|

시장보고서

상품코드

2065602

임상 분석 플랫폼 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Clinical Analytics Platforms - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

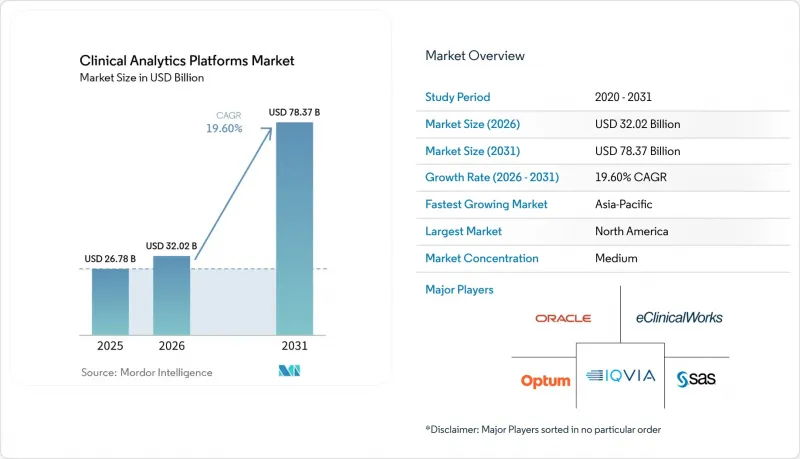

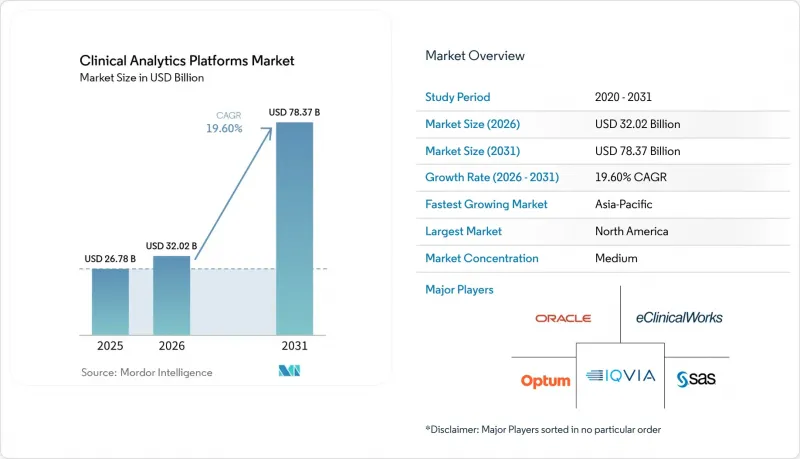

Mordor Intelligence에 의하면, 임상 분석 플랫폼 시장 규모는 2025년 267억 8,000만 달러로 평가되었고, 2026년에는 320억 2,000만 달러로 확대될 전망이며, 2026-2031년 CAGR 19.60%로 성장을 지속하여, 2031년에는 783억 7,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 제공 형태별(원시 데이터, 소프트웨어, 플랫폼), 도입 모델별(클라우드 기반, 온프레미스형, 하이브리드형), 데이터 소스별(전자건강기록(EHR), 보험 청구 데이터, 임상시험, 실세계 데이터(RWE), 영상 진단, 검사 및 병리, 기타), 이용 사례별(헬스케어, 생명과학), 최종 사용자별(의료 제공업체, 보험사, 생명과학, 기타), 지역별(북미, 유럽, 아시아태평양, 중동 및 아프리카, 남미)로 분류되어 있습니다. 시장 규모 예측은 달러 기준으로 이루어집니다.

세계의 임상 분석 플랫폼 시장 동향 및 인사이트

가치 기반 의료와 성과 연계형 보상

CMS는 2026년 7월 5일, 서비스 양이 아닌 만성 질환 관리 분야에서 측정 가능한 성과에 따라 보험 급여를 연계하는 10년간의 자발적 이니셔티브인 ‘ACCESS 모델’을 도입했습니다. 2030년까지 CMS는 모든 기존 메디케어 수급자를 책임의료(Accountable Care) 체계에 임베디드하는 것을 목표로 하고 있으며, 이에 따라 성과 모니터링, 위험 계층화, 조기 개입을 가능하게 하는 분석 도구에 대한 수요가 증가하고 있습니다. 이러한 변화로 인해, 치료 과정에서 위험을 적극적으로 관리하는 조직이 보상을 받게 되었으며, 임상 분석 플랫폼은 보상 절차에 있어 필수적인 요소로서의 위상을 확립하고 있습니다. 집단 건강 분석과 실용적인 워크플로를 결합한 공급업체는 사후 보고에만 초점을 맞추고 있는 공급업체보다 유리한 입장에 있습니다.

클라우드 및 AI/ML을 통한 의료 데이터 인프라의 현대화

의료 시스템에서는 분산된 분석 기능을 통합된 데이터 레이어를 통해 운영 분석, 임상 AI, 조사를 지원하는 클라우드 네이티브 플랫폼으로 통합하고 있습니다. UNC Health의 Microsoft Fabric 도입은 데이터에서 인사이트를 도출하는 과정을 효율화하려는 노력을 상징합니다. 클라우드를 통한 현대화는 엔지니어링상의 병목 현상을 완화하고, 모델 개발 및 워크플로우 배포를 가속화합니다. IQVIA가 2026년 3월, 100건 이상의 AI 특허와 150개의 지능형 에이전트를 기반으로 ‘IQVIA.ai’를 출시한 것은 AI가 임상 워크플로우에 빠르게 통합되고 있음을 여실히 보여줍니다. 엄선된 임상적 관련성이 높은 데이터를 갖춘 확장 가능한 인프라를 제공하는 공급업체는 경쟁 우위를 확보할 가능성이 높을 것입니다.

데이터 개인정보 보호, 보안 및 거버넌스에 따른 부담

임상 AI 워크플로에서는 수집, 추론, 저장, 모니터링의 각 단계에서 기밀성이 높은 건강 데이터를 관리하지만, 이러한 처리 과정은 기존 규정 준수 모델의 역량을 초과하는 경우가 종종 있습니다. 이 과제는 플랫폼이 의료 제공업체, 보험사, 생명과학 기업 등 각각 고유한 관리 체계와 승인 절차를 갖춘 조직들 간에 운영될 경우 더욱 심각해집니다. 임상 분석 플랫폼 시장은 연방형 분석, 현지화된 처리, 엄격한 감사 가능성 등 개인정보 보호를 중시하는 아키텍처를 채택해야 한다는 강력한 압력을 받고 있습니다. OMOP CDM을 기반으로 연방형 설계를 채택한 일본의 NTT 정밀의학 플랫폼은 환자 데이터를 이동시키지 않고도 분석적 가치를 실현할 수 있음을 보여주고 있으며, 이는 개인정보 보호가 중시되는 지역에서 매우 중요합니다.

부문별 분석

2025년, 임상 분석 플랫폼 시장에서 원시 데이터(Raw Data)의 점유율은 37.10%를 차지했으며, 데이터 수집, 익명화, 조화화 및 연구용으로 활용 가능한 자산 구축에 대한 막대한 투자가 주목받고 있습니다. 이 소프트웨어는 여전히 중요하며, 임상 의사결정 지원, 집단 건강 관리 및 수익 주기 분석을 위한 모듈형 도구를 제공합니다. 플랫폼은 가장 빠르게 성장하고 있는 부문으로, 2026-2031년 연평균 성장률(CAGR) 22.70%를 나타낼 것으로 전망됩니다. 이는 데이터 수집, 거버넌스, 분석, AI 추론을 통합한 통합 환경으로의 전환이 원동력이 되고 있습니다.

공급업체의 전략도 이러한 변화를 반영하고 있습니다. IQVIA는 독자적인 헬스케어 데이터를 활용하고, AI 지원 플랫폼 및 워크플로우 도구를 확대함으로써 2025년에 163억 달러의 매출을 기록했습니다. Flatiron Health가 2026년에 출시한 다중 에이전트 적응형 분석 플랫폼 ‘Telescope’는 벤더들이 AI 네이티브 인터페이스를 통해 데이터를 수익화하고 인프라 운영을 간소화하고 있음을 보여줍니다.

2025년 매출액 중 온프레미스 구축이 60.95%를 차지했습니다. 이는 조직의 데이터 주권, 지금까지의 인프라 투자, 그리고 PHI(개인 건강 정보)에 대한 엄격한 취급 방침이 배경에 있습니다. 많은 통합 의료 네트워크에서는 레거시 프로세스와 관련된 기밀성이 높은 워크로드를 처리하기 위해 사설 환경에 의존하고 있습니다. 그러나 투자가 확장 가능하고 AI를 지원하는 인프라로 전환됨에 따라, 클라우드 기반 도입은 가장 빠르게 성장하는 부문으로 부상했으며, 2026년부터 2031년까지 연평균 성장률(CAGR) 22.55%로 성장을 지속하고, 있습니다.

Innovaccer가 2026년에 Snowflake와 체결한 파트너십은 클라우드 도입의 확대를 여실히 보여주는 것으로, Gravity 플랫폼과 Snowflake의 AI Data Cloud를 연동하여 엔터프라이즈급 AI 워크플로우를 지원합니다. 하이브리드 전략은 레거시 시스템에 대한 현지 제어와 클라우드 기반 분석 및 AI의 확장을 조화롭게 균형 잡으려는 조직에게 여전히 필수적입니다. 특히, 데이터의 소재지나 주권적 AI 인프라의 우선순위가 의사결정에 영향을 미치는 유럽 및 아시아태평양 지역 일부에서는 그 중요성이 두드러집니다.

지역별 분석

2025년, 북미는 임상 분석 플랫폼 시장의 41.12%를 차지했으며, 기업용 임상 분석 도입 측면에서 가장 규모가 크고 성숙한 지역이 되었습니다. 미국은 가치 기반 의료, 전자건강기록(EHR)의 광범위한 보급, 그리고 보험사와 의료 제공업체 간의 데이터 교환 요건에 힘입어 해당 지역의 성장을 주도하고 있습니다. 또한, CMS-0057-F를 통해 청구, 사전 승인, 의료 제공업체 기록에 걸친 데이터 흐름을 강화하기 위한 FHIR 기반 API의 도입이 촉진되었습니다. 캐나다는 주 차원의 의료 데이터 이니셔티브를 통해 기여하고 있으며, 멕시코는 초기 단계에 있지만 대도시권 병원 시스템 내에서 진전을 보이고 있습니다.

아시아태평양은 임상 분석 플랫폼 시장에서 가장 빠르게 성장하고 있는 지역으로, 2031년까지 연평균 성장률(CAGR)이 20.20%를 나타낼 것으로 전망됩니다. 이러한 성장은 의료의 디지털화, 임상시험 활동의 확대, 그리고 구조화된 의료 데이터 환경에 대한 정부의 집중에 힘입어 이루어지고 있습니다. 2026년 1월, 일본의 후지쯔와 JMDC는 익명화된 DPC 병원 데이터와 보험사 기록을 연계하여 2,000만 건의 기록을 포괄함으로써, 제약 업계 및 공공 부문을 대상으로 한 환자 여정 분석을 강화했습니다. 중국에서는 그 규모가 급속히 확대되고 있으며, MSTATA와 같은 플랫폼이 2024년 이후 1,200편 이상의 SCI 논문을 지원한 것은 병원 네트워크 전반에 걸친 광범위한 도입을 반영하고 있습니다.

유럽은 여전히 기술적으로 선진적이지만, 개인정보 보호, 주권, 규제 인프라의 영향을 받고 있습니다. 독일의 NUKLEUS 플랫폼은 2025년 7월에 확장되어, 적응형 임상 플랫폼 연구를 지원하는 동시에 대학병원 전체의 법정 건강보험 데이터 및 암 등록 데이터를 활용할 수 있게 되었습니다. 중동 및 아프리카은 주권에 기반한 AI 의료 분야 투자를 통해 발전하고 있으며, 2025년 5월에 발표된 Oracle, 클리블랜드 클리닉, G42간의 제휴가 그 대표적인 사례입니다. 남미는 브라질과 아르헨티나에서 디지털화가 진행되고 있음에도 불구하고, 여전히 지역 시장으로는 가장 작은 규모에 머물러 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

LSH 26.06.24According to Mordor Intelligence, the clinical analytics platforms market size is expected to grow from USD 26.78 billion in 2025 to USD 32.02 billion in 2026 and is forecast to reach USD 78.37 billion by 2031 at 19.60% CAGR over 2026-2031.

This report is Segmented by Offering (Raw Data, Software, Platform), Deployment Model (Cloud-Based, On-Premises, Hybrid), Data Source (EHR, Claims, Clinical Trials, RWE, Imaging, Lab & Pathology, Others), Use Case (Healthcare, Life Sciences), End User (Providers, Payers, Life Sciences and Others), and Geography (North America, Europe, Asia-Pacific, MEA, South America). Forecasts in Value (USD).

Global Clinical Analytics Platforms Market Trends and Insights

Value-Based Care and Outcome-Linked Reimbursement

CMS introduced the ACCESS Model on July 5, 2026, a 10-year voluntary initiative linking reimbursements to measurable outcomes in chronic disease management rather than service volume. By 2030, CMS aims to place all Traditional Medicare beneficiaries in accountable care relationships, driving demand for analytics to monitor performance, stratify risk, and enable early intervention. This shift rewards organizations that proactively manage risks during care, positioning clinical analytics platforms as integral to reimbursement processes. Vendors combining population health analytics with actionable workflows are better positioned than those focusing solely on retrospective reporting.

Cloud and AI/ML Modernization of Healthcare Data Infrastructure

Healthcare systems are consolidating fragmented analytics into cloud-native platforms that support operational analytics, clinical AI, and research from a unified data layer. UNC Health's adoption of Microsoft Fabric highlights efforts to streamline data-to-insight processes. Cloud modernization reduces engineering bottlenecks, accelerating model development and workflow deployment. IQVIA's launch of IQVIA.ai in March 2026, supported by over 100 AI patents and 150 intelligent agents, underscores the rapid integration of AI into clinical workflows. Vendors offering scalable infrastructure with curated, clinically relevant data are likely to gain a competitive edge.

Data Privacy, Security, and Governance Burden

Clinical AI workflows manage sensitive health data across ingestion, inference, storage, and monitoring, often exceeding the capabilities of traditional compliance models. This challenge grows when platforms operate across providers, payers, and life sciences, each with unique controls and approval processes. The clinical analytics platforms market is under pressure to adopt privacy-focused architectures like federated analytics, localized processing, and strict auditability. Japan's NTT Precision Medicine Platform, built on OMOP CDM with a federated design, demonstrates how analytical value can be achieved without moving patient data, which is critical in privacy-sensitive regions.

Other drivers and restraints analyzed in the detailed report include:

- CMS Interoperability and Prior-Authorization API Mandates

- Regulatory Openness to Real-World Evidence and Precision Medicine

- Data Quality, Standardization, and Legacy Interoperability

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, Raw Data held a 37.10% share of the clinical analytics platforms market, highlighting significant investments in data acquisition, de-identification, harmonization, and creating research-ready assets. Software remains critical, offering modular tools for clinical decision support, population health, and revenue cycle analytics. Platforms are the fastest-growing segment, with a 22.70% CAGR during 2026-2031, driven by the shift toward unified environments integrating ingestion, governance, analytics, and AI inferencing.

Vendor strategies reflect this shift. IQVIA reported USD 16.3 billion in revenue in 2025, leveraging proprietary healthcare data and advancing AI-enabled platforms and workflow tools. Flatiron Health's 2026 launch of Telescope, a multi-agent adaptive analytics platform, demonstrates how vendors monetize data through AI-native interfaces, simplifying infrastructure navigation.

On-premises deployment accounted for 60.95% of revenue in 2025, driven by institutional data sovereignty, prior infrastructure investments, and strict PHI handling preferences. Many integrated delivery networks rely on private environments for sensitive workloads tied to legacy processes. However, cloud-based deployment is the fastest-growing segment, with a 22.55% CAGR during 2026-2031, as investments shift to scalable AI-ready infrastructure.

Innovaccer's 2026 partnership with Snowflake highlights rising cloud adoption, linking the Gravity platform with Snowflake's AI Data Cloud to support enterprise-scale AI workflows. Hybrid deployment remains vital for organizations balancing local control over legacy systems with cloud-based analytics and AI expansion, especially in Europe and parts of Asia-Pacific, where data residency and sovereign AI infrastructure priorities influence decisions.

Geography Analysis

In 2025, North America accounted for 41.12% of the clinical analytics platforms market, making it the largest and most mature region for enterprise clinical analytics adoption. The U.S. drives growth in the region due to value-based care, extensive EHR penetration, and payer-provider data exchange requirements. Additionally, CMS-0057-F encouraged the adoption of FHIR-based APIs to enhance data flow across claims, prior authorizations, and provider records. Canada contributes through provincial health data initiatives, while Mexico, though in earlier stages, is advancing within large urban hospital systems.

Asia-Pacific is the fastest-growing region in the clinical analytics platforms market, with a projected CAGR of 20.20% through 2031. Growth is driven by healthcare digitalization, expanding clinical trial activities, and government focus on structured health data environments. In January 2026, Fujitsu Japan and JMDC linked anonymized DPC hospital data with insurer records, covering 20 million records, enhancing patient journey analysis for pharmaceutical and public sector applications. China is scaling rapidly, with platforms like MSTATA supporting over 1,200 SCI publications since 2024, reflecting widespread adoption across hospital networks.

Europe remains technically advanced but is shaped by privacy, sovereignty, and regulatory infrastructure. Germany's NUKLEUS platform expanded in July 2025 to support adaptive clinical platform studies and leverage statutory health insurance and cancer registry data across university hospitals. The Middle East and Africa are advancing through sovereign AI healthcare investments, highlighted by the Oracle, Cleveland Clinic, and G42 partnership announced in May 2025. South America, despite progress in digitalization in Brazil and Argentina, remains the smallest regional market.

- eClinicalWorks

- Flatiron Health, Inc.

- GE HealthCare Technologies Inc.

- Health Catalyst, Inc.

- Innovaccer

- Inovalon, Inc.

- Intersystems

- IQVIA

- Komodo Health, Inc.

- Koninklijke Philips

- MedeAnalytics

- Medidata Solutions, Inc.

- Merative

- Optum

- Oracle

- SAS Institute

- Siemens Healthineers

- SOPHiA GENETICS SA

- Tempus AI, Inc.

- Veeva Systems

- Veradigm Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Value-Based Care and Outcome-Linked Reimbursement Adoption

- 4.2.2 Explosion of Multimodal Clinical Data Across Care Settings

- 4.2.3 Cloud And AI/ML Modernization of Healthcare Data Infrastructure

- 4.2.4 Regulatory Openness to Real-World Evidence and Precision Medicine Analytics

- 4.2.5 Bulk FHIR and Population-Level API Maturation

- 4.2.6 CMS Interoperability and Prior-Authorization API Mandates Converting Workflow Pain into Software Budgets

- 4.3 Market Restraints

- 4.3.1 Data Privacy, Security, and Governance Burden

- 4.3.2 Data Quality, Standardization, and Legacy Interoperability Gaps

- 4.3.3 Post-Deployment Model Drift and Fragmented Accountability

- 4.3.4 Workflow Backlash from Alert Fatigue, Low Trust, and Hidden Implementation Labor

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Offering

- 5.1.1 Raw Data

- 5.1.2 Software

- 5.1.3 Platform

- 5.2 By Deployment Model

- 5.2.1 Cloud-based

- 5.2.2 On-premises

- 5.2.3 Hybrid

- 5.3 By Data Source

- 5.3.1 Electronic Health Records

- 5.3.2 Claims Data

- 5.3.3 Clinical Trials Data

- 5.3.4 Registries & Real-World Evidence

- 5.3.5 Imaging & Diagnostics

- 5.3.6 Lab & Pathology

- 5.3.7 Others

- 5.4 By Use Case

- 5.4.1 Healthcare

- 5.4.2 Life Sciences

- 5.5 By End User

- 5.5.1 Healthcare Providers

- 5.5.2 Healthcare Payers

- 5.5.3 Life Sciences Companies

- 5.5.4 Others

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 Australia

- 5.6.3.5 South Korea

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East and Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 eClinicalWorks, LLC

- 6.3.2 Flatiron Health, Inc.

- 6.3.3 GE HealthCare Technologies Inc.

- 6.3.4 Health Catalyst, Inc.

- 6.3.5 Innovaccer Inc.

- 6.3.6 Inovalon, Inc.

- 6.3.7 InterSystems Corporation

- 6.3.8 IQVIA Holdings Inc.

- 6.3.9 Komodo Health, Inc.

- 6.3.10 Koninklijke Philips N.V.

- 6.3.11 MedeAnalytics, Inc.

- 6.3.12 Medidata Solutions, Inc.

- 6.3.13 Merative

- 6.3.14 Optum, Inc.

- 6.3.15 Oracle Corporation

- 6.3.16 SAS Institute Inc.

- 6.3.17 Siemens Healthineers AG

- 6.3.18 SOPHiA GENETICS SA

- 6.3.19 Tempus AI, Inc.

- 6.3.20 Veeva Systems Inc.

- 6.3.21 Veradigm Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment