|

시장보고서

상품코드

2063835

약물감시 분야 인공지능(AI) : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)AI In Pharmacovigilance - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

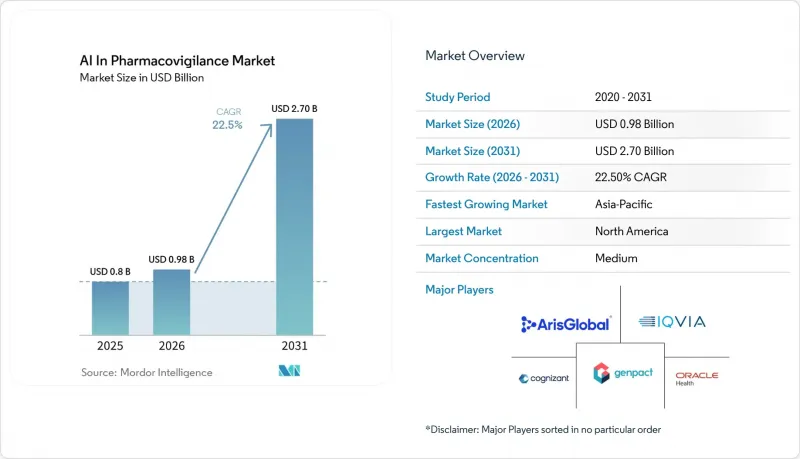

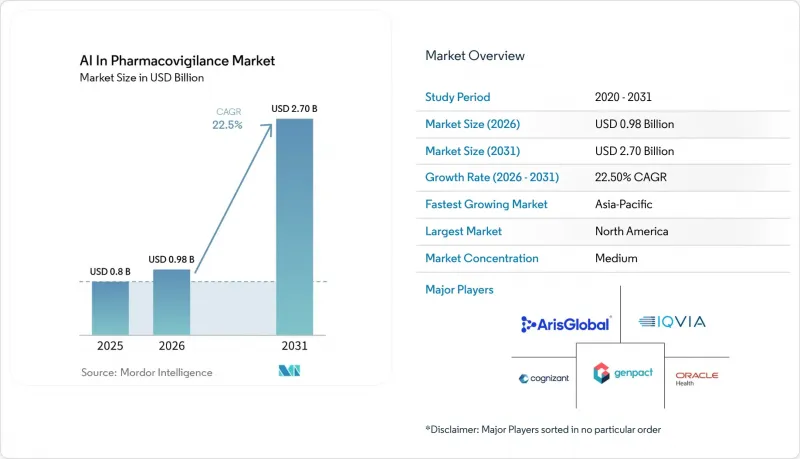

Mordor Intelligence에 의하면, 약물감시 분야 인공지능(AI)시장 규모는 2025년 8억 달러로 평가되었습니다. 2026년에는 9억 8,000만 달러로 확대되어 2031년까지 27억 달러에 이를 것으로 예측되며, 2026-2031년 CAGR은 22.5%를 나타낼 전망입니다.

본 보고서는 구성 요소(소프트웨어 플랫폼, 서비스), 배포 방식(클라우드 기반, On-Premise형), 용도(유해 사건 사례 처리, 신호 감지 및 우선순위 지정), 최종 사용자(제약·바이오기술 기업, CRO, 규제 당국), 지역(북미, 유럽, 아시아태평양, 중동 및 아프리카, 남미)별로 분류되어 있습니다. 시장 전망치는 금액(달러)으로 표시되어 있습니다.

세계의 약물감시 분야 인공지능(AI) 시장 동향 및 인사이트

안전성 데이터의 양과 복잡성 증가

2024년, FAERS에 제출된 ICSR(의약품 안전성 보고)의 연간 건수는 190만 건을 넘어섰으며, 같은 해 EudraVigilance가 접수한 ADR(유해사건 보고)은 170만 건에 달하고, 수동으로 진행되는 분류 업무에 부담이 가중되었습니다. 소셜 미디어 게시물, 전자건강기록(EHR)에서 추출한 데이터, 웨어러블 기기의 피드는 기존의 키워드 필터로는 분석할 수 없는 데이터 레이크를 확대시키고 있습니다. 현재 AI 파이프라인은 구조화된 임상 보고서에서 85-100%의 실체 일치율을 달성하여, 사람이 직접 수정해야 하는 데이터 포인트를 불과 3.5%로 줄였습니다. 새로운 데이터 스트림이 늘어날 때마다 24시간 체제의 규제 보고 기한을 맞추어야 하는 제약사들에게, 약물감시 분야 인공지능(AI) 시장은 점점 더 필수적인 요소가 되고 있습니다.

실시간 모니터링을 위한 규제 당국의 추진

2024년에 시작된 FDA의 EDSTP에서는 AI 시스템을 평가하기 위한 분기별 후원자 회의가 예정되어 있으며, 정책은 사후 보고에서 병행 감독으로 전환되고 있습니다. 대서양을 사이에 둔 유럽에서는 개정된 EU 규정에 따라, 시판 허가 보유자는 디지털 채널을 통해 자발적으로 보고된 이상반응(ADR)을 모니터링하고, 예기치 못한 중증 사례를 15일 이내에 보고해야 할 의무가 있습니다. 소셜 미디어에 매일 올라오는 게시물 수는 5억 건에 육박하며, 그중 약 0.02%가 의약품이나 부작용을 언급하고 있습니다. 이 정도 규모의 데이터를 신속하게 선별할 수 있는 것은 AI뿐이며, 이것이 약물감시 분야에서 AI 시장에 대한 지속적인 투자를 뒷받침하고 있습니다.

데이터 개인정보 보호 및 국경을 넘는 데이터 전송에 관한 규제

다국적 제약 기업들은 GDPR(EU 개인정보보호규정), 중국의 PIPL, 일본의 APPI와 같이 건강 데이터의 해외 저장을 제한하는 규제로 인해 어려움에 직면해 있습니다. 그 결과, 이들 기업은 데이터 세트를 분리하거나 지역 제한적인 클라우드 솔루션을 도입해야 합니다. 또한, 공개 데이터를 활용한 사전 학습 과정에서 의도치 않게 개인정보가 포함될 가능성이 있으므로, LLM(대규모 언어 모델)이 환자를 재식별해 버릴 수 있는 중대한 위험이 존재합니다. 2025년에 실시된 연구에 따르면, 임상 사례에서 환각 발생률이 83%인 것으로 밝혀졌습니다. 규제 준수 비용이 도입을 더욱 지연시키고 있어, 약물감시 분야 인공지능(AI) 시장의 단기적인 성장이 억제되고 있습니다.

부문별 분석

2025년에는 Oracle Argus Safety, ArisGlobal LifeSphere, Veeva Vault Safety 제품군이 주도하면서 플랫폼이 매출의 64.15%를 차지했습니다. 이러한 플랫폼은 데이터 수집, MedDRA 코딩 및 E2B(R3) 제출을 단일 검증된 환경에 통합하여 감사 위험을 최소화합니다. 이러한 통합된 변경 관리 기능은 연간 50만 건 이상의 사례를 처리하는 상위 20개 제약 기업에 특히 매력적입니다. 한편, 약물감시 분야 인공지능(AI) 시장 나머지 부분을 차지하는 서비스는 연평균 성장률(CAGR) 23.45%라는 견실한 성장세를 보이고 있습니다. 이러한 급속한 성장은 주로 사내에 검증 팀을 갖추지 않은 중견 생명공학 기업들이 턴키 방식의 아웃소싱 솔루션을 선택하고 있기 때문인 것으로 보입니다. EU AI법은 AI 모델에 대한 지속적인 모니터링, 정기적인 재훈련, 그리고 설명 가능성에 대한 평가를 의무화하고 있으며, 이로 인해 컨설팅 업무가 안정적인 수익원으로 자리 잡고 있습니다.

2025년에는 클라우드 모델이 약물감시 분야 인공지능(AI) 시장의 71.15%를 차지했으며, On-Premise형 솔루션을 웃도는 연평균 성장률(CAGR) 23.85%를 나타낼 것으로 전망됩니다. SaaS 플랫폼은 버전 관리가 필요 없는 규정 준수 기능을 제공하며, 공급업체가 ICH, MedDRA 및 FDA 양식에 대한 변경 사항을 하룻밤 사이에 적용할 수 있도록 지원합니다. 이 기능을 통해 IQ/OQ/PQ와 관련된 가동 중단 주기가 제거됩니다. 사용자 1인당 연간 약 600달러부터 시작하는 종량제 요금제를 통해 조직은 자본 지출(CapEx)에서 운영 비용(OpEx)으로 전환할 수 있으며, 서버 폐기 비용을 절감할 수 있습니다. 그 결과, IT 유지보수 비용은 On-Premise 환경에 비해 40% 낮아집니다.

지역별 분석

북미는 6,000억 달러 규모의 미국 제약 산업과 ‘센티넬 이니셔티브(Sentinel Initiative)’의 8억 명에 달하는 광범위한 환자 데이터베이스에 힘입어 2025년 매출의 41.56%를 차지했습니다. 이 지역은 클라우드 도입률이 가장 높으며, 의약품 안전 담당 임원의 85%가 2026년에 AI 예산을 증액할 계획인 것으로 나타나, 약물감시 분야 인공지능(AI) 시장에서 북미의 선도적 입지를 공고히 하고 있습니다.

한편, 아시아·태평양 지역은 연평균 성장률(CAGR) 23.35%를 나타낼 것으로 전망됩니다. 이는 전 세계 임상시험의 3분의 1 이상을 차지하며, 그에 비례하는 안전성 관련 업무 부담을 야기하고 있는 중국, 인도, 일본, 한국에 의해 뒷받침된 결과입니다. 2025년 PMDA의 ICH E2B(R3) 적용 및 NMPA의 조화 로드맵을 포함한 규제 조화를 통해, 표준화된 메시지 구조 내에서 국경을 초월한 데이터 흐름이 가능해짐에 따라 SaaS 도입이 촉진되고 있습니다. 인도 및 동남아시아 전역에 걸쳐 클라우드 가용성 구역이 확대됨에 따라, CRO는 하이퍼스케일 GPU 클러스터를 활용하면서도 환자 데이터를 로컬에 저장할 수 있게 되었으며, 이로 인해 해당 지역의 AI 도입이 강화되어 약물감시 분야 인공지능(AI) 시장 규모 성장에 기여하고 있습니다.

남미 및 중동 및 아프리카는 여전히 규모는 작지만, 꾸준한 진전을 보이고 있습니다. 브라질 규제 당국은 약물감시 분야 인공지능(AI) 시장을 위한 샌드박스를 도입했습니다. 또한, 2024년부터 WHO 지정 기관으로 인정받은 아프리카 의약품청은 지역 차원의 시판 후 조사를 조정하고 있으며, 수작업으로 작성하는 스프레드시트를 대체할 수 있는 도구가 필요합니다. 이러한 동향은 공급업체의 파이프라인을 뒷받침하며, 광대역 및 클라우드 인프라의 발전에 따라 약물감시 분야 인공지능(AI) 시장이 지닌 장기적인 잠재력을 부각시키고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.24According to Mordor Intelligence, the aI in pharmacovigilance market size is expected to increase from USD 0.8 billion in 2025 to USD 0.98 billion in 2026 and reach USD 2.70 billion by 2031, growing at a CAGR of 22.5% over 2026-2031.

This report is Segmented by Component (Software Platforms, Services), Deployment Model (Cloud-Based, On-Premise), Application (Adverse Event Case Processing, Signal Detection & Prioritisation), End-User (Pharmaceutical & Biotech, Cros, Regulators), and Geography (North America, Europe, Asia-Pacific, MEA, South America). Market Forecasts are in Value (USD).

Global AI In Pharmacovigilance Market Trends and Insights

Rising Volume and Complexity of Safety Data

Annual ICSR submissions to FAERS topped 1.9 million in 2024, and EudraVigilance received 1.7 million ADRs in the same year, straining manual triage workflows. Social-media posts, EHR extracts, and wearable-device feeds enlarge data lakes that classical keyword filters cannot parse. AI pipelines now achieve 85-100% entity-match rates for structured clinical reports and reduce human correction to just 3.5% of data points. With every extra data stream, the AI in pharmacovigilance market becomes more indispensable to sponsors that must keep pace with twenty-four-hour regulatory reporting clocks.

Regulatory Push for Real-Time Monitoring

The FDA's EDSTP, initiated in 2024, schedules quarterly sponsor meetings to evaluate AI systems, moving policy from retrospective submissions toward concurrent oversight. Across the Atlantic, revised EU rules obligate marketing authorization holders to monitor digital channels for unsolicited ADRs and submit serious unexpected cases within 15 days. Daily social-media output approaches 500 million posts, and roughly 0.02% reference medicines or side effects, a scale only AI can screen promptly, driving recurring investment in the AI in Pharmacovigilance market.

Data Privacy and Cross-Border Transfer Rules

Multinational pharmaceutical companies are facing challenges due to regulations such as GDPR, China's PIPL, and Japan's APPI, which limit the offshore storage of health data. Consequently, these companies must either isolate datasets or implement regional cloud solutions. Additionally, there is a significant risk of LLMs re-identifying patients, as public-data pre-training can unintentionally embed personal information. A 2025 study revealed an 83% hallucination rate in clinical vignettes. Compliance costs are further slowing some deployments, restricting short-term growth in the AI in Pharmacovigilance market.

Other drivers and restraints analyzed in the detailed report include:

- Cost Pressure to Automate Case Processing

- Social-Listening NLP for Patient-Reported Outcomes

- Algorithmic Opacity and Regulatory Defensibility

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, platforms accounted for 64.15% of the revenue, driven by Oracle Argus Safety, ArisGlobal LifeSphere, and Veeva Vault Safety suites. These platforms integrate intake, MedDRA coding, and E2B(R3) submissions into a single validated environment, minimizing audit risks. This unified change control feature is particularly appealing to top-20 pharmaceutical firms, each handling over 500,000 cases annually. Meanwhile, services, which make up the remaining portion of the AI in Pharmacovigilance market, are witnessing robust growth at a 23.45% CAGR. This surge is largely due to mid-tier biotech firms, lacking in-house validation teams, opting for turnkey outsourcing solutions. The EU AI Act mandates continuous AI model monitoring, periodic retraining, and explainability assessments, transforming consulting hours into a consistent revenue stream.

In 2025, cloud models dominated the AI in Pharmacovigilance market with a 71.15% share and are projected to grow at a 23.85% CAGR, outpacing on-premise solutions. SaaS platforms offer versionless compliance, allowing vendors to implement overnight changes in ICH, MedDRA, and FDA forms. This capability eliminates downtime cycles associated with IQ/OQ/PQ. With pay-per-user pricing starting around USD 600 annually per user, organizations can shift from capital expenditures (CapEx) to operational expenditures (OpEx), avoiding server decommissioning costs. This results in IT maintenance bills that are 40% lower than those of on-premise setups.

Geography Analysis

North America generated 41.56% of 2025 revenue, driven by the United States' USD 600 billion pharmaceutical economy and the extensive 800 million-patient database of the Sentinel Initiative. The region demonstrates the highest cloud adoption, with 85% of drug-safety executives planning to increase AI budgets in 2026, reinforcing North America's leadership in the AI in Pharmacovigilance market.

Asia-Pacific, however, is projected to grow at a 23.35% CAGR, supported by China, India, Japan, and South Korea, which collectively host more than one-third of global clinical trials, creating proportional safety workloads. Regulatory harmonization, including PMDA's ICH E2B(R3) activation in 2025 and NMPA's alignment roadmap, enables cross-border data flow within standardized message structures, encouraging SaaS adoption. The expansion of cloud availability zones across India and Southeast Asia allows CROs to store patient data locally while utilizing hyperscale GPU clusters, enhancing regional AI deployments and contributing to the growth of the AI in the Pharmacovigilance market size.

South America and the Middle East & Africa remain smaller but show targeted progress. Brazil's regulator has introduced a sandbox for AI-enabled vigilance, and the African Medicines Agency, recognized as a WHO-Listed Authority since 2024, is coordinating regional post-market surveillance, necessitating tools beyond manual spreadsheets. These developments sustain vendor pipelines and highlight the long-term potential of the AI in Pharmacovigilance market as broadband and cloud infrastructure continue to advance.

- AB Cube

- Accenture

- Anju Software

- Aris Global

- Capgemini

- Clario (formerly BioClinica)

- Cloudbyz

- Cognizant

- Ennov

- Genpact

- IBM Merative

- IQVIA

- Oracle

- Parexel International

- Sparta Systems (Honeywell)

- Tata Consultancy Services

- Thermo Fisher Scientific Inc. (PPD)

- United BioSource

- Wipro

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Volume & Complexity of Safety Data

- 4.2.2 Regulatory Push for Real-Time Monitoring

- 4.2.3 Cost Pressure to Automate Case Processing

- 4.2.4 Social-Listening NLP for Patient-Reported Outcomes

- 4.2.5 Foundation Models for Rare-Disease Signal Detection

- 4.2.6 Federated Learning Agreements with EHR Exchanges

- 4.3 Market Restraints

- 4.3.1 Data-Privacy / Cross-Border Transfer Rules

- 4.3.2 Scarcity of Labeled Safety Datasets

- 4.3.3 Algorithmic Opacity Vs Regulatory Defensibility

- 4.3.4 High Compute Cost of Genai Inference

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Component

- 5.1.1 Software Platforms

- 5.1.2 Services

- 5.2 By Deployment Model

- 5.2.1 Cloud-Based

- 5.2.2 On-Premise

- 5.3 By Application

- 5.3.1 Adverse Event Case Processing

- 5.3.2 Signal Detection & Prioritisation

- 5.3.3 Risk Management & Mitigation

- 5.3.4 Regulatory Reporting & Submissions

- 5.4 By End User

- 5.4.1 Pharmaceutical & Biotech Companies

- 5.4.2 Contract Research Organizations (CROs)

- 5.4.3 Medical Device Manufacturers

- 5.4.4 Regulatory Authorities

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East & Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 AB Cube

- 6.3.2 Accenture

- 6.3.3 Anju Software

- 6.3.4 ArisGlobal

- 6.3.5 Capgemini

- 6.3.6 Clario (formerly BioClinica)

- 6.3.7 Cloudbyz

- 6.3.8 Cognizant

- 6.3.9 Ennov

- 6.3.10 Genpact

- 6.3.11 IBM Merative

- 6.3.12 IQVIA

- 6.3.13 Oracle

- 6.3.14 Parexel

- 6.3.15 Sparta Systems (Honeywell)

- 6.3.16 Tata Consultancy Services

- 6.3.17 Thermo Fisher Scientific Inc. (PPD)

- 6.3.18 United BioSource Corporation

- 6.3.19 Wipro

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment