되고 있습니다. 모든 산업 분야에서 대출 실행 속도, 환자의 복약 순응도, 배출량 감축과 같은 성과 지표가 계약 조건에 반영되고 있으며, 아시아태평양의 전략 컨설팅 서비스 시장에서 성과 기반 계약 모델이 점차 정착되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTHAccording to Mordor Intelligence, asia pacific strategic consulting services market size in 2026 is estimated at USD 11.64 billion, growing from 2025 value of USD 10.34 billion with 2031 projections showing USD 20.98 billion, growing at 12.52% CAGR over 2026-2031.

This report is Segmented by Service Type (Corporate Strategy, Digital Strategy, and More), End-User Industry (Financial Services, Retail and Consumer, and More), Enterprise Size (Large Enterprises, and Small and Medium Enterprises), Delivery Model (On-Site Consulting, Remote/Virtual Consulting, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Asia Pacific Strategic Consulting Services Market Trends and Insights

Digital-transformation wave across Asia Pacific

Enterprises in the region accelerated digital spending following pandemic disruptions, with 44% of previously offline organizations planning to automate over half their non-automated processes by 2025. Consulting firms are seizing the opportunity by embedding AI throughout project lifecycles, raising utilization rates by up to 50% and enabling data-rich strategy sprints that shorten engagement timelines. Regulators are also shaping demand: Singapore's Monetary Authority issued transition planning guidelines, and Japan's Financial Services Agency published AI use frameworks that encourage structured advisory support. As clients favor expert-heavy teams, firms are migrating from pyramid to diamond staffing, pushing mid-level and specialist hiring higher and redefining talent economics across the Asia Pacific strategic consulting services market.

Surge in cross-border M and A and restructuring mandates

Supply-chain diversification and geopolitical realignment lifted regional deal volumes to multi-year highs in 2024, energizing transaction strategy practices. The complexity of navigating disparate regulatory codes and national security reviews gives a distinct edge to advisory teams with deep local credentials and collaborative toolsets. Technology-driven acquisitions such as IBM's USD 6.4 billion HashiCorp purchase underscore how software capabilities influence valuation thresholds, while spin-offs and carve-outs linked to de-risking strategies further expand restructuring pipelines. As a result, consultancies are formalizing geostrategy cells that translate macro risk signals into board-level action plans across ASEAN, Japan, and Australia.

Rising price sensitivity among large enterprise clients

C-suite buyers are renegotiating fee structures in response to macro uncertainty, shifting toward outcome-based pricing and shorter project cycles. Firms are countering with fixed-fee models underpinned by detailed ROI baselines and AI-enabled delivery accelerators that sustain margins even at lower blended rates. The emphasis on specialist staffing further compresses junior demand, intensifying the search for mid-level talent and fostering alumni networks that feed freelance marketplaces.

Other drivers and restraints analyzed in the detailed report include:

- Escalating demand for ESG / sustainability road-maps

- Embedded-finance disruption driving payments strategy work

- Intensifying competition from Big Tech and IT-services firms

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The digital strategy segment contributed 27.20% to Asia Pacific strategic consulting services market size in 2025 and remains the reference point for enterprise reinvention programs. Its dominance is rooted in AI integration, data modernization, and platform business model expansion that deliver quantifiable revenue lifts and cost efficiencies. ESG and sustainability consulting, though smaller today, is posting a 13.05% CAGR and is expected to chip away at traditional corporate strategy budgets, as disclosure mandates embed environmental metrics into boardroom agendas. M and A strategy rides the wave of supply-chain and geopolitical realignments, reinforcing demand for integrative transaction playbooks. Risk and compliance work remains resilient, fueled by tightening anti-money-laundering standards, cyber regulations, and digital sovereignty laws proliferating across Asia Pacific jurisdictions.

Service providers are differentiating by sector-specific accelerators and proprietary data assets that compress time to insight. For example, carbon-accounting platforms are embedded into ESG engagements, while digital twins accelerate manufacturing strategy design. These tools create recurring revenue streams via subscription or managed-service models, subtly shifting revenue mixes away from pure time-and-materials billing. In parallel, the Asia Pacific strategic consulting services market is witnessing consultancies spinning off specialist boutiques to maintain premium pricing and brand clarity in digital strategy and sustainability niches.

Financial institutions captured 24.12% of Asia Pacific strategic consulting services market share in 2025 as banks, insurers, and capital-market operators navigated digital disruption and regulatory tightrope walks. Fintech collaborations, open-banking interfaces, and embedded finance ecosystems require intricate transition blueprints that integrate technology, operations, and compliance layers. Life sciences and healthcare, meanwhile, is accelerating at a 13.70% CAGR, underpinned by demographic shifts, telehealth diffusion, and rising biotech investment. TMT players continue to seek guidance on 5G-enabled platforms, AI content generation, and data-privacy imperatives, while manufacturing clients demand Industry 4.0 roadmaps with decarbonization milestones.

Sector specialization is redefining delivery teams: consultants with dual backgrounds in, for instance, clinical research and data science, or payments operations and cybersecurity, now command premium billing rates. Government clients are selectively commissioning smart-city and public-finance transformation projects, although budget constraints temper overall growth. Across sectors, outcome metrics such as loan origination speed, patient adherence, or emissions reduction are baked into contracting terms, reinforcing result-based engagement models in the Asia Pacific strategic consulting services market.

Complete Report Scope:

- By Service Type

- Corporate Strategy

- Digital Strategy

- Operations Strategy

- M&A and Restructuring

- Sustainability and ESG Strategy

- Risk and Compliance Strategy

- By End-User Industry

- Financial Services

- Life Sciences and Healthcare

- Retail and Consumer

- Government and Public Sector

- Energy and Utilities

- Manufacturing

- Technology Media and Telecommunications

- Other End-User Industries

- By Enterprise Size

- Large Enterprises

- Small and Medium Enterprises (SMEs)

- By Delivery Model

- On-site Consulting

- Remote / Virtual Consulting

- Hybrid Consulting

- By Country

- China

- Japan

- India

- Australia

- South Korea

- Singapore

- Indonesia

- Malaysia

- Thailand

- Rest of Asia Pacific

List of Companies Covered in this Report:

- McKinsey and Company

- Boston Consulting Group

- Bain and Company

- A.T. Kearney Inc.

- Deloitte Touche Tohmatsu Limited

- Ernst and Young Global Limited

- KPMG International Limited

- PricewaterhouseCoopers International Limited

- Accenture plc

- Mercer LLC

- Oliver Wyman Group

- Roland Berger Holding GmbH

- L.E.K. Consulting LLC

- Strategy& (part of PwC)

- Capgemini Invent

- IBM Consulting

- Monitor Deloitte

- Arthur D. Little

- Nomura Research Institute Ltd.

- Frost and Sullivan Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Digital-transformation wave across Asia Pacific

- 4.2.2 Surge in cross-border M&A and restructuring mandates

- 4.2.3 Escalating demand for ESG/sustainability road-maps

- 4.2.4 Embedded-finance disruption driving payments strategy work

- 4.2.5 Freelance-consultant supply mismatch enabling new delivery models

- 4.2.6 Heavy-industry supply-chain decarbonisation (CBAM spill-overs)

- 4.3 Market Restraints

- 4.3.1 Rising price sensitivity among large enterprise clients

- 4.3.2 Intensifying competition from Big Tech and IT-services firms

- 4.3.3 Client skepticism on Gen-AI consulting ROI

- 4.3.4 Regional talent drain to freelance / in-house strategy teams

- 4.4 Industry Ecosystem Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers/Consumers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Service Type

- 5.1.1 Corporate Strategy

- 5.1.2 Digital Strategy

- 5.1.3 Operations Strategy

- 5.1.4 M&A and Restructuring

- 5.1.5 Sustainability and ESG Strategy

- 5.1.6 Risk and Compliance Strategy

- 5.2 By End-User Industry

- 5.2.1 Financial Services

- 5.2.2 Life Sciences and Healthcare

- 5.2.3 Retail and Consumer

- 5.2.4 Government and Public Sector

- 5.2.5 Energy and Utilities

- 5.2.6 Manufacturing

- 5.2.7 Technology Media and Telecommunications

- 5.2.8 Other End-User Industries

- 5.3 By Enterprise Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises (SMEs)

- 5.4 By Delivery Model

- 5.4.1 On-site Consulting

- 5.4.2 Remote / Virtual Consulting

- 5.4.3 Hybrid Consulting

- 5.5 By Country

- 5.5.1 China

- 5.5.2 Japan

- 5.5.3 India

- 5.5.4 Australia

- 5.5.5 South Korea

- 5.5.6 Singapore

- 5.5.7 Indonesia

- 5.5.8 Malaysia

- 5.5.9 Thailand

- 5.5.10 Rest of Asia Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 McKinsey and Company

- 6.4.2 Boston Consulting Group

- 6.4.3 Bain and Company

- 6.4.4 A.T. Kearney Inc.

- 6.4.5 Deloitte Touche Tohmatsu Limited

- 6.4.6 Ernst and Young Global Limited

- 6.4.7 KPMG International Limited

- 6.4.8 PricewaterhouseCoopers International Limited

- 6.4.9 Accenture plc

- 6.4.10 Mercer LLC

- 6.4.11 Oliver Wyman Group

- 6.4.12 Roland Berger Holding GmbH

- 6.4.13 L.E.K. Consulting LLC

- 6.4.14 Strategy& (part of PwC)

- 6.4.15 Capgemini Invent

- 6.4.16 IBM Consulting

- 6.4.17 Monitor Deloitte

- 6.4.18 Arthur D. Little

- 6.4.19 Nomura Research Institute Ltd.

- 6.4.20 Frost and Sullivan Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and unmet-need assessment