|

시장보고서

상품코드

2063755

경구 단백질 및 펩티드 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Oral Proteins And Peptides - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

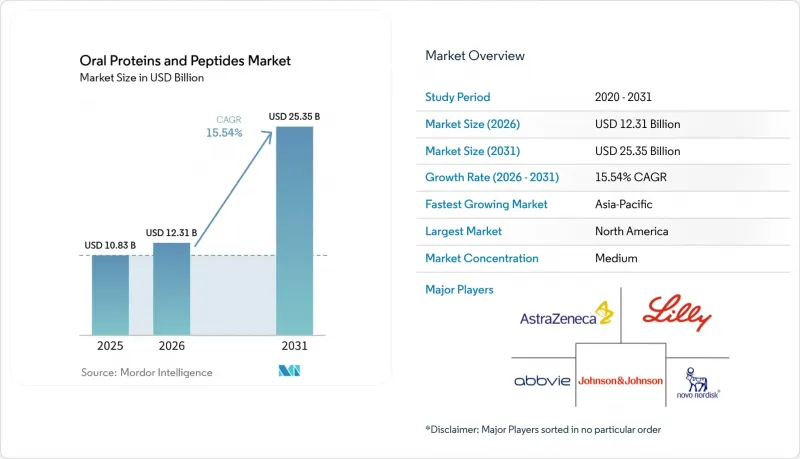

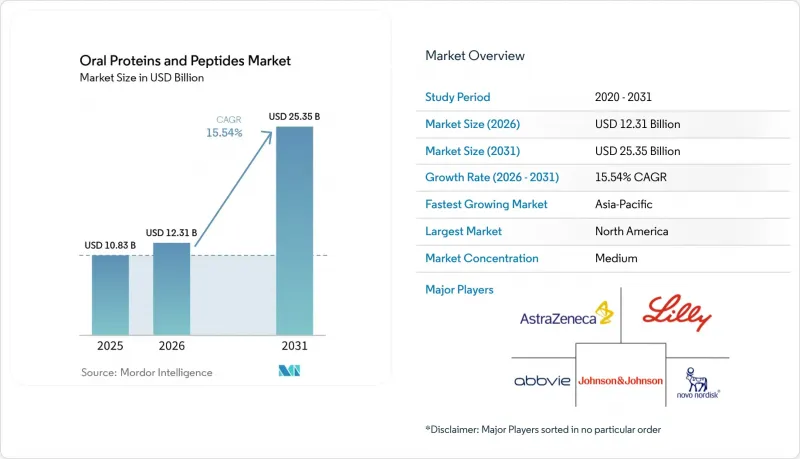

Mordor Intelligence에 의하면, 경구 단백질 및 펩티드 시장 규모는 2025년에 108억 3,000만 달러로 평가되었습니다. 2026년 123억 1,000만 달러에서 2031년까지 253억 5,000만 달러에 이를 것으로 예상되며, 예측 기간(2026-2031년) CAGR은 15.54%를 나타낼 전망입니다.

본 보고서는 분자 분류(펩티드, 단백질, 효소), 약물 분류별(GLP-1 수용체 작용제, GC-C 작용제, 소마토스타틴 수용체 작용제, 췌장 효소, 바소프레신 유사체), 적응증(2형 당뇨병, 비만, IBS-C, CIC, EPI, 말단거대증, 기타), 지역(북미, 유럽, 아시아태평양, 중동 및 아프리카, 남미)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 경구 단백질 및 펩티드 시장 동향 및 인사이트

GLP-1 경구제 개발의 기세와 비만 치료제 출시가 대상 시장과 복약 순응도를 확대

일라이 릴리사의 ‘Foundayo(올포르글리프론)’는 2026년 4월 FDA 승인을 획득했으며, 노보노르디스크사의 25mg 경구용 세마글루티드 정제는 2026년 1월 미국 약국에 유통되기 시작하면서, 비만 치료제로 승인된 최초의 펩티드 정제가 상업적 규모로 시장에 등장했습니다. 2026년 7월부터 시행되는 메디케어의 GLP-1 브릿지 시범 사업에서는 두 제품에 대해월245달러의 순가격(본인 부담금 50달러)으로 환급이 이루어지고 있으며, 이는 치료 지속률을 높이는 경구용 펩티드 제제에 대한 자금 지원에 대해 지불 주체의 준비가 되어 있음을 보여줍니다. 7만 8,297명의 환자를 대상으로 한 미국의 청구 데이터 분석에 따르면, 경구용 세마글루티드는 12개월 시점에서 65.1%라는 높은 복약 순응도를 보인 반면, 주사제는 38.8%에 그쳤습니다. 그러나 이탈리아의 관찰 연구에 따르면, 위장 장애로 인해 18개월 시점의 지속률이 46.0%로 떨어진 것으로 나타났습니다. 이러한 데이터는 2세대 정제가 공복 시간을 단축하고 메스꺼움 발생률을 낮춘다면, 경구 단백질 및 펩티드 시장이 그 혜택을 볼 것임을 시사합니다.

만성 질환의 경우, 환자의 선호도와 복약 순응도에 따라 주사제에서 경구용 고분자 제제로 전환되고 있습니다.

여러 만성 질환에서 높은 복약 순응도는 질환 활동성의 감소와 상관관계가 있으며, 투여의 용이성이 그 순응도를 좌우합니다. 염증성 장질환에 대한 실세계 연구에 따르면, 80%의 복약 순응도가 활동성 질환 발병 위험을 70% 감소시키는 것과 관련이 있는 것으로 나타났습니다. 따라서, 새롭게 등장한 경구용 펩티드 제제는 편의성과 내약성 사이의 균형을 맞추어야 합니다. 엄격한 ‘물만 마시기’ 단식 규칙이나 투여량과 관련된 소화불량은 치료의 지속을 위협하는 요인이 됩니다. Structure Therapeutics사의 GSBR-1290이나 Hansoh Pharma사의 HS-10535와 같은 2상 및 3상 후보 약물은 금식 시간을 10분 미만으로 단축하고 구토 유발성을 줄이는 것을 목표로 하고 있으며, 주 1회 주사제에 대한 향후 시장 점유율 잠식 압력을 시사하고 있습니다.

경구 생체이용률이 극히 낮고 변동성이 커서, 고용량의 원료의약품과 높은 제조 원가를 초래합니다.

기존 경구용 펩티드 제제의 흡수율이 1% 이상의 경우는 드물며, 그 결과 주사제의 10-100배에 달하는 투여량이 필요하게 되어 비용과 위장관 부작용이 모두 증가하고 있습니다. 경구용 세마글루티드는 1mg 주사제와 동등한 효과를 얻기 위해 14mg이 필요하며, 그럼에도 노출량의 변동계수는 50-60%에 달할 전망입니다. 이러한 변동성은 경구 단백질 및 펩티드 제제 시장 규모 측면에서 경제성을 저해하는 요인이 되고 있습니다.

부문별 분석

2025년 기준으로, 펩티드 제품은 확립된 GLP-1 및 GC-C 프랜차이즈 덕분에 경구 단백질 및 펩티드 시장의 78.31%를 차지했습니다. 단백질 및 효소 분야의 경구 단백질 및 펩티드 시장 규모는 경구용 제제가 장벽을 우회함에 따라 연평균 성장률(CAGR) 16.32%로 확대될 것으로 전망됩니다. 아이언우드사의 펩티드 제제 ‘LINZESS’는 2026년 1분기에 전년 동기 대비 97% 증가한 2억 7,250만 달러의 매출을 기록하며, 펩티드 시장의 회복력을 보여주었습니다. 이와 동시에, ‘RaniPill’은 우스테키누맙 바이오시밀러에서 84%의 생체이용률을 달성하여 단백질 전달의 유효성을 입증했습니다. 이 부문의 장기적인 성장 여지는 기기 생산 규모의 확대와 반복 투여 시 장의 안전성 입증에 달려 있습니다.

2세대 효소 제제도 단백질의 성장 잠재력을 뒷받침하고 있습니다. 갱신된 CREON 및 Pertzye의 첨부문서에는 지방 흡수율이 83% 이상이라고 명시되어 있으며, 고액의 보험 급여를 정당화할 수 있는 명확한 유효성 평가 지표가 제시되어 있습니다. 그렇긴 하지만, 기존의 경구용 제제에서는 그램 단위의 API(유효 성분)가 필요하기 때문에 단백질 제제는 제조 원가가 높게 책정되는 경향이 있으며, 성장의 열쇠는 여전히 디바이스 플랫폼에 있습니다.

지역별 분석

북미는 메디케어 GLP-1 브릿지 및 FDA의 펩티드에 관한 명확한 지침과 같은 지불자 주도적 노력에 힘입어 2025년 매출의 45.75%를 차지했습니다. 또한, 해당 지역에는 경구용 기기 관련 임상시험 기관의 대부분이 집중되어 있어, 단백질 전달 기술의 초기 성장 기회를 포착하기에 유리한 위치에 있습니다. 그러나 위장관 부작용으로 인해 실제 복용 순응도가 낮아, 장기적인 시장 점유율 확대에 걸림돌이 되고 있습니다.

유럽에서는 간호사가 투여하는 데 드는 비용을 절감할 수 있는 경우, 경구용 제제를 선호하는 중앙집권적인 의료기술평가의 혜택을 받고 있습니다. EMA의 펩티드 생물학적 동등성에 관한 지침의 통일은 신청 위험을 줄이고, 가격 경쟁을 촉진할 가능성이 있는 바이오시밀러 시장 진입을 촉진하고 있습니다.

아시아태평양은 인크레틴 계열 약물의 혁신에 대한 중국 규제 당국의 개방적인 태도와 일본의 치료법별 PMDA 지침에 힘입어, 2031년까지 연평균 성장률(CAGR) 16.12%를 나타낼 것으로 전망됩니다. 아스트라제네카가 CSPC와 체결한 12억 달러 규모의 계약과 같은 현지 생산 협정은 공급망의 지역화를 목표로 하며, 고용량 정제에 대한 관세 및 운송 비용 절감으로 이어집니다.

남미 및 중동 및 아프리카은 상환의 장벽과 콜드체인 인프라 부족으로 인해 여전히 발전 단계에 머물러 있습니다. 그렇긴 하지만, 비만 유병률 증가와 원격 약국 서비스의 보급은 더 저렴한 제네릭 펩티드가 등장할 경우의 미래 기회를 시사하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTHAccording to Mordor Intelligence, the oral proteins and peptides market size was valued at USD 10.83 billion in 2025 and is estimated to grow from USD 12.31 billion in 2026 to reach USD 25.35 billion by 2031, at a CAGR of 15.54% during the forecast period (2026-2031).

This report is Segmented by Molecule Class (Peptides, Proteins & Enzymes), Drug Class (GLP-1 RAs, GC-C Agonists, Somatostatin RAs, Pancreatic Enzymes, Vasopressin Analogs), Indication (T2D, Obesity, IBS-C, CIC, EPI, Acromegaly, Others), and Geography (North America, Europe, Asia-Pacific, MEA, South America). Market Forecasts are Provided in Terms of Value (USD).

Global Oral Proteins And Peptides Market Trends and Insights

GLP-1 Oralization Momentum and Obesity Pill Launches Expand Addressable Market and Adherence

Eli Lilly's Foundayo (orforglipron) won FDA approval in April 2026, and Novo Nordisk's 25 mg oral semaglutide tablet reached U.S. pharmacies in January 2026, creating the first obesity-labeled peptide tablets to hit commercial scale. The Medicare GLP-1 Bridge demonstration, effective July 2026, reimburses both products at a USD 245 net monthly price with a USD 50 out-of-pocket cost, underscoring payer readiness to fund oral peptides that improve persistence. A 78,297-patient U.S. claims analysis found that oral semaglutide achieved 65.1% high adherence at 12 months versus 38.8% for injectables. However, an Italian observational study showed that 18-month persistence fell to 46.0% owing to gastrointestinal intolerance. The data suggest the oral proteins and peptides market will benefit when second-generation tablets reduce fasting windows and nausea rates.

Patient Preference and Adherence Shift from Injections to Oral Macromolecules in Chronic Diseases

High refill adherence correlates with lower disease activity across multiple chronic illnesses, and ease of administration drives that adherence. Real-world studies in inflammatory bowel disease linked 80% medication possession to a 70% fall in active-disease odds. Emerging oral peptides must therefore balance convenience with tolerability; strict "water-only" fasting rules and dose-related dyspepsia threaten persistence. Phase 2 and Phase 3 assets such as Structure Therapeutics' GSBR-1290 and Hansoh Pharma's HS-10535 aim to cut fasting windows below 10 minutes and reduce emetogenicity, suggesting future crowd-out pressure on weekly injectables.

Very Low and Variable Oral Bioavailability Drives High API Loads and Cost of Goods

Classic oral peptides rarely exceed 1% absorption, forcing 10-100X injectable doses and inflating both cost and gastrointestinal side-effects. Oral semaglutide requires 14 mg to match a 1 mg injection and still posts 50-60% coefficient-of-variation in exposure. Variability undermines the oral proteins and peptides market size economics.

Other drivers and restraints analyzed in the detailed report include:

- Regulatory Tailwinds for Oral Peptides

- Next-Generation Ingestible Devices Unlock Systemic Delivery of Large Proteins

- Complex CMC and Stringent Regulatory Evidence for Enhancer/Device Safety

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Peptides held 78.31% of the oral proteins and peptides market in 2025 thanks to entrenched GLP-1 and GC-C franchises. The oral proteins and peptides market size for proteins and enzymes is projected to expand at 16.32% CAGR as ingestible injectors sidestep gut-wall barriers. Ironwood's LINZESS peptide reported USD 272.5 million Q1 2026 revenue, up 97% year over year, illustrating peptide resilience. In parallel, RaniPill achieved 84% bioavailability for ustekinumab biosimilar, validating protein delivery viability. The segment's long-run upside hinges on scaling device manufacturing and proving repeat-dose intestinal safety.

Second-generation enzyme formulations also reinforce protein upside. Updated CREON and Pertzye labels now cite coefficients of fat absorption above 83%, providing clear efficacy endpoints that justify premium reimbursement. Still, proteins face steep cost-of-goods when classical oral formulations demand gram-level API loads, keeping device platforms central to growth.

Geography Analysis

North America retained 45.75% of 2025 revenue, bolstered by payer initiatives like the Medicare GLP-1 Bridge and clear FDA peptide guidance. The region also hosts most ingestible-device clinical sites, positioning it to capture early protein-delivery upside. Yet real-world adherence gaps driven by gastrointestinal side-effects cap long-term share gains.

Europe benefits from centralized health-technology assessments that welcome oral options when they lower nurse-administered costs. EMA alignment on peptide bioequivalence lowers filing risk, encouraging biosimilar entrants that could compress price points.

Asia-Pacific is projected to record a 16.12% CAGR to 2031, supported by China's regulatory openness to incretin innovation and Japan's modality-specific PMDA guidance. Local manufacturing pacts, such as AstraZeneca's USD 1.2 billion CSPC agreement, aim to regionalize supply chains, cutting tariffs and shipping cost for high-dose tablets.

South America and the Middle East & Africa remain nascent, constrained by reimbursement hurdles and limited cold-chain infrastructure. Nonetheless, rising obesity prevalence and tele-pharmacy adoption point toward future opportunities once cheaper generic peptides arrive.

- Abbvie

- Astellas Pharma

- AstraZeneca

- Bausch Health

- Biora Therapeutics

- Bio-Thera Solutions

- Celltrion

- Chiesi Group

- Emisphere/Novo

- Enteris BioPharma

- Eli Lilly and Company

- Ferring Pharmaceuticals

- i2O Therapeutics

- Intract Pharma

- Ironwood Pharmaceuticals

- Johnson & Johnson

- Merrion Pharmaceuticals

- Novo Nordisk

- Oramed Pharmaceuticals

- Rani Therapeutics

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 GLP-1 Oralization Momentum and Obesity Pill Launches Expand Addressable Market and Adherence

- 4.2.2 Patient Preference and Adherence Shift from Injections to Oral Macromolecules in Chronic Diseases

- 4.2.3 Regulatory Tailwinds for Oral Peptides

- 4.2.4 Next-Gen Ingestible Devices Unlock Systemic Delivery of Large Proteins

- 4.2.5 Colon-Targeted Platforms for Local Biologics Transform IBD and GI Antibodies Use-Cases

- 4.2.6 Ionic-Liquid and Novel Excipient Systems Raise Feasible BA Windows for Select Peptides

- 4.3 Market Restraints

- 4.3.1 Very Low and Variable Oral Bioavailability Drives High API Loads and CoGs

- 4.3.2 Complex CMC and Stringent Regulatory Evidence for Enhancer/Device Safety

- 4.3.3 Long-Term Safety Questions for Chronic Use of Potent Permeation Enhancers

- 4.3.4 Limited Generalizable Enhancer Chemistries; Platform Applicability Remains Molecule-Specific

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Molecule Class

- 5.1.1 Peptides

- 5.1.2 Proteins & Enzymes

- 5.2 By Drug Class

- 5.2.1 GLP-1 receptor agonists

- 5.2.2 GC-C agonists

- 5.2.3 Somatostatin receptor agonists

- 5.2.4 Pancreatic enzymes

- 5.2.5 Vasopressin analogs

- 5.3 By Indication

- 5.3.1 Type 2 Diabetes

- 5.3.2 Obesity & Overweight Management

- 5.3.3 IBS-C

- 5.3.4 Chronic Idiopathic Constipation (CIC)

- 5.3.5 Exocrine Pancreatic Insufficiency (EPI)

- 5.3.6 Acromegaly

- 5.3.7 Others (Celiac Disease, Inflammatory Bowel Disease, etc.)

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.3.1 AbbVie Inc.

- 6.3.2 Astellas Pharma

- 6.3.3 AstraZeneca

- 6.3.4 Bausch Health

- 6.3.5 Biora Therapeutics

- 6.3.6 Bio-Thera Solutions

- 6.3.7 Celltrion

- 6.3.8 Chiesi Group

- 6.3.9 Emisphere/Novo

- 6.3.10 Enteris BioPharma

- 6.3.11 Eli Lilly and Company

- 6.3.12 Ferring Pharmaceuticals

- 6.3.13 i2O Therapeutics

- 6.3.14 Intract Pharma

- 6.3.15 Ironwood Pharmaceuticals, Inc.

- 6.3.16 Johnson & Johnson

- 6.3.17 Merrion Pharmaceuticals

- 6.3.18 Novo Nordisk A/S

- 6.3.19 Oramed Pharmaceuticals

- 6.3.20 Rani Therapeutics

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment