|

시장보고서

상품코드

2063568

빌리루빈 측정기 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Bilirubin Meters - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

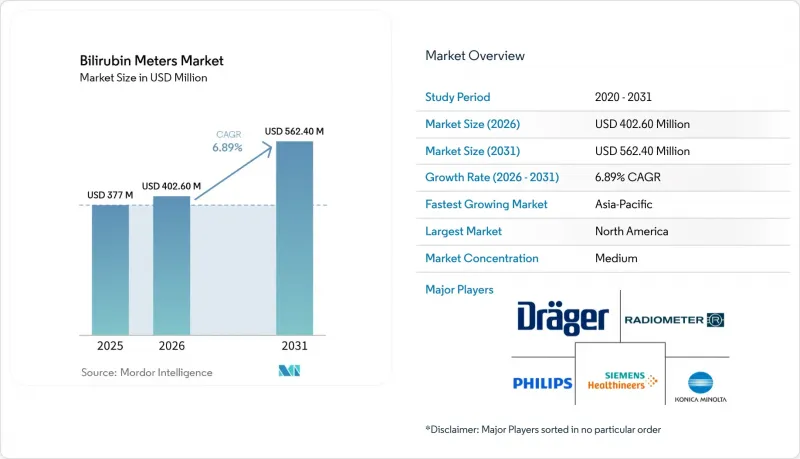

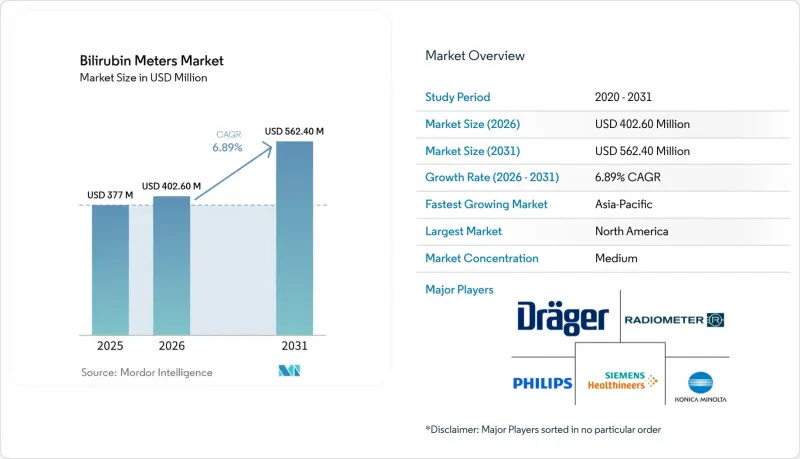

Mordor Intelligence에 의하면, 빌리루빈 측정기 시장 규모는 2025년 3억 7,700만 달러에서 2026년에는 4억 260만 달러로 확대되어 2031년까지 5억 6,240만 달러에 이를 것으로 예측되며, 2026년부터 2031년까지 CAGR 6.89%로 성장할 전망입니다.

본 보고서는 제품 유형(경피 빌리루빈 측정기, 탁상형/혈청 빌리루빈 측정기), 최종 사용자(병원, 신생아 클리닉·출산 센터, 진단실험실, 재택 간호), 용도(스크리닝, 진단·모니터링), 지역(북미, 유럽, 아시아태평양, 중동 및 아프리카, 남미)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

전 세계 빌리루빈 측정기 시장 동향 및 인사이트

신생아 황달의 높은 유병률과 퇴원 전 선별검사의 확산 추세

만삭 신생아 10명 중 6명, 조산아 10명 중 8명이 생후 1주일 이내에 육안으로 확인 가능한 황달 증상을 보이며, 이에 따라 지침 제정 기관은 분만 병동 전체에서 정기 검사를 실시할 것을 강력히 권고하고 있습니다. 인도의 ‘미션 안몰(Mission ANMOL)’은 빌리루빈 검사를 다른 55개 항목의 신생아 선별 검사와 한 번의 진료에 통합함으로써, 중소득국의 의료 시스템이 이 의무를 어떻게 대규모로 이행할 수 있는지를 보여주고 있습니다. 이러한 규제의 통합으로 인해, 임의 검사가 표준적인 의료 서비스로 자리 잡을 것으로 기대되며, 의료기기 및 소모품에 대한 다년간의 예산 배분이 촉진되고 있습니다. 스크리닝이 보편화됨에 따라, 장비 자금 조달과 직원 교육을 턴키 계약에 포함시킬 수 있는 공급업체가 유리한 입지를 차지할 것입니다.

비침습적 TcB 선별 검사로의 전환으로 인해 채혈 횟수와 재입원 건수가 감소했습니다.

발뒤꿈치 천자를 통한 혈청 채취에는 평균 8분의 인력이 소요되지만, 경피적 스캔은 2분이면 충분하기 때문에 1회 선별 검사당 즉시 40%의 인건비 절감 효과를 가져옵니다. 2024년 『JAMA Pediatrics』에 게재된 코호트 연구에 따르면, TcB의 보편적인 도입으로 인해 1년 이내의 황달 관련 재입원률이 32% 감소한 것으로 나타났습니다. 연간 최대 5,000건의 분만을 처리하는 미국의 산과 병동에서는 업무 흐름의 효율화가 더욱 두드러지며, 이러한 전환을 통해 간호팀은 수유 지원 및 퇴원 시 지도에 더 많은 시간을 할애할 수 있게 됩니다. 이에 대응하여 기기 제조업체들은 바코드 스캐너와 HL7 FHIR 데이터 교환 기능을 탑재함으로써, 측정값이 전자차트에 자동으로 입력될 뿐만 아니라, 광선 요법의 임계치에 가까워지면 경보가 울리도록 하고 있습니다. 그러나 치료 기준치 부근에서는 혈청 검사를 통한 확인이 필요하기 때문에 잠재적인 시장 규모는 제한되며, 여전히 실험실에서의 분석이 필요합니다.

TcB는 임계치 부근 및 광선 요법 종료 후의 한계치에서 TSB를 통한 확인이 필요합니다.

광학식 빌리루빈 측정법은 15 mg/dL을 초과하는 수치를 과소평가하는 경향이 있으며, 광선 요법 후에는 피부 반사율의 변화가 알고리즘의 정확도를 저하시켜 신뢰성이 떨어집니다. 따라서 NICE 지침에서는 TcB 측정값이 치료 시작 기준치에서 3 mg/dL 이내인 경우, 반드시 혈청 검사를 통해 확인하도록 규정하고 있습니다. 가나에서는 이러한 이중 검사로 인해 영아 1인당 비용이 8.50달러로 상승했습니다. 반면, TcB만 사용하는 워크플로우의 경우 3.20달러이므로, 공립병원의 경제적 이점이 훼손되고 있습니다. Radiometer ABL90 FLEX 또는 Siemens RAPIDPoint 405 플랫폼을 도입한 검사실에서는 이미 혈액가스 분석과 함께 빌리루빈을 측정하고 있으며, 이를 통해 임상의는 중환자 치료 환경에서 별도의 장비를 사용할 필요가 없게 되었습니다. TcB 공급업체가 광선 요법 후의 정확도를 향상시키지 못하는 한, 혈청 검사는 여전히 중요한 위치를 차지할 것입니다.

부문별 분석

경피형 기기는 2025년 매출의 61.30%를 차지했으며, 검체 채취 시간을 75% 단축하고 전자 차트와 원활하게 연동되는 비침습적 워크플로우에 대한 병원 측의 선호도가 입증되었습니다. 보편적인 선별 검사를 통해 모든 분만실에서 이 장비가 필수적으로 도입됨에 따라, 경피적 빌리루빈 측정 시스템 시장 규모는 꾸준히 확대될 것으로 예측됩니다. 한편, 탁상형 혈청 분석기는 빌리루빈 외에도 6가지 생화학 검사를 처리할 수 있는 다항목 혈액가스 분석기로의 검사실 통합에 힘입어, 2031년까지 연평균 성장률(CAGR) 8.36%라는 더 높은 성장세를 보일 것으로 전망됩니다. 경피 농도와 혈청 농도의 상관계수는 여전히 0.76에서 0.92 사이이므로, 선별 검사를 받은 영아 3명 중 1명은 혈청 검사를 통한 확인이 필요하며, 이를 통해 잔여 수요가 확보됩니다.

임상의들은 정확도와 업무 흐름의 균형을 고려하고 있습니다. Dragerwerk사의 JM-105는 5가지 파장의 광학 시스템과 바코드 스캐너를 내장하고 있으며, 임계값에 가까운 수치를 감지하면 재검사를 지시합니다. 한편, QuidelOrtho사의 Vitros BuBc Slide는 담도폐쇄증 진단에 필수적인 결합형 및 비결합형 빌리루빈 분획을 제공합니다. 알고리즘의 발전으로 경피 측정 정확도가 향상되는 가운데, 나머지 차별화 요인은 소모품 비용과 교정의 안정성에 좌우될 가능성이 있습니다. 일회용 프로브 팁과 클라우드 분석 기능을 구독 번들에 포함시킨 공급업체는 AI 기반 스마트폰 앱이 빌리루빈 측정기 시장의 보급형 시장을 뒤흔들기 전에 고객 기반을 공고히 할 수 있을 것입니다.

지역별 분석

북미는 2025년에 37.18%의 점유율을 차지했습니다. 이는 미국 내 연간 360만 명의 출생 수, 종합적인 보험 적용 범위, 그리고 모든 퇴원 체크리스트에 빌리루빈 측정을 포함하도록 한 지침의 일관성에 의해 뒷받침되고 있습니다. 현재, 기기의 보급은 교체 주기에 따라 주도되고 있으며, 병원들은 Wi-Fi 지원 모델로 업그레이드하거나 소모품을 절약할 수 있는 대체품을 도입하고 있습니다. 캐나다 역시 비슷한 성숙 단계에 있는 반면, 멕시코에서는 시설 보급 상황에 편차가 있어 지방의 진료소에서는 시각적 평가에 의존할 수밖에 없는 실정입니다.

아시아태평양은 성장의 중심지이며, 중국과 인도가 신생아 중환자실(NICU) 병상 수와 전국적인 선별 검사 프로그램을 확대하고 있어, 2031년까지 연평균 성장률(CAGR)은 7.98%를 나타낼 것으로 전망됩니다. 해당 지역의 빌리루빈 측정기 시장 규모는 현재 북미보다 작지만, 막대한 출생 수와 의료시설에서의 분만 증가로 인해 매우 큰 성장 여지가 생겨나고 있습니다. 보상 격차는 여전히 존재하며, 남아시아의 공립병원 중 진단 예산이 확보된 곳은 30% 미만에 불과하지만, 국가 제도나 자선 단체의 보조금을 통해 일시적인 지원이 이루어지고 있습니다.

유럽에서는 NICE(영국 국립의료기술평가기구)가 TcB의 전면적인 도입에 신중한 입장을 보이고 있어, 시장 규모 성장세가 둔화되고 있습니다. 독일과 프랑스는 대상을 제한한 프로토콜을 유지하고 있는 반면, 스페인은 2027년 전 인구 대상 선별 검사의 시범 사업을 위해 EU 자금 확보를 목표로 하고 있습니다. 중동 및 아프리카 및 남미에서는 인프라 부족이 과제로 대두되고 있으며, 사하라 이남 아프리카의 공립 병원 중 TcB 측정기를 보유하고 있는 곳은 극히 일부에 불과합니다. 브라질의 SUS(공공 의료 제도)는 공립 산부인과 병동에서 실시하는 선별 검사에 대해서는 보험 급여를 지급하지만, 사립 클리닉에서는 지급하지 않기 때문에 시장이 양분되어 있습니다. 필터가 장착된 태양광선 요법과 같은 새로운 저비용 중재법을 통해, 이러한 지역에서는 기존의 측정 장비를 완전히 생략할 수 있을 가능성이 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.23According to Mordor Intelligence, the bilirubin meters market size is expected to increase from USD 377 million in 2025 to USD 402.60 million in 2026 and reach USD 562.40 million by 2031, growing at a CAGR of 6.89% over 2026-2031.

This report is Segmented by Product Type (Transcutaneous Bilirubinometers, Bench-top/Serum Bilirubinometers), End User (Hospitals, Neonatal Clinics & Birth Centers, Diagnostic Laboratories, Home Care), Application (Screening, Diagnosis & Monitoring), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, South America). Market Forecasts are Provided in Terms of Value (USD).

Global Bilirubin Meters Market Trends and Insights

High Neonatal Jaundice Prevalence and Universal Predischarge Screening Momentum

Six of every ten term newborns and eight of every ten preterm infants exhibit visible jaundice during the first week of life, prompting guideline bodies to press for routine testing across delivery wards. India's Mission ANMOL shows how middle-income health systems can operationalize the mandate at scale by integrating bilirubin with 55 other newborn screens in a single visit. This regulatory alignment transforms discretionary testing into a standard-of-care expectation, driving multiyear budget allocations for capital devices and consumables. As screening becomes universal, vendors that can bundle equipment financing and staff training into turnkey contracts stand to gain.

Shift to Non-Invasive TcB Screening Reduces Blood Draws and Readmissions

A heel-stick serum draw averages eight minutes of staff time versus two minutes for a transcutaneous scan, creating an immediate 40% labor saving per screening episode . A 2024 JAMA Pediatrics cohort study tied universal TcB adoption to a 32% drop in jaundice-related readmissions within one year. Workflow efficiency is magnified in U.S. maternity wards processing up to 5,000 deliveries each year, where the switch frees nursing teams for lactation support and discharge education. Device makers have responded by embedding barcode scanners and HL7 FHIR data exchange so readings auto-populate the electronic health record and trigger alerts when phototherapy thresholds loom. Yet the necessity for serum confirmation near treatment cutoffs tempers the total addressable volume, keeping laboratory assays in play.

TcB Requires Confirmatory TSB Near Thresholds and Post-Phototherapy Limits

Optical bilirubinometry underestimates values above 15 mg/dL and becomes unreliable after phototherapy, when skin reflectance changes foil algorithms. NICE guidelines, therefore, impose serum confirmation whenever TcB readings fall within 3 mg/dL of treatment cutoffs. In Ghana, this double-testing pushed per-infant costs to USD 8.50, versus USD 3.20 for TcB-only workflows, eroding the economic case in public hospitals . Laboratories equipped with Radiometer ABL90 FLEX or Siemens RAPIDPoint 405 platforms already measure bilirubin alongside blood gases, enabling clinicians to bypass standalone devices in critical-care settings. Unless TcB vendors can lift post-phototherapy accuracy, serum assays will retain a foothold.

Other drivers and restraints analyzed in the detailed report include:

- APAC Birth Volumes and Neonatal Capacity Expansion Raise Device Demand

- EHR/HIS Connectivity and Workflow Automation Drive Hospital Procurement

- High Upfront Cost and Patchy Reimbursement in Emerging Markets

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Transcutaneous devices captured 61.30% of 2025 revenue, validating hospital preference for non-invasive workflows that cut collection time by 75% and integrate smoothly with electronic records. The bilirubin meters market size for transcutaneous systems is projected to climb steadily as universal screening makes a device mandatory for every delivery ward. Bench-top serum analyzers, however, are forecast to post the brisker 8.36% CAGR through 2031, buoyed by laboratory consolidation onto multi-parameter blood-gas instruments that can process bilirubin alongside six other chemistries. Correlation coefficients between transcutaneous and serum values still range from 0.76 to 0.92, so one in three infants screened will need serum confirmation, safeguarding residual demand.

Clinicians weigh accuracy against workflow: Dragerwerk's JM-105 embeds five-wavelength optics and barcode scanners that flag near-threshold values for confirmatory draws, while QuidelOrtho's Vitros BuBc Slide delivers conjugated and unconjugated fractions vital for biliary atresia diagnosis. As algorithmic advances lift transcutaneous precision, remaining differentiation may hinge on consumable costs and calibration stability. Vendors that wrap disposable probe tips and cloud analytics into subscription bundles could lock accounts before AI-based smartphone apps disrupt the entry-level tier of the bilirubin meters market.

Geography Analysis

North America held 37.18% share in 2025, underpinned by 3.6 million annual U.S. births, comprehensive insurance coverage, and guideline alignment that embeds bilirubin measurement into every discharge checklist. Device penetration is now replacement-cycle driven; hospitals upgrade to Wi-Fi-enabled models or pursue consumable-saving alternatives. Canada mirrors this maturity, while Mexico's uneven facility coverage leaves rural clinics reliant on visual assessment.

Asia-Pacific is the growth epicenter, projected at a 7.98% CAGR to 2031 as China and India scale NICU beds and national screening programs. Although the bilirubin meters market size in the region is smaller than North America's today, sheer birth volumes and rising institutional deliveries create outsized upside. Reimbursement gaps persist; fewer than 30% of South Asian public hospitals have ring-fenced diagnostic budgets, but state schemes and philanthropic grants offer episodic boosts.

Europe trails in volume growth, restrained by NICE's caution that discourages blanket TcB adoption. Germany and France retain targeted protocols, while Spain seeks EU funds to pilot universal screening in 2027. Middle East & Africa and South America suffer infrastructure deficits; only a few of Sub-Saharan public hospitals own a TcB meter. Brazil's SUS reimburses screening in public maternity wards but not in private clinics, splitting the market. Novel low-cost interventions such as filtered-sunlight phototherapy could allow these regions to bypass traditional meters altogether.

- Advanced Instruments, LLC

- APEL Co., Ltd

- Beijing M&B Electronic Instruments Co., Ltd

- BIOBASE Group

- Delta Medical International

- Dragerwerk

- Roche

- GINEVRI srl

- Heal Force Bio-meditech Holdings

- Konica Minolta

- Koninklijke Philips

- Labotronics Scientific

- Mennen Medical Ltd

- Ningbo David Medical Device

- QuidelOrtho (Ortho Clinical Diagnostics)

- Radiometer Medical

- Reichert Analytical Instruments (AMETEK)

- Siemens Healthineers

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 High Neonatal Jaundice Prevalence; Universal Predischarge Screening Momentum

- 4.2.2 Shift To Non-Invasive TcB Screening Reduces Blood Draws and Readmissions

- 4.2.3 APAC Birth Volumes and Neonatal Capacity Expansion Raise Device Demand

- 4.2.4 EHR/HIS Connectivity and Workflow Automation Drive Hospital Procurement

- 4.2.5 Algorithmic/Sensor Advances (Multi-Wavelength, AI) Improve Accuracy

- 4.2.6 Remote/Community TcB Programs for Post-Discharge Monitoring

- 4.3 Market Restraints

- 4.3.1 TcB Requires Confirmatory TSB Near Thresholds; Post-Phototherapy Limits

- 4.3.2 High Upfront Cost; Patchy Reimbursement in Emerging Markets

- 4.3.3 Divergent Guidelines (NICE Vs AAP) Dampen Universal Screening Adoption

- 4.3.4 Substitution By Multi-Parameter Blood-Gas/Chemistry Analyzers in Labs

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product Type

- 5.1.1 Transcutaneous Bilirubinometers

- 5.1.2 Bench-top/Serum Bilirubinometers

- 5.2 By End User

- 5.2.1 Hospitals

- 5.2.2 Neonatal Clinics & Birth Centers

- 5.2.3 Diagnostic Laboratories

- 5.2.4 Home Care

- 5.3 By Application

- 5.3.1 Screening

- 5.3.2 Diagnosis & Monitoring

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 Australia

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles

- 6.3.1 Advanced Instruments, LLC

- 6.3.2 APEL Co., Ltd

- 6.3.3 Beijing M&B Electronic Instruments Co., Ltd

- 6.3.4 BIOBASE Group

- 6.3.5 Delta Medical International

- 6.3.6 Dragerwerk AG & Co. KGaA

- 6.3.7 F. Hoffmann-La Roche Ltd

- 6.3.8 GINEVRI srl

- 6.3.9 Heal Force Bio-meditech Holdings

- 6.3.10 Konica Minolta, Inc.

- 6.3.11 Koninklijke Philips N.V.

- 6.3.12 Labotronics Scientific

- 6.3.13 Mennen Medical Ltd

- 6.3.14 Ningbo David Medical Device Co., Ltd

- 6.3.15 QuidelOrtho (Ortho Clinical Diagnostics)

- 6.3.16 Radiometer Medical

- 6.3.17 Reichert Analytical Instruments (AMETEK)

- 6.3.18 Siemens Healthineers

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment