|

시장보고서

상품코드

2063722

대형 폐기물 수거 서비스 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Bulky Waste Collection Service - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

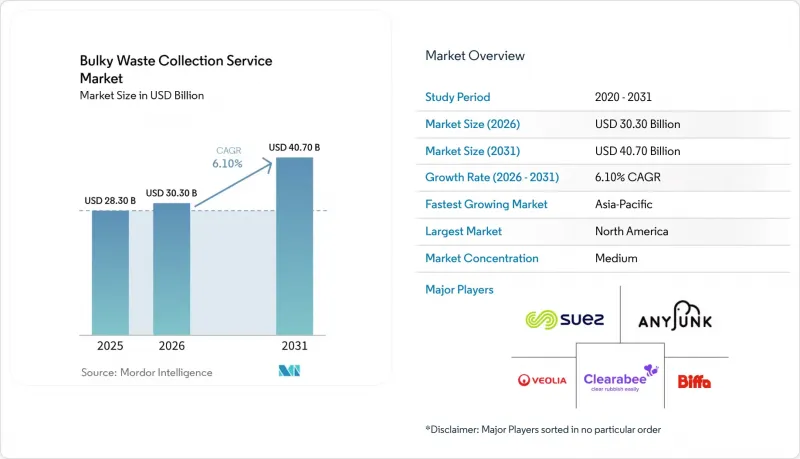

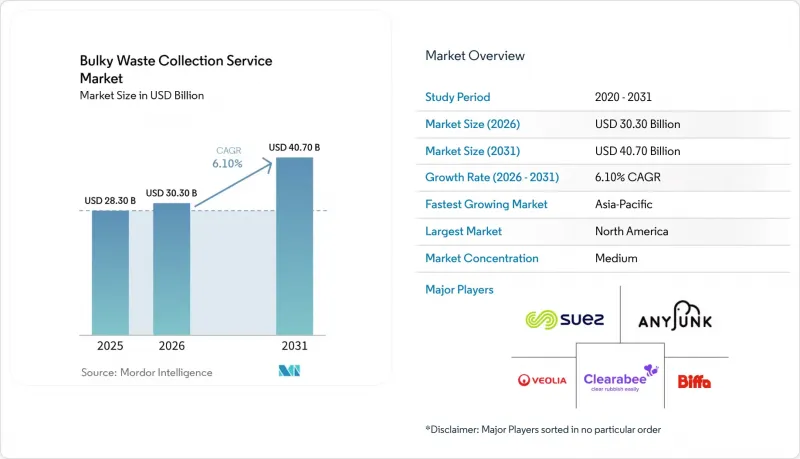

Mordor Intelligence에 의하면, 대형 폐기물 수거 서비스 시장 규모는 2025년 283억 달러로 평가되었습니다. 2026년에는 303억 달러로 확대되어 2026-2031년 CAGR은 6.10%를 나타내, 2031년에는 407억 달러에 이를 것으로 예측됩니다.

본 보고서는 폐기물 유형(가구·실내 장식용품, 금속·고철 등), 발생원(주택, 상업시설 등), 수거 모델(문 앞 수거, 주문형 수거 등) 및 지역(북미, 유럽, 아시아·태평양, 남미, 중동 및 아프리카)별로 분류되어 있습니다. 시장 전망은 금액(10억 달러) 및 수량(톤) 단위로 제시되어 있습니다.

세계의 대형 폐기물 수거 서비스 시장 동향 및 인사이트

도시화의 진전과 일반 폐기물 발생량 증가

급속한 도시 집중으로 인해 가구, 가전제품, 리모델링 공사 잔해 등 대형 폐기물의 발생량이 계속 증가하고 있습니다. 전 세계 폐기물 발생량은 2023년 21억 톤에서 2050년까지 38억 톤으로 증가할 것으로 예상되며, 이미 수송 능력이나 대형 물품에 대한 전문적인 처리 능력이 부족한 도시 시스템에 가해지는 압박이 더욱 커지고 있습니다. 저소득 지역에서는 수거되지 않거나 부적절하게 관리된 폐기물이 공식적인 수거 체계를 구축하는 데 지속적인 구조적 장벽으로 작용하고 있으며, 재정 능력, 기부자 프로그램, 인프라 자금 조달을 통해 서비스 격차가 점차 해소됨에 따라 잠재적 수요가 지속적으로 발생하고 있습니다. 잉글랜드 지방 자치단체의 데이터에 따르면, 2024년부터 2025년에 걸쳐 2,520만 톤의 폐기물이 수거되었으며, 이는 컨테이너에 담을 수 없는 대형 폐기물에 대한 전용 처리 솔루션의 중요성을 뒷받침하는 안정적인 처리량을 보여줍니다. 도시화가 진행됨에 따라 대형 폐기물 수거 서비스 시장은 다세대 주택의 예측 가능한 교체 주기 및 개보수 공사의 혜택을 받고 있으며, 이로 인해 수요가 도심 지역에 집중되고 있습니다. 또한, 안전하고 편리한 수거 서비스에 대한 일반 시민들의 기대가 높아지면서 이 시장을 뒷받침하고 있으며, 이용자들을 정식 업체로 유도하고 있습니다.

폐기물 관리에 관한 정부의 엄격한 규제

주요 관할 구역에서 정책이 강화됨에 따라 추적 가능성과 자원화 의무가 강화되고 있으며, 이로 인해 인증된 수거·선별 능력의 도입이 촉진되고 있습니다. 유럽연합(EU)에서는 개정된 폐기물 기본지침이 2025년 10월 16일에 발효됨에 따라, 회원국들에게 30개월 이내에 섬유 제품 및 신발에 관한 확대 생산자 책임(EPR) 제도를 수립할 것을 의무화하고 있습니다. 이를 통해 처리하기 어려운 대형 폐기물의 공식 수거를 확대하기 위한 새로운 자금 조달 및 운영 절차가 도입됩니다. 잉글랜드에서는 폐기물 관련 범죄 단속에 투입되는 자금을 확충하고, 드론 감시 및 자동 번호판 인식 등의 도구를 확대하여, 법규 준수 서비스 요금을 인하해 경쟁하는 불법 업체들을 견제하고 있습니다. 분리 수거, 친환경 요금, 수출용 선적 전 선별에 대한 규제가 강화됨에 따라, 시스템은 검증 가능한 회수율로 전환되고 있으며, 감사에 대응할 수 있는 디지털 기록과 견고한 품질 관리 체계를 갖춘 사업자가 유리한 입장에 서게 되었습니다. 인도에서는 건설 및 철거 폐기물에 관한 요건의 개정이 법제화되었습니다. 전국적인 폐기물 추적 시스템의 도입이 진행되고 있으며, 이는 자발적인 노력에서 의무적인 이행으로의 전환을 시사하는 것으로, 전문적인 대형 폐기물 수거 및 기록이 남는 처리 서비스에 대한 수요를 확대시키고 있습니다. 대형 폐기물 수거 서비스 시장은 규제 대상 폐기물 흐름에 대한 처리 능력을 구축하고, 규정 준수를 중시하는 입찰 및 파트너십을 통해 이에 대응하고 있습니다.

불법 투기의 만연과 비공식 부문과의 경쟁

불법 투기는 여전히 정식 업체로부터 자재를 빼앗고 있으며, 지방자치단체에 청소 비용을 부담시키고 있습니다. 잉글랜드에서는 2024년부터 2025년에 걸쳐 126만 건의 불법 투기 사례가 기록되었으며, 그중 상당수가 간선 도로에서 발생했습니다. 또한, 대규모 폐기물 철거에 공공 부문이 지출하는 비용이 산정되고 있으며, 이는 규정 준수를 바탕으로 한 서비스 모델의 경제성을 직접적으로 저해하는 요인입니다. 집행 기관은 불법 수출을 저지하고 다수의 무허가 시설을 적발해 왔지만, 조사 능력에 비해 사건 건수는 여전히 많아, 암시장 활동을 조장하는 뿌리 깊은 격차가 존재함을 보여주고 있습니다. 폐기물 범죄는 거시경제적인 걸림돌이 되고 있으며, 영국에서는 연간 수억 파운드의 비용이 발생하는 것으로 추정됩니다. 이는 규정 준수를 바탕으로 한 네트워크 투자를 저해하며, 저렴한 불법 대안이 계속 존재하는 지역에서는 정식 회수율을 떨어뜨리고 있습니다. 법 집행이 미흡할 경우, 가정이나 중소기업은 정식 경로와 비정식 경로 중 어느 쪽을 선택할지 결정할 때 편의성과 인식되는 위험을 저울질하게 되므로, 대형 폐기물 수거 서비스 시장은 고객 확보 비용 증가에 직면하게 됩니다. 디지털 폐기물 추적 및 표적화된 법 집행이 확대됨에 따라 유출 위험은 줄어들 가능성이 있지만, 단기적인 변동성은 여전히 계획 수립과 활용을 복잡하게 만들고 있습니다. 따라서 위험에 노출된 지역의 사업자들은 지자체와 긴밀히 협력하는 전략을 수립해야 하며, 홍보, 요금 체계, 서비스 제공 기간을 해당 지역의 법 집행 속도에 맞추어야 합니다.

부문별 분석

2025년, 대형 폐기물 수거 시장 점유율의 49.21%를 가정별 수거 서비스가 차지했습니다. 이는 수년에 걸친 지자체와의 계약을 통해 예측 가능한 정기 노선이 유지되었기 때문입니다. 한편, 온디맨드 방식은 앱을 통한 예약, IoT를 활용한 경로 최적화, 그리고 전기화 차량 군을 통해 한계 수거 비용이 감소하고 서비스 제공 시간대가 개선됨에 따라, 2031년까지 연평균 성장률(CAGR) 6.71%로 더욱 빠르게 성장할 것으로 예측됩니다. 리퍼블릭 서비스가 2025년과 2026년에 실시한 전기 수거 차량, 재생 천연가스 프로젝트 및 폴리머 처리 분야에 대한 투자는 다운스트림 공정과의 통합이 수거 업무의 변동성을 어떻게 상쇄하고 지자체 입찰에서의 서비스 제안을 강화할 수 있는지를 보여줍니다. 수에즈의 ‘WasteConnect’ 및 ‘AutoDiag’ 도입 사례는 커넥티드 컨테이너, 실시간 품질 모니터링, 흐름 분석이 어떻게 노선 밀도를 높이고 이물질을 줄일 수 있는지를 보여주고 있으며, 이는 유연한 업무 수행에 있어 매우 중요합니다. 이러한 부피가 큰 폐기물의 수거 방식은 그 구성에 따라 크게 다릅니다. 따라서 대형 폐기물 수거 서비스 시장은 기본 노선의 효율성과 당일 또는 익일 대응이 가능한 유연한 처리 능력을 결합한 하이브리드형 운영 방식으로 수렴되고 있습니다.

공공 수거 센터의 방침 또한 이러한 하이브리드화를 뒷받침하고 있습니다. 엑스-마르세유-프로방스 지역에서는 2025년에 공공 수거 센터의 이용 규정과 일일 수거 한도를 재검토하여 서비스의 표준화와 평가 향상을 도모했습니다. 이를 통해 자원화 목표 달성을 촉진하는 동시에, 계절적 피크 시기에 가구별 수거 시스템에 가해지는 부담을 줄이고 있습니다. 독일에서는 오버하펠이 주민들을 대상으로 실시하고 있는 무료 대형 폐기물 반입 접수와 같은 프로젝트가, 기존의 가정별 수거 방식을 보완하고 무허가 경로를 통한 폐기물 투기를 억제하는 데 기여하고 있습니다. 또한, 신원 확인 및 거주 증명 확인을 통해, 과거에는 업체들의 불법 투기를 방치했던 허점이 메워졌습니다. 수거별 수량 상한선 및 분리 배출 규칙 등 지역 서비스의 업데이트를 통해 현장 운영과 처리 수요 간의 조화가 이루어지고 있으며, 중계 시설의 처리 능력이 지속적으로 향상되고 있습니다. 예약 시스템과 공공 센터의 규정이 적절히 홍보되면, 수거 누락이 줄어들고 고객 경험이 향상되며 반입되는 폐기물의 품질이 안정화되어 대형 폐기물 수거 서비스 시장에 이점을 가져다줍니다. 규제가 허용하는 범위 내에서 예약 슬롯이나 비성수기 인센티브와 연계된 가격 신호를 도입함으로써 수요를 더욱 평준화할 수 있으며, 그 결과 노선의 생산성과 자산 활용 효율이 향상됩니다.

지역별 분석

2025년, 북미는 대형 폐기물 수거 서비스 시장 점유율의 35.70%를 차지하며 시장을 주도했습니다. 이는 가구의 꾸준한 교체와, 일부 주에서 매트리스 및 가구 수거를 지원하는 ‘확대 생산자 책임(EPR)’ 제도의 정착에 힘입은 결과입니다. 2025년과 2026년에 보고된 재생 가능 천연가스, 폴리머 및 전기화에 대한 기업 투자는 정기 및 주문형 대형 폐기물 수거를 보완하는 가치 회수에 대한 지속적인 중점을 보여주고 있습니다. 지자체들이 품질 기준을 강화하고, 가구별 수거 프로그램에 디지털 보고 시스템을 도입하는 가운데, 다운스트림 공정의 자산을 통합한 사업자는 규정 준수 및 경제성 측면에서 차별화를 꾀할 수 있습니다. 캐나다와 멕시코의 대형 폐기물 수거 서비스 시장 역시 제도화 추세를 보이고 있지만, 집행 역량의 불균형으로 인해 비공식적인 활동이 여전히 걸림돌이 되고 있습니다. 이 지역, 특히 계절에 따라 대형 폐기물 발생량이 정점에 달하는 대도시권에서는 수거 노선 밀도와 인력 확보가 다년 계약을 따내기 위한 결정적인 요인으로 계속해서 작용하고 있습니다.

유럽 내 정책 조화는 수집의 경제성과 이행 체제를 재구축하고 있습니다. 2025년 10월, EU의 개정된 ‘폐기물 기본 지침’이 발효됨에 따라, 섬유 제품 및 신발에 대한 확대 생산자 책임(EPR)이 의무화되었습니다. 이 지침에서는 유해 물질의 분리 수거도 강조되었으며, 음식물 쓰레기 감축 목표도 설정되었습니다. 이러한 변경으로 인해 공공 프로그램에서 관리되는 자재의 범위가 확대됨에 따라, 추적 가능한 경로 관리 및 선별에 대한 수요가 증가하고 있습니다. 프랑스의 공공 수거 거점 네트워크는 시민과 수거 업체가 대형 폐기물을 정식 경로를 통해 배출하도록 유도하는 체계가 잘 정립된 모델로, 매립 규제와 프로그램 설계가 이용자의 행동에 미치는 영향을 반영하고 있습니다. 잉글랜드 지방 자치단체가 수집한 폐기물 수거 및 불법 투기 관련 데이터는 법규를 준수하는 사업자를 보호하고 자원화 목표 달성을 위한 진전을 유지하기 위해 법 집행이 얼마나 중요한지를 여실히 보여주고 있습니다. 국경을 넘는 폐기물 운송 규정에 따른 디지털 추적 기술의 발전과, 회원국들의 섬유 제품에 대한 확대 생산자 책임(EPR) 제도의 시행에 따라, 사업자들은 강력한 시스템 통합 능력을 갖춘 기업에 유리한 새로운 물류 요건을 마주하고 있습니다. 따라서 유럽의 대형 폐기물 수거 서비스 시장에서는 분리수거 및 수거 시설에서의 원활한 인계와 확실한 처리 능력을 확보하기 위해, 노선 계획과 공공 센터의 출입 통제, 예약 시스템을 연계하고 있습니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR) 6.52%를 기록하며 가장 빠르게 성장하는 지역이 될 것으로 전망됩니다. 인도의 전국적인 디지털 폐기물 추적 프로그램과 건설·철거 폐기물 관련 규정의 최근 개정은 공식적인 수거 및 추적 체계로의 전환을 나타내며, 더 많은 대형 폐기물이 규제된 경로로 임베디드되고 있습니다. 이 지역의 주요 도시들이 대형 폐기물의 가정별 수거 및 예약제 모델을 확대하는 가운데, 정책 입안자들은 품질과 안전 기준을 최우선으로 하고 있으며, 이를 위해서는 더 높은 수준의 훈련을 받은 작업 인력과 현대화된 차량의 배치가 필요합니다. 동남아시아와 아프리카의 일부 지역에서는 특히 대형 폐기물의 경우, 비공식 경로를 통한 유출을 줄이고 서비스 보급률을 높이기 위해서는 법 집행 강화와 시민 대상의 인식 제고가 필수적입니다. 사하라 이남 아프리카의 학술 연구에 따르면, 가정 내 분리수거 규정 준수는 명확한 홍보와 일관된 집행에 달려 있으며, 이 두 가지 모두 대형 폐기물을 정식 수거 경로로 유도하는 데 직접적인 영향을 미칩니다는 점이 강조되고 있습니다. 정부가 통합 시스템을 도입하고 감독을 강화함에 따라, 대형 폐기물 수거 서비스 시장은 정식 참여 업체의 확대와 보다 안정적인 처리 흐름의 혜택을 누리게 될 것입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측(금액 : 달러, 수량 : 톤)

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.24According to Mordor Intelligence, the bulky waste collection service market size is expected to grow from USD 28.30 billion in 2025 to USD 30.30 billion in 2026 and is forecast to reach USD 40.70 billion by 2031 at 6.10% CAGR over 2026-2031.

This report is Segmented by Waste Type (Furniture & Upholstery, Metal & Scrap Items, and More), by Source (Residential, Commercial, and More), by Collection Model (Curbside, On-Demand, and More), and by Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD Billion) and Volume (Tons).

Global Bulky Waste Collection Service Market Trends and Insights

Rising Urbanization and Municipal Solid Waste Generation

Rapid urban concentration continues to elevate bulky streams such as furniture, appliances, and renovation debris. Global waste volumes are projected to increase from 2.1 billion tonnes in 2023 to 3.8 billion tonnes by 2050, intensifying pressure on city systems that are already short of transfer capacity and specialized handling for oversized items. In lower-income settings, uncollected and mismanaged waste remains a structural barrier to formal capture, creating a long pipeline of latent demand as fiscal capacity, donor programs, and infrastructure financing close service gaps over time. Local authority data in England showed 25.2 million tonnes of waste collected in 2024-2025, indicating steady volumes that underscore the importance of dedicated solutions for oversized fractions that cannot be containerized. As urbanization advances, the bulky waste collection service market benefits from predictable replacement cycles and renovation activity in multi-family housing, which concentrates demand into municipal cores. The bulky waste collection service market also benefits from rising public expectations for safe, convenient removal, which steers users toward formal providers

Stringent Government Regulations on Waste Management

Policy tightening across leading jurisdictions is increasing traceability and diversion obligations, which drives the adoption of certified collection and sorting capabilities. In the European Union, the revised Waste Framework Directive entered into force on October 16, 2025, and requires Member States to establish Extended Producer Responsibility for textiles and footwear within 30 months, introducing new funding and operational flows to expand formal collection of the difficult, bulky fraction. England has increased funding for waste crime enforcement and is scaling tools such as drone surveillance and automatic number plate recognition to deter illegal operators that undercut compliant service. Regulatory emphasis on separate collection, eco-modulated fees, and pre-shipment sorting for exports is moving the system toward verifiable recovery rates, favoring operators with audit-ready digital records and robust quality control. India has codified updated construction and demolition requirements. It is rolling out national waste tracking, signaling a transition from voluntary practices to mandatory performance that expands demand for specialized bulky pick-ups and documented processing. The bulky waste collection service market is responding through compliance-led bids and partnerships that build capacity for regulated streams.

Prevalence of Illegal Dumping and Informal Sector Competition

Illegal disposal continues to divert material away from formal providers and imposes cleanup costs on local authorities. England recorded 1.26 million fly-tipping incidents in 2024-2025, with a significant share occurring on highways, and a measured public-sector spend to clear larger loads, which directly erodes the economics of compliant service models. Enforcement agencies have disrupted illegal exports and identified numerous unlicensed sites, but case volumes remain high relative to investigative capacity, indicating a persistent gap that sustains shadow activity. Waste crime is also a macroeconomic drag, with estimated multi-hundred-million-pound annual costs in the United Kingdom, which undermine investment in compliant networks and lower formal capture rates where cheap, illegal options persist. The bulky waste collection service market faces higher customer acquisition costs when enforcement is inconsistent, as households and small businesses weigh convenience and perceived risk when choosing between formal and informal channels. As digital waste tracking and targeted enforcement scale, leakage risks can recede, but near-term variability still complicates planning and utilization. Operator strategies in exposed geographies, therefore, depend on close coordination with municipalities to align communications, fee structures, and service windows with local enforcement rhythms.

Other drivers and restraints analyzed in the detailed report include:

- Smart City Initiatives and Digital Infrastructure Development

- Increase in Construction and Demolition Activities

- Shortage of Trained Workforce and Specialized Equipment

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Curbside service accounted for 49.21% of the bulky waste collection market share in 2025, as long-standing municipal agreements maintained predictable, scheduled routes. On-demand formats are projected to grow faster, at a 6.71% CAGR through 2031, as app-based scheduling, IoT-enabled route optimization, and electrified fleets lower marginal pickup costs and improve service windows. Republic Services' 2025 and 2026 investments in electric collection vehicles, renewable natural gas projects, and polymer processing demonstrate how downstream integration can offset collection volatility and enhance service proposals in municipal tenders. SUEZ's WasteConnect and AutoDiag deployments demonstrate how connected containers, live quality monitoring, and flow analytics can increase route density and reduce contamination, which is critical for ad hoc operations. These bulky pickups vary widely in composition. The bulky waste collection service market is thus converging on hybrid operations that blend base-route efficiency with flexible capacity for same-day or next-day requests.

Public center policies reinforce this hybridization. The Aix-Marseille-Provence area revised access rules and daily limits for public drop-off centers in 2025 to standardize services and enhance valuation, thereby advancing diversion goals and reducing strain on curbside systems during seasonal peaks. In Germany, projects like Oberhavel's free bulky waste delivery window for residents complement traditional curbside pickups and help divert volumes from unauthorized channels, while identity checks and residency proof close loopholes that previously allowed professional dumping. Local service updates, including per-collection volume caps and separate placement rules, continue to align field operations with processing needs and improve throughput at transfer sites. The bulky waste collection service market benefits when appointment systems and public center rules are well communicated, as they reduce missed collections, enhance the customer experience, and stabilize inbound quality. Price signals tied to appointment slots and off-peak incentives can further smooth demand, where regulations allow, thereby improving route productivity and asset utilization.

Geography Analysis

North America led with 35.70% of the bulky waste collection service market share in 2025, supported by steady furniture turnover and maturing Extended Producer Responsibility measures that subsidized mattress and furniture collection in several states. Reported company investments into renewable natural gas, polymers, and electrification in 2025 and 2026 indicate continued emphasis on value recovery that complements scheduled and on-demand bulky pickups. As municipalities tighten quality expectations and add digital reporting to curbside programs, operators with integrated downstream assets can differentiate on both compliance and economics. The bulky waste collection service market in Canada and Mexico is also navigating formalization trends, though informal activity remains a headwind due to uneven enforcement capacity. In this region, route density and workforce availability remain the decisive factors in securing multi-year contracts, particularly in large metropolitan areas with seasonal, bulky peaks.

Europe's policy harmonization is reshaping collection economics and execution. In October 2025, the EU's updated Waste Framework Directive came into effect, mandating Extended Producer Responsibility for textiles and footwear. The directive also emphasized the separate collection of hazardous materials and set targets for reducing food waste. These changes broadened the scope of materials managed under official programs, heightening the demand for traceable routing and sorting. France's public drop-off network serves as a mature template for how citizens and contractors route bulky items into formal channels, reflecting the impact of landfill restrictions and program design on user behavior. England's data on local authority-collected waste and fly-tipping underscores the importance of enforcement to protect compliant operators and maintain progress toward diversion goals. As digital tracking advances in cross-border waste shipment rules and Member States operationalize textile EPR schemes, operators see new logistics requirements that favor those with strong systems integration. The bulky waste collection service market in Europe is, therefore, aligning route planning with public center access controls and appointment systems to ensure smooth handoffs and reliable throughput at sorting and recovery sites.

Asia-Pacific is projected to be the fastest-growing region at a 6.52% CAGR through 2031. India's national digital waste-tracking program and recent updates to construction and demolition rules signal a shift toward formalized recovery and traceability, bringing more bulky loads into regulated channels. As major cities in the region scale curbside and appointment models for oversized items, policymakers are prioritizing quality and safety standards, which require better-trained crews and modernized fleets. In Southeast Asia and parts of Africa, improving enforcement and public education will be a prerequisite for reducing leakage into informal channels and increasing service penetration, especially for bulky waste. Academic work in Sub-Saharan Africa highlights that regulatory compliance with household segregation depends on clear communication and consistent enforcement, both of which directly affect routing bulky fractions toward formal collection. As governments roll out integrated systems and step up oversight, the bulky waste collection service market will benefit from broader formal participation and more stable processing flows.

- Waste Management, Inc.

- Republic Services, Inc.

- Veolia Environnement S.A.

- SUEZ S.A.

- Biffa plc

- Clean Harbors, Inc.

- Stericycle, Inc.

- Remondis SE & Co. KG

- Casella Waste Systems, Inc.

- GFL Environmental Inc.

- Waste Connections, Inc.

- Rumpke Waste & Recycling

- Recology Inc

- ALBA Group

- Van Gansewinkel

- PreZero

- Junk King

- LoadUp Technologies

- Renewi plc

- EnviroServ Holdings

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Urbanization and Municipal Solid Waste Generation

- 4.2.2 Stringent Government Regulations on Waste Management

- 4.2.3 Growing Environmental Consciousness Among Consumers

- 4.2.4 Increase in Construction and Demolition Activities

- 4.2.5 Smart City Initiatives and Digital Infrastructure Development

- 4.2.6 Expansion of E-Commerce and Furniture Replacement Trends

- 4.3 Market Restraints

- 4.3.1 Lack of Standardized Waste Segregation Practices

- 4.3.2 Limited Awareness in Rural and Developing Regions

- 4.3.3 Shortage of Trained Workforce and Specialized Equipment

- 4.3.4 Prevalence of Illegal Dumping and Informal Sector Competition

- 4.4 Value / Supply-Chain Analysis

- 4.4.1 Collection scheduling systems

- 4.4.2 Route optimization methods

- 4.4.3 Dispatch and logistics framework

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

- 4.8 Impact of GenAI-Powered Waste Collection on Service Providers' Revenue Growth

5 Market Size & Growth Forecasts (Value in USD & Volume in Tons)

- 5.1 By Collection Model

- 5.1.1 Curbside

- 5.1.2 On-Demand

- 5.1.3 Hybrid

- 5.1.4 Contracted B2B

- 5.1.5 Others

- 5.2 By Source

- 5.2.1 Residential

- 5.2.2 Commercial

- 5.2.3 Industrial

- 5.2.4 Municipal/Government

- 5.2.5 Others (Religious Institutions, Temporary Disaster Relief Camps, Film/TV Production Sets)

- 5.3 By Waste Type

- 5.3.1 Furniture & Upholstery

- 5.3.2 Metal & Scrap Items

- 5.3.3 White Goods/Appliances

- 5.3.4 Construction & Demolition

- 5.3.5 Others (Event-specific Waste, Biomedical/Institutional)

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 United Kingdom

- 5.4.2.2 Germany

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Russia

- 5.4.2.7 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines)

- 5.4.3.7 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 Turkey

- 5.4.5.4 South Africa

- 5.4.5.5 Nigeria

- 5.4.5.6 Rest of Middle East and Africa

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Partnership Model Benchmarking

- 6.3 Strategic Moves

- 6.4 Market Share Analysis

- 6.5 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)}

- 6.5.1 Waste Management, Inc.

- 6.5.2 Republic Services, Inc.

- 6.5.3 Veolia Environnement S.A.

- 6.5.4 SUEZ S.A.

- 6.5.5 Biffa plc

- 6.5.6 Clean Harbors, Inc.

- 6.5.7 Stericycle, Inc.

- 6.5.8 Remondis SE & Co. KG

- 6.5.9 Casella Waste Systems, Inc.

- 6.5.10 GFL Environmental Inc.

- 6.5.11 Waste Connections, Inc.

- 6.5.12 Rumpke Waste & Recycling

- 6.5.13 Recology Inc

- 6.5.14 ALBA Group

- 6.5.15 Van Gansewinkel

- 6.5.16 PreZero

- 6.5.17 Junk King

- 6.5.18 LoadUp Technologies

- 6.5.19 Renewi plc

- 6.5.20 EnviroServ Holdings

7 Market Opportunities & Future Outlook

- 7.1 Smart Cities & IoT Integration

- 7.2 Producer Responsibility Expansion

- 7.3 Key Investment Strategies