|

시장보고서

상품코드

2063645

트리클라벤다졸 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Triclabendazole - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

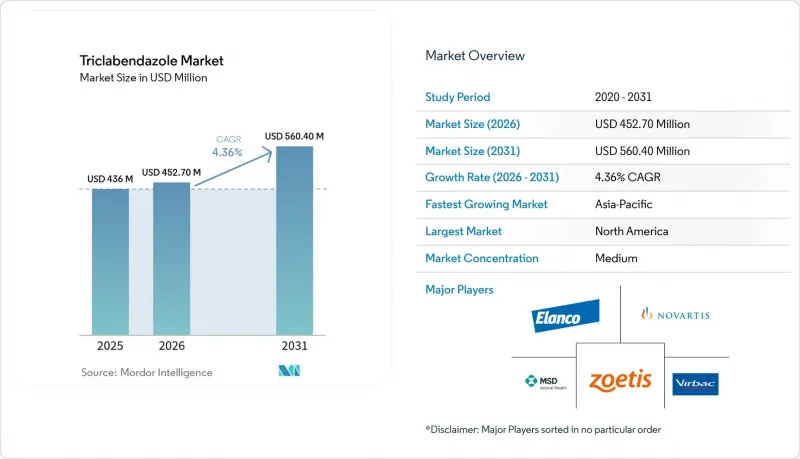

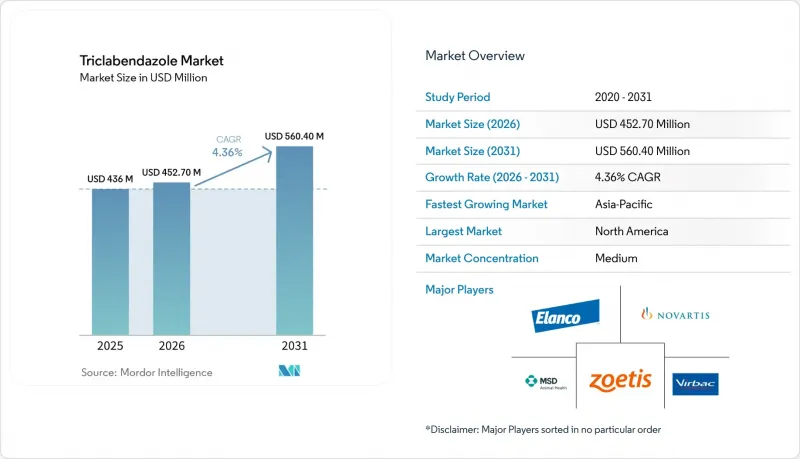

Mordor Intelligence에 의하면, 트리클라벤다졸 시장 규모는 2025년에 4억 3,600만 달러, 2026년에 4억 5,270만 달러, 2031년까지 5억 6,040만 달러에 이를 것으로 예측되며, 2026년부터 2031년까지 CAGR 4.36%로 성장할 전망입니다.

본 보고서는 용도별(수의용 가축{소, 양, 염소} 및 인간용), 제품 유형별(브랜드 제품 및 제네릭), 유통 채널별(동물병원, 동물진료소, 약국/드럭스토어), 그리고 지역별(북미, 유럽, 아시아태평양, 중동 및 아프리카, 남미)로 분류되어 있습니다. 본 보고서에서는 상기 각 부문 시장 규모(달러)를 제시하고 있습니다.

세계 트리클라벤다졸 시장 동향 및 분석

내성이 나타났음에도 불구하고, 다단계 효능 덕분에 트리클라벤다졸이 표준 치료법으로 자리 잡았습니다.

트리클라벤다졸은 이동 중인 유충이 급성 간 손상을 유발하는 경우, 표준 치료 프로토콜에서 미성숙 및 성충 모두의 파시오라속을 표적으로 하는 유일하게 널리 사용되는 흡충 구제제입니다. 미국의 인간 파시오라증에 대한 적응증 표시 및 약리학적 특성 평가가 이러한 다단계 효능 프로파일을 뒷받침한다는 사실이 확립되어 있으며, 이는 내성 징후가 보고되고 있음에도 불구하고 수의학 분야에서 이 약물에 대한 지속적인 의존을 뒷받침하고 있습니다. 『Frontiers in Veterinary Science』지에 게재된 연구 결과에 따르면, 높은 유효성과 이에 상응하는 생화학적 회복 양상이 확인되었으며, 대상에 한정된 사용 체계에서의 지속성이 입증되었습니다. 호주의 생산자 주도 프로그램에서는 감시 대상 낙농장 전체에서 내성이 확인되었습니다. 그러나 생산자들은 대체 약물에 비해 트리클라벤다졸이 미성숙 흡충에 대해 나타내는 독특한 활성 덕분에 계절별 전략에서 이 약제의 사용을 유지하고 있으며, 겨울 전 유충이 가장 많이 발생하는 시기에 맞추어 투여했을 때 이유 송아지의 성장 촉진 효과가 보고되고 있습니다.

WHO의 권고와 FDA의 승인을 통해 상업적 및 프로그램적 접근 경로가 확대되었습니다.

인체용 트리클라벤다졸 제제인 ‘에가텐’은 간흡충증 치료제로 FDA의 승인을 받았으며, 이를 통해 규제 환경 하에서의 안전성과 사용에 관한 불확실성이 해소됨으로써, 스튜어드십 및 의약품 안전성 감시 데이터가 중시되는 수의학 분야에서 이 약물의 수용을 간접적으로 뒷받침했습니다. 인간 간흡충증을 대상으로 한 WHO와의 협력 기부 프로그램은 세계 공중보건 분야에서 그 역할을 확고히 했으며, 그 결과 신청 자료에서 인간 대상 사용 경험을 바탕으로 한 안전성 및 노출에 관한 지식이 인용됨에 따라, 수의학 시장에서 제네릭 의약품의 진입 장벽이 낮아졌습니다. 이러한 파급 효과로 인해, 인수공통감염병 대책에 대한 논의가 반추동물용 의약품 정책에 영향을 미치는 신흥 시장에서 규제 승인 절차가 신속화되었으며, 트리클라벤다졸 시장이 민관 협력 채널을 통해 새로운 처방자층에 도달할 수 있게 되었습니다. 동아프리카 및 동남아시아의 일부 관할 구역에서는 인간 대상 프로그램을 통한 검증이 수의학적 승인 및 유통 인프라 구축을 촉진하고, 제품의 지속성을 높였으며, 계절별 치료 계획을 방해하던 재고 부족 현상을 줄였습니다. 이러한 접근성 증진 요인들은 증거에 기반한 수의학적 프로토콜을 보완하며, 항생제 내성 관리와 질병 대책 목표 간의 균형을 맞추는 약물 목록에 포함되도록 뒷받침하고 있습니다.

트리클라벤다졸에 대한 내성 사례가 보고됨에 따라, 1차 치료제로서의 유효성이 저하되어 치료 프로토콜을 조정해야 할 필요성이 대두되고 있습니다.

2026년까지 여러 지역에서 내성이 확인되고, 효능이 다소 떨어지는 점에 대한 타협이 허용 가능한 범위 내에 있는 경우, 수의학 현장에서는 진단에 기반한 투여나 대체 약물군을 활용한 보다 빈번한 로테이션으로 전환하고 있습니다. 호주에서는 체계적인 생산자 프로그램을 통해 최근 실시된 검사에서 모니터링 대상인 모든 낙농장에서 내성이 확인되었습니다. 그러나 이러한 프로그램에서는 측정 가능한 생산량 감소가 관찰되지 않았습니다. 이 결과에 대해 실무자들은 대체 의약품과 비교했을 때 여전히 급성 질환의 위험을 줄여주는 부분적인 효능 때문이라고 보고 있습니다. 인간 간흡충증에 대한 조사 결과, 숙주의 미생물군집 특성이 치료 결과와 관련이 있는 것으로 나타났으며, 비반응군은 반응군과 비교해 다른 미생물학적 특성을 보이는 것으로 밝혀졌습니다. 이로 인해 치료 실패의 모든 원인을 기생충의 유전적 요인에만 돌리는 판단은 더욱 복잡해지고 있습니다. 2024년 10월 Farm Advisory Service가 발표한 자료에 따르면, 내성 위험이 높아지고 있는 만큼 수의사들은 트리클라벤다졸 시장에서 감염 부하가 높은 시기에 효능을 유지하기 위한 ‘검사 및 치료’, 분변 항원 모니터링, 그리고 계획적인 약물 순환 사용을 강조하고 있습니다. 제약 기업들은 내성 유전자형 분석 및 대변 항원 검사에 대한 제휴에 자금을 지원하고 있지만, 적정 사용 프로그램으로 인해 중소 제네릭 의약품 공급업체의 비용이 증가하면서, 경쟁이 치열한 유통 채널에서 저가 진출기업들의 수익성이 압박받고 있습니다.

부문별 분석

2025년 기준으로 트리클라벤다졸 시장의 78.77%를 차지하는 가축용 수의약품은 2031년까지 연평균 성장률(CAGR) 5.34%로 성장할 것으로 전망됩니다. 이는 기후 변화로 인한 감염 위험 증가와 확진 사례에 대한 책임감 있는 관리에 기반한 반복적인 개입을 모두 반영한 것입니다. 수요는 배수가 잘되지 않는 목초지, 범람원, 관개된 사료 재배지가 감염 창구를 유지하는 중간 숙주인 달팽이의 서식에 적합한 온대 및 아열대 지역에 집중되어 있습니다. 습한 저지대나 멕시코만 연안의 목초지에서 이루어지는 북미의 소 사육 사업에서는 계절마다 반복적인 치료가 유지되고 있는 반면, 영국 제도와 북서유럽의 소 무리에서는 비가 더 많이 내리는 여름과 온화한 겨울에 대응하기 위해 안전한 방목 간격을 단축하고, 가을 치료 시기를 앞당기고 있습니다. 가축 부문의 지속가능성은 트리클라벤다졸 시장에서 나타나는 세 가지 시너지 효과를 내는 변화에 힘입고 있습니다. 기후 변화의 추세로 인해 노출 기간이 길어지고 있으며, 이에 따라 계절별 치료 계획을 도입하는 가축 사육 농가의 수가 증가하고 있습니다. 분변 항원 ELISA 및 분자진단 기술을 통해 일률적인 투여 대신 표적을 좁힌 개입이 가능해졌으며, 이로 인해 농장당 투여량이 감소하고 임상 성과와 약제 관리가 개선되고 있습니다. 이러한 요인들이 복합적으로 작용하여, 2031년까지의 트리클라벤다졸 시장에서 수의용 가축 부문이 시장 평균을 상회하는 성장을 이룰 수 있는 기반이 되고 있습니다.

지역별 분석

2025년 기준으로 북미는 트리클라벤다졸 시장 점유율의 41.34%를 차지하고 있으며, 이는 선진적인 수의학 인프라, 진단 기술의 광범위한 보급, 그리고 임상 통합형 처방을 촉진하는 규제된 유통 체계를 반영한 것입니다. 미국은 습지대나 멕시코만 연안의 목초지에서 지속되는 흡충 감염으로 인해 지역별 판매량에서 1위를 차지하고 있으며, 고위험 지역에서는 연 2회의 투약이 일반적입니다. 감시 중심의 프로토콜은 시장의 회복력을 강화하고 있으며, 트리클라벤다졸 시장에서 내성 우려를 관리하기 위해 진단에 기반한 확인이 투여 시기 및 로테이션에 대한 지침으로 활용되고 있습니다. 캐나다의 성장은 통합된 낙농 건강 프로그램과 제품 유통을 원활하게 하는 국경을 초월한 규제 조화와 밀접한 관련이 있습니다. 멕시코에서는 농촌 지역 접근성이나 가격에 민감한 계층이 제네릭 의약품을 선호하는 경향이 있지만, 지역에 따라 수의사 접근성이 달라 미국이나 캐나다에 비해 보급 속도가 더딘 임베디드니다.

아시아태평양은 기후 변화로 인한 달팽이의 서식지 확대와 다양한 농업 생태계 내 반추동물 사육 시스템의 강화 등을 배경으로, 연평균 성장률(CAGR) 8.32%라는 가장 빠른 성장세를 기록할 것으로 전망됩니다. 칭하이·티베트 고원에서는 고원의 기후 조건을 바탕으로 한 모델링 결과, 더 높은 고지대로의 흡충 전파에 적합한 지리적 범위가 확대되고 있는 것으로 나타났으며, 이에 따라 야크와 양의 방목지에서는 이미 예방적 감시 및 대응 계획이 추진되고 있습니다.

유럽 시장은 성장 요인에 힘입어 성장하고 있지만, 관리 체계의 틀로 인해 낙농 지역에서의 예방적 투여가 제한되고 있습니다. 남유럽에서는 겨울철 기온 상승과 강우 패턴의 변동으로 인해 정기적인 치료 대상 지역이 새롭게 확대되고 있는 반면, 동유럽의 생산자들은 인도와 중국공급업체로부터 제네릭 의약품 도입을 가속화하고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.23According to Mordor Intelligence, the triclabendazole market size is projected to be USD 436 million in 2025, USD 452.70 million in 2026, and reach USD 560.40 million by 2031, growing at a CAGR of 4.36% from 2026 to 2031.

This report is Segmented by Application (Veterinary Livestock {Cattle, Sheep, and Goats}, and Human Health), by Product Type (Brand and Generic), by Distribution Channel (Veterinary Hospitals, Veterinary Clinics, and Pharmacies / Drug Stores), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The Report Offers the Value (USD) for the Above Segments.

Global Triclabendazole Market Trends and Insights

Multi-Stage Efficacy Anchors Triclabendazole as Protocol Standard Despite Resistance Emergence

Triclabendazole is the only widely used flukicide that targets both immature and adult Fasciola species in standard treatment protocols when migrating juveniles drive acute hepatic pathology. It is established that the United States labeling for human fascioliasis and pharmacological characterization reinforces this multi-stage efficacy profile, which underpins continued veterinary reliance despite documented resistance signals. Results published in Frontiers in Veterinary Science showed high efficacy along with corresponding biochemical recovery patterns, supporting durability in targeted use frameworks. Australian producer-led programsconfirmed resistance across monitored dairy properties. Yet, producers maintained triclabendazole in seasonal strategies due to its unique immature fluke activity relative to alternatives, with reported gains in weaner growth when timing aligned to pre-winter juvenile peaks.

WHO Endorsement and FDA Validation Expand Commercial and Programmatic Access Channels

Egaten, the human triclabendazole product, is FDA approved for fascioliasis, which helped reduce ambiguity on safety and use in regulated settings and indirectly supported veterinary acceptance, where stewardship and pharmacovigilance data are valued. WHO-aligned donation programs for human fascioliasis cemented a global public health role that, in turn, lowered barriers for generics in veterinary markets as dossiers referenced safety and exposure insights from the human use experience. The downstream effect includes faster regulatory pathways in emerging markets where zoonotic disease control narratives influence ruminant drug policies, helping the triclabendazole market reach new prescriber bases through aligned public and private channels. In several jurisdictions across East Africa and Southeast Asia, validation from human programs catalyzed veterinary approvals and distribution infrastructure, improving product continuity and reducing stockouts that had hampered seasonal treatment planning. These access enablers complement evidence-based veterinary protocols and encourage formulary adoption that balances resistance stewardship with disease control goals.

Documented Triclabendazole Resistance Erodes First-Line Efficacy and Compels Protocol Adjustments

Resistance has been confirmed in multiple regions by 2026, shifting veterinary practice toward diagnostics-led dosing and more frequent rotation with alternate classes where immature efficacy tradeoffs are manageable. In Australia, structured producer programs recorded resistance across all monitored dairy farms in recent trials. However, the programs did not observe measurable production loss, a result that practitioners attribute to partial efficacy that still reduces acute disease risk relative to alternatives. Research in human fascioliasis indicated that host microbiome features were associated with treatment outcomes, showing that non-responders present distinct microbial signatures compared to responders, which complicates the attribution of all failures to parasite genetics alone. As per the data published by Farm Advisory Service in October 2024, resistance risk is elevated, veterinarians emphasize test-and-treat, coproantigen monitoring, and scheduled rotations that preserve efficacy for high-burden windows in the triclabendazole market. Sponsors fund resistance genotyping and coproantigen testing partnerships, but stewardship programs raise costs for smaller generic suppliers, tightening the economics for low-price entrants in competitive channels.

Other drivers and restraints analyzed in the detailed report include:

- Climate Change Extends Transmission Seasons and Expands Snail Habitats into Previously Marginal Zones

- Adoption of Fixed-Dose Combinations Enhances Compliance and Addresses Co-Infection Burdens

- Stringent Residue Withdrawal Periods Restrict Treatment Timing and Limit Dairy Market Penetration

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Veterinary livestock accounted for 78.77% of the triclabendazole market share in 2025 and is projected to grow at a 5.34% CAGR through 2031, reflecting both climate-amplified exposure and stewardship-driven repeat interventions on confirmed cases. Demand concentrates in temperate and subtropical belts where poorly drained pastures, floodplains, and irrigated forage favor intermediate host snails that sustain transmission windows. North American cattle operations in wet bottomlands and Gulf Coast pastures maintain repeated seasonal treatments, while British Isles and northwest European herds respond to wetter summers and milder winters by compressing safe grazing intervals and advancing autumn treatments. Livestock segment durability rests on three reinforcing shifts in the triclabendazole market. Climate trends stretch exposure windows, which raises the number of herds entering seasonal treatment plans. Coproantigen ELISA and molecular diagnostics enable targeted interventions that substitute precision for blanket dosing, which improves clinical outcomes and drug stewardship at the cost of lower per-farm volumes. Together, these factors underpin the higher-than-market growth of the veterinary livestock segment in the triclabendazole market through 2031.

Geography Analysis

North America accounted for 41.34% of the triclabendazole market share in 2025, reflecting advanced veterinary infrastructure, widespread diagnostic adoption, and regulated distribution that favors clinically integrated prescribing. The United States leads regional volumes due to persistent fluke burdens in wet bottomlands and Gulf Coast pastures, which keeps biannual coverage common in risk-prone locales. Surveillance-led protocols deepen market resilience, with diagnostic-based confirmation guiding timing and rotation to manage resistance concerns in the triclabendazole market. Canada's growth aligns with integrated dairy health programs and cross-border regulatory alignment that eases product flow. In Mexico, rural access and price-sensitive segments favor generics, yet variable veterinary access slows uptake relative to the United States and Canada.

Asia Pacific is projected to register the fastest pace at an 8.32% CAGR, underpinned by climate-driven expansion of snail habitats and intensifying ruminant systems across diverse agro-ecologies. On the Qinghai-Tibet Plateau, modeling under plateau climatic conditions indicates expanded geographical suitability for fluke transmission into higher altitudes, which is already prompting proactive surveillance and response plans in yak and sheep ranges.

The market in Europe is driven by growth factors, while stewardship frameworks are constraining prophylactic dosing in dairy regions. Southern Europe's warming winters and variable rainfall patterns bring new pockets into regular treatment schedules, while Eastern European producers accelerate generic uptake from Indian and Chinese suppliers.

- Elanco

- Alivira Animal Health (SeQuent)

- Bimeda

- Chanelle Pharma

- Hebei Veyong pharmaceutical Co., Ltd.

- MSD Animal Health

- Norbrook

- Novartis

- Virbac

- Zoetis

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 High veterinary fascioliasis burden; only flukicide effective across all life stages

- 4.2.2 WHO endorsement, donation-linked access, and FDA approval improve availability

- 4.2.3 Multi-stage efficacy sustains protocol-standard status in flukicide programs

- 4.2.4 Climate change expanding fascioliasis risk zones and seasonality

- 4.2.5 Adoption of triclabendazole fixed-dose combinations (macrocyclic lactones, levamisole)

- 4.2.6 Better diagnostics (coproantigen ELISA/molecular assays) enabling targeted treatment & surveillance

- 4.3 Market Restraints

- 4.3.1 Growing triclabendazole resistance in Fasciola spp.

- 4.3.2 Milk/meat residue withdrawal and lactation restrictions constrain dairy usage

- 4.3.3 Stewardship/rotation protocols reduce prophylactic dosing frequency

- 4.3.4 Human market monetization constrained by donation-based supply

- 4.4 Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Application

- 5.1.1 Veterinary Livestock

- 5.1.1.1 Cattle

- 5.1.1.2 Sheep

- 5.1.1.3 Goats

- 5.1.2 Human Health

- 5.1.1 Veterinary Livestock

- 5.2 By Product Type

- 5.2.1 Brand

- 5.2.2 Generic

- 5.3 By Distribution Channel

- 5.3.1 Veterinary Hospitals

- 5.3.2 Veterinary Clinics

- 5.3.3 Pharmacies / Drug Stores

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, Recent Developments)

- 6.3.1 Elanco Animal Health

- 6.3.2 Alivira Animal Health (SeQuent)

- 6.3.3 Bimeda

- 6.3.4 Chanelle Pharma

- 6.3.5 Hebei Veyong pharmaceutical Co., Ltd.

- 6.3.6 MSD Animal Health

- 6.3.7 Norbrook

- 6.3.8 Novartis AG

- 6.3.9 Virbac

- 6.3.10 Zoetis

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment