|

시장보고서

상품코드

2063870

치과용 컴프레서 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Dental Compressors - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

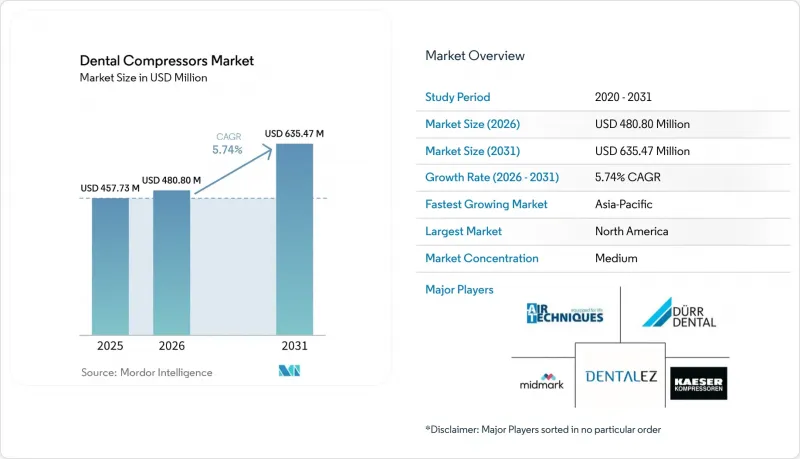

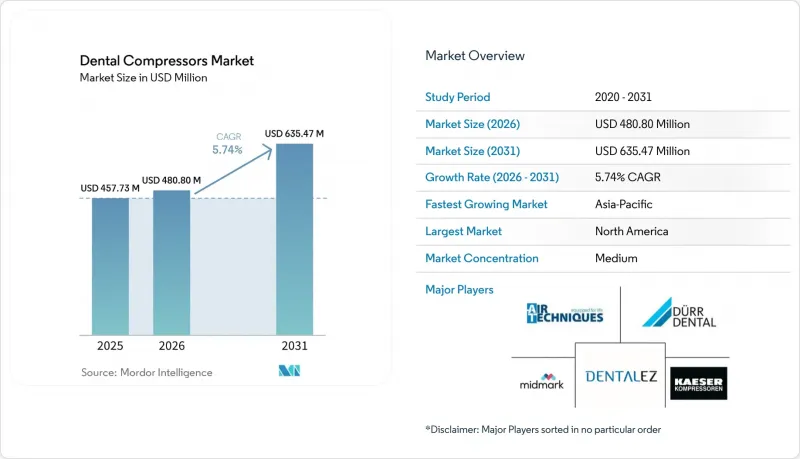

Mordor Intelligence에 의하면, 치과용 컴프레서 시장 규모는 2025년에 4억 5,773만 달러로 평가되었고 2026년 4억 8,080만 달러에서 2031년까지 6억 3,547만 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 5.74%를 나타낼 전망입니다.

본 보고서는 유형별(오일프리 컴프레서, 윤활식 컴프레서), 기술별(건조제식 컴프레서, 막식 컴프레서), 용도(고속 핸드피스, 스케일러 등), 최종 사용자(치과·병원 등), 지역(북미, 유럽, 아시아태평양, 중동 및 아프리카, 남미)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계 치과용 컴프레서 시장 동향 및 인사이트

감염 관리에서 오일 프리이며 깨끗하고 건조한 공기로의 전환

멸균 프로토콜이 더욱 엄격해지고, 임상용 압축 공기가 규제 대상 공급원으로 공식적으로 지정됨에 따라, 각 시술 과정에서 오일 혼입이나 습기에 대한 허용 기준이 낮아지고 있습니다. 압축 공기의 순도에 관한 규정을 치과 진료 용어로 대체한 EU MDR 및 ISO 22052에 따라, 진료소는 다단계 여과 및 검증된 건조기를 갖춘 오일 프리 설계로 전환해야 할 필요에 직면해 있습니다. 미국에서는 2024년 공기 구동 핸드피스에 관한 지침에 따라, 사용 현장에서의 깨끗하고 건조한 공기에 의존하는 성능 및 재처리 관련 기대치가 강화되었습니다.

이러한 규정 준수 기준에 따라 조달 방침은 ‘시설 인프라’에서 ‘임상 품질’로 전환되었습니다. 이에 따라, 치과 진료실 공기에 적용되는 ISO 8573-1 등급에 기반한 순도 기준을 기본적으로 충족하는 오일 프리 컴프레서가 선호되고 있습니다. 치과용 컴프레서 시장에 미친 실질적인 영향으로는 건조도 및 순도에 관한 기본 사양이 강화되었으며, 정기 유지보수 기록에 대한 문서화된 검증이 중요시되게 되었습니다. 규제 당국과 임상 지침 수립 기관들은 치과 병원이 업스트림 공기 품질이 멸균 결과를 뒷받침한다는 증거를 제시할 것을 점점 더 기대하고 있으며, 이슬점 제어 및 미세 응집 필터를 갖춘 오일 프리 시스템의 표준화를 촉진하고 있습니다.

치과 시술 증가와 장비 업그레이드

DSO 네트워크는 계속해서 규모를 확대하며 새로운 클리닉을 개설하고 있으며, 이러한 확장에 따라 표준화된 컴프레서 사양과 통합된 유지보수 계획이 수반됩니다. 하트랜드 덴탈은 2024년에 22개 주에서 105개 진료소를 개설하고, 2025년 상반기에 수십 개의 신규 거점을 추가했다고 보고했으며, 이를 통해 확장되는 전체 시설에 걸쳐 일관된 공기질 목표가 수립되었습니다. 이러한 수준의 계획적인 성장은 멤브레인식 또는 건조제식 드라이어가 장착된 오일 프리 컴프레서의 대량 구매를 뒷받침하며, 치과용 컴프레서 시장을 클라우드 모니터링과 문서화된 서비스 이력을 통해 관리되는 플릿으로 전환시키고 있습니다.

또한, 네트워크 운영사는 치과와의 제휴를 통해 확보한 레거시 시스템에 대해서도, 접착 치과 치료나 고속 핸드피스에서 일반적으로 적용되고 있는 새로운 수분·유분 기준에 부합하도록 개조를 진행하고 있습니다. 디지털 진단 및 영상 진단의 활용 확대에는 터빈 업스트림에서의 안정적인 압력 공급이 필수적이며, 이러한 요인도 장비 조달을 표준화된 컴프레서 구성에 더욱 부합하도록 하는 한 요인이 되고 있습니다. 그 결과, 신규 설치뿐만 아니라 꾸준한 교체 작업이 진행되고 있으며, 이에 따라 치과용 컴프레서 시장에서 지역별 유통망과 신속한 서비스 체계를 지원할 수 있는 공급업체에게 예측 가능한 성장 패턴이 더욱 공고해지고 있습니다.

오일 프리 시스템의 높은 초기 비용과 수명 주기 총 소유 비용(TCO)

오일 프리 컴프레서는 윤활식 컴프레서에 비해 구입 가격이 높은 경우가 많으며, 초기 투자를 우선시하는 개인 개업의나 클리닉의 경우 그 가격 차이는 큰 의미를 가질 수 있습니다. 흡습제식 건조기는 카트리지를 정기적으로 교체해야 하므로 지속적인 비용이 발생하지만, 막식 건조기는 소모품을 줄일 수 있는 반면 초기 비용이 높아질 가능성이 있습니다. 구매자들은 필터 교체 빈도나 다단계 여과 과정에서 발생하는 압력 손실로 인한 에너지 소비의 영향을 과소평가하는 경우가 있으며, 이로 인해 총 소유 비용(TCO) 산정이 복잡해지고 오일 프리 시스템으로의 전환이 지연되고 있습니다. 대출 조건이 제한적이거나 리스 옵션이 적은 경우, 또는 높은 초기 비용에 놀라 하류에 응집 여과나 활성탄 여과를 결합한 윤활식 시스템이 선택되기도 합니다.

소규모 진료소가 많은 지역에서는 규제와 정책이 오일 프리 시스템이나 검증된 공기질 성능을 권장하고 있음에도 불구하고, 이러한 상황이 시설 개선 속도를 늦추고 있습니다. 공급업체 측은 서비스 주기 연장이나 조기 교체를 방지하는 모니터링 기능 도입 등으로 대응하고 있지만, 치과용 컴프레서 시장의 일부에서는 여전히 구매 가격에 대한 민감도가 장벽으로 작용하고 있습니다.

부문별 분석

2025년, 무유 컴프레서는 57.9%의 시장 점유율을 차지했습니다. 이는 진료소가 감염 관리, 접착 감도 문제, 그리고 검증된 건조도를 중시하여 조달을 진행했기 때문이며, 이러한 자세가 무유 컴프레서가 치과용 컴프레서 시장에서 주도적인 위치를 유지하는 요인이 되고 있습니다. 또한, 오일 프리 설계는 업스트림의 공기에서 윤활유를 제거하여 복합재 접착이나 멸균 기구 취급에 지장을 줄 수 있는 유증기 혼입 위험을 줄여주므로, 순도 입증도 용이해집니다. 서비스 주기를 연장하고 냉각 효율을 향상시키는 OEM의 업데이트는 오일 프리 플랫폼의 신뢰성을 한층 더 높이고 있습니다. 이러한 제품들은 접착 및 CAD/CAM 작업에 적합한 더 낮은 이슬점을 달성하는 흡착식 또는 하이브리드식 드라이어와 함께 사용되는 경우가 많아, 이용 빈도가 높은 진료소에서 표준적인 선택지로 자리매김하고 있습니다. 감사에서 시험 및 검증에 대한 문서화가 요구되는 지역에서는 진료소에서 샘플링 지점이 내장되어 있고 검증 체계가 명확한 오일 프리 제품이 선호되는 경향이 있습니다. 이러한 추세에 따라 진료소, 병원, 학술 기관에서의 오일 프리 컴프레서 수요 양상은 안정적인 상태를 유지하고 있습니다.

윤활식 컴프레서는 다수의 진료실을 지원하기 위해 높은 총 유량이 필요하며, 투자 회수 기간이 긴 상황에서 초기 투자 비용을 절감해야 하는 연수 센터나 대규모 학술 기관에서 여전히 중요한 역할을 하고 있으며, 치과용 컴프레서 시장에서 이 부문은 2031년까지 연평균 성장률(CAGR) 6.24%를 나타낼 것으로 예측됩니다. 이러한 설비에서는 일반적으로 사용 지점의 유증기 허용 한도를 충족하기 위해 다단식 유분리 및 활성탄 흡착에 의존하고 있습니다. 이는 문서화가 엄격하게 이루어지고, 유지보수가 예정대로 수행되는 경우 효과적인 접근 방식입니다. 장기적으로는 막식 건조기나 수명이 긴 필터를 통해 오일 프리형 플랫폼에 비해 수명 주기 비용이 절감될 가능성이 있지만, 단기적인 선택은 구매 가격이나 구하기 쉬움 여부에 따라 좌우되는 경우가 많습니다. 많은 학술 기관에서는 중앙 플랜트에 이중화 체계를 갖추고 있으며, 대형 탱크와 철저한 여과 과정을 결합하여 다양한 처치 및 학생들의 연수 주기에 대응하고 있습니다. 이로 인해, 적절히 유지보수된다면 순도 목표를 달성할 수 있는 윤활식 유닛을 위한 실용적인 틈새 시장이 생겨나고 있습니다. 그 결과, 치과용 컴프레서 시장에서는 민간 진료소에서는 오일프리 방식이 주류를 이루는 반면, 일부 기관에서는 견고한 여과 시스템과 함께 윤활식 기술을 계속 도입하는 등 안정적인 양극화 구도가 형성되고 있습니다.

흡착식 시스템은 본딩 및 밀링 요건에 부합하는 더 낮은 이슬점을 실현할 수 있기 때문에 2025년에는 64.65%의 시장 점유율을 차지하며 치과용 컴프레서 시장에서 주도적인 위치를 확립하고 있습니다. 장시간 가동되는 클리닉이나 연구실에서는 습도 변동이 심한 환경에서도 터빈 및 정밀 밀링의 성과를 보호해 주는 -30°C에서 -40°C의 이슬점에 의해 확보되는 안전 여유를 높이 평가했습니다. 각 제조업체는 카트리지 미디어를 개선하고 지능형 시퀀싱 제어 기능을 설계함으로써, 유지보수 주기를 연장하고 장기간에 걸쳐 안정적인 이슬점을 유지할 수 있도록 하고 있습니다. RFID 태그가 부착된 카트리지와 IoT 대시보드는 직원들이 적절한 시기에 건조제를 교체하는 데 도움이 되어, 시기상조인 교체를 줄이고 경비를 명확히 파악할 수 있게 해줍니다. 이러한 노력을 통해, 예산을 준수하고 가동 시간을 유지해야 하는 관리자에게 있어 건조제 솔루션의 운영이 더욱 예측 가능해질 것입니다. 이러한 동향은 특히 치과용 컴프레서 시장에서 연속 운전이나 고부하 운전에 의존하는 다중 진료실, 병원, 연구소에서 건조제 플랫폼의 확고한 역할을 더욱 공고히 하고 있습니다.

막식 건조기는 소모품이 전혀 필요 없는 운영, 재생 주기가 필요 없는 안정적인 성능, 그리고 도심 지역의 진료소에 적합한 저소음성을 추구하는 중소규모 클리닉에 매력적인 선택지입니다. 이러한 시스템은 유지보수 빈도를 줄이고 퍼지 공기의 손실을 방지하기 때문에 수자원이 부족한 지역이나 에너지 효율을 중시하는 지역에서 특히 매력적입니다. 대부분의 기후 조건에서 멤브레인식 건조기는 고효율 응집 여과와 결합하여 일상적인 임상 요구 사항을 충족하는 매우 건조한 공기를 공급하며, 정기 유지보수(PM) 일정에서 카트리지 교체를 제외함으로써 일상적인 운영을 간소화합니다. 하이브리드 구성에서는 막식 프리드라이어를 하류의 정제 공정과 결합함으로써, 빈번한 건조제 재생에 따른 에너지 소비 증가를 초래하지 않으면서 더 낮은 이슬점을 달성할 수 있습니다. 진료소에서 IoT 모니터링 시스템을 도입하여 이슬점의 추이를 시각화함으로써, 실제 상황에 맞추어 유지보수를 조정할 수 있게 되어 낭비를 줄이고 성능의 예측 가능성을 높일 수 있습니다. 이러한 실용적인 이점 덕분에, 치과용 컴프레서 시장에서 건조제 방식이 주도적인 위치를 차지하는 한편, 막 방식 및 하이브리드 방식의 채택이 확대되고 있는 이유를 설명해 줍니다.

지역별 분석

북미는 2025년에 47.42%의 점유율을 차지했습니다. 이는 DSO(치과 진료소 수) 밀도, 문서화된 멸균 프로토콜, 그리고 컴프레서의 성능과 유지보수를 임상 품질에 반영한 조달 기준에 기반을 두고 있습니다. 대형 운영사는 계속해서 클리닉을 개설하고 인수한 진료소의 개보수를 진행하고 있으며, 이에 따라 막식 또는 건조제식 건조 기능을 갖춘 오일프리 플랫폼에 대한 수요는 안정적인 상태를 유지하고 있습니다. 이 지역에 서비스를 제공하는 공급업체들은 신속한 대응, 광범위한 서비스 네트워크, 그리고 진료소 대시보드와 연동되는 클라우드 모니터링에 주력하고 있습니다. 이러한 요소들은 업무량이 많은 다중 진료과 클리닉에서 규정 준수 요건과 가동률 목표 모두를 뒷받침하고 있습니다. 대규모 네트워크의 집중은 또한 비용을 분산시키고, 모든 장비에 걸쳐 예측 가능한 유지보수 일정을 가능하게 하는 구독 모델과 통합 서비스 플랜을 뒷받침하고 있습니다. 이러한 추세로 인해 북미는 치과용 컴프레서 시장에서 주도적인 입지를 더욱 공고히 하고 있습니다.

유럽은 여전히 중요한 지역이며, 독일, 이탈리아 및 인근 시장의 활발한 OEM 및 설치 업체 활동과 더불어, 사용 현장에서의 성능 검증을 요구하는 지속적인 규정 준수 검사를 통해 뒷받침되고 있습니다. 영국 국민보건서비스(NHS)의 HTM 2022 프레임워크 및 정기 점검에 따라, 치과 병원에서는 흡습제 방식 또는 하이브리드 방식의 건조 방식을 도입하고, 샘플링 포트를 추가하며, 정기적인 감사를 실시하도록 장려하고 있습니다. 이 지역공급업체들은 오일 프리 설계와 검사를 위한 기록 관리를 효율화하는 문서화 워크플로우를 중시하고 있습니다. 이탈리아 및 인근 지중해 시장에서는 컴프레서, 흡입 장치, 부속품을 조합하여 지역 밀착형 서비스망을 구축하는 현지 제조업체와 판매업체들이 확고한 입지를 다지고 있습니다. 또한, 중부 유럽의 OEM 기반은 수출 수요와 제품 개발을 뒷받침하고 있으며, 이는 전 세계적인 사양 선정 추세에 영향을 미치고 있습니다. 이러한 특징 덕분에, 치과용 컴프레서 시장에서 유럽은 제품 혁신과 기존 설비의 업그레이드에 있어 계속해서 중심적인 역할을 수행하고 있습니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR) 6.36%를 기록하며 성장할 것으로 전망됩니다. 이는 여러 국가에서 치과대학이 확대되고 공공 부문의 투자가 증가함에 따라, 교육용 클리닉에 오일 프리 공기 공급과 문서화된 유지보수가 요구되기 때문입니다. 시장 교육과 디지털 덴티스트리의 보급은 더 낮은 이슬점과 더 엄격한 수분 임계값을 요구하는 장비의 업그레이드에 기여하고 있습니다. 제조 거점 내 연구소에는 가동률이 높은 멀티밀 셀이 추가되었으며, 이는 건조제나 하이브리드 건조 방식의 선택, 그리고 더 대형의 오일프리 집적 장치에 대한 수요를 시사하고 있습니다. 유통업체은 현지 기준에 맞춘 설치, 검증, 교육 패키지를 통해 차별화를 꾀하고 있으며, 다수의 진료실을 운영하는 클리닉의 문서화 절차를 간소화하기 위해 모니터링 기능을 추가하고 있습니다. 더 많은 시스템이 클라우드 대시보드로 전환됨에 따라, 자산 관리자는 필터와 건조기의 상태를 보다 명확하게 파악하고, 실제 상황에 맞추어 서비스를 조정할 수 있게 됩니다. 이러한 변화로 인해 사양 기준은 지속적으로 높아지고 있으며, 개발도상국에서의 치과용 컴프레서 시장 수요가 촉진되고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.23According to Mordor Intelligence, the dental compressors market size was valued at USD 457.73 million in 2025 and is estimated to grow from USD 480.80 million in 2026 to reach USD 635.47 million by 2031, at a CAGR of 5.74% during the forecast period (2026-2031).

This report is Segmented by Type (Oil-Free Compressors, Lubricated Compressors), Technology (Desiccant-Based Compressors, Membrane-Based Compressors), Application (High-Speed Handpieces, Scalers, and More), End User (Dental Clinics and Hospitals, and More), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

Global Dental Compressors Market Trends and Insights

Infection Control Shift to Oil-Free, Clean, Dry Air

Stricter sterilization protocols and the formal treatment of clinical compressed air as a regulated input have reduced tolerance for oil carryover and moisture across procedures. EU MDR and ISO 22052, which translate compressed air purity rules into dental practice language, have pushed clinics toward oil-free designs with multi-stage filtration and validated dryers. In the U.S., 2024 guidance on air-powered handpieces reinforced performance and reprocessing expectations that depend on clean, dry air at the point of use.

These compliance anchors have changed procurement from "facility infrastructure" to "clinical quality," which favors oil-free compressors that natively meet purity targets under ISO 8573-1 classes used in dental operatory air. The net effect on the dental compressors market is higher baseline specifications for dryness and purity, and an emphasis on documented validation within routine maintenance logs. Regulators and clinical guidance authors increasingly expect practices to show evidence that upstream air quality supports sterilization outcomes, encouraging standardization on oil-free systems with dew point control and fine coalescing filters.

Rising Dental Procedures and Equipment Upgrades

DSO networks continue to expand capacity and open new clinics, and these buildouts come with standardized compressor specifications and centralized maintenance plans. Heartland Dental reported opening 105 practices across 22 states in 2024 and added dozens of new locations in the first half of 2025, which locked in consistent air quality targets across a growing estate. This level of programmatic growth supports volume purchasing of oil-free compressors with membrane or desiccant dryers and shifts the dental compressors market toward fleets managed with cloud monitoring and documented service events.

Network operators also retrofit legacy systems acquired through practice affiliations to align with newer moisture and oil thresholds common in adhesive dentistry and high-speed handpieces. Expanded digital diagnostics and imaging usage rely on stable pressure delivery upstream of turbines, a factor that further aligns equipment procurement with standardized compressor setups. The result is steady replacement activity alongside greenfield installs, which reinforces predictable growth patterns for vendors that can support regional distribution and timely service coverage in the dental compressors market.

High Upfront Cost and Lifecycle TCO of Oil Free Systems

Oil free compressors often carry higher purchase prices than lubricated alternatives, and that differential can be meaningful for solo practices and clinics that prioritize upfront capex. Desiccant dryers add recurring spend because cartridges need periodic replacement, while membrane dryers reduce consumables but can add to initial cost. Buyers sometimes underestimate filter replacement frequency and the energy impact of pressure drops across multi stage filtration, which complicates TCO calculations and delays oil free conversions. Where financing terms are limited or leasing options are scarce, sticker shock can favor lubricated systems paired with downstream coalescing and carbon filtration.

In regions with many small clinics, this dynamic slows the pace of upgrades even as regulations and clinical policies favor oil free systems and documented air quality performance. Vendors have responded with extended service intervals and monitoring features that curb premature changeouts, but purchase price sensitivity remains an inhibitor in parts of the dental compressors market.

Other drivers and restraints analyzed in the detailed report include:

- DSO Consolidation and Multi Chair Clinic Expansion

- Regulatory Standards Elevating Air Quality Requirements

- Maintenance Burden of Filters/Dryers and Consumables

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Oil-free compressors held 57.9% share in 2025 as clinics oriented procurement toward infection control, bonding sensitivity, and validated dryness, a posture that has sustained leadership in the dental compressors market. Oil-free designs also simplify proof of purity because they remove lubricants from upstream air and reduce the risk of oil vapor breakthrough that can compromise composite bonding or sterile instrument handling. OEM updates that extend service intervals and improve cooling efficiency have strengthened reliability narratives for oil-free platforms. These products are also paired more often with desiccant or hybrid dryers that reach lower dew points suited to bonding and CAD/CAM operations, reinforcing their position as the default for high utilization practices. In regions where audits require documented testing or validation, clinics often favor oil-free options with built-in sampling points and straightforward proof frameworks. These practices stabilize demand patterns in the dental compressors market for oil-free fleets in clinics, hospitals, and academic centers.

Lubricated compressors remain important in training centers and large academic settings that need higher aggregate flow for many operatories and budget for lower upfront capex over long payback windows, and this cohort is projected to grow at 6.24% CAGR through 2031 within the dental compressors market. These installations typically rely on multi stage oil removal and carbon adsorption to meet oil vapor thresholds at the point of use, an approach that can work when documentation is rigorous and maintenance is on schedule. Over time, membrane dryers and longer life filters may narrow lifecycle costs relative to oil free platforms, but purchase price and availability often drive near term choices. Many academic centers also maintain redundancy in central plants, and the combination of larger tanks and careful filtration supports a range of procedures and student training cycles. This creates a practical niche for lubricated units that can still meet purity targets when well maintained. The result is a stable dual track configuration where oil free dominates private practice, while selected institutions continue to deploy lubricated technology alongside robust filtration in the dental compressors market.

Desiccant based systems commanded 64.65% share in 2025 because they achieve lower dew points that align with bonding and milling requirements, which underpins leadership in the dental compressors market. Clinics and labs that operate for extended hours value the safety margin created by -30°C to -40°C dew points that protect turbines and precision milling outcomes under fluctuating humidity. Vendors have refined cartridge media and designed intelligent sequencing to extend service intervals and maintain stable dew points across longer periods. RFID tagged cartridges and IoT dashboards also help staff replace desiccant at the right time, which reduces premature changeouts and clarifies spend. These steps make desiccant solutions more predictable for managers who need to defend budgets and sustain uptime. The above trends reinforce a durable role for desiccant platforms, especially in multi chair clinics, hospitals, and labs that depend on continuous or high duty operation in the dental compressors market.

Membrane dryers appeal to small and mid size clinics that want zero consumable operation, steady performance without regeneration cycles, and quieter acoustic profiles that suit urban practices. These systems reduce maintenance touch points and avoid purge air losses, which makes them compelling in water scarce or energy sensitive regions. For most climates, membrane dryers deliver very dry air that satisfies routine clinical needs when combined with high efficiency coalescing filtration, and they simplify daily operations by removing cartridge changes from PM calendars. In hybrid configurations, membrane pre drying can be paired with downstream polishing to reach lower dew points without the energy penalty associated with frequent desiccant regeneration. As clinics add IoT monitoring and visibility into dew point trends, they can tune maintenance to actual conditions, which reduces waste and improves performance predictability. These practical advantages explain why membrane and hybrid architectures are gaining adoption alongside desiccant leadership in the dental compressors market.

Geography Analysis

North America captured 47.42% share in 2025, supported by DSO density, documented sterilization protocols, and procurement standards that embed compressor performance and maintenance into clinical quality. Leading operators continue to open clinics and retrofit acquired practices, which keeps demand steady for oil free platforms with membrane or desiccant drying. Suppliers serving the region focus on fast response times, broad service coverage, and cloud monitoring that integrates with practice dashboards. These elements support both compliance requirements and uptime targets in busy multi chair clinics. The concentration of large networks also favors subscription models and unified service plans that spread costs and enable predictable maintenance scheduling across fleets. These patterns reinforce North America's leadership within the dental compressors market.

Europe remains a significant region anchored by active OEMs and installers in Germany, Italy, and neighboring markets, and by sustained compliance checks that push for validated point of use performance. NHS England's HTM 2022 framework and routine testing have driven clinics to adopt desiccant or hybrid drying, add sampling ports, and schedule regular audits. Vendors in the region emphasize oil free designs and documentation workflows that streamline record keeping for inspections. Italy and neighboring Mediterranean markets see strong positioning from local manufacturers and distributors that combine compressors, suction, and accessories with regional service density. Central Europe's OEM base also supports export demand and product development that influences specification preferences globally. These features keep Europe central to product innovation and installed base upgrades in the dental compressors market.

Asia Pacific is projected to grow at a 6.36% CAGR to 2031 as dental school expansions and public sector investments in several countries require oil free air and documented maintenance for teaching clinics. Market education and digital dentistry adoption contribute to equipment upgrades that call for lower dew points and tighter moisture thresholds. Labs in manufacturing hubs add multi mill cells that operate with high duty cycles, which points to desiccant and hybrid drying choices and larger oil free aggregates. Distributors differentiate with installation, validation, and training packages aligned to local standards, and they add monitoring to simplify documentation in clinics that run many operatories. As more systems move to cloud dashboards, asset managers improve visibility into filter and dryer status and align service with actual conditions. These shifts continue to raise the specification floor and seed demand in developing corridors of the dental compressors market.

- Air Techniques

- Anest Iwata

- Bambi Air

- Cattani S.p.A.

- DENTALEZ

- Durr Dental

- EKOM spol. s r.o.

- Gentilin

- Gnatus

- Jun-Air

- Kaeser Kompressoren

- MGF Compressors

- Midmark

- Nardi Compressori

- Powerex

- Schulz Compressores

- Tech West Inc.

- TPC Advanced Technology

- Werther International

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Infection-Control Shift to Oil-Free, Clean, Dry Air

- 4.2.2 Rising Dental Procedures and Equipment Upgrades

- 4.2.3 DSO Consolidation and Multi-Chair Clinic Expansion

- 4.2.4 Regulatory Standards Elevating Air-Quality Requirements

- 4.2.5 CAD/CAM Milling Needs Ultra-Dry, Stable Compressed Air

- 4.2.6 Predictive Maintenance and Smart Monitoring Adoption

- 4.3 Market Restraints

- 4.3.1 High Upfront Cost and Lifecycle TCO of Oil-Free Systems

- 4.3.2 Maintenance Burden of Filters/Dryers and Consumables

- 4.3.3 Space and Noise Constraints in Small Practices

- 4.3.4 Shift Toward Electric Handpieces Lowers Air Demand

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Type

- 5.1.1 Oil-free Compressors

- 5.1.2 Lubricated Compressors

- 5.2 By Technology

- 5.2.1 Desiccant-based Compressors

- 5.2.2 Membrane-based Compressors

- 5.3 By Application

- 5.3.1 High-speed Handpieces

- 5.3.2 Scalers

- 5.3.3 Chair Valves and Actuators

- 5.3.4 CAD/CAM Milling Systems Air Supply

- 5.4 By End User

- 5.4.1 Dental Clinics and Hospitals

- 5.4.2 Dental Laboratories

- 5.4.3 Academic & Research Institutes

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.3.1 Air Techniques

- 6.3.2 Anest Iwata

- 6.3.3 Bambi Air

- 6.3.4 Cattani S.p.A.

- 6.3.5 DENTALEZ

- 6.3.6 Durr Dental

- 6.3.7 EKOM spol. s r.o.

- 6.3.8 Gentilin

- 6.3.9 Gnatus

- 6.3.10 Jun-Air

- 6.3.11 Kaeser Kompressoren

- 6.3.12 MGF Compressors

- 6.3.13 Midmark Corporation

- 6.3.14 Nardi Compressori

- 6.3.15 Powerex

- 6.3.16 Schulz Compressores

- 6.3.17 Tech West Inc.

- 6.3.18 TPC Advanced Technology

- 6.3.19 Werther International

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment