|

시장보고서

상품코드

2063725

유럽의 대형 폐기물 수거 서비스 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Europe Bulky Waste Collection Service - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

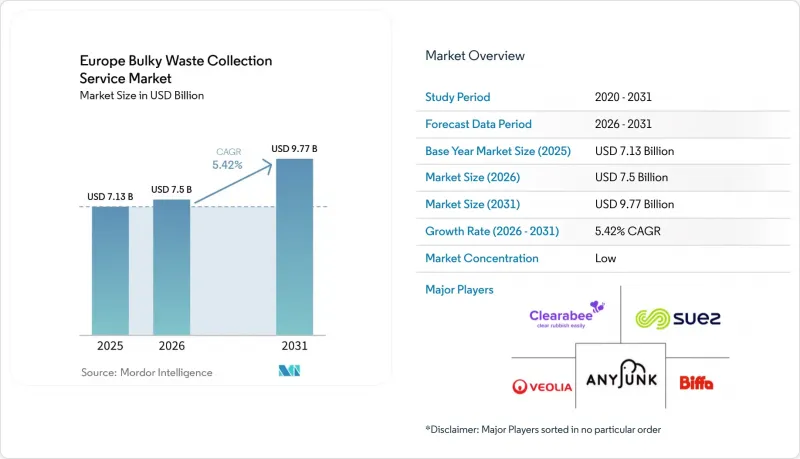

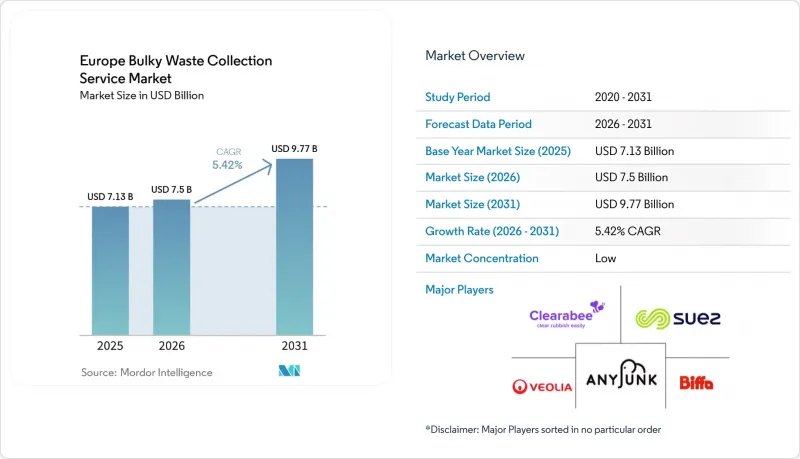

Mordor Intelligence에 의하면, 유럽 대형 폐기물 수거 서비스 시장 규모는 2025년 71억 3,000만 달러, 2026년 75억 달러에서 2031년까지 97억 7,000만 달러로 확대되어 2026년부터 2031년까지 CAGR 5.42%를 나타낼 것으로 예측됩니다.

본 보고서는 수거 모델(가정별 수거, 주문형 수거, 기타), 발생원(주거, 상업, 기타), 폐기물 유형(가구·실내 장식물, 금속·고철, 기타) 및 지역(영국, 독일, 프랑스, 이탈리아, 스페인, 러시아, 기타 유럽)별로 분류되어 있습니다. 시장 전망은 금액(달러) 및 수량(톤) 단위로 제시되어 있습니다.

유럽 대형 폐기물 수거 서비스 시장 동향 및 인사이트

주택 및 상업 부문에서의 개보수 및 리모델링 활동 증가

유럽의 대형 폐기물 수거 서비스 시장은 주거 및 상업시설에서의 리모델링 및 개조 활동 증가에 힘입어 눈에 띄게 성장하고 있습니다. 코로나19 팬데믹 이후 주택 개보수 지출이 급증하고 있으며, 프랑스, 독일, 스페인, 이탈리아 등에서는 재택근무의 확산과 에너지 효율 개선 수요를 배경으로 개보수 허가 건수가 연간 15-20%의 성장률을 보이고 있습니다. 주택 리모델링 시에는 낡은 설비, 바닥재, 가전제품, 가구 등을 포함해 한 건당 2-5톤의 대형 폐기물이 발생하므로, 전문적인 처리 서비스가 필요합니다. ‘건축물의 에너지 성능에 관한 지침(EPBD)’ 등 EU의 에너지 효율화 이니셔티브와 독일, 프랑스, 네덜란드의 보조금 프로그램에 힘입어 리노베이션 비율이 더욱 높아지고 있으며, 그 결과 대형 폐기물의 양이 증가하고 있습니다. 하이브리드 근무 모델과 사무실, 소매점, 호텔, 레스토랑의 재설계를 배경으로 한 상업시설의 개보수 공사 역시 칸막이 벽, 비품, 구형 설비 등을 포함해 이러한 폐기물 발생량을 더욱 가중시키고 있습니다. 유럽 건물의 35%는 1970년 이전에 지어진 것이며, 노후화된 건물에는 지속적인 유지보수가 필요하기 때문에 폐기물 수거 서비스에 대한 수요가 유지되고 있습니다. 지자체와 민간 사업자들은 규제적 압력, 인구 동향, 그리고 유럽 건축 환경의 수명 주기에 힘입어 주문형 수거 및 분리 수거 시설 등의 서비스를 확대하며, 혼합 대형 폐기물 관리에 힘쓰고 있습니다.

유럽연합(EU)의 엄격한 폐기물 관리 규정과 순환형 경제 정책

유럽연합(EU)은 생산자부터 수거업체에 이르기까지 공급망 전반의 역할을 재구성하는 규정을 포함시켜, 최근 몇 년간 가장 종합적인 폐기물 개혁을 시행하고 있습니다. 개정된 폐기물 기본 지침은 2025년 10월에 발효되며, 정해진 일정에 따른 섬유 제품에 대한 확대된 생산자 책임 및 식품 폐기물 감축 목표 등의 요건을 포함하고 있어, 궁극적으로 분리수거 및 수거 실무에 영향을 미치는 업스트림 단계에서의 압력을 야기하고 있습니다. 디지털 폐기물 운송 시스템에 따르면, 2026년 5월부터 유럽연합(EU) 내 폐기물 이동에 대해 거의 실시간으로 추적하는 것이 의무화되며, 이를 통해 집행 체제가 강화될 뿐만 아니라, 재활용 의무를 회피하기 위해 이루어지던 잘못된 분류를 가능하게 했던 기존의 허점이 메워지게 됩니다. 포장 개혁은 재활용 적합성 평가 및 분야별 의무화를 향해 지속적으로 진전되고 있으며, 이에 따라 소재 재설계와 다운스트림 공정에서의 분리 수거가 가속화될 것입니다. 이러한 변경 사항은 대형 폐기물 처리 과정 전반에 걸쳐 데이터의 일관성, 인증 및 선별 품질을 관리할 수 있는 사업자를 평가하기 위한 것입니다. 또한, 규정 준수 기준을 강화함으로써 유럽의 대형 폐기물 수거 서비스 시장에서 입찰, 가격 책정 및 기술 도입에 영향을 미치게 될 것입니다.

불법 투기와 규정 위반 문제

폐기물 관련 범죄나 규정 위반은 정식 사업자의 가격 경쟁력을 약화시키고, 환경 목표 달성을 저해합니다. 잉글랜드에서는 당국이 폐기물 관련 범죄로 인한 막대한 경제적 손실을 밝히고, 디지털 폐기물 추적 시스템에 대한 자금 지원 및 불법 행위 억제를 위한 집행 수단 확충을 포함하는 다년 계획을 도입했습니다. 이 계획에는 데이터, 감시, 허가 및 감독에 대한 개선 방안이 포함되어 있으며, 데이터 기반의 억제 및 조기 개입을 지향하는 집행 방침의 전환을 시사하고 있습니다. 세계적 차원에서 다자간 기구들은 폐기물 밀수 문제의 규모와 복잡성을 지적하고 있으며, 이로 인해 공급망 내 책임 소재가 불분명해지고 합법적인 수거 업체에 추가적인 규정 준수 비용이 부과되고 있습니다. 이러한 경향은 법 집행이 미흡한 지역에서 단기적인 가격 압박을 초래하고 있습니다. 장기적으로는 디지털 추적 요건과 협력적인 국경 간 조치로 인해 기본적인 규정 준수 수준이 향상되어, 유럽의 대형 폐기물 수거 서비스 시장에서 규정을 준수하는 사업자들에게 이익이 될 것으로 보입니다.

부문별 분석

2025년에는 가구별 수거가 46.72%의 점유율을 차지했으나, 인구 밀집 도시에서 편의성에 대한 기대가 높아지는 가운데, 온디맨드 서비스는 2031년까지 연평균 성장률(CAGR) 5.82%로 확대될 것으로 예측됩니다. 이러한 격차는 서비스 설계에 있어 광범위한 변화를 반영하고 있으며, 대도시권에서는 앱을 통한 예약과 신속한 대응이 더 이상 선택 사항이 아닙니다. 고정 노선과 비상 대기 대응 능력을 결합한 하이브리드 모델은 노선 밀도를 유지하면서도 수요가 급증할 때에도 유연하게 대응할 수 있어 지지를 얻고 있습니다. GPS 추적 및 동적 스케줄링을 포함한 디지털 기능은 유럽의 대형 폐기물 수거 서비스 시장에서 진행되는 대규모 지자체 입찰에서 기본 요건으로 자리 잡고 있습니다. 데이터 수거 및 서비스 제공 증명을 표준화한 사업자는 청구 정확성, 감사 대응 능력 및 고객 만족도를 향상시킬 수 있습니다.

도로변 수거의 견고성은 확립된 노선망에서 비롯된 네트워크 효과에 기인하며, 최적화된 노선을 통해 규모 확대에 따른 단위 비용 절감이 실현됩니다. 입찰 사양서에는 지속가능성 및 보고와 관련된 조항이 점점 더 많이 포함되고 있으며, 최근 공공 계약에서는 지역의 기후 목표를 달성하기 위해 전기차, 적정 크기의 차량 및 첨단 차량 시스템으로의 전환이 진행되고 있는 것으로 나타났습니다. 앱 기반 플랫폼은 세심한 서비스와 투명한 가격 책정을 통해 경쟁하고 있으며, 인구 밀도가 높은 지역에서 가장 지속적인 성과를 거두고 있습니다. 지자체 운영의 반입 네트워크나 접근이 통제된 시설은 폐기물 발생이 가장 많은 시기의 부담을 줄여줌으로써, 도로변 수거를 보완할 수 있습니다. 규정 준수 및 성과 보고가 통합됨에 따라, 유럽의 대형 폐기물 수거 서비스 시장에서 수거 모델을 선택할 때는 비용, 대응 능력, 데이터의 완전성 사이에서 균형을 맞추어야할 것입니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측 및

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.23According to Mordor Intelligence, the europe bulky waste collection service market size is projected to expand from USD 7.13 billion in 2025 and USD 7.5 billion in 2026 to USD 9.77 billion by 2031, registering a CAGR of 5.42% between 2026 to 2031.

This report is Segmented by Collection Model (Curbside, On-Demand, and More), Source (Residential, Commercial, and More), by Waste Type (Furniture & Upholstery, Metal & Scrap Items, and More), and by Geography (United Kingdom, Germany, France, Italy, Spain, Russia, Rest of Europe). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Tons).

Europe Bulky Waste Collection Service Market Trends and Insights

Increasing Renovation and Refurbishment Activities Across Residential and Commercial Sectors

The European bulky waste collection service market is growing significantly, driven by increased renovation and refurbishment activities in residential and commercial properties. Post-COVID-19, home improvement spending has surged, with countries such as France, Germany, Spain, and Italy reporting 15-20% annual growth in renovation permits driven by remote work trends and energy-efficiency upgrades. Residential renovations generate 2-5 tons of bulky waste per project, including old fixtures, flooring, appliances, and furniture, requiring specialized disposal services. EU energy efficiency initiatives, such as the Energy Performance of Buildings Directive (EPBD), and subsidy programs in Germany, France, and the Netherlands have further boosted renovation rates, thereby contributing to increased bulky waste volumes. Commercial refurbishments, driven by hybrid work models and redesigns in offices, retail, hotels, and restaurants, add to this waste, including partition walls, fixtures, and outdated equipment. With 35% of European buildings constructed before 1970, aging properties require ongoing maintenance, sustaining demand for waste collection services. Municipalities and private operators are expanding services such as on-demand pickups and sorting facilities to manage mixed bulky waste, driven by regulatory pressures, demographic trends, and the lifecycle of Europe's built environment.

Stringent European Union Waste Management Regulations and Circular Economy Policies

The European Union is implementing the most comprehensive waste reforms in years, with provisions that reshape roles across the chain from producers to collectors. The revised Waste Framework Directive entered into force in October 2025 and includes requirements such as Extended Producer Responsibility for textiles on a set timetable and targets to reduce food waste, creating upstream pressure that ultimately affects sorting and collection practices. The Digital Waste Shipment System requires near real-time tracking for intra-European Union waste movements from May 2026, enabling better enforcement and closing gaps that previously allowed misclassification to avoid recycling obligations. Packaging reforms continue to advance toward recyclability grading and domain-specific obligations that will accelerate material redesign and downstream separation. These changes reward operators who can manage data integrity, certification, and sorting quality across bulky waste streams. They also set a higher baseline for compliance that will influence bids, pricing, and technology adoption in the Europe bulky waste collection service market.

Illegal Dumping and Non-Compliance Issues

Waste crime and non-compliance erode legitimate operators' pricing and undermine environmental goals. In England, authorities have documented significant financial losses from waste crime and introduced a multi-year plan that funds digital waste tracking and expands enforcement tools to deter illegal activity. The plan includes measures to improve data, surveillance, and permitting oversight, signaling an enforcement shift toward data-driven deterrence and earlier intervention. At the global level, multilateral bodies have highlighted the scale and complexity of waste trafficking, which complicates accountability along the supply chain and imposes additional compliance costs on lawful collectors. These patterns create near-term pricing pressure in regions with persistent enforcement gaps. Over time, digital tracking requirements and coordinated cross-border action can improve baseline compliance, which should benefit aligned operators in the Europe bulky waste collection service market.

Other drivers and restraints analyzed in the detailed report include:

- Rising Adoption of Smart Waste Management Technologies

- Increasing Urbanization and Household Waste Generation

- High Operational Costs of Specialized Collection Equipment

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Curbside collection held 46.72% share in 2025, while on-demand services are projected to advance at a 5.82% CAGR through 2031 as convenience expectations rise in dense cities. This divergence reflects a broader shift in service design, where app-based booking and shorter response times are no longer optional in metropolitan areas. Hybrid models that blend fixed routes with on-call capacity are gaining favor because they protect route density while enabling flexible surge response. Digital capabilities, including GPS tracking and dynamic scheduling, are becoming a baseline requirement in large municipal tenders in the Europe bulky waste collection service market. Operators that standardize data capture and proof-of-service improve billing accuracy, audit readiness, and customer satisfaction.

Curbside's resilience stems from network effects in established corridors, where optimized routes lower unit costs at scale. Tender specifications increasingly embed sustainability and reporting clauses, and recent public contracts illustrate the shift toward electric or right-sized vehicles and advanced in-cab systems to meet local climate goals. App-based platforms compete through service granularity and transparent pricing, with the most durable gains in high-density neighborhoods. Municipal drop-off networks and access-controlled sites can complement curbside by relieving pressure during peak disposal periods. As compliance and performance reporting converge, selection of the collection model in the Europe bulky waste collection service market will balance cost, responsiveness, and data integrity.

List of Companies Covered in this Report:

- Clearabee

- AnyJunk Limited

- Veolia Environnement S.A.

- SUEZ S.A.

- Biffa plc

- FCC Environment (FCC Recycling UK Limited)

- Stericycle, Inc.

- Remondis SE & Co. KG

- Casella Waste Systems, Inc.

- Serco

- Waste Connections, Inc.

- PreZero Service Sud GmbH

- Redooo GmbH

- Eggersmann GmbH

- FES Frankfurter Entsorgungs

- Mucvibes

- Aflex

- S&D Recycler

- WeGreen

- Stadtwerke Offenbach

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing urbanization and household waste generation

- 4.2.2 Stringent European Union waste management regulations and circular economy policies

- 4.2.3 Growing environmental awareness among European consumers

- 4.2.4 Rising adoption of smart waste management technologies

- 4.2.5 Expansion of municipal waste collection programs

- 4.2.6 Growth in e-commerce and packaging waste

- 4.3 Market Restraints

- 4.3.1 High operational costs of specialized collection equipment

- 4.3.2 Limited infrastructure in rural and remote areas

- 4.3.3 Budget constraints faced by municipal authorities

- 4.3.4 Illegal dumping and non-compliance issues

- 4.4 Value / Supply-Chain Analysis

- 4.4.1 Collection scheduling systems

- 4.4.2 Route optimization methods

- 4.4.3 Dispatch and logistics framework

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

- 4.8 Impact of GenAI-Powered Waste Collection on Service Providers' Revenue Growth

5 Market Size & Growth Forecasts (Value) and (Volume)

- 5.1 By Collection Model

- 5.1.1 Curbside

- 5.1.2 On-Demand

- 5.1.3 Hybrid

- 5.1.4 Contracted B2B

- 5.1.5 Others

- 5.2 By Source

- 5.2.1 Residential

- 5.2.2 Commercial

- 5.2.3 Industrial

- 5.2.4 Municipal/Government

- 5.2.5 Others (Religious Institutions, Temporary Disaster Relief Camps, Film/TV Production Sets)

- 5.3 By Waste Type

- 5.3.1 Furniture & Upholstery

- 5.3.2 Metal & Scrap Items

- 5.3.3 White Goods/Appliances

- 5.3.4 Construction & Demolition

- 5.3.5 Others (Event-specific Waste, Biomedical/Institutional)

- 5.4 By Country

- 5.4.1 United Kingdom

- 5.4.2 Germany

- 5.4.3 France

- 5.4.4 Italy

- 5.4.5 Spain

- 5.4.6 Russia

- 5.4.7 Rest of Europe

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)}

- 6.4.1 Clearabee

- 6.4.2 AnyJunk Limited

- 6.4.3 Veolia Environnement S.A.

- 6.4.4 SUEZ S.A.

- 6.4.5 Biffa plc

- 6.4.6 FCC Environment (FCC Recycling UK Limited)

- 6.4.7 Stericycle, Inc.

- 6.4.8 Remondis SE & Co. KG

- 6.4.9 Casella Waste Systems, Inc.

- 6.4.10 Serco

- 6.4.11 Waste Connections, Inc.

- 6.4.12 PreZero Service Sud GmbH

- 6.4.13 Redooo GmbH

- 6.4.14 Eggersmann GmbH

- 6.4.15 FES Frankfurter Entsorgungs

- 6.4.16 Mucvibes

- 6.4.17 Aflex

- 6.4.18 S&D Recycler

- 6.4.19 WeGreen

- 6.4.20 Stadtwerke Offenbach

7 Market Opportunities & Future Outlook

- 7.1 Smart Cities & IoT Integration

- 7.2 Producer Responsibility Expansion