|

시장보고서

상품코드

2063543

마이크로플레이트 워셔 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Microplate Washers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

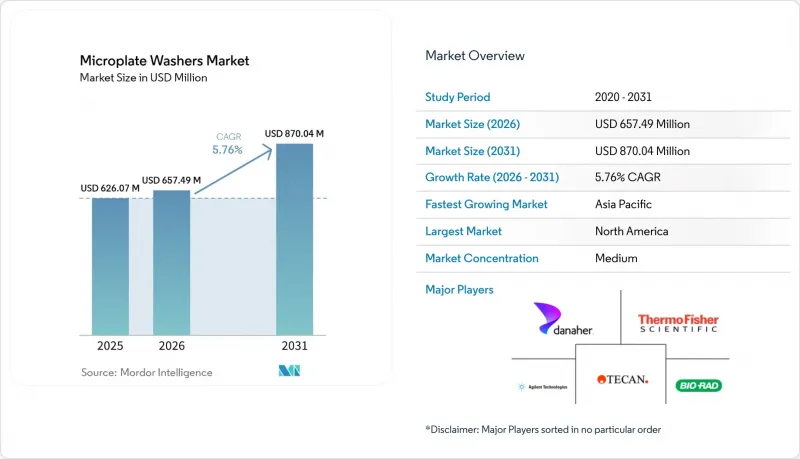

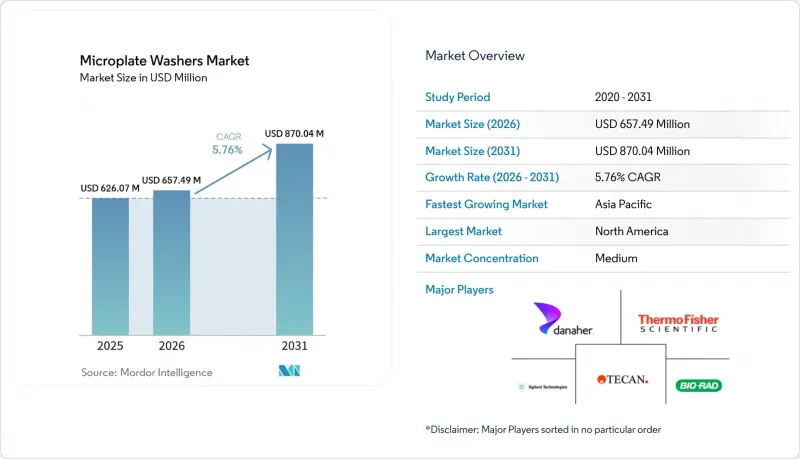

Mordor Intelligence에 의하면, 마이크로플레이트 워셔 시장 규모는 2025년 6억 2,607만 달러로 평가되었습니다. 2026년에는 6억 5,749만 달러로 확대되어 2026년부터 2031년에 걸쳐 CAGR 5.76%로 성장을 지속하여, 2031년에는 8억 7,004만 달러에 이를 것으로 예측됩니다.

본 보고서는 자동화 수준(완전 자동, 반자동, 수동), 용도(ELISA/면역측정법 등), 최종 사용자(병원 및 진단실험실, 기준 검사 기관, 제약·바이오기술 기업 등) 및 지역(북미, 유럽, 아시아태평양, 중동 및 아프리카, 남미)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 마이크로플레이트 워셔 시장 동향 및 인사이트

임상 및 연구 실험실에서의 ELISA/면역측정 검사 건수 증가

만성 질환 감시 및 감염병 모니터링으로 인해, 병원 및 중개연구실에서의 ELISA 플레이트 처리량이 증가하고 있습니다. 웰당 최대 40종의 분석 대상을 측정할 수 있는 멀티플렉스 키트의 등장으로, 세척 과정의 일관성에 대한 요구가 높아지고 있습니다. 자동화 시스템 덕분에 분석 결과 간의 편차가 12%에서 5% 미만으로 감소했습니다. 미들웨어로 제어되는 플레이트 워셔는 현재 검사 정보 시스템에 통합되어 있으며, 기존에 검사실당 연간 7만 달러 이상의 재작업 비용을 초래하던 수동 데이터 입력 오류를 제거하고 있습니다.

제약·바이오기술 업계에서의 실험실 자동화 및 고처리량 스크리닝 도입 확대

대형 제약 그룹은 신약 개발 주기를 단축하고 시약을 절약하기 위해 로봇 스크리닝 셀 내에 세척기를 장착하고 있습니다. Tecan사는 2024년 3분기에 3억 1,190만 스위스 프랑의 매출을 기록했으며, 그 요인으로 액체 처리 분야에 대한 강한 수요를 꼽았습니다. 같은 기간, Bio-Rad의 임상 진단 부문 매출은 6.5% 증가한 3억 9,310만 달러를 기록하며, 분석 처리량이 세척기의 가동률과 직접적인 관련이 있음을 입증했습니다. 제약 품질 관리(QC) 분야에서 자동 세척기의 투자 회수 기간은 6-12개월이며, 이는 96웰 분석에서 1,536웰 플레이트로의 전환에 따른 시약비 절감이 주된 요인입니다.

첨단 자동 세척기의 높은 도입 및 유지 비용

완전 자동 384채널 세척기의 가격은 2만 5,000-6만 달러이며, 연간 유지보수 계약에 따라 10-15%의 비용이 추가로 부과됩니다. 학계에서는 자금 조달에 대한 압박이 두드러지며, NIH의 연구비 지원금이 2024년 대비 34% 감소했고, 장비 구입을 위한 지원금 규모가 축소되고 있습니다. 리스를 이용하면 초기 비용은 줄어들지만, 5년간의 총 소유 비용은 15-20% 증가합니다. Autobio나 Kehua와 같은 중국 제조업체들은 현재 1만 5,000달러 미만의 기종을 현지 서비스 센터와 함께 제공하며, 자금 면에서 제약이 큰 지역의 가격 장벽을 낮추고 있습니다.

부문별 분석

자동화 플랫폼은 2025년 매출의 41.12%를 차지했으며, 2026년부터 2031년까지 연평균 성장률(CAGR) 7.13%로 성장할 전망입니다. 384채널 매니폴드와 결합된 로봇 로더는 1536웰 플레이트의 세척 주기를 90초 만에 완료하여, 스크리닝 센터가 하루에 10만 건 이상의 데이터 포인트를 기록할 수 있게 해줍니다. 반자동 유닛 마이크로플레이트 워셔 시장 점유율은 하락 추세를 보이고 있습니다. 이는 작업에 소요되는 시간이 길기 때문에 GMP 규제 환경에서의 품질 관리 프로토콜과 상충되기 때문입니다. 자본 예산이 제한적이고 유지보수 체계가 갖춰지지 않은 지역, 특히 라틴아메리카의 지방이나 중동 및 아프리카(MEA) 지역에서는 여전히 수동식 장비가 널리 사용되고 있지만, 정밀도 시험에서 15%를 초과하는 편차로 인해 보급형 자동화 장비로의 단계적 교체가 진행되고 있습니다.

중국공급업체가 1만 달러가 조금 넘는 자동화 모델을 출시하고, 유럽 및 미국의 기존 제조업체 제품보다 최대 40% 저렴한 가격을 책정함에 따라 비용 동향은 변화하고 있습니다. 주당 200-500장의 플레이트를 처리하는 병원에서는 반자동 세척기를 도입함으로써 시약 절감과 재작업률 감소로 인해 18개월 이내에 투자 비용을 회수할 수 있는 것으로 밝혀졌습니다. 그러나 검사 기관이나 제약 회사의 검사실에서는 검사 정보 시스템(LIS)과 통합된 종단 간 자동화를 중시하고 있으며, 많은 입찰에서 미들웨어를 통한 연결성은 잔류량 사양에 이어 두 번째로 중요한 요건으로 꼽히고 있습니다.

지역별 분석

북미는 2025년 매출의 47.13%를 차지했으며, 이는 설치 대수가 많을 뿐만 아니라 유럽의 기한보다 앞서 IVDR에 부합하는 업그레이드가 조기에 이루어졌음을 반영합니다. 미국 학술 기관의 지출은 NIH(미국 국립보건원)의 예산 삭감으로 인해 둔화되고 있지만, 민간 검사실이 막대한 자동화 예산을 통해 그 차이를 메우고 있습니다. 새로운 ISO 15189 표준을 충족하는 미들웨어 통합은 캐나다와 미국의 병원 시스템 모두에서 사양서의 지침으로 채택되고 있습니다.

유럽은 두 번째로 큰 시장 점유율을 차지하고 있으며, EU IVDR에 따른 CE-IVD 인증 세척기로의 의무적 전환이 이를 주도하고 있습니다. 독일, 프랑스, 영국의 검사실에서는 인증 관련 위험을 피하기 위해 2024년부터 교체를 가속화하기 시작했습니다. '호라이즌 유럽'의 보조금은 검증된 면역 측정 플랫폼이 필요한 중개 연구 프로젝트에 대한 자금 지원을 지속하고 있으며, 공공 연구 분야의 워셔에 대한 안정적인 수요를 뒷받침하고 있습니다.

아시아태평양은 연평균 성장률(CAGR) 7.19%를 기록하며 성장의 중심지로 자리매김하고 있습니다. 대만이나 일본 등 선진국에서는 병원 내 자동화가 점차 확산되고 있습니다. 중국과 인도에서는 정부의 인센티브 제도에 따라 검사실용 로봇이 지원 대상이 되어, Mindray나 Autobio와 같은 현지 제조업체들을 뒷받침하고 있습니다. 1만 5,000달러 미만의 자동화 모델은 투자 회수 기간을 2회계연도로 단축하기 때문에 중규모 지방 병원에서도 자동화 도입이 조달 결정의 결정적인 요인이 되고 있습니다.

남미 및 중동 및 아프리카 시장 점유율은 소폭이지만, 서비스 네트워크의 과제가 해소된다면 잠재적인 성장 여지가 있습니다. 사하라 이남 아프리카에서는 부품 납기 지연이 90일을 초과함에 따라 소유주들은 수동 시스템을 선택할 수밖에 없었지만, 클라우드 기반 모니터링 세차기를 도입함으로써 현장 기술 방문 횟수가 크게 줄어들고 있습니다. 예비 부품을 재고로 확보하고, 다양한 브랜드에 대한 교육을 제공하는 현지 유통업체은 두 지역 모두에서 경쟁 우위를 누리고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.26According to Mordor Intelligence, the microplate washers market size is expected to grow from USD 626.07 million in 2025 to USD 657.49 million in 2026 and is forecast to reach USD 870.04 million by 2031 at 5.76% CAGR over 2026-2031.

This report is Segmented by Automation Level (Automated, Semi-Automated, Manual), Application (ELISA/Immunoassays, and More), End User (Hospital & Diagnostic Laboratories, Reference Laboratories, Pharmaceutical & Biotechnology Companies, and More), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

Global Microplate Washers Market Trends and Insights

Growth in ELISA/Immunoassay Testing Volumes in Clinical and Research Labs

Chronic-disease surveillance and infectious-disease monitoring are expanding ELISA plate throughput across hospital and translational laboratories. Multiplex kits measuring up to 40 analytes per well heighten the need for wash consistency; automated systems reduce inter-assay variability from 12% to below 5%. Middleware-controlled plate washers are now integrated into laboratory information systems, eliminating manual data entry errors that historically drove rework costs above USD 70,000 per lab each year.

Rising Lab Automation and High-Throughput Screening Adoption in Pharma/Biotech

Top pharmaceutical groups embed washers inside robotic screening cells to compress discovery cycles and save reagents. Tecan recorded CHF 311.9 million in revenue in the third quarter of 2024, citing strong liquid-handling demand. Bio-Rad's clinical-diagnostics arm grew 6.5% to USD 393.1 million in the same period, confirming that assay volume directly translates into washer utilization. Payback periods for automated washers range from 6-12 months in pharmaceutical QC, driven by reagent savings when 96-well assays migrate to 1536-well plates.

High Acquisition and Maintenance Costs for Advanced Automated Washers

A fully automated 384-channel washer costs USD 25,000-60,000, with annual service contracts adding another 10-15%. Funding pressure is visible in academia, where NIH obligations fell 34% versus 2024, shrinking equipment-grant pools. Leasing mitigates upfront cash but raises five-year ownership cost by 15-20%. Chinese suppliers such as Autobio and Kehua now ship sub-USD 15,000 units with local service centers, loosening the price barrier in resource-sensitive regions.

Other drivers and restraints analyzed in the detailed report include:

- Shift Toward Higher-Density Plates Requiring Precision Washing

- Expansion of Life-Sciences R&D Funding and Installed-Base Refresh Cycles

- Skills/Training Gaps to Optimize Wash Protocols and Reduce Assay Variability

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Automated platforms captured 41.12% of 2025 revenue and will advance at 7.13% CAGR over 2026-2031. Robotic loaders paired with 384-channel manifolds complete a wash cycle on a 1536-well plate in 90 seconds, enabling screening centers to log over 100,000 data points daily. The microplate washers market share for semi-automated units is sliding as their higher operator-touch time clashes with quality-control protocols in GMP-regulated environments. Manual devices remain entrenched where capital budgets are thin and maintenance infrastructure is sparse, especially in rural Latin America and MEA, but their variability above 15% in proficiency tests is driving gradual replacement by entry-level automation.

Cost dynamics are shifting as Chinese vendors introduce automated models just above USD 10,000, undercutting Western incumbents by up to 40%. Hospitals processing 200-500 plates weekly find that semi-automated washers earn payback within 18 months through reagent savings and lower rework rates. However, reference and pharma labs value end-to-end automation that integrates with laboratory information systems; middleware connectivity now ranks second only to residual volume specification in many tenders.

Geography Analysis

North America generated 47.13% of 2025 revenue, reflecting dense installed bases and early IVDR-aligned upgrades even before European deadlines. U.S. academic spending is softening due to reduced NIH appropriations, yet private labs offset the gap through large automation budgets. Middleware integration that satisfies emerging ISO 15189 criteria is guiding specification sheets in Canadian and U.S. hospital systems alike.

Europe holds the second-largest slice, driven by the mandatory shift to CE-IVD washers under EU IVDR. Laboratories in Germany, France, and the United Kingdom began accelerated replacement during 2024 to avoid accreditation risk. Horizon Europe grants continue to fund translational projects that require validated immunoassay platforms, supporting steady washer demand in public research.

Asia-Pacific is the expansion hotspot at 7.19% CAGR. Developed economies such as Taiwan and Japan boast hospital-automation penetration. Government incentive schemes in China and India now subsidize laboratory robotics, propelling local makers such as Mindray and Autobio. Sub-USD 15,000 automated models shorten payback to two fiscal years, tipping procurement decisions in favor of automation even in mid-tier provincial hospitals.

South America and Middle East & Africa account for modest shares but present latent upside once service-network hurdles recede. Parts delays exceeding 90 days in sub-Saharan Africa push owners toward manual systems, but cloud-monitored washers are starting to reduce on-site technical visits significantly. Local distributors that stock spare parts and provide multi-brand training enjoy a competitive edge in both regions.

- Accuris Instruments

- Agilent Technologies

- Autobio Diagnostics

- Awareness Technology

- Berthold Technologies

- BIOBASE

- Bio-Rad Laboratories

- Biosan

- CAPP / AHN Biotechnologie

- Caretium Medical Instruments

- Danaher

- Erba Mannheim

- Hudson Robotics

- HUMAN Diagnostics

- Mindray

- Perlong Medical

- Shanghai Kehua Bio-Engineering (KHB)

- Tecan Group

- Thermo Fisher Scientific

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growth In ELISA/Immunoassay Testing Volumes in Clinical and Research Labs

- 4.2.2 Rising Lab Automation and High-Throughput Screening Adoption in Pharma/Biotech

- 4.2.3 Shift Toward Higher-Density Plates (E.G., 384-Well) Requiring Precision Washing

- 4.2.4 Expansion Of Life Sciences R&D Funding and Installed Base Refresh Cycles

- 4.2.5 Magnetic Bead-Based Workflows Expanding Washer Use Cases (Bead Washing)

- 4.2.6 EU IVDR/Quality Compliance Pushing CE-IVD-Capable Washers In Diagnostics

- 4.3 Market Restraints

- 4.3.1 High Acquisition and Maintenance Costs for Advanced Automated Washers

- 4.3.2 Skills/Training Gaps to Optimize Wash Protocols and Reduce Assay Variability

- 4.3.3 Lack Of Protocol Standardization Increases Reproducibility Risks

- 4.3.4 Fragmented After-Sales/Service Networks in Developing Regions

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Automation Level

- 5.1.1 Automated

- 5.1.2 Semi-automated

- 5.1.3 Manual

- 5.2 By Application

- 5.2.1 ELISA / Immunoassays

- 5.2.2 Cell-based assays

- 5.2.3 Bead-based assays

- 5.2.4 Filter-plate assays

- 5.3 By End User

- 5.3.1 Hospital & diagnostic laboratories

- 5.3.2 Reference laboratories

- 5.3.3 Pharmaceutical & biotechnology companies

- 5.3.4 Academic & research institutes

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 Australia

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.3.1 Accuris Instruments

- 6.3.2 Agilent Technologies

- 6.3.3 Autobio Diagnostics

- 6.3.4 Awareness Technology

- 6.3.5 Berthold Technologies

- 6.3.6 BIOBASE

- 6.3.7 Bio-Rad Laboratories

- 6.3.8 Biosan

- 6.3.9 CAPP / AHN Biotechnologie

- 6.3.10 Caretium Medical Instruments

- 6.3.11 Danaher Corporation

- 6.3.12 Erba Mannheim

- 6.3.13 Hudson Robotics

- 6.3.14 HUMAN Diagnostics

- 6.3.15 Mindray

- 6.3.16 Perlong Medical

- 6.3.17 Shanghai Kehua Bio-Engineering (KHB)

- 6.3.18 Tecan Group

- 6.3.19 Thermo Fisher Scientific

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment