|

시장보고서

상품코드

2063816

SOHO 라우터 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)SOHO Router - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

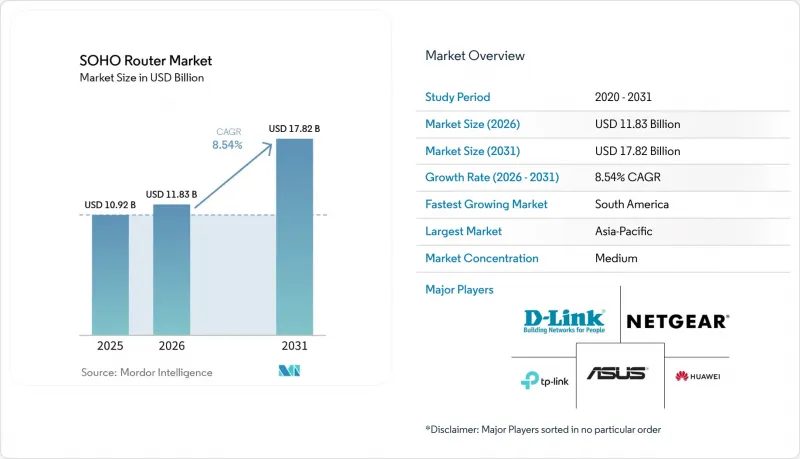

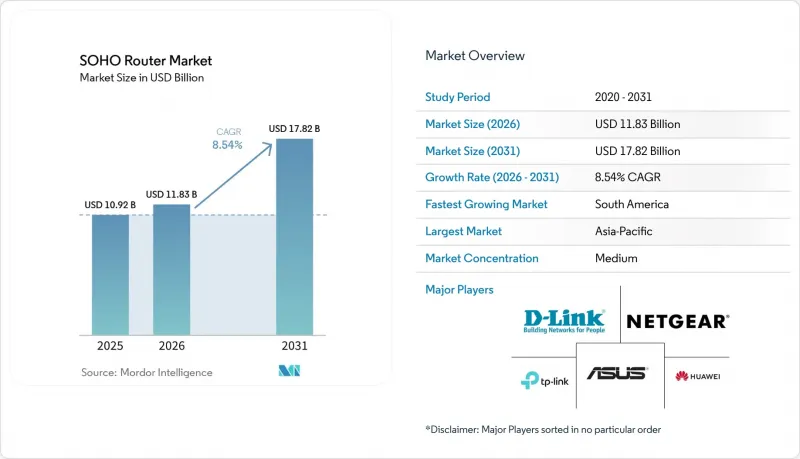

Mordor Intelligence에 의하면, SOHO 라우터 시장 규모는 2025년에 109억 2,000만 달러로 평가되었습니다. 2026년 118억 3,000만 달러에서 2031년까지 178억 2,000만 달러에 이를 것으로 예상되며, 예측 기간(2026-2031년) CAGR은 8.54%를 나타낼 전망입니다.

본 보고서는 주파수 대역(싱글 밴드, 듀얼 밴드, 트라이 밴드, 쿼드 밴드), Wi-Fi 표준(Wi-Fi 4, Wi-Fi 5, Wi-Fi 6, Wi-Fi 6E, Wi-Fi 7), 용도(주거용, 홈 오피스, 소규모 사무실 등), 판매 채널(온라인 소매, 오프라인 소매, ISP 번들 CPE 및 엔터프라이즈 채널 파트너), 그리고 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제공됩니다.

세계의 SOHO 라우터 시장 동향 및 인사이트

라우터에 AI 가속기를 통합하여 실시간 트래픽 최적화 실현

신경망 처리 장치를 탑재한 라우터는 수동적인 패킷 전달에서 능동적인 오케스트레이션으로 전환되고 있습니다. 차터 스펙트럼은 2025년에 기기 내 AI를 탑재한 Wi-Fi 7 게이트웨이를 도입하고, 동적 혼잡 재라우팅을 시행한 후 지원 문의 건수가 감소했다고 보고했습니다. 퀄컴은 2025년 투자자 브리핑에서 추론 엔진이 탑재된 Wi-Fi 7 칩셋을 채택한 250개 이상의 네트워크 설계를 확인했습니다. 이러한 실리콘은 수동으로 설정하는 QoS(서비스 품질) 규칙 없이도 트래픽 흐름을 분류하고, 지연에 민감한 패킷을 우선적으로 처리합니다. 화상 회의, 클라우드 게임, IoT 센서를 동시에 사용하는 가정에서는 지터 감소로 인한 이점을 누릴 수 있어, 서비스 제공업체의 해지율을 낮출 수 있습니다. 비정상적인 트래픽을 감지하는 예측 알림은 관리형 보안 구독의 업셀링 기회를 창출합니다.

Wi-Fi 6 및 Wi-Fi 7 규격의 급속한 보급

Wi-Fi Alliance는 2024년에 2억 3,300만 대의 Wi-Fi 7 기기를 인증했으며, 2028년까지 21억 대에 달할 것으로 전망하고 있는데, 이는 Wi-Fi 6의 보급 속도를 웃도는 수치입니다. MediaTek의 Filogic 880 및 660 플랫폼은 2025년에 출하가 시작되어, 200달러 미만의 트라이밴드 라우터를 실현했습니다. 이에 이어 브로드컴과 퀄컴은 320MHz 채널과 4096-QAM을 활용해 40Gbps의 처리량을 실현하는 쿼드밴드 레퍼런스 설계를 발표했습니다. 2026년 1월, FCC가 표준 출력의 6GHz 대역 기기에 대한 승인을 내리고 실내 통신 범위 제한이 철폐됨에 따라, 소규모 사무실 및 산업 분야에서의 도입이 가속화되었습니다. 칩셋 비용의 하락과 규제의 명확화가 맞물리면서, Wi-Fi 5 하드웨어의 교체 주기가 단축되고 있습니다.

통신 사업자가 번들로 제공하는 5G 고정 무선 게이트웨이에 대한 대체 제품의 위협이 커지고 있습니다.

T-Mobile은 Inseego사의 FX4200 및 FX4100 게이트웨이를 초기 비용 없이 번들로 제공하며, 트라이밴드 Wi-Fi 7과 5G 백홀을 통합함으로써 독립형 라우터를 대체하려 하고 있습니다. 퀄컴의 싱글 다이 Dragonwing 플랫폼은 부품 원가를 더욱 낮춤으로써, 통신 사업자가 하드웨어 보조금을 제공할 수 있게 해줍니다. 통합된 요금 청구를 원하는 중소기업들은 이러한 게이트웨이를 선택하고 있으며, 특히 광섬유가 보급되지 않은 지역에서 소매용 라우터의 판매량을 감소시키고 있습니다.

부문별 분석

2025년, 트리밴드 라우터는 지연에 민감한 4K 스트리밍 및 클라우드 게임 수요를 흡수함으로써 SOHO 라우터 시장 점유율을 끌어올렸습니다. 듀얼 밴드 시스템은 여전히 중가 시장을 주도하고 있지만, 2031년까지는 트리플 밴드 제품의 출하량이 SOHO 라우터 시장 전체보다 더 빠르게 증가할 것으로 예측됩니다. MediaTek과 Broadcom이 개발한 저비용 Wi-Fi 7용 칩 덕분에 실제 판매 가격이 200달러 미만으로 떨어졌으며, 멀티 기가비트급 용량을 일반 소비자용 가격대에서 이용할 수 있게 되었습니다.

메쉬 네트워크가 주요 원동력이 되고 있습니다. 쿼드밴드 설계에서는 6GHz 대역의 무선 기능을 백홀 전용으로 할당함으로써, 이더넷 케이블 없이도 결정적 지연을 실현하고 있습니다. 2026년 1월, 표준 출력의 6GHz 대역 무선 기기에 대한 규제 승인이 내려짐에 따라 트라이밴드 키트가 더 넓은 범위를 커버할 수 있게 되었고, 교외 주택에서의 도입률이 높아지고 있습니다. 싱글 밴드 기기는 초저가 제품군이나 임베디드형 IoT 엔드포인트에만 남아 있지만, 칩셋 비용이 지속적으로 하락함에 따라 결국에는 사라질 것으로 예측됩니다.

2025년에도 Wi-Fi 5는 여전히 가성비형 ISP 번들 상품의 기반을 이루었지만, Wi-Fi 7의 연평균 성장률(CAGR) 24.76%는 2027년 이후 SOHO 라우터 시장 규모에서 판매 대수를 견인하는 주역으로서의 입지를 확고히 하고 있습니다. FCC의 고출력 6GHz 대역 운용 승인으로 인해 실질적인 커버리지 범위가 확대된 한편, 각 칩셋 공급업체들은 320 MHz 채널 및 멀티링크 운용의 통합을 앞다투어 추진했습니다. 게이밍이나 프로슈머와 같은 틈새 시장의 얼리 어답터들은 기기의 수명 주기에 앞서 업그레이드를 하려는 의지를 보이고 있으며, 이로 인해 교체 주기가 단축되고 있습니다.

엔터프라이즈급 소규모 사무실에서는 OFDMA의 효율성과 IoT 기기의 배터리 수명을 연장하는 타겟 웨이크 타임 기능을 갖춘 Wi-Fi 6E가 중요하게 여겨지고 있습니다. Wi-Fi 4 및 그 이전 세대는 점차 줄어들고 있으며, 개조 예산이 확보될 때까지는 구형 산업용 컨트롤러로만 제한되고 있습니다. 트리밴드 무선 기능을 탑재한 클라이언트 기기가 증가함에 따라 상호 운용성에 대한 우려는 줄어들고 있으며, 공급업체에게는 교체 기회가 확대되고 있습니다.

지역별 분석

2025년 SOHO 라우터 시장에서 아시아태평양은 36.52%를 차지했습니다. 이는 중국의 범용 광대역 정책과 인도의 2선 도시에 대한 광섬유 구축이 뒷받침한 결과입니다. 샤오미는 자사 생태계 전반에 걸쳐 9억 460만 대의 연결 기기를 통해 수익을 창출하고 있으며, 플래시 세일을 활용해 인도(시장 점유율 13.4%) 및 동남아시아(16.7%)에서 라우터 보급률을 높였습니다. 일본에서는 밀집된 공동주택이 Wi-Fi 6E의 보급을 가속화한 반면, 호주에서는 NBN의 업그레이드로 인해 구형 ADSL 하드웨어의 교체 작업이 진행되었습니다. 해당 지역의 다양성으로 인해 수요는 가격을 중시하는 듀얼 밴드 제품과 프리미엄 쿼드 밴드 제품으로 나뉘고 있습니다.

남미에서는 통신 사업자들이 지방 도시로 광섬유망을 확장함에 따라 연평균 성장률(CAGR) 10.46%로 성장을 주도하고 있습니다. 브라질, 칠레, 페루, 멕시코에서는 2024년 말까지 각각 광섬유 보급률이 70%를 넘어섬에 따라, 2.4GHz만 지원하는 라우터의 대역폭 제약이 두드러지고 있습니다. TP-Link가 브라질에 신설할 예정인 공장은 공급망을 단축하고 배송 비용을 절감하는 한편, 샤오미는 지역 시장 점유율 17.9%를 차지하며 2위를 기록하고 있습니다. 경제적 역풍과 통화 약세로 인해 가격에 대한 민감도가 높아지고 있지만, 상파울루와 부에노스아이레스의 도심 지역에서는 메쉬 번들 수요가 확대되고 있습니다.

북미와 유럽에서는 보급률이 성숙 단계에 접어들었음에도 불구하고, Wi-Fi 7로의 업그레이드나 관리형 서비스로의 전환을 통해 교체 수요가 유지되고 있습니다. 미국에서는 2025년 9월까지 광섬유 가입자 수가 1억 건을 돌파하며, 기가비트 대칭 처리량을 지원하는 라우터의 보급을 촉진했습니다. 차터사의 5G 페일오버 기능을 탑재한 Wi-Fi 7 게이트웨이는 지원 부담을 줄이고 고객 만족도를 높임으로써, 매니지드 모델의 효과성을 입증했습니다. UAE와 사우디아라비아를 비롯한 중동의 스마트시티 구상이 엔터프라이즈급 라우터 수요를 견인하고 있는 반면, 아프리카의 많은 지역은 모바일 광대역에 의존하고 있어 하이엔드 라우터의 보급은 제한적입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTHAccording to Mordor Intelligence, the sOHO router market size was valued at USD 10.92 billion in 2025 and estimated to grow from USD 11.83 billion in 2026 to reach USD 17.82 billion by 2031, at a CAGR of 8.54% during the forecast period (2026-2031).

This report is Segmented by Frequency Band (Single-Band, Dual-Band, Tri-Band, and Quad-Band), Wi-Fi Standard (Wi-Fi 4, Wi-Fi 5, Wi-Fi 6, Wi-Fi 6E, and Wi-Fi 7), Application (Residential, Home Office, Small Office, and More), Distribution Channel (Online Retail, Offline Retail, ISP Bundled CPE, and Enterprise Channel Partners), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global SOHO Router Market Trends and Insights

Integration of AI Accelerators in Routers Enabling Real-Time Traffic Optimization

Routers embedding neural-processing units have shifted from passive packet forwarding to active orchestration. Charter Spectrum introduced Wi-Fi 7 gateways with on-device AI in 2025, reporting lower support calls after dynamic congestion rerouting. Qualcomm confirmed more than 250 networking designs using Wi-Fi 7 chipsets equipped with inference engines in its 2025 investor briefing. Such silicon classifies traffic flows and prioritizes latency-sensitive packets without manual quality-of-service rules. Households running simultaneous video conferences, cloud gaming, and IoT sensors benefit from lower jitter, reducing churn for service providers. Predictive alerts that flag anomalous traffic create upsell opportunities for managed security subscriptions.

Rapid Adoption of Wi-Fi 6 and Wi-Fi 7 Standards

The Wi-Fi Alliance certified 233 million Wi-Fi 7 devices in 2024 and forecasts 2.1 billion by 2028, eclipsing the ramp of Wi-Fi 6. MediaTek's Filogic 880 and 660 platforms began shipping in 2025, enabling sub-USD 200 tri-band routers. Broadcom and Qualcomm followed with quad-band reference designs that exploit 320-MHz channels and 4096-QAM to achieve 40 Gbps throughput. January 2026 FCC authorization for standard-power 6 GHz devices removed indoor-range limits, catalyzing small-office and industrial uptake. Together, lower chipset costs and regulatory clarity compress replacement windows for Wi-Fi 5 hardware.

Growing Substitution Threat from 5G Fixed-Wireless Gateways Bundled by Carriers

T-Mobile bundles Inseego's FX4200 and FX4100 gateways at zero upfront cost, integrating tri-band Wi-Fi 7 and 5G backhaul to displace standalone routers. Qualcomm's single-die Dragonwing platform further lowers bill-of-materials, letting carriers subsidize hardware. Small enterprises seeking unified billing opt for these gateways, eroding retail router volumes, especially in areas where fiber is scarce.

Other drivers and restraints analyzed in the detailed report include:

- Accelerated Rollout of Fiber and 5G Home Broadband Services

- ISPs Transitioning to Subscription-Based Managed Wi-Fi Services for SOHO Customers

- Cybersecurity Vulnerabilities and Firmware Update Negligence

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Tri-band routers boosted the SOHO router market share by capturing latency-sensitive 4K streaming and cloud gaming demand in 2025. Dual-band systems still dominate the mid-priced tiers, but tri-band shipments are forecast to grow faster than the overall SOHO router market through 2031. Lower-cost Wi-Fi 7 silicon from MediaTek and Broadcom lowered street prices beneath USD 200, bringing multi-gigabit capacity to mass-market budgets.

Mesh networking is the principal catalyst: quad-band designs dedicate a 6 GHz radio for backhaul, delivering deterministic latency without Ethernet cabling. Regulatory clearance for standard-power 6 GHz radios in January 2026 allows tri-band kits to cover larger floorplates, boosting attachment rates in suburban homes. Single-band devices linger only in ultra-low-cost brackets and embedded IoT endpoints, signaling eventual obsolescence as chipset costs continue to fall.

Wi-Fi 5 still anchors value-tier ISP bundles in 2025, yet Wi-Fi 7's 24.76% CAGR positions it as the volume engine for the SOHO router market size beyond 2027. FCC authorization for higher-power 6 GHz operation expanded viable coverage footprints, while chipset vendors raced to integrate 320 MHz channels and multi-link operation. Early adopters in gaming and prosumer niches validated willingness to upgrade ahead of device cycles, shortening refresh intervals.

Enterprise-grade small offices prize Wi-Fi 6E for its OFDMA efficiency and target wake time features that prolong IoT battery life. Wi-Fi 4 and earlier generations are in steady decline, limited to legacy industrial controllers pending retrofit budgets. As more client devices ship with tri-band radios, interoperability concerns recede, widening replacement opportunities for vendors.

Geography Analysis

Asia-Pacific contributed 36.52% to the SOHO router market in 2025, buoyed by China's universal-broadband policy and India's tier-2 fiber rollouts. Xiaomi monetized 904.6 million connected devices across its ecosystem, leveraging flash sales to lift router penetration in India (13.4% unit share) and Southeast Asia (16.7%). Japan's dense apartment clusters accelerated Wi-Fi 6E adoption, while Australia's NBN upgrades drove replacements of legacy ADSL hardware. The region's heterogeneity divides demand between cost-optimized dual-band units and premium quad-band offerings.

South America leads growth at 10.46% CAGR as carriers extend fiber to secondary cities. Brazil, Chile, Peru and Mexico each exceeded 70% fiber penetration by late 2024, exposing bandwidth constraints in 2.4 GHz-only routers. TP-Link's upcoming Brazilian factory will shorten supply chains and lower landed costs, while Xiaomi ranks second in regional share at 17.9%. Economic headwinds and currency depreciation heighten price sensitivity, but mesh bundles gain traction in urban Sao Paulo and Buenos Aires.

North America and Europe show mature penetration yet sustain replacement demand through Wi-Fi 7 upgrades and managed-service transitions. U.S. fiber passings crossed 100 million by September 2025, driving the adoption of routers capable of gigabit symmetric throughput. Charter's Wi-Fi 7 gateway with 5G failover reduced support overhead and improved customer satisfaction, validating the managed model. Middle East smart-city agendas in the UAE and Saudi Arabia drive enterprise-grade router demand, whereas much of Africa relies on mobile broadband, limiting high-end router adoption.

- TP-Link Corporation Limited

- NETGEAR-Inc.

- ASUSTeK Computer Inc.

- Shenzhen Tenda Technology Co., Ltd.

- AVM GmbH

- Linksys USA, Inc.

- D-Link Corporation

- Belkin International, Inc.

- Ubiquiti Inc.

- MikroTikls SIA

- Synology Inc.

- TRENDnet, Inc.

- GL Technologies (Hong Kong) Limited

- Peplink International Limited

- DrayTek Corp.

- Comtrend Corporation

- Ruijie Networks Co., Ltd.

- Mercusys Technologies Co., Ltd.

- Edimax Technology Co., Ltd.

- Xiaomi Communications Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerating Fibre-to-the-Home Roll-outs Boosting Router Upgrades

- 4.2.2 Rapid Adoption of Wi-Fi 6 and 6E Standards in SOHO Environments

- 4.2.3 Growth of Hybrid and Remote Work Requiring Enterprise-Grade Home Networking

- 4.2.4 Mesh Wi-Fi Systems Eliminating Coverage Dead Zones

- 4.2.5 AI-Enabled Traffic Optimisation Creating Premium Differentiation (Under-the-Radar)

- 4.2.6 ISP Bundled Security Subscriptions Increasing Refresh Cycles (Under-the-Radar)

- 4.3 Market Restraints

- 4.3.1 Price Sensitivity in Emerging Markets Limiting High-End Adoption

- 4.3.2 Rapid Technology Obsolescence Shortening Product Life Cycles

- 4.3.3 Fragmented 6 GHz Spectrum Policies Delaying Wi-Fi 6E/7 Launches (Under-the-Radar)

- 4.3.4 Supply-Chain Semiconductor Shortages Constraining Production (Under-the-Radar)

- 4.4 Industry Supply-Chain Analysis

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Bandwidth Standard

- 5.1.1 Wi-Fi 5

- 5.1.2 Wi-Fi 6

- 5.1.3 Wi-Fi 6E

- 5.1.4 Wi-Fi 7

- 5.2 By Product Type

- 5.2.1 Single-band Router

- 5.2.2 Dual-band Router

- 5.2.3 Tri-band Router

- 5.2.4 Mesh Wi-Fi System

- 5.2.5 Gaming Router

- 5.2.6 Portable Travel Router

- 5.3 By Distribution Channel

- 5.3.1 Online Retail

- 5.3.2 ISP/Telecom Provider Bundles

- 5.3.3 Electronics Specialty Stores

- 5.3.4 Mass Market/Hypermarket

- 5.4 By Application/User Type

- 5.4.1 Residential Home

- 5.4.2 Small Office/Home Office (SOHO)

- 5.4.3 Small Business (SMB)

- 5.4.4 Remote Workforce

- 5.4.5 Gaming Enthusiasts

- 5.4.6 Smart Home/IoT

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 France

- 5.5.3.3 United Kingdom

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia and New Zealand

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Egypt

- 5.5.6.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 TP-Link Corporation Limited

- 6.4.2 NETGEAR-Inc.

- 6.4.3 ASUSTeK Computer Inc.

- 6.4.4 Shenzhen Tenda Technology Co., Ltd.

- 6.4.5 AVM GmbH

- 6.4.6 Linksys USA, Inc.

- 6.4.7 D-Link Corporation

- 6.4.8 Belkin International, Inc.

- 6.4.9 Ubiquiti Inc.

- 6.4.10 MikroTikls SIA

- 6.4.11 Synology Inc.

- 6.4.12 TRENDnet, Inc.

- 6.4.13 GL Technologies (Hong Kong) Limited

- 6.4.14 Peplink International Limited

- 6.4.15 DrayTek Corp.

- 6.4.16 Comtrend Corporation

- 6.4.17 Ruijie Networks Co., Ltd.

- 6.4.18 Mercusys Technologies Co., Ltd.

- 6.4.19 Edimax Technology Co., Ltd.

- 6.4.20 Xiaomi Communications Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment