|

시장보고서

상품코드

2063941

POC(Point of Care) 혈액검사 AI 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)AI In Point-of-Care Hematology - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

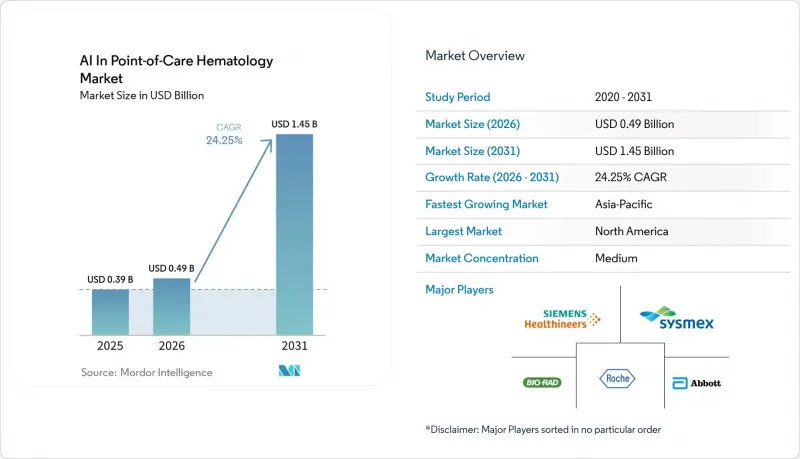

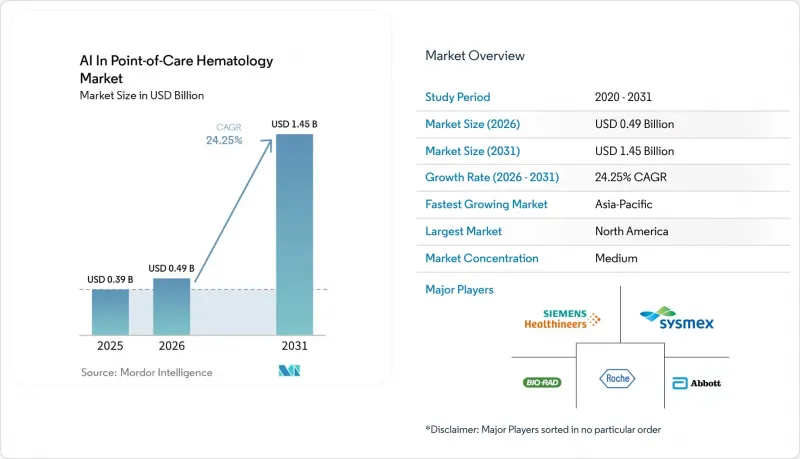

Mordor Intelligence에 의하면, POC(Point of Care) 혈액검사 AI 시장 규모는 2025년 3억 9,000만 달러로 평가되었고, 2026년 4억 9,000만 달러로 추정되고, 2031년까지 14억 5,000만 달러로 확대될 전망이며, 2026-2031년 연평균 복합 성장률(CAGR)은 24.25%를 나타낼 것으로 예측됩니다.

본 보고서는 제품별(시스템, 소모품, 시약), 검사 유형별(CBC, 헤모글로빈/헤마토크리트, 기타), 기술별(임피던스식, 광학/이미징식, 기타), 최종 사용자별(병원, 응급실, 진단 실험실, 혈액은행, 외래 진료 센터), 지역별(북미, 유럽, 기타)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 현장 진단 혈액 검사 분야의 AI 시장 동향 및 인사이트

급성기 및 외래 진료에서 신속한 병상side CBC에 대한 수요

응급의료 및 외래 진료 팀이 치료 방침을 결정하기 위해 즉각적인 혈액 검사 결과가 필요하기 때문에 신속한 병상 혈액 검사가 필수적이어지고 있습니다. 현장 혈액 검사 분야의 AI 시장은 이러한 수요의 혜택을 누리고 있으며, 고급 분석 장비가 손가락 끝에서 채취한 혈액이나 소량의 검체를 통해 몇 분 만에 다항목 혈액 검사 결과를 제공합니다. 이 기능은 지연으로 인해 환자 흐름이 방해받고 재진료 횟수가 늘어날 가능성이 있는 종양학 후속 관리, 면역억제 환자 모니터링, 응급 분류 분야에서 특히 큰 효과를 발휘합니다. 환자 곁에서 사용할 수 있는 AI 탑재 검사 장비의 도입은 분산형 진단으로의 전환을 부각시키고 있으며, 보다 신속하고 효율적인 의사결정을 가능하게 하고 있습니다. 의료진은 또한 이 기술을 활용하여, 기존에는 중앙 검사실에 의존하던 일상적인 혈액 모니터링을 진료 현장으로 옮기고 있습니다.

빈혈, 감염증, 혈액 질환으로 인한 부담 증가

빈혈, 감염증, 암 사례, 혈액 질환의 유병률 증가는 현장 진단 혈액 검사 분야에서 AI에 대한 수요를 촉진하고 있습니다. 소아 종양학 분야에서 AI 지원형 분석 장치의 임상 검증 결과, 98.9%를 상회하는 분류 정확도와 0.95 이상의 코헨 카파 계수가 확인되어, 빈번하게 시행되는 검사에서의 신뢰성이 입증되었습니다. 이러한 시스템은 비용 면에서도 이점을 제공하기 때문에 클리닉이나 자원이 제한된 환경에 적합합니다. 또한, 패혈증 분류용 AI 장치는 기존 바이오마커에 비해 뛰어난 성능을 보여주고 있으며, 세균성 감염증에서 AUROC 0.83을 달성하고, 중환자실 수준의 치료에 대한 민감도도 향상시켰습니다. 이러한 발전 덕분에 일상 진료와 중환자 치료 두 분야 모두에서 AI 도구에 대한 신뢰도가 높아지고 있습니다.

중앙 검사실의 워크플로우와 정확도 검증 간의 차이

현장 혈액 검사 분야의 AI 시장에서 중요한 과제는 모세혈관 검사나 현장 검사의 결과가 고처리량 중앙 검사실 시스템의 신뢰성 기준을 충족하도록 보장하는 것입니다. 높은 일치율이 나타났음에도 불구하고, 인증된 보고 환경에서는 검사법의 비교, 정확도 평가, 시설 간 일관된 근거가 요구됩니다. 상업적 도입은 확립된 검사실 품질 기준에 대한 검증에 달려 있으며, ISO 15189 준수가 이를 더욱 복잡하게 만들고 있습니다. 소규모 기업은 대규모 검증 프로그램을 뒷받침할 자원이나 인프라가 부족한 경우가 많아, 시장 진입이 지연된다는 과제에 직면해 있습니다.

부문별 분석

2025년에는 시스템이 매출의 38.2%를 차지했으며, 제품 구성을 주도했습니다. 이는 설비 투자 동향과 병원 내 검증 완료된 분석 장비 플랫폼에 대한 수요를 반영한 것입니다. 시스템 부문은 병원의 조달 주기와 서비스 계약의 혜택을 받고 있으며, 워크플로우에서 소모품의 선정은 대개 장비 도입에 따라 결정됩니다. 소모품 및 시약은 2031년까지 연평균 성장률(CAGR) 25.05%라는 견조한 성장이 예상됩니다. 이는 정기적인 지출을 개별 검사 항목으로 전환하는 카트리지 기반 및 폐쇄형 테스트 설계에 의해 주도되고 있습니다.

2025년에는 전혈구계수(CBC) 검사가 검사 유형별 매출의 39.78%를 차지했으며, 현장 진단 혈액 검사 분야의 AI 시장에서 검사 건수 측면에서 핵심적인 위치를 유지했습니다. 감염증 평가, 빈혈 정밀 검사, 종양 모니터링, 수술 전 선별 검사 등 CBC의 폭넓은 임상적 활용이 해당 시장에서 그 우위를 뒷받침하고 있습니다. 빈혈 선별 검사 및 겸상적혈구증 모니터링에 따른 수요에 힘입어 헤모글로빈 및 헤마토크리트 검사는 2031년까지 연평균 성장률(CAGR)이 25.76%를 나타낼 것으로 예측되며, 가장 빠르게 성장하는 검사 유형입니다.

지역별 분석

2025년, 북미는 현장 혈액 검사 분야의 AI 시장에서 매출의 44.32%라는 압도적인 점유율을 차지했습니다. 이러한 선도적 지위는 견고한 규제 체계, 환자 인근 검사 비용에 대한 보험 적용 확대, 병원 및 외래 진료에 대한 막대한 투자에 의해 뒷받침되고 있습니다. 2026년 2월, CLIA 면제 절차를 통해 ‘Athelas Home’이 인가를 받음으로써 분산형 의료 환경에서 AI를 활용한 검사가 가능해졌으며, 이 지역의 위상이 한층 더 강화되었습니다. 환자의 신속한 치료 경로 결정과 모니터링의 신속화에 주력하는 북미는 이 부문의 혁신을 위한 중요한 도입 시장으로 계속 자리 잡고 있습니다.

유럽은 도입 과정에서 중요한 역할을 하고 있지만, 그 속도는 국가나 의료 환경에 따라 다릅니다. 서유럽 시장에서는 AI를 활용한 디지털 형태 진단 및 워크플로우 현대화가 진행되고 있지만, 중동 및 아프리카에서는 도입이 아직 초기 단계에 머물러 있습니다. 2026년 2월, Scopio Labs의 AI 탑재 플랫폼이 EU IVDR 규정에 따라 인증을 받음에 따라 EU 전역에서 사용할 수 있게 되었습니다. 유럽 내 이 시장의 성장은 병원과 검사실이 시범 프로그램에서 일상적인 업무 흐름으로 전환하는 속도에 달려 있습니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR) 27.25%라는 견조한 성장이 예상되며, 현장 혈액 검사 분야의 AI 시장에서 가장 빠르게 성장하는 지역이 될 전망입니다. 이러한 성장은 의료의 분산화, 지역 진단에 대한 수요 증가, 지역의 요구에 부응하는 현지 제조업체의 존재에 힘입어 이루어지고 있습니다. 일본의 업무 혁신은 이러한 추세를 여실히 보여주고 있으며, 검사 업무에 AI 솔루션을 도입한 결과 효율성이 대폭 향상되었다고 보고되고 있습니다. 또한, 보다 간소화된 현장 진단 플랫폼은 검사 시설 이용이 제한된 지역의 서비스 격차 해소에도 기여하고 있으며, 지역 클리닉과 1차 진료 네트워크는 신흥 지역에서의 도입을 위한 중요한 관문이 되고 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.24According to Mordor Intelligence, the aI in point-of-Care hematology market size is projected to expand from USD 0.39 billion in 2025 and USD 0.49 billion in 2026 to USD 1.45 billion by 2031, registering a CAGR of 24.25% between 2026 to 2031.

This report is Segmented by Product (Systems, Consumables and Reagents), Test Type (CBC, Hemoglobin/Hematocrit, and More), Technology (Impedance-Based, Optical/Imaging-based, and More), End User (Hospitals, Emergency Departments, Diagnostic Laboratories, Blood Banks, Ambulatory Centers), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global AI In Point-of-Care Hematology Market Trends and Insights

Rapid Bedside CBC Demand in Acute and Ambulatory Care

Rapid bedside hematology is becoming critical as emergency and ambulatory teams require immediate blood count results to make treatment decisions. The AI in point-of-care hematology market is benefiting from this demand, with advanced analyzers delivering multi-parameter blood counts from fingerstick or low-volume samples in minutes. This capability is particularly impactful in oncology follow-ups, monitoring immunosuppressed patients, and urgent triage, where delays can disrupt patient flow and increase repeat visits. The introduction of AI-supported testing devices for near-patient use highlights the shift toward decentralized diagnostics, enabling faster and more efficient decision-making. Providers are also leveraging this technology to transition routine blood monitoring to care sites previously reliant on central laboratories.

Rising Burden of Anemia, Infection, and Hematologic Disease

The growing prevalence of anemia, infections, oncology cases, and hematologic diseases is driving demand for AI in point-of-care hematology. Clinical validation of AI-supported analyzers in pediatric oncology demonstrated over 98.9% classification accuracy and Cohen's kappa values above 0.95, proving their reliability in high-frequency testing. These systems also offer cost advantages, making them suitable for clinics and resource-limited settings. Additionally, AI devices for sepsis triage have shown superior performance compared to traditional markers, achieving a bacterial infection AUROC of 0.83 and enhanced sensitivity for ICU-level care. These advancements are building trust in AI tools for both routine and critical care applications.

Accuracy Validation Gap Versus Central Laboratory Workflows

A critical challenge in the AI-driven point-of-care hematology market is ensuring that capillary or point-of-care test results meet the reliability standards of high-throughput central laboratory systems. Despite strong concordance results, accredited reporting environments demand method comparisons, precision assessments, and consistent evidence across sites. Commercial adoption depends on validation against established laboratory quality benchmarks, and compliance with ISO 15189 adds complexity. Smaller companies face hurdles as they often lack the resources or infrastructure to support extensive validation programs, slowing their market entry.

Other drivers and restraints analyzed in the detailed report include:

- Miniaturized Cartridge and Capillary Sampling Adoption

- Expansion of Decentralized Diagnostics in APAC and Emerging Markets

- LIS Interoperability and Cybersecurity Compliance at Decentralized Sites

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, systems dominated the product structure with 38.2% of revenue, reflecting capital spending trends and the demand for validated analyzer platforms in hospitals. The systems category benefits from hospital procurement cycles and service contracts, with instrument placement often determining consumables in workflows. Consumables and reagents are projected to grow at a robust 25.05% CAGR through 2031, driven by cartridge-based and closed-test designs that shift recurring spending to individual test events.

Complete blood count (CBC) testing contributed 39.78% of test-type revenue in 2025, maintaining its position as the volume anchor in the AI-driven point-of-care hematology market. CBC's broad clinical applications, including infection assessment, anemia workup, oncology monitoring, and pre-surgical screening, sustain its market dominance. Hemoglobin and hematocrit testing, supported by demand from anemia screening and sickle-cell monitoring, is the fastest-growing test type, with a 25.76% CAGR forecast through 2031.

Geography Analysis

In 2025, North America commanded a dominant 44.32% share of the revenue in the AI-driven point-of-care hematology market. This leadership is supported by a strong regulatory framework, enhanced reimbursement for near-patient testing, and significant investments in hospital and outpatient care. The February 2026 clearance of Athelas Home under a CLIA-waived pathway further strengthened the region's position by enabling AI-powered testing in decentralized care settings. North America's focus on faster patient routing and quicker monitoring continues to make it a key launch market for innovations in this sector.

While Europe plays a crucial role in adoption, the pace varies across nations and healthcare settings. Western European markets are advancing in AI-supported digital morphology and workflow modernization, while other regions remain in early stages of integration. The February 2026 certification of Scopio Labs' AI-powered platforms under EU IVDR regulations expanded access across the EU. Europe's growth in this market depends on how quickly hospitals and laboratories transition from pilot programs to routine workflows.

Asia-Pacific is on track to witness a robust 27.25% CAGR growth rate through 2031, making it the fastest-growing region in the AI-driven point-of-care hematology market. Growth is driven by healthcare decentralization, rising demand for community diagnostics, and local manufacturers catering to regional needs. Operational changes in Japan highlight this trend, with significant efficiency gains reported after deploying AI solutions in laboratory operations. Simpler point-of-care platforms also address service gaps in areas with limited laboratory access, while community clinics and primary care networks serve as key entry points for adoption in emerging regions.

- Abbott Laboratories

- Beckton Dickinson

- Bio-Rad Laboratories

- Boule Diagnostics

- CellaVision AB

- Diatron

- EKF Diagnostics Holdings plc

- Roche

- HemoCue AB

- HORIBA Ltd.

- Nihon Kohden

- Nova Biomedical

- PixCell Medical Technologies

- Scopio Labs

- Mindray

- Siemens Healthineers

- Sight Diagnostics

- Sysmex

- Transasia Bio-Medicals Ltd.

- Trivitron Healthcare

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid Bedside CBC Demand in Acute Care

- 4.2.2 Rising Burden of Anemia, Infection, and Hematologic Disorders

- 4.2.3 Miniaturized Cartridge and Capillary Sampling Adoption

- 4.2.4 Expansion of Decentralized Diagnostics in APAC and Emerging Markets

- 4.2.5 Morphology Workforce Shortages Favor AI-Assisted Review

- 4.2.6 Remote Telehematology and Digital Collaboration Unlock Small-Site Adoption

- 4.3 Market Restraints

- 4.3.1 Accuracy Validation Gap Versus Central Lab Workflows

- 4.3.2 High Instrument and Per-Test Consumable Costs

- 4.3.3 AI Bias Risk in Rare-Cell and Low-Prevalence Scenarios

- 4.3.4 LIS Interoperability and Cybersecurity Burdens at Decentralized Sites

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product

- 5.1.1 Systems

- 5.1.2 Consumables & Reagents

- 5.2 By Test Type

- 5.2.1 Complete Blood Count (CBC)

- 5.2.2 White Blood Cell Count / Differential

- 5.2.3 Hemoglobin / Hematocrit Testing

- 5.2.4 Anemia Screening & Triage

- 5.2.5 ESR / CRP-enabled Hematology

- 5.2.6 Digital Morphology / Peripheral Smear Review

- 5.3 By Technology & AI Capability

- 5.3.1 Impedance-based Analysis

- 5.3.2 Optical / Imaging-based Analysis

- 5.3.3 Flow cytometry-based Analysis

- 5.3.4 Microfluidic / Lab-on-Cartridge Analysis

- 5.3.5 AI-assisted Cell Classification

- 5.3.6 Others

- 5.4 By End User

- 5.4.1 Hospitals

- 5.4.2 Emergency Departments

- 5.4.3 Diagnostic Laboratories

- 5.4.4 Blood Banks & Transfusion Centers

- 5.4.5 Ambulatory / Urgent Care Centers

- 5.4.6 Others

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 Abbott

- 6.3.2 Beckman Coulter

- 6.3.3 Bio-Rad Laboratories, Inc.

- 6.3.4 Boule Diagnostics AB

- 6.3.5 CellaVision AB

- 6.3.6 Diatron

- 6.3.7 EKF Diagnostics Holdings plc

- 6.3.8 F. Hoffmann-La Roche Ltd

- 6.3.9 HemoCue AB

- 6.3.10 HORIBA Ltd.

- 6.3.11 Nihon Kohden Corporation

- 6.3.12 Nova Biomedical

- 6.3.13 PixCell Medical Technologies

- 6.3.14 Scopio Labs

- 6.3.15 Shenzhen Mindray Bio-Medical Electronics Co., Ltd.

- 6.3.16 Siemens Healthineers

- 6.3.17 Sight Diagnostics

- 6.3.18 Sysmex Corporation

- 6.3.19 Transasia Bio-Medicals Ltd.

- 6.3.20 Trivitron Healthcare

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment