|

시장보고서

상품코드

2064483

빌리루빈 혈액검사 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Bilirubin Blood Test - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

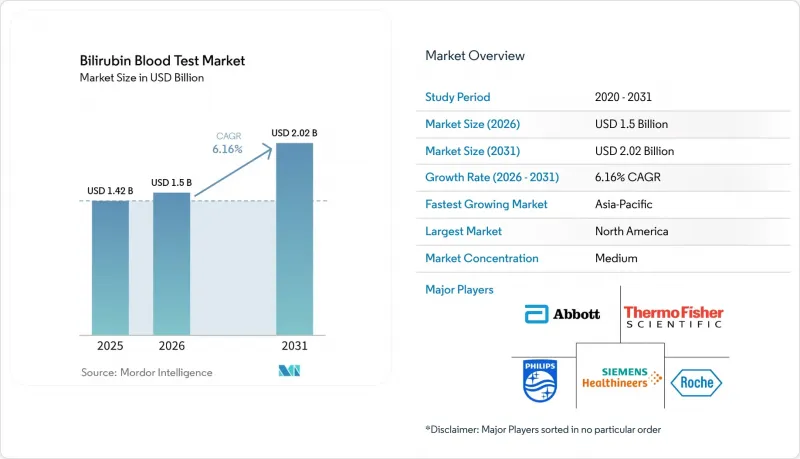

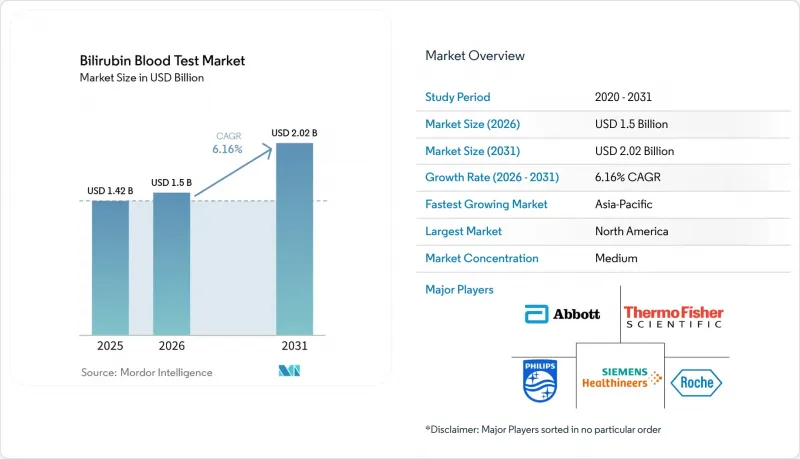

Mordor Intelligence에 의하면, 빌리루빈 혈액검사 시장 규모는 2025년 14억 2,000만 달러로 평가되었고, 2026년에는 15억 달러로 추정되고, 2031년까지 20억 2,000만 달러에 이를 것으로 예상되며, 2026-2031년 CAGR 6.16%로 성장할 전망입니다.

본 보고서는 검사 유형별(총 빌리루빈, 직접 빌리루빈, 간접 빌리루빈), 제품 유형별(시약, 교정제, 분석기), 기술별(실험실 기반, POC 혈액 검사, 경피 검사), 용도별(신생아 황달, 간 기능, 기타), 최종 사용자별(병원/신생아 중환자실(NICU), 진단 실험실, 기타), 지역별(북미, 유럽, 아시아태평양, 중동 및 아프리카, 남미)로 분류되어 있습니다. 시장 전망치는 달러 기준 금액으로 제시되어 있습니다.

세계의 빌리루빈 혈액 검사 시장 동향 및 인사이트

신생아 황달 선별검사의 실시 빈도 증가

많은 병원 시스템에서 신생아 빌리루빈 선별검사가 권장되는 관행에서 일상적인 진료 요건으로 전환됨에 따라, 빌리루빈 혈액 검사 시장은 안정적인 수요 기반을 확보해 가고 있습니다. AAP(미국소아과학회)의 기술 보고서는 퇴원 전 빌리루빈 측정을 신생아 관리의 핵심으로 계속 강조하고 있으며, 이에 따라 고위험군 영아에 대한 총 빌리루빈 검사의 반복 실시와 추적 측정을 권장하고 있습니다. 호주에서는 2026년 1월, 뉴사우스웨일스주(NSW)가 신생아 황달 지침을 개정하여 더 광범위한 임신 주수에 걸쳐 경피 빌리루빈 검사를 의무화함에 따라 이러한 경향이 더욱 강화되었습니다. 빌리루빈 혈액 검사 시장은 2차 검사 실시로 인해 혜택을 보고 있습니다. 이는 황달이 있는 영아의 경우, 조기에 담즙 정체를 배제해야 할 때 결합형 빌리루빈 측정이 필요한 경우가 많기 때문입니다. 또한, 스위스 소아과 지침에 따르면 2026년에 Biliscreen.org를 통해 이 검사 경로가 공식적으로 정해졌습니다. 이는 단일 검사가 아니라, 하나의 임상적 사건에 대해 선별 검사, 확정 진단, 세분화 검사가 이루어짐을 의미하며, 환자 1인당 검사 실시 빈도가 구조적으로 높아지는 요인이 되고 있습니다.

증가하는 간 질환 진단 건수

빌리루빈 혈액 검사 시장은 일상적인 간 질환 검사에서도 지지를 받고 있습니다. 왜냐하면 총 빌리루빈은 1차 진료부터 전문의 진료에 이르기까지 간 기능 검사의 표준 항목으로 계속 자리 잡고 있기 때문입니다. MASLD는 전 세계 성인의 38%에게 영향을 미치고 있으며, 빌리루빈을 비롯한 기타 간 기능 지표를 포함하는 대규모 패널 검사 수요를 뒷받침하고 있습니다. 이러한 수요는 새로운 섬유화 평가 도구로 대체될 수 없습니다. 이는 빌리루빈이 FibroTest, Hepascore, SteatoTest 등의 다중 마커 알고리즘에 포함되어 있어, 이를 통해 검사가 비침습적인 간 질환 평가와 연계되기 때문입니다. 빌리루빈 혈액 검사 시장은 MASH 및 MASLD 치료 과정에서의 치료 모니터링 및 진단 범위의 확대로 인해 더욱 성장하고 있습니다. 여기에는 비침습적 간 진단 역량을 확대하기 위해 2025년에 Fibronostics가 진행한 인수도 포함됩니다. 용혈성 질환 역시 지속적인 수요층을 형성하고 있습니다. 2025년의 임상 증거에 따르면, 겸상적혈구빈혈에서 혈관 내 용혈을 모니터링하는 데 있어 총 빌리루빈과 관련 지표가 여전히 실용적인 도구임이 계속해서 입증되었기 때문입니다.

분석 장비와 비침습적 기기의 높은 비용

빌리루빈 혈액 검사 시장은 여전히 자본적 장벽에 직면해 있습니다. 이는 대형 공급업체에서 제조한 경피 빌리루빈 측정 장비가 소규모 시설에 있어서는 여전히 고가이기 때문입니다. 2025년 일본의 연구에 따르면, 시판 장치의 단가가 대당 5,000-1만 달러인 것으로 지적되고 있으며, 이로 인해 신생아 선별 검사를 실시하더라도 설비 예산이 제한적인 1차 의료 및 지역 의료 현장에서의 도입이 제한되고 있습니다. 중국의 공공 조달 데이터에 따르면, 병원들은 여전히 신생아용 경피형 측정 기기에 대한 예산을 신중하게 편성하고 있으며, 룽옌 제1병원은 대당 1만 3,000위안(대당 1,790달러 상당)에 3대를 입찰했습니다. 이러한 비용 제약으로 인해 빌리루빈 혈액 검사 시장의 전반적인 확산이 지연되고 있으며, 특히 시립 병원이나 지역 클리닉이 선별 검사 장비와 보다 광범위한 임상 검사에 대한 투자 중 어느 쪽을 선택할지 고민해야 하는 상황에서 이러한 현상이 두드러지게 나타나고 있습니다. 한편, 저비용 혁신 기술도 등장하고 있으며, 앞서 언급한 일본의 조사에서는 단가가 100달러에 가까운, 혈청 빌리루빈 수치와 임상적으로 유의미한 상관관계를 보이는 웨어러블형 TcB 프로토타입이 검증되었습니다. 이는 향후 가격 경쟁이 격화될 가능성을 시사하고 있습니다.

부문별 분석

빌리루빈 혈액 검사 시장에서 2025년에는 총 빌리루빈 검사가 시장 점유율의 61.68%를 차지했습니다. 이 부문은 신생아 황달 프로토콜, 간 기능 패널, 종합 생화학 검사에서 여전히 첫 번째로 선택되는 검사법으로 자리 잡고 있습니다. AAP(미국소아과학회)의 지침에서는 퇴원 전 빌리루빈 측정과 정기적인 추적 관찰을 신생아 관리의 핵심으로 삼고 있으며, 이를 통해 여러 차례의 내원 시에 걸친 검사 의뢰가 장려되고 있습니다. 신생아 담즙 정체 검사, MASLD(다인자성 비알코올성 지방간 질환)와 관련된 간담도계 평가, 용혈성 질환 평가에서 빌리루빈 분획 측정이 필요한 사례가 증가하고 있어, 직접 빌리루빈 검사는 2031년까지 연평균 7.94%의 성장률을 보일 것으로 예측됩니다.

간접 빌리루빈은 일반적으로 별도로 의뢰되는 검사가 아니라 파생 값으로 보고되지만, 여전히 중요합니다. 임상의들이 황달의 간전, 간내, 간후 유형을 구별하는 데 이를 활용하기 때문에 임상 분류에서 여전히 중요한 역할을 하고 있습니다. 2025년 사라세미아에 관한 연구에 따르면, 비결합형 빌리루빈 수치가 59.8 마이크로몰/L를 초과할 경우, UGT1A1 변이체 보균 여부를 예측하는 곡선 아래 면적(AUC)이 0.90인 것으로 나타나, 보다 전문적인 추적 관찰 채널에서의 그 중요성을 뒷받침하고 있습니다. 따라서 빌리루빈 혈액 검사 시장은 단순한 총 빌리루빈 검사 모델에서 보다 광범위한 분획 검사 조합으로 전환되고 있습니다. 특히 소아 간장학 및 신생아 진단 시스템이 표준화되고 있는 분야에서 이러한 경향은 두드러집니다.

2025년 빌리루빈 혈액 검사 시장 규모에서 시약 및 검사용 소모품은 63.23%의 점유율을 차지했습니다. 이러한 우위는 시약 임대 계약을 통해 창출되는 지속적인 수익 구조를 반영하고 있습니다. 이 계약에서는 플랫폼이 일회용 분석기 판매가 아닌, 수년에 걸친 공급 계약과 연계되어 있습니다. 이 모델을 통해 기존 공급업체는 병원 검사실 고객을 대상으로 더 강력한 이탈 방지 효과와 더 안정적인 수익 전망을 확보할 수 있습니다. 앨버타 프리시전 래버러토리즈는 2025년, 지역 거점 전체에 로슈사의 Cobas Pure 분석 장비를 도입함으로써 이러한 추세를 더욱 공고히 했습니다. 이를 통해 단일 공급업체에 의한 생화학 검사의 표준화가 촉진되었으며, 빌리루빈 시약에 대한 지속적인 수요가 확보되었습니다.

교정기 및 품질 관리 제품은 여전히 매출 규모가 작은 부문이지만, 추적성 기준이 강화되고 플랫폼 간 비교 가능성이 조달상의 중요한 과제로 대두됨에 따라 전략적 중요성이 커지고 있습니다. 빌리루빈 혈액 검사 업계에서는 여러 분석기 제품군을 지원하며, 측정법 간 편차를 줄일 수 있는 소아용 표준 물질에 대한 관심이 계속해서 높아질 것으로 보입니다. 빌리루빈 분석 장치와 측정기는 전용 경피 측정 기기 및 휴대용 혈청 분석 장치의 지원에 힘입어 7.66%라는 가장 높은 성장률을 보이는 제품 유형입니다. 베크만 콜터사가 인도에서 실시한 DxC 500i에 관한 2025년 조사 결과, 고농도 총 빌리루빈에서 실험실 내 CV가 1.13%였으며, 비교 대상 시스템과의 상관계수(r)가 0.984로 뛰어난 분석 성능을 보여주었으며, 대규모 3차 의료기관에서의 도입이 입증되었습니다. 또한, 빌리루빈 혈액 검사 시장에서는 저비용 웨어러블 TcB(경피 빌리루빈) 측정 장치의 개발로 인해 하드웨어 측면에서 장기적인 압박도 발생하고 있습니다. 이로 인해 신생아 선별검사에 대한 접근성은 확대되는 반면, 기존 장비 제조업체의 가격 우위는 축소될 가능성이 있습니다.

지역별 분석

2025년 기준으로 북미는 빌리루빈 혈액 검사 시장 규모의 48.21%를 차지했습니다. 이 지역이 1위를 차지하는 이유는 AAP(미국소아과학회)의 신생아 선별검사 지침이 임상 현장에 널리 정착되어 있으며, 메디케어의 보상 대상에 간기능 검사 패널 코드 체계 내의 총 빌리루빈과 직접 빌리루빈이 포함되어 있기 때문입니다. 캐나다의 빌리루빈 혈액 검사 시장은 앨버타주가 2025년까지 지역 병원 전체에 도입할 예정인 로슈사의 ‘Cobas Pure’를 포함한 검사실 표준화 프로그램에 힘입어 성장하고 있습니다. 유럽의 경우, 각국의 프로토콜이 보다 광범위한 NICE(영국 국립의료기술평가기구) 방식의 선별 검사 기법 및 활발히 진행 중인 IFCC(국제임상화학연합)의 표준화 작업과 공존하고 있기 때문에 여전히 보다 다양한 상황에 놓여 있습니다. 보편적인 선별검사로 인해 지역 전체의 검사 건수는 꾸준히 증가하고 있으며, 소아과 조사에 따르면, 특정 유럽 국가들에서 중증 고빌리루빈혈증과 관련된 영아 사망률은 1990년 출생 100만 명당 21.4건에서 2019년에는 4.2건으로 감소했습니다.

아시아태평양은 빌리루빈 혈액 검사 시장에서 가장 빠르게 성장하고 있는 지역으로, 2031년까지의 예상 연평균 성장률(CAGR)은 8.45%입니다. 중국에서는 병원들이 신생아용 경피 빌리루빈 측정기를 적극적으로 도입함으로써, 그 보급 확대에 일조하고 있습니다. 예를 들어, 2025년 9월 룽옌 제1병원이 실시한 입찰에서는 1대당 1만 3,000위안(1대당 1,790달러에 해당)에 3대가 조달되었습니다. 인도에서는 현장 진단(POC) 혈청 검사를 통해 시장이 확대되고 있으며, 2025년 첸나이에서 실시된 ‘Bilistick System 2.0’ 검증 결과, 환자 수가 많은 공립 병원 환경에서 임상적으로 유용한 성능이 입증되었습니다. 일본과 호주는 산과 의료 분야에서 경피 빌리루빈 측정(TcB)의 일상적인 사용과 개정된 보편적 선별 검사 지침에 따라 신생아 빌리루빈 검사가 빈번하게 이루어지고 있어, 이는 시장 성장을 더욱 촉진하는 요인이 되고 있습니다.

중동 및 아프리카와 남미의 빌리루빈 혈액 검사 시장은 절대적인 규모 면에서는 여전히 작지만, 두 지역 모두 상당한 성장 잠재력을 지니고 있습니다. GCC는 집중화된 신생아 의료 인프라의 혜택을 누리고 있는 반면, 남아프리카공화국의 3차 의료기관 네트워크는 실험실 기반 검사 건수를 지속적으로 뒷받침하고 있습니다. 사하라 이남 아프리카와 중동 일부 지역에서도 빌리루빈 모니터링에 대한 수요가 증가하고 있습니다. 이는 남성 인구에서 G6PD 결핍증의 유병률이 15%에서 26%에 달할 수 있어, 용혈성 황달에 대한 검사 수요가 증가하고 있기 때문입니다. 라틴아메리카는 간 관련 검사 분야에서 여전히 중요한 시장입니다. 이 지역의 MASLD(다단계 지방간 질환) 유병률은 44.37%로 전 세계에서 가장 높으며, 이것이 정기 간 기능 검사 패널에서 빌리루빈 검사 수요를 뒷받침하고 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.26According to Mordor Intelligence, the bilirubin blood test market size is expected to increase from USD 1.42 billion in 2025 to USD 1.5 billion in 2026 and reach USD 2.02 billion by 2031, growing at a CAGR of 6.16% over 2026-2031.

This report is Segmented by Test Type (Total, Direct, Indirect), Product Type (Reagents, Calibrators, Analyzers), Technology (Lab-Based, POC Blood, Transcutaneous), Application (Neonatal Jaundice, Liver Function, and More), End User (Hospitals/NICUs, Diagnostic Labs, and More), and Geography (North America, Europe, Asia-Pacific, MEA, South America). The Market Forecasts are Provided in Terms of Value in USD.

Global Bilirubin Blood Test Market Trends and Insights

Rising Neonatal Jaundice Screening Intensity

The bilirubin blood test market is gaining a stable demand base because neonatal bilirubin screening has moved from a preferred practice to a routine care expectation in many hospital systems. The AAP technical report kept predischarge bilirubin measurement central to newborn care, which supports repeated total bilirubin testing and follow-up measurement in at-risk infants. Australia strengthened this pattern when NSW updated its neonatal jaundice guideline in January 2026 and mandated universal transcutaneous bilirubin screening with broader gestational coverage. The bilirubin blood test market also benefits from a second testing step because jaundiced infants often need conjugated bilirubin measurement when cholestasis must be ruled out early, and Swiss pediatric guidance formalized that pathway through Biliscreen.org in 2026. This means one clinical event can generate screening, confirmation, and fractionation rather than a single assay, which keeps per-patient test intensity structurally high.

Growing Liver Disease Diagnostic Volumes

The bilirubin blood test market is also supported by routine liver disease workups because total bilirubin remains a standard component of liver function testing across primary care and specialist pathways. MASLD affects 38% of adults worldwide, which sustains large panel volumes that include bilirubin alongside other liver markers. This demand is not displaced by newer fibrosis tools because bilirubin is built into multimarker algorithms such as FibroTest, Hepascore, and SteatoTest, which keep the assay tied to noninvasive liver disease assessment. The bilirubin blood test market is further supported by treatment monitoring and diagnostic expansion in MASH and MASLD workflows, including the 2025 acquisition by Fibronostics to broaden noninvasive liver diagnostics capacity. Hemolytic disease adds another recurring layer because 2025 clinical evidence continued to show that total bilirubin and related markers remain practical tools for monitoring intravascular hemolysis in sickle cell anemia.

High Cost of Analyzers and Noninvasive Devices

The bilirubin blood test market still faces a capital barrier because transcutaneous bilirubinometers from established suppliers remain expensive for smaller facilities. A 2025 Japanese study noted commercial device pricing of USD 5,000 to USD 10,000 per unit, which limits adoption in primary and community settings that screen newborns but do not have large equipment budgets. Public procurement data in China still showed that hospitals were budgeting carefully for neonatal transcutaneous units, with Longyan First Hospital tendering 3 units at RMB 13,000 each, equal to USD 1,790 per unit. These cost limits slow wider penetration across the bilirubin blood test market, especially where township hospitals and community clinics must choose between screening equipment and broader chemistry investments. At the same time, low-cost innovation is emerging, and the same Japanese research validated a wearable TcB prototype with a unit cost near USD 100 and clinically meaningful correlation with serum bilirubin, which suggests that pricing pressure could intensify over time.

Other drivers and restraints analyzed in the detailed report include:

- Adoption of Point-of-Care Bilirubin Workflows

- Remote Newborn Follow-Up and Digital Jaundice Monitoring

- Assay Standardization and Interference Limitations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Within the bilirubin blood test market, total bilirubin tests held 61.68% of the bilirubin blood test market share in 2025. This segment remains the first-line assay in neonatal jaundice protocols, liver panels, and comprehensive chemistry testing. The AAP framework kept predischarge bilirubin measurement and repeat follow-up central to newborn care, which supports repeated ordering across multiple encounters. Direct bilirubin tests are projected to grow at 7.94% through 2031 because neonatal cholestasis workups, MASLD-related hepatobiliary assessment, and hemolytic disorder evaluation increasingly require bilirubin fractionation.

Indirect bilirubin remains important even though it is usually reported as a derived value rather than a separately ordered assay. It still shapes clinical classification because clinicians use it to separate pre-hepatic, hepatic, and post-hepatic patterns of jaundice. A 2025 thalassemia study showed that unconjugated bilirubin above 59.8 µmol/L predicted UGT1A1 variant carriage with an area under the curve of 0.90, which supports its relevance in more specialized follow-up pathways. The bilirubin blood test market is therefore shifting from a simple total bilirubin model toward a broader fractionation mix, especially where pediatric hepatology and neonatal referral systems are becoming more standardized.

Reagents and assay consumables accounted for 63.23% share of the bilirubin blood test market size in 2025. Their lead reflects the recurring revenue structure created by reagent-rental agreements, where platforms are tied to multiyear supply contracts rather than one-time analyzer sales. This model gives established vendors stronger switching protection and steadier revenue visibility across hospital laboratory accounts. Alberta Precision Laboratories reinforced this pattern in 2025 when it implemented Roche Cobas Pure analyzers across regional sites, which supported single-vendor chemistry standardization and locked in ongoing bilirubin reagent demand.

Calibrators and quality controls remain a smaller revenue category, but they are gaining strategic weight as traceability standards tighten and cross-platform comparability becomes a larger procurement issue. The bilirubin blood test industry is likely to see continued interest in pediatric control materials that can support multiple analyzer families and reduce method-to-method drift. Bilirubin analyzers and meters are the fastest-growing product type at 7.66%, supported by dedicated transcutaneous devices and portable serum analyzers. Beckman Coulter's 2025 study of the DxC 500i in India showed strong analytical performance with a within-lab CV of 1.13% for higher-concentration total bilirubin and an r of 0.984 against comparator systems, which supports deployment in large tertiary settings. The bilirubin blood test market is also seeing longer-term hardware pressure from low-cost wearable TcB development, which could expand neonatal screening access while narrowing the pricing advantage of incumbent device makers.

Geography Analysis

North America accounted for 48.21% share of the bilirubin blood test market size in 2025. The region leads because AAP newborn screening guidance is widely embedded in clinical practice and because Medicare reimbursement includes total and direct bilirubin within the hepatic function panel coding structure. The bilirubin blood test market in Canada is also supported by laboratory standardization programs, including Alberta's 2025 Roche Cobas Pure implementation across regional hospitals. Europe remains a more heterogeneous setting because country-specific protocols coexist with broader NICE-style screening approaches and active IFCC standardization work. Universal screening has still kept testing volumes durable across the region, and pediatric research showed that extreme hyperbilirubinemia-related infant mortality in select European countries fell from 21.4 per million live births in 1990 to 4.2 per million in 2019.

Asia-Pacific is the fastest-growing geography in the bilirubin blood test market, with forecast CAGR of 8.45% through 2031. China is driving part of that expansion through active hospital procurement of neonatal transcutaneous bilirubinometers, including the September 2025 Longyan First Hospital tender for 3 units at RMB 13,000 each, equal to USD 1,790 per unit. India is expanding through point-of-care serum testing, and the 2025 Chennai validation of Bilistick System 2.0 showed clinically useful performance in a high-volume public hospital environment. Japan and Australia add another growth layer because routine TcB use in maternity care and updated universal screening guidance continue to support frequent neonatal bilirubin checks.

The bilirubin blood test market in the Middle East and Africa and in South America remains smaller in absolute size, but both regions carry targeted growth potential. GCC countries benefit from concentrated neonatal care infrastructure, while tertiary hospital networks in South Africa continue to support laboratory-based testing volume. Parts of Sub-Saharan Africa and the Middle East also face elevated bilirubin monitoring need because G6PD deficiency prevalence can range from 15% to 26% in male populations, which increases demand for hemolytic jaundice workups. Latin America remains important for liver-related testing because MASLD prevalence is highest globally in the region at 44.37%, which sustains bilirubin demand within routine hepatology panels.

- Abbott Laboratories

- Beckton Dickinson

- DiaSys Diagnostic Systems

- Dragerwerk

- Elitech Group

- Fortress Diagnostics

- Roche

- FUJIFILM Wako Pure Chemical Corporation

- HORIBA Medical

- Konica Minolta

- Koninklijke Philips

- Mennen Medical Ltd.

- Nova Biomedical

- QuidelOrtho

- Randox Laboratories

- Reichert

- SEKISUI Diagnostics, LLC

- Mindray

- Siemens Healthineers

- Thermo Fisher Scientific

- Werfen, S.A.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Neonatal Jaundice Screening Intensity

- 4.2.2 Growing Liver Disease Diagnostic Volumes

- 4.2.3 Expansion of Routine Hospital Chemistry Testing

- 4.2.4 Adoption of Point-of-Care Bilirubin Workflows

- 4.2.5 Increasing Use of Transcutaneous Pre-Screening

- 4.2.6 Remote Newborn Follow-Up and Digital Jaundice Monitoring

- 4.3 Market Restraints

- 4.3.1 High Cost of Analyzers and Noninvasive Devices

- 4.3.2 Need for Serum Confirmation at Clinical Decision Thresholds

- 4.3.3 Assay Standardization and Interference Limitations

- 4.3.4 Cross-Platform Assay Bias and Preanalytical Interference Risk

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Test Type

- 5.1.1 Total Bilirubin Tests

- 5.1.2 Direct Bilirubin Tests

- 5.1.3 Indirect Bilirubin Tests

- 5.2 By Product Type

- 5.2.1 Reagents and Assay Consumables

- 5.2.2 Calibrators and Quality Controls

- 5.2.3 Bilirubin Analyzers and Meters

- 5.3 By Technology

- 5.3.1 Laboratory-Based Testing

- 5.3.2 Point-of-Care Blood Testing

- 5.3.3 Transcutaneous Screening Systems

- 5.4 By Application

- 5.4.1 Neonatal Jaundice Screening and Monitoring

- 5.4.2 Liver Function Assessment

- 5.4.3 Hemolytic Disorder Assessment

- 5.4.4 Pre-operative and Routine Health Screening

- 5.5 By End User

- 5.5.1 Hospitals and NICUs

- 5.5.2 Diagnostic Laboratories

- 5.5.3 Maternity and Neonatal Clinics

- 5.5.4 Outpatient and Ambulatory Care Centers

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 Australia

- 5.6.3.5 South Korea

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East & Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East & Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 Abbott Laboratories

- 6.3.2 Beckman Coulter, Inc.

- 6.3.3 DiaSys Diagnostic Systems GmbH

- 6.3.4 Dragerwerk AG & Co. KGaA

- 6.3.5 ELITechGroup

- 6.3.6 Fortress Diagnostics

- 6.3.7 F. Hoffmann-La Roche Ltd

- 6.3.8 FUJIFILM Wako Pure Chemical Corporation

- 6.3.9 HORIBA Medical

- 6.3.10 Konica Minolta, Inc.

- 6.3.11 Koninklijke Philips N.V.

- 6.3.12 Mennen Medical Ltd.

- 6.3.13 Nova Biomedical

- 6.3.14 QuidelOrtho Corporation

- 6.3.15 Randox Laboratories Ltd.

- 6.3.16 Reichert, Inc.

- 6.3.17 SEKISUI Diagnostics, LLC

- 6.3.18 Shenzhen Mindray Bio-Medical Electronics Co., Ltd.

- 6.3.19 Siemens Healthineers AG

- 6.3.20 Thermo Fisher Scientific Inc.

- 6.3.21 Werfen, S.A.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment