|

시장보고서

상품코드

2063836

시판 후 감시 소프트웨어 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Postmarketing Surveillance Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

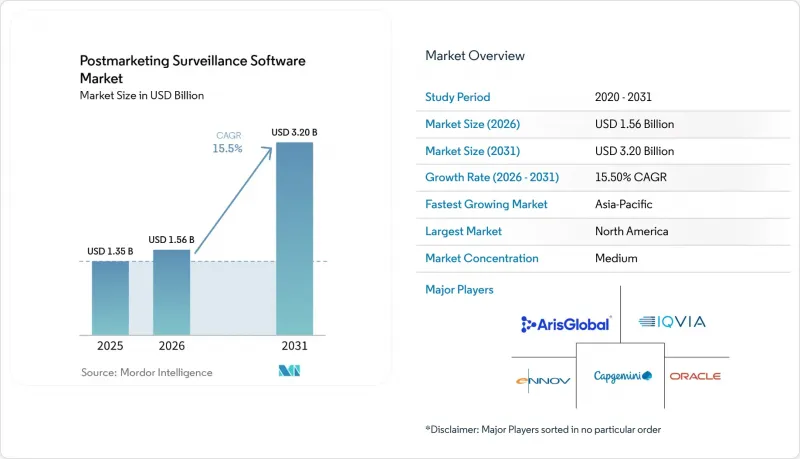

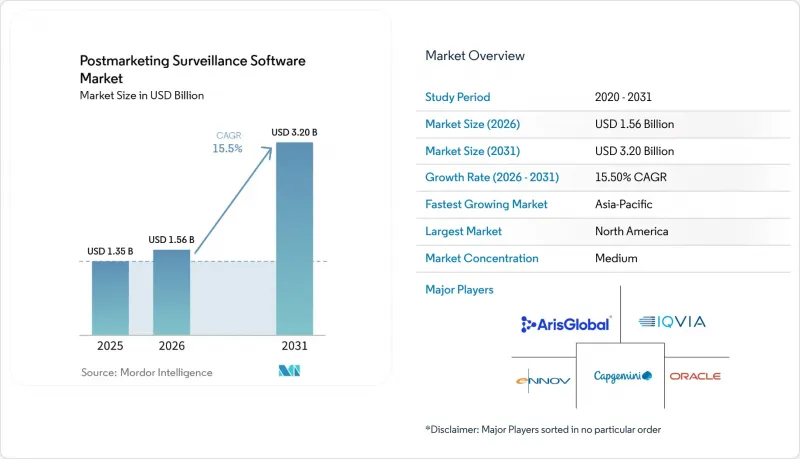

Mordor Intelligence에 의하면, 시판 후 감시 소프트웨어 시장 규모는 2025년 13억 5,000만 달러로 평가되었습니다. 2026년에는 15억 6,000만 달러로 확대되어 2031년까지 32억 달러에 이를 것으로 예측되며, 2026-2031년 CAGR은 15.5%를 나타낼 전망입니다.

본 보고서는 구성 요소(소프트웨어 플랫폼, 서비스), 배포 방식(On-Premise, 클라우드 기반), 최종 사용자(제약 회사, 생명공학 기업, 의료기기 제조업체, CRO 및 PV 서비스 제공업체, 규제 당국) 및 지역(북미, 유럽, 아시아태평양, 기타)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 시판 후 감시 소프트웨어 시장 동향 및 인사이트

이용 가능한 실세계 데이터의 양 증가

현재 조사 플랫폼은 병원, 보험사, 환자로부터 직접 데이터 스트림을 수신하고 있으며, 기존의 자발적 보고를 넘어 분석 가능한 이상반응 신호의 양이 크게 증가하고 있습니다. 많은 신청 건에서 식별 가능한 환자 데이터에 대한 요건을 완화한 FDA의 2025년판 ‘실세계 증거(Real-World Evidence)’ 지침에 따라, 일상적인 안전성 분석에서 전국적인 등록부 및 청구 데이터베이스를 활용할 수 있게 되었습니다. 주요 벤더들은 전자건강기록(EHR) 네트워크에서 구조화 데이터와 비구조화 데이터를 거의 실시간으로 수집하고 정규화하는 자동화된 추출·변환·로드(ETL) 파이프라인을 도입하고 있습니다. 한 중견 바이오의약품 기업은 이처럼 더 풍부한 데이터 소스를 활용하는 데 따른 이점을 강조하며, 청구 데이터 피드를 자사 플랫폼에 통합한 결과 사례 처리 시간이 60% 단축되었다고 보고했습니다. 그러나 웨어러블 기기나 레지스트리 정보에는 투여량이나 투여 시점에 대한 세부 사항에서 불일치가 자주 발견되기 때문에 데이터의 완전성은 여전히 과제로 남아 있습니다. ISO IDMP를 둘러싼 다지역적 노력은 코딩의 통일성을 높이는 것을 목표로 하고 있지만, 완전한 조화가 이루어지는 것은 2028년 이후가 될 것으로 예측됩니다.

AI를 활용한 신호 감지로 속도와 정확도 향상

머신러닝 모델은 기존의 빈도론적 및 베이즈적 불균형 통계를 능가하는 성능을 보여주고 있으며, 동료 심사를 거친 연구에서 AUROC 값이 0.97에 육박하는 결과를 달성했습니다. 사노피가 이러한 모델을 도입한 결과, 민감도 85%, 특이도 75%를 달성했으며, 신호 식별까지 걸리는 기간을 6개월 단축했습니다. LifeSphere Advanced Signals와 같은 플랫폼에는 교란 요인을 자동으로 보정하는 기능이 내장되어 있어, 위양성으로 인한 업무 부담을 40-50% 줄이고 있습니다. 이에 따라 규제 당국도 내부 시범 프로젝트를 시작했습니다. 예를 들어, FDA의 ‘Project Elsa’에서는 지도 학습 기반 트랜스포머를 활용해 서술문을 요약하고, 인간의 감독을 유지하면서 중복될 가능성이 있는 사례에 플래그를 표시하고 있습니다. 이러한 발전으로 심사위원의 생산성이 크게 향상되어, 의사들은 데이터 관리 업무가 아닌 인과관계 평가에 집중할 수 있게 됩니다.

분절화된 세계의 데이터 표준이 상호 운용성을 저해하고 있습니다.

ICH 준수를 위한 노력에도 불구하고, 기술 필드, 타임라인 요건 및 관리 용어집에서 지역 간 불일치를 완전히 해소하지는 못했습니다. 유럽에서의 ISO IDMP 도입은 아시아태평양보다 훨씬 더 진전되어 있으며, 전 세계의 후원사는 데이터 요소를 다양한 지역 형식에 맞추어 조정해야 합니다. 또한, MedDRA의 반기별 업데이트에 따라 버전 관리도 수행해야 합니다. 이러한 중복 현상은 검증 리소스에 부담을 주고, 시스템 업그레이드 기간을 연장시키고 있습니다. 이 과제는 현지 규제 당국이 ICH 지침을 넘어서는 국가별 고유 요소를 도입할 경우 더욱 복잡해집니다. 이러한 채용상의 격차가 해소될 때까지는 기업이 이중 검증 워크플로우를 지원하기 위해 추가 자원을 배정해야 합니다.

부문별 분석

2025년에는 소프트웨어 플랫폼이 총 지출의 64.15%를 차지할 것으로 전망됩니다. 이러한 추세는 기업들이 사례 접수, 규제 당국에 대한 보고, 분석 기능을 통합한 솔루션을 선호하고 있음을 보여줍니다. 업계의 진화를 상징하듯, Oracle의 ‘Safety One Argus’ 출시는 벤더의 기술적 진보를 여실히 보여주고 있으며, 구조화된 사례 데이터의 90%를 자율적으로 추출하는 머신러닝 추출 기능을 탑재함으로써 수작업에 의한 재입력의 필요성을 없앴습니다. 서비스 부문이 나머지 시장 점유율을 차지하고 있지만, 연평균 성장률(CAGR) 15.95%를 나타낼 것으로 예측되며, 소프트웨어 플랫폼을 앞지르는 기세를 보이고 있습니다. 이러한 변화는 사내 팀을 유지하는 것보다 변동비형 운영 모델을 선호하는 후원사의 의향에서 비롯된 것입니다. 또한, 아웃소싱의 확산은 업그레이드를 가속화할 뿐만 아니라, 서비스 제공업체가 여러 고객에게 동시에 새로운 AI 모듈을 배포할 수 있게 하여 검증 비용을 효과적으로 분산시킵니다.

지역별 분석

2025년, 북미는 시판 후 감시 소프트웨어 시장의 42.65%를 차지했습니다. 해당 지역은 FDA가 AI 및 클라우드 검증 프레임워크에 대해 조기에 승인함에 따라 선구자로서의 우위를 활용하고 있습니다. 또한, 미국의 주요 기업 소프트웨어 공급업체와 지리적으로 인접해 있다는 점이 시장 내 입지를 강화하고 있습니다. 국내 보안 소프트웨어 계약은 특히 여러 해에 걸친 관리형 서비스와 결합된 경우, 연간 1,000만 달러를 초과하는 경우가 많아 북미의 높은 수요를 반영하고 있습니다.

유럽은 EMA의 EudraVigilance 생태계에 힘입어 구축된 대규모 도입 기반에 힘입어, 북미에 근소한 차이로 뒤를 따르고 있습니다. 일반 데이터 보호 규정(GDPR(EU 개인정보보호규정))의 엄격한 요건으로 인해 규정 준수 과정이 더욱 복잡해지고 있으며, 상세한 감사 추적 기록과 현지화된 데이터 저장 위치에 대한 수요가 증가하고 있습니다. 많은 다국적 후원사들은 FDA 규정을 준수하도록 설계된 데이터베이스와 EMA 기준에 맞추어 조정된 데이터베이스, 이 두 가지 데이터베이스를 별도로 운영하고 있습니다. 두 기관이 매일 데이터 공개 일정을 조정하고 있기 때문에 이러한 이중 접근 방식으로 인해 빈번한 시스템 업그레이드가 필요하게 되었습니다.

아시아태평양은 연평균 성장률(CAGR) 16.45%를 기록하며 가장 빠르게 성장하고 있는 지역입니다. 일본, 중국, 인도 등의 국가들은 ICH 기준 준수를 추진하고 있습니다. 중국은 국제적인 임상시험을 유치하기 위해 국가 의약품 이상반응 감시 시스템을 업그레이드하고 있으며, 이에 따라 현지 후원사들은 2개 국어로 보고할 수 있는 기능을 갖춘 ICH 준수 안전성 관리 시스템을 도입하도록 권장받고 있습니다. 인도가 2024년에 AI를 활용한 ADR 플랫폼을 출범시킨 것은 디지털 감시에 대한 노력을 보여주는 것이지만, 그 성공 여부는 병원이 전자차트 시스템을 도입할지 여부에 달려 있습니다. 동남아시아의 소규모 시장은 대개 싱가포르에 위치한 통합 아웃소싱 허브에 의존하고 있으며, 그곳에서 서비스 제공업체가 아세안(ASEAN) 국가 전체의 안전 관련 의무를 관리하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.24According to Mordor Intelligence, the postmarketing surveillance software market size is expected to increase from USD 1.35 billion in 2025 to USD 1.56 billion in 2026 and reach USD 3.20 billion by 2031, growing at a CAGR of 15.5% over 2026-2031.

This report is Segmented by Component (Software Platform, Services), Deployment Mode (On-Premises, Cloud-Based), End-User (Pharmaceutical Companies, Biotechnology Firms, Medical Device Manufacturers, Cros & PV Service Providers, Regulatory Agencies), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Postmarketing Surveillance Software Market Trends and Insights

Increasing Volume of Real-World Data Availability

Surveillance platforms now directly receive data streams from hospitals, payers, and patients, significantly increasing the volume of analyzable adverse-event signals beyond traditional spontaneous reports. The FDA's 2025 guidance on real-world evidence, which eased the requirement for identifiable patient data in many submissions, has enabled the use of national registries and claims databases for routine safety analyses. Leading vendors have implemented automated extract-transform-load pipelines, pulling and normalizing both structured and unstructured records from electronic health-record networks in near real-time. A mid-cap biopharma highlighted the operational benefits of these richer data sources, reporting a 60% reduction in case-touch time after integrating claims feeds into its platform. However, data completeness remains a challenge, as wearable and registry information often include inconsistent dosage or timing details. While multiregional initiatives around ISO IDMP aim to enhance coding uniformity, full alignment is not expected before 2028.

AI-Enabled Signal Detection Improves Speed and Accuracy

Machine-learning models have outperformed traditional frequentist and Bayesian disproportionality statistics, achieving AUROC values nearing 0.97 in peer-reviewed studies. Sanofi's implementation of these models achieved 85% sensitivity and 75% specificity, reducing its signal-identification timeline by six months. Platforms like LifeSphere Advanced Signals have incorporated automated confounder adjustments, leading to a 40-50% reduction in false-positive workloads. In response, regulators have initiated internal pilots; for instance, FDA's Project Elsa uses supervised transformers to summarize narrative text, flagging potential case duplicates while maintaining human oversight. This advancement significantly enhances reviewer productivity, enabling physicians to focus on causality assessments rather than data management tasks.

Fragmented Global Data Standards Hinder Interoperability

Efforts to achieve ICH alignment have not fully resolved regional discrepancies in narrative fields, timeline requirements, and controlled terminologies. Europe's ISO IDMP implementation is significantly ahead of the Asia-Pacific region, requiring global sponsors to adapt data elements to various regional formats. Additionally, they must manage version control due to MedDRA's biannual updates. This duplication places a strain on validation resources and extends system upgrade timelines. The challenge is further compounded when local regulators introduce country-specific elements that go beyond ICH guidance. Until these adoption gaps are addressed, companies will need to allocate additional resources to support dual validation workflows.

Other drivers and restraints analyzed in the detailed report include:

- Regulatory Mandates for Proactive Pharmacovigilance

- Growing Complexity of Combination Products

- High Capital Investment Costs for Legacy IT Stacks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, software platforms accounting for 64.15% of total expenditures. This trend underscores companies' preference for integrated solutions, combining case intake, regulatory reporting, and analytics. Highlighting the industry's evolution, Oracle's Safety One Argus release demonstrates vendors' advancements, embedding machine-learning extractors that autonomously capture 90% of structured case data, eliminating the need for manual re-keying. While services took the remaining market share, they are poised to outpace software platforms, projecting a robust 15.95% CAGR. This shift is driven by sponsors' preference for variable-cost operating models over maintaining in-house teams. Furthermore, the momentum in outsourcing not only accelerates upgrades but also allows service providers to deploy new AI modules across multiple clients simultaneously, effectively distributing validation costs.

Geography Analysis

In 2025, North America captured 42.65% of the postmarketing surveillance software market. The region leverages a first-mover advantage due to early FDA endorsements of AI and cloud validation frameworks. Additionally, its proximity to leading enterprise software vendors in the United States strengthens its market position. Domestic safety-software contracts often exceed annual values of USD 10 million, particularly when bundled with multi-year managed services, reflecting the substantial demand in North America.

Europe follows closely, supported by a significant installed base anchored in the EMA's EudraVigilance ecosystem. The stringent requirements of the General Data Protection Regulation increase compliance complexity, driving demand for detailed audit trails and localized data residency. Many multinational sponsors maintain dual databases-one designed for FDA regulations and another tailored to EMA standards. This dual approach drives frequent system upgrades as both agencies align their daily data-release schedules.

Asia-Pacific is the fastest-growing region, with a 16.45% CAGR. Countries such as Japan, China, and India are aligning with ICH standards. China is upgrading its National Adverse Drug Reaction Monitoring System to attract international trials, prompting local sponsors to adopt ICH-compliant safety systems with bilingual reporting capabilities. India's launch of an AI-driven ADR platform in 2024 demonstrates its commitment to digital surveillance, though its success depends on hospitals adopting electronic medical record systems. Smaller Southeast Asian markets typically rely on centralized outsourcing hubs in Singapore, where service providers manage safety obligations across ASEAN nations.

- AB Cube

- Aris Global

- Axpharma

- Bioclinica (Clario)

- BioPharma PV

- Capgemini

- Ennov

- EXTEDO

- Indegene

- IQVIA

- Omniscient Safety

- Oracle

- PharmInvent

- RXLogix

- Safety First Consulting

- SAS Institute

- Sparta Systems (Honeywell)

- TCS ADD Safety Platform

- United BioSource (UBC)

- Vigilare International

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Volume of Real-World Data Availability

- 4.2.2 AI-Enabled Signal Detection Improves Speed & Accuracy

- 4.2.3 Regulatory Mandates for Proactive Pharmacovigilance

- 4.2.4 Growing Complexity of Combination Products

- 4.2.5 Expansion of Post-Authorization Safety Studies in Emerging Markets

- 4.2.6 Decentralized Clinical Trial Models Feeding Post-Market Platforms

- 4.3 Market Restraints

- 4.3.1 Fragmented Global Data Standards Hinder Interoperability

- 4.3.2 High Upfront Integration Costs for Legacy IT Stacks

- 4.3.3 Shortage of Qualified Safety Informatics Personnel

- 4.3.4 Cyber-Security Concerns Over Cloud-Hosted Safety Data

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Component

- 5.1.1 Software Platform

- 5.1.2 Services

- 5.2 By Deployment Mode

- 5.2.1 On-premises

- 5.2.2 Cloud-based

- 5.3 By End-user

- 5.3.1 Pharmaceutical Companies

- 5.3.2 Biotechnology Firms

- 5.3.3 Medical Device Manufacturers

- 5.3.4 CROs & PV Service Providers

- 5.3.5 Regulatory Agencies

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 Australia

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East & Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 AB Cube

- 6.3.2 ArisGlobal

- 6.3.3 Axpharma

- 6.3.4 Bioclinica (Clario)

- 6.3.5 BioPharma PV

- 6.3.6 Capgemini

- 6.3.7 Ennov

- 6.3.8 EXTEDO

- 6.3.9 Indegene

- 6.3.10 IQVIA

- 6.3.11 Omniscient Safety

- 6.3.12 Oracle

- 6.3.13 PharmInvent

- 6.3.14 RXLogix

- 6.3.15 Safety First Consulting

- 6.3.16 SAS Institute

- 6.3.17 Sparta Systems (Honeywell)

- 6.3.18 TCS ADD Safety Platform

- 6.3.19 United BioSource (UBC)

- 6.3.20 Vigilare International

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment