|

시장보고서

상품코드

2063861

아시아태평양의 GPU 침지 냉각 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Asia Pacific GPU Immersion Cooling - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

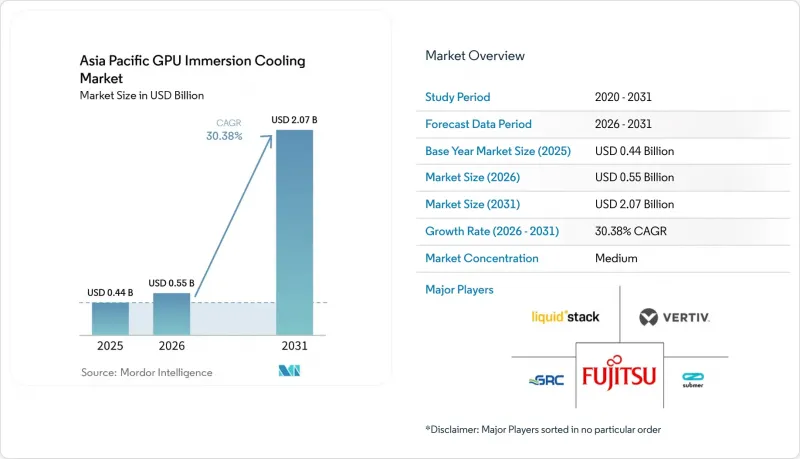

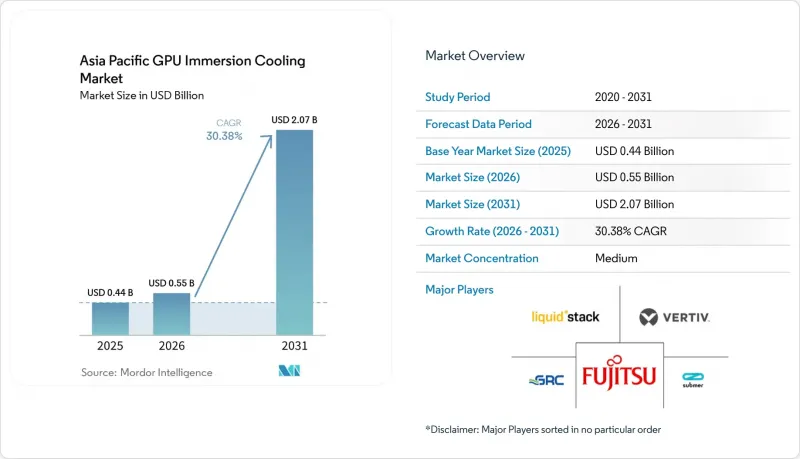

Mordor Intelligence에 의하면, 아시아태평양의 GPU 침지 냉각 시장 규모는 2025년 4억 4,000만 달러로 평가되었습니다. 2026년에는 5억 5,000만 달러로 확대되어 2026년부터 2031년에 걸쳐 CAGR 30.38%로 성장을 지속하여, 2031년에는 20억 7,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 침지형(단상 침지 냉각 및 2상 침지 냉각), 용액형(침지 냉각 탱크/시스템, 유전체 유체 등), 적용 분야(하이퍼스케일 클라우드, 엔터프라이즈, 정부·연구기관용 HPC), GPU 전력 밀도(300W 미만, 300W-700W, 기타), 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

아시아태평양의 GPU 침지 냉각 시장 동향 및 인사이트

하이퍼스케일 데이터센터 전반에 걸친 AI 및 HPC용 GPU 도입의 급증

각 하이퍼스케일러 기업들은 사상 최대 규모의 가속기를 도입함에 따라 랙당 전력 소비량을 100kW 이상으로 끌어올렸으며, 이로 인해 액체 침지 냉각 솔루션으로의 급속한 전환을 피할 수 없게 되었습니다. ByteDance는 2025년 GPU 조달에 140억 달러를 투자하고, Alibaba Cloud는 AI 인프라에 1,000억 달러를 배정했으며, 두 회사 모두 약 700W급 장비를 중심으로 데이터센터를 구축했습니다. 네이버의 NVIDIA B200 4,000대 도입 사례와 SK텔레콤의 1,000대 도입 사례는 정격 성능에서 지속적인 가동을 위해서는 칩 발열을 액체 냉각으로 효과적으로 제어하는 것이 필수적임을 보여줍니다. 일본에 위치한 120억 달러 규모의 GMI Cloud 캠퍼스에서는 Blackwell 세대 클러스터를 위해 침지 탱크의 도입이 명시적으로 의무화되어 있습니다. NVIDIA의 로드맵에 따르면, 향후 2개 제품 주기 이내에 TDP가 1,000W를 초과하는 장치가 등장할 것으로 예상되므로, 침지 냉각은 더 이상 틈새 시장의 효율화 방안이 아니라, 경쟁력 있는 AI 훈련 처리량을 실현하기 위한 열 관리의 필수 조건이 되었습니다.

엄격한 에너지 효율 규제와 PUE 목표

각국 정부는 데이터센터의 전력 수요를 억제하기 위해 PUE 상한 규제를 강력한 수단으로 활용하고 있습니다. 일본에서는 기존 시설에 대해 2030년까지 1.4를 달성하고, 신규 건설 시설에 대해서는 2029년 이후부터 1.3을 충족하도록 의무화하고 있으며, 액침 프로젝트에는 최대 1,146억 엔(10억 달러)의 보조금이 마련되어 있습니다. 싱가포르는 신규 시설의 PUE를 1.3 이하로 제한하고 있으며, 2026년을 목표로 전용 액체 냉각에 관한 규정을 마련 중입니다. 베이징, 상하이, 광둥성에서는 이미 1.2에서 1.3의 기준치가 적용되고 있습니다. 실증된 수냉식 시설에서는 PUE가 1.02 전후로 안정적으로 달성되고 있으며, CRAH 팬이나 덕트 설비를 불필요하게 만드는 동시에 냉각 전력을 최대 90%까지 절감하고 있습니다. 이러한 정책 동향을 고려할 때, 2020년대 말보다 훨씬 이전에 주요 도시권 전체에서 공랭식 방식이 규제 기준을 충족하지 못하게 될 것으로 예측됩니다.

공랭식에 비해 높은 초기 설비 투자 비용

총 소유 비용(TCO) 측면에서 볼 때, 랙당 50kW를 초과하는 경우 액침 냉각 방식이 더 유리하지만, 많은 기업의 예산은 여전히 초기 비용에 중점을 두고 있습니다. 인도의 사업자들은 탱크, 펌프, 수입 액체의 조달 비용이 증가함에 따라 가동 시작 시 10-20% 더 높은 비용을 지불하고 있습니다. 냉각액만으로도, 배합이나 탱크 용량에 따라 랙당 6,000-6만 달러의 추가 비용이 발생할 가능성이 있습니다. 싱가포르에서는 쉘(Shell)과 케펠(Keppel)이 수명 주기 비용에서 40%의 절감 효과를 보여주었으나, 18개월의 회수 기간을 전제로 하는 기업들은 이러한 전환을 승인하는 데 주저하고 있습니다. 수입 부품에 대한 의존은 관세와 물류 비용을 통해, 특히 남아시아에서 그 격차를 더욱 벌리고 있습니다.

부문별 분석

2025년 기준으로, 아시아태평양의 GPU 침지 냉각 시장 점유율의 79.45%를 단상 설계가 차지했습니다. 광물유나 합성 에스테르계 유체를 사용하면, 운영자가 밀폐형 커버 없이도 표준 서버를 액체에 담글 수 있어 유지보수나 개조 작업이 용이해지기 때문에 여전히 인기가 높습니다. Asperitas사는 시리즈 C 라운드에서 5,550만 달러를 조달하고, 태국의 열대 기후 환경에서 이러한 시스템의 구축을 시작했습니다. 그러나 700W를 초과하는 차세대 GPU의 등장으로 인해, 대류만으로 구성된 루프의 여유 용량이 점차 줄어들고 있습니다. 저비점 유체를 기화시켜 뛰어난 열유속을 실현하는 2상 솔루션은 하이퍼스케일러들이 150 kW를 초과하는 랙 밀도를 추구함에 따라 점차 보급이 확대되고 있습니다. Sabey Data Centers는 냉수를 완전히 배제하고, 전체 포트폴리오에 OptiCool 냉매 루프를 도입하고 있습니다.

앞으로 NVIDIA의 Blackwell 시리즈는 장치당 TDP를 1,000W 가까이 끌어올릴 것으로 예상되며, 그때쯤이면 2상 냉각 방식이 클라우드 구축 사업자들 사이에서 주류가 될 것입니다. SLiquid의 C8000 캐비닛은 이미 200 W/cm²의 방열 성능과 220 kW의 부하를 지원한다고 밝히고 있습니다. 그렇다고 해서 단상 방식이 사라지는 것은 아닙니다. 700W 미만의 가속기를 도입하는 기업들은 여전히 그 낮은 복잡성을 선호하며, 엣지 노드에서는 기술자가 침지 처리된 기판에 직접 접근할 수 있다는 점을 중요하게 여깁니다. 그 결과, 아시아·태평양 지역의 GPU 침지 냉각 시장은 양극화되어 있습니다. 중출력 시스템에서는 대류 루프가 주류를 이루는 반면, 초고밀도 AI 훈련 팜에서는 상변화 탱크가 핵심 역할을 담당하고 있습니다.

탱크 및 부대 시스템은 모든 액체 냉각 시스템 구축의 출발점이기 때문에 2025년 아시아태평양의 GPU 침지 냉각 시장 규모에서 55.34%를 차지했습니다. 예를 들어, Green Revolution Cooling사의 CarnotJet 유닛은 현재 Samsung C&T사와의 제휴를 통해 아시아태평양의 여러 캠퍼스로 출하되고 있습니다. 한편, 각 OEM 업체들은 액체 환경에서 사용하기 위해 특별히 설계된 보드를 출시하고 있습니다. 후지쯔, Supermicro, 그리고 닛폰덴산은 방열판과 송풍기를 제거한 팬리스 섀시를 공동 개발하여 부품 비용을 최대 15% 절감했습니다. Wiwynn은 설계 단계부터 침지 대응 기능을 탑재하기 위해 LiquidStack의 생산 라인에 투자했습니다.

이러한 통합형 솔루션을 통해 액체 호환성과 관련된 보증 분쟁이 해소되고, 노드당 GPU 탑재 수가 증가함에 따라 랙당 성능이 향상됩니다. 그 결과, 액체 침지 냉각에 최적화된 서버 시장 규모는 연평균 성장률(CAGR) 30.85%를 기록하며 탱크형 시스템을 앞지를 것으로 전망됩니다. 탱크형 시스템은 공급 수단으로서 계속 유지될 것이며, 가치 창출은 스택의 업스트림 단계로 이동하여, 하이퍼스케일 및 엔터프라이즈급 구매자들에게 통합 위험을 대폭 줄여주는 사전 검증된 컴퓨팅 모듈로 전환될 것입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측(금액 기준, 2025년 기준)

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.26According to Mordor Intelligence, the asia pacific gPU immersion cooling market size is expected to grow from USD 0.44 billion in 2025 to USD 0.55 billion in 2026 and is forecast to reach USD 2.07 billion by 2031 at a 30.38% CAGR over 2026-2031.

This report is Segmented by Immersion Type (Single-Phase Immersion Cooling, and Two-Phase Immersion Cooling), Solution Type (Immersion Cooling Tanks/Systems, Dielectric Fluids, and More), Deployment (Hyperscale and Cloud, Enterprise, and Government and Research HPC), GPU Power Density (Below 300W, 300W-700W, and More), and Region. The Market Forecasts are Provided in Terms of Value (USD).

Asia Pacific GPU Immersion Cooling Market Trends and Insights

Surge in AI and HPC GPU Deployments Across Hyperscale Data Centers

Hyperscalers are acquiring record volumes of accelerators, pushing rack power beyond 100 kW and forcing a rapid pivot to immersion solutions. ByteDance committed USD 14 billion for GPU procurement in 2025, while Alibaba Cloud earmarked USD 100 billion for AI infrastructure, both sizing their halls around 700 W-class devices. Naver's 4,000-unit NVIDIA B200 roll-out and SK Telecom's 1,000-unit deployment show that sustained operation at nameplate performance requires liquid capture of chip heat. Japan's USD 12 billion GMI Cloud campus explicitly mandates immersion tanks for Blackwell-generation clusters. Because NVIDIA roadmaps indicate devices surpassing 1,000 W TDP within two product cycles, immersion is no longer a niche efficiency play, it is the thermal pre-requisite for competitive AI training throughput.

Stringent Energy-Efficiency Regulations and PUE Targets

Governments are weaponizing PUE caps to curb data-center electricity demand. Japan requires existing sites to hit 1.4 by 2030 and new builds to meet 1.3 from 2029, backed by subsidies up to JPY 114.6 billion (USD 1.0 billion) for immersion projects. Singapore limits new facilities to PUE more than 1.3 and is drafting a dedicated liquid-cooling code for 2026. Beijing, Shanghai, and Guangdong already enforce thresholds between 1.2 and 1.3. Demonstrated immersion fields routinely deliver PUE near 1.02, eliminating CRAH fans and ductwork while slashing cooling power by up to 90%. The policy trajectory suggests air cooling will be non-compliant across tier-1 metros well before the end of the decade.

High Upfront Capital Expenditure Versus Air Cooling

Total cost of ownership favors immersion above 50 kW per rack, yet many enterprise budgets still focus on initial price tags. Indian operators pay 10-20% more at commissioning because tanks, pumps, and imported fluids inflate procurement outlays. Fluid alone can add USD 6,000-60,000 per rack, depending on formulation and tank volume. Although Shell and Keppel showed 40% life-cycle savings in Singapore, enterprises operating on 18-month payback horizons hesitate to approve the switch. Reliance on imported components further widens the gap through tariffs and logistics, particularly in South Asia.

Other drivers and restraints analyzed in the detailed report include:

- Scarcity of Water Resources in Major Asian Metros Driving Liquid Cooling Adoption

- Accelerated Adoption of Edge Immersion Micro-Data Centers for 5G Densification

- Limited Industry Standards and Hardware Certification

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Single-phase designs held 79.45% of Asia Pacific GPU immersion cooling market share in 2025. They remain popular because mineral-oil and synthetic-ester fluids let operators submerge standard servers without sealed lids, easing maintenance and retrofit projects. Asperitas attracted USD 55.5 million in Series C funding and began rolling out such systems in Thailand's tropical climate. Yet next-wave GPUs topping 700 W are eroding the headroom of convection-only loops. Two-phase solutions, which vaporize low-boiling-point fluids for superior heat flux, are scaling as hyperscalers chase rack densities above 150 kW. Sabey Data Centers is integrating OptiCool refrigerant loops portfolio-wide, bypassing chilled water entirely.

Looking ahead, NVIDIA's Blackwell parts are expected to push per-device TDP near 1,000 W, at which point two-phase will mainstream among cloud builders. SLiquid's C8000 cabinet already claims 200 W/cm2 dissipation and 220 kW loads. Nevertheless, single-phase will not disappear; enterprises with <700 W accelerators still favor its lower complexity, and edge nodes prize direct technician access to submerged boards. The Asia Pacific GPU immersion cooling market therefore bifurcates: convection loops dominate mid-power deployments, while phase-change tanks anchor ultra-dense AI training farms.

Tanks and ancillary systems represented 55.34% of Asia Pacific GPU immersion cooling market size in 2025 because they are the starting point for any liquid build. Green Revolution Cooling's CarnotJet units, for example, are now shipping under a Samsung C&T alliance across multiple APAC campuses. OEMs, however, are unveiling boards purpose-engineered for submerged use. Fujitsu, Supermicro, and Nidec co-developed fan-less chassis that shed heatsinks and blowers, cutting bill of materials by up to 15%. Wiwynn invested in LiquidStack manufacturing lines to embed immersion readiness at design time.

Such integrated offerings eliminate warranty disputes about fluid compatibility and support higher GPU counts per node, translating to better performance per rack. As a result, immersion-optimized servers are projected to outgrow tanks at a 30.85% CAGR. Tanks will persist as the delivery vehicle, but value capture migrates up-stack toward pre-validated compute modules that slash integration risk for hyperscale and enterprise buyers.

List of Companies Covered in this Report:

- Submer Technologies, S.L.

- LiquidStack Inc.

- Green Revolution Cooling Inc.

- Giga-Byte Technology Co., Ltd.

- Fujitsu Limited

- Wiwynn Corporation

- Iceotope Technologies Limited

- Engineered Fluids Inc.

- Vertiv Group Corp.

- CoolIT Systems Inc.

- Boyd Corporation

- nVent Electric plc

- SK Enmove Co., Ltd.

- HD Hyundai Oilbank Co., Ltd.

- Shell plc

- Huawei Technologies Co., Ltd.

- ExaScaler Inc.

- Chemours Company

- Alibaba Cloud Computing Co., Ltd.

- Super Micro Computer, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in AI and HPC GPU Deployments Across Hyperscale Data Centers

- 4.2.2 Stringent Energy-Efficiency Regulations and PUE Targets

- 4.2.3 Scarcity of Water Resources in Major Asian Metros Driving Liquid Cooling Adoption

- 4.2.4 Accelerated Adoption of Edge Immersion Micro-Data Centers for 5G Densification

- 4.2.5 Government-Funded National Supercomputing and Sovereign AI Clusters

- 4.2.6 Local Manufacturing Incentives for Immersion Tanks and Dielectric Fluids

- 4.3 Market Restraints

- 4.3.1 High Upfront Capital Expenditure Versus Air Cooling

- 4.3.2 Limited Industry Standards and Hardware Certification

- 4.3.3 Uncertain Long-Term Environmental Rules on Fluorinated Fluids

- 4.3.4 Skill Shortages in Immersion-Specific Maintenance

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE and GROWTH FORECASTS (VALUE, 2025 BASE YEAR)

- 5.1 By Immersion Type

- 5.1.1 Single-Phase Immersion Cooling

- 5.1.2 Two-Phase Immersion Cooling

- 5.2 By Solution Type

- 5.2.1 Immersion Cooling Tanks / Systems

- 5.2.2 Dielectric Fluids

- 5.2.3 Immersion-Optimized GPU Server Systems

- 5.3 By Deployment

- 5.3.1 Hyperscale / Cloud

- 5.3.2 Enterprise

- 5.3.3 Government and Research (HPC)

- 5.4 By GPU Power Density

- 5.4.1 Below 300W

- 5.4.2 300W - 700W

- 5.4.3 Above 700W

- 5.5 By Region

- 5.5.1 Asia Pacific

- 5.5.1.1 China

- 5.5.1.2 Japan

- 5.5.1.3 South Korea

- 5.5.1.4 India

- 5.5.1.5 Southeast Asia

- 5.5.1.6 Rest of Asia Pacific

- 5.5.1 Asia Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Submer Technologies, S.L.

- 6.4.2 LiquidStack Inc.

- 6.4.3 Green Revolution Cooling Inc.

- 6.4.4 Giga-Byte Technology Co., Ltd.

- 6.4.5 Fujitsu Limited

- 6.4.6 Wiwynn Corporation

- 6.4.7 Iceotope Technologies Limited

- 6.4.8 Engineered Fluids Inc.

- 6.4.9 Vertiv Group Corp.

- 6.4.10 CoolIT Systems Inc.

- 6.4.11 Boyd Corporation

- 6.4.12 nVent Electric plc

- 6.4.13 SK Enmove Co., Ltd.

- 6.4.14 HD Hyundai Oilbank Co., Ltd.

- 6.4.15 Shell plc

- 6.4.16 Huawei Technologies Co., Ltd.

- 6.4.17 ExaScaler Inc.

- 6.4.18 Chemours Company

- 6.4.19 Alibaba Cloud Computing Co., Ltd.

- 6.4.20 Super Micro Computer, Inc.

7 MARKET OPPORTUNITIES and FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment