|

시장보고서

상품코드

2063942

아시아태평양의 통합 시설 관리 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Asia-Pacific Integrated Facility Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

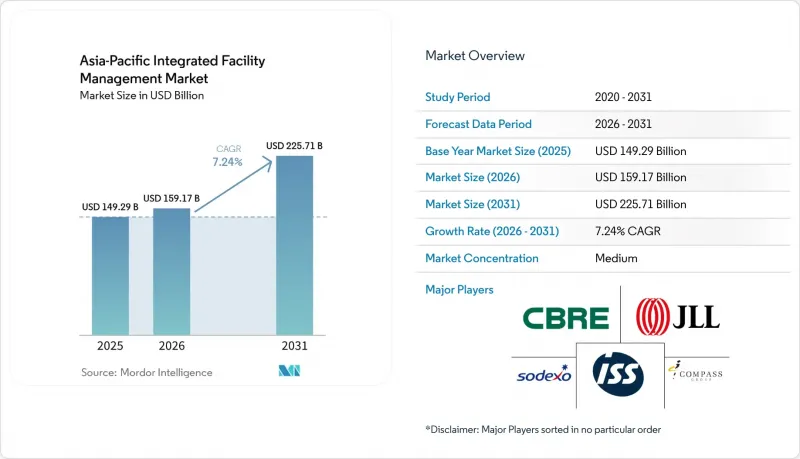

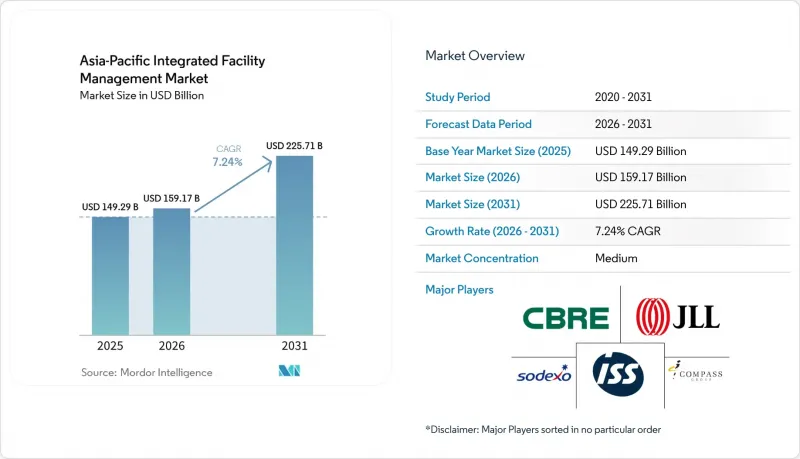

Mordor Intelligence에 의하면, 아시아태평양 통합 시설 관리 시장 규모는 2025년 1,492억 9,000만 달러에서 2026년에는 1,591억 7,000만 달러로 확대되어 2026년부터 2031년까지 CAGR 7.24%로 성장을 지속하여, 2031년에는 2,257억 1,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 서비스 유형(하드 시설 관리(자산 관리, MEP 및 HVAC 서비스 등), 소프트 시설 관리(사무 지원 및 보안, 청소 서비스, 케이터링 서비스 등)), 최종 사용자(상업, 호텔·관광, 산업 및 공정 부문 등) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

아시아태평양의 통합 시설 관리 시장 동향 및 인사이트

시설 관리 분야에서 IoT 및 스마트 빌딩 기술의 도입 확대

아시아태평양의 통합 시설 관리 시장에서 커넥티드 빌딩 시스템은 상업용 포트폴리오에서 단순한 선택적 업그레이드에서 일상적인 운영 도구로 전환되고 있습니다. 싱가포르의 ‘그린 빌딩 마스터플랜’은 건물의 성능 향상을 매우 중시하고 있으며, 이에 따라 일상 업무에서 통합적인 모니터링과 서비스 대응의 가치가 높아지고 있습니다. 또한, 기존 건축물에 대한 ‘건축물 관리법’ 개정으로 인해 운영상의 의사결정 과정에서 에너지 성능과 설비 효율이 더욱 가시화됨에 따라, 소유주는 수작업에 의한 순회 점검에만 의존하지 않고, 풍부한 데이터를 갖춘 FM 모델에 의존하게 되었습니다. 상하이의 2025년 그린빌딩 규정은 더 높은 기준 성능이 시운전부터 운영에 이르기까지 시스템 통합의 중요성을 부각시킴으로써, 이에 더욱 박차를 가하고 있습니다. 이로 인해 센서, 자산 데이터, 작업 지시서를 단일 워크플로우로 연계할 수 있는 제공업체와, 과제 기반 서비스만 제공하는 제공업체 간의 상업적 격차가 확대되고 있습니다. 도입이 확대됨에 따라, 아시아태평양의 통합 시설 관리 시장에서는 건물 데이터를 신속한 서비스 결정, 명확한 규정 준수 기록, 그리고 보다 안정적인 서비스 품질로 전환할 수 있는 사업자가 높이 평가받게 될 것입니다.

에너지 효율 및 친환경 건축 규정 준수에 대한 수요 증가

아시아태평양의 통합 시설 관리 시장의 상당 부분에서 에너지 효율은 선택적인 개선 사항이 아니라 조달 요건으로 자리 잡고 있습니다. 싱가포르의 에너지 다소비형 대형 빌딩에 적용되는 ‘의무적 에너지 개선 제도’에서는 감사와 에너지 사용 원단위의 측정 가능한 감축이 의무화되어 있으며, 이에 따라 FM 제공업체는 규정 준수 계획의 수립 및 실행에 직접 관여하게 됩니다. 현재 상하이에서는 모든 신규 민간 건물에 대해 최소 1성급 친환경 기준을 충족해야 할 의무가 있으며, 정부 및 대규모 공공 건물은 최고 등급인 3성급을 달성해야 합니다. 홍콩에서는 의무화된 에너지 감사 대상 건물을 11유형로 확대하고, 감사 주기를 5년으로 단축했습니다. 이로 인해 정기적인 기술 검토 및 후속 조치의 필요성이 커지고 있습니다. 소유주는 단순한 서비스 제공 범위뿐만 아니라 운영 개선에 대한 증명을 요구하고 있기 때문에 이러한 규제는 유지보수, 리트로커미셔닝, 디지털 보고를 하나의 계약으로 통합할 수 있는 공급자에게 유리하게 작용합니다. 그 결과, APAC(아시아태평양) 지역의 통합 시설 관리 시장에서 인증된 에너지 관리 역량을 갖춘 기업의 입찰 경쟁력이 강화되고 있습니다.

아시아태평양의 각 관할 구역마다 상이한 규제 기준이 규정 준수 비용을 증가시키고 있습니다.

아시아태평양의 관할 구역에서는 건물의 에너지 성능, 안전성, 감사 주기, 보고와 관련하여 서로 다른 규정이 적용되고 있기 때문에 국경을 초월한 FM 서비스 제공은 여전히 어려운 실정입니다. 싱가포르, 호주, 인도, 동남아시아에서 사업을 전개하는 서비스 제공업체들은 단일한 규정 준수 매뉴얼에만 의존할 수 없어, 그 결과 간접비가 증가하고 표준화가 지연되고 있습니다. 말레이시아의 스마트 빌딩 도입에 관한 조사에서도 데이터 공유 및 소유권 문제 외에도 구체적인 법적 규제 및 정책 체계의 부재가 큰 장벽으로 드러났습니다. 이러한 마찰은 클라이언트가 거점 간 일관성을 요구하는 반면, 현지 운영 규정에 따라 시장별로 맞춤화가 불가피한 지역 계약에서 가장 큰 문제가 됩니다. 단일 관할 구역 내에 머무르는 현지 사업자는 이러한 부담의 일부를 피할 수 있는 경우가 많아, 그 범위가 좁더라도 비용이 낮게 보일 수 있습니다. 기준이 더욱 통일될 때까지 APAC 지역의 IFM 시장은 중복되는 규정 준수 업무와 불균일한 운영 요건으로 인한 이익률 압박에 계속 직면할 것입니다.

부문별 분석

2025년에는 소프트 FM이 지역 수익의 61.72%를 차지했으나, 하드 FM은 2031년까지 연평균 성장률(CAGR) 7.74%로 성장할 전망입니다. 청소, 경비, 사무 지원, 급식 서비스는 노동 집약적이며, 상업시설, 공공시설, 공공기관에서 널리 외부에 위탁되고 있기 때문에 소프트 FM 서비스가 여전히 큰 비중을 차지하고 있습니다. 하지만 에너지 규제가 강화되고 설비가 복잡해짐에 따라 통합 계약에서 기술적 유지보수의 가치가 높아지고 있어, 그 균형은 변화하고 있습니다. 하드 FM은 데이터센터나 생명과학 캠퍼스 등 MEP(기계·전기·배관) 설비가 집중된 자산 증가로 인해 직접적인 혜택을 보고 있습니다. 이러한 시설에서는 일상적인 서비스 제공과 마찬가지로 가동률과 규정 준수가 중요하게 여겨지기 때문입니다. 이에 따라 아시아태평양의 통합 시설 관리 시장은 기본적인 업무 수행보다는 엔지니어링 전문성이 가격 결정력을 좌우하는 계약 형태로 점차 전환되고 있습니다.

하드 FM의 등장으로 수익 모델도 변화하고 있습니다. 왜냐하면, 예측 유지보수나 원격 감시를 통해 과거에는 정기 점검이나 고장 수리가 주를 이루던 업무에 지속적인 디지털 요소가 더해지고 있기 때문입니다. 싱가포르의 정기적인 공조 설비 감사 요건과 홍콩의 보다 광범위한 감사 범위는 모두 설비 데이터를 해석하고 이를 시정 조치로 전환할 수 있는 서비스 제공업체에 대한 수요를 높이고 있습니다. 한국에 위치한 Samsung Electronics의 ‘팩투아리 손스’ 빌딩은 통합 빌딩 제어 시스템이 에너지 소비 절감과 스마트 빌딩으로서의 신뢰성 향상을 어떻게 뒷받침할 수 있는지를 보여주고 있으며, 이는 기술력을 갖춘 운영자의 중요성을 입증하는 사례입니다. 통합 시설 관리 업계에서 현장 기술자, 에너지 관련 전문 지식, 그리고 빌딩 시스템의 가시성을 모두 갖춘 공급업체는 순수한 소프트웨어 서비스 공급업체보다 APAC(아시아태평양) 지역의 통합 시설 관리 시장에서 성장세가 빠른 분야를 선점하는 데 유리한 입장에 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHSAccording to Mordor Intelligence, the asia-Pacific integrated facility management market size is expected to grow from USD 149.29 billion in 2025 to USD 159.17 billion in 2026 and is forecast to reach USD 225.71 billion by 2031 at 7.24% CAGR over 2026-2031.

This report is Segmented by Service Type (Hard Facility Management [Asset Management, MEP and HVAC Services, and More], and Soft Facility Management [Office Support and Security, Cleaning Services, Catering Services, and More]), End User (Commercial, Hospitality, Industrial and Process Sector, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific Integrated Facility Management Market Trends and Insights

Increasing Adoption of IoT and Smart Building Technologies in Facility Management

Connected building systems are moving from optional upgrades to routine operating tools in commercial portfolios across the APAC integrated facility management market. Singapore's Green Building Masterplan places strong emphasis on better building performance, which raises the value of integrated monitoring and service response in daily operations. The Building Control Act changes for existing buildings also make energy performance and plant efficiency more visible in operating decisions, which pushes owners to rely on data-rich FM models rather than manual rounds alone. Shanghai's 2025 green building rules add further momentum because higher baseline performance standards increase the importance of system integration from commissioning through operations. This is widening the commercial gap between providers that can connect sensors, asset data, and work orders in one workflow and providers that only offer task-based delivery. As adoption broadens, the Asia-Pacific integrated facility management market is likely to reward operators that can turn building data into faster service decisions, clearer compliance records, and more stable service quality.

Rising Demand For Energy Efficiency and Green Buildings Compliance

Energy efficiency has become a procurement requirement rather than a discretionary upgrade in much of the Asia-Pacific integrated facility management market. Singapore's Mandatory Energy Improvement regime for large energy-intensive buildings requires audits and measurable reductions in energy use intensity, which brings FM providers directly into compliance planning and execution. Shanghai now requires all new civilian buildings to meet at least a one-star green standard, while government and large public buildings must reach the highest three-star level. Hong Kong has broadened mandatory energy audits to 11 building types and shortened the audit cycle to 5 years, which raises the need for recurring technical review and follow-through. These rules favor providers that can combine maintenance, retro-commissioning, and digital reporting in one contract because owners need proof of operational improvement and not only service coverage. The result is a stronger bidding position for companies with certified energy management capabilities across the APAC integrated facility management market.

Fragmented Regulatory Codes Across Asia-Pacific Jurisdictions Increasing Compliance Costs

Cross-border FM delivery remains difficult because APAC jurisdictions apply different rules for building energy performance, safety, audit cycles, and reporting. A provider serving Singapore, Australia, India, and Southeast Asia cannot rely on one compliance playbook, which raises overhead and slows standardization. Research on smart building adoption in Malaysia also identified the absence of specific legislation and policy frameworks as a major barrier, alongside data-sharing and ownership issues. These frictions matter most in regional contracts where clients want consistency across sites but local operating rules force market-by-market customization. Local operators that stay within one jurisdiction often avoid part of this burden, which can make them look cheaper even when their scope is narrower. Until standards align further, the APAC IFM market will continue to face margin pressure from duplicated compliance work and uneven operating requirements.

Other drivers and restraints analyzed in the detailed report include:

- Government Net-Zero Carbon Mandates Accelerating Retro-Commissioning Contracts

- Rapid Commercial Real Estate Growth in Tier 2 Asia-Pacific Cities

- Cybersecurity Vulnerabilities Arising From Connected Building Systems

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Soft FM accounted for 61.72% of regional revenue in 2025, while Hard FM is set to expand at a 7.74% CAGR through 2031. Soft facility management services remained the larger pool because cleaning, security, office support, and catering are labor-intensive and widely outsourced across commercial, institutional, and public facilities. Even so, the balance is shifting because energy codes and equipment complexity are increasing the value of technical maintenance inside integrated contracts. Hard FM benefits directly from the growing stock of MEP-heavy assets, including data centers and life-sciences campuses, where uptime and compliance matter as much as routine service coverage. This is pushing the Asia-Pacific integrated facility management market toward contracts where engineering depth carries more pricing power than basic task execution.

The hard FM opportunity is also changing the revenue model because predictive maintenance and remote monitoring add recurring digital layers to what used to be scheduled or break-fix work. Singapore's periodic air-conditioning plant audit requirement and Hong Kong's broader audit scope both strengthen demand for providers that can interpret plant data and translate it into corrective action. Samsung Electronics' Factorial Seongsu building in South Korea showed how integrated building controls can support lower energy use and stronger smart building credentials, which reinforces the case for technically capable operators. In the integrated facility management industry, providers that combine field technicians, energy expertise, and building systems visibility are better positioned than pure soft-service vendors to capture the faster-growing side of the APAC integrated facility management market.

List of Companies Covered in this Report:

- Sodexo SA

- CBRE Group, Inc.

- ISS A/S

- Compass Group PLC

- Jones Lang LaSalle Incorporated

- Colliers International Group Inc.

- Cushman & Wakefield plc

- Ventia Services Group

- OCS Group Limited

- Aeon Delight Co. Ltd.

- Serco Group plc

- Aramark Corporation

- Quess Corp Limited

- Aden Services

- Atalian Global Services

- Sinar Jernih Sdn Bhd

- UEMS Solutions Pte Ltd.

- NIPPON KANZAI Co., Ltd.

- Keppel Land Limited (Keppel Infrastructure Services)

- SIS Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid Commercial Real Estate Growth in Tier 2 Asian-Pacific Cities

- 4.2.2 Rising Demand for Energy Efficiency and Green Buildings Compliance

- 4.2.3 Outsourcing Trend Among Multinational Corporations for Non-Core FM Functions

- 4.2.4 Increasing Adoption of IoT and Smart Building Technologies in Facility Management

- 4.2.5 Government Net-Zero Carbon Mandates Accelerating Retro-Commissioning Contracts

- 4.2.6 Aging Building Stock Pushing Predictive Maintenance-as-a-Service Models

- 4.3 Market Restraints

- 4.3.1 Fragmented Regulatory Codes Across Asia-Pacific Jurisdictions Increasing Compliance Costs

- 4.3.2 Low Penetration of IFM in Small and Medium Enterprises Due to Cost Sensitivity

- 4.3.3 Skilled Labor Shortages in Hybrid Hard-Soft FM Roles Post-Pandemic

- 4.3.4 Cybersecurity Vulnerabilities Arising From Connected Building Systems

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Industry Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Service Type

- 5.1.1 Hard Facility Management

- 5.1.1.1 Asset Management

- 5.1.1.2 MEP and HVAC Services

- 5.1.1.3 Fire Systems and Safety

- 5.1.1.4 Other Hard Facility Management Services

- 5.1.2 Soft Facility Management

- 5.1.2.1 Office Support and Security

- 5.1.2.2 Cleaning Services

- 5.1.2.3 Catering Services

- 5.1.2.4 Other Soft Facility Management Services

- 5.1.1 Hard Facility Management

- 5.2 By End User

- 5.2.1 Commercial

- 5.2.2 Hospitality

- 5.2.3 Institutional and Public Infrastructure

- 5.2.4 Healthcare

- 5.2.5 Industrial and Process Sector

- 5.2.6 Other End-User Industries

- 5.3 By Geography

- 5.3.1 China

- 5.3.2 Japan

- 5.3.3 India

- 5.3.4 South Korea

- 5.3.5 Australia

- 5.3.6 New Zealand

- 5.3.7 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Sodexo SA

- 6.4.2 CBRE Group, Inc.

- 6.4.3 ISS A/S

- 6.4.4 Compass Group PLC

- 6.4.5 Jones Lang LaSalle Incorporated

- 6.4.6 Colliers International Group Inc.

- 6.4.7 Cushman & Wakefield plc

- 6.4.8 Ventia Services Group

- 6.4.9 OCS Group Limited

- 6.4.10 Aeon Delight Co. Ltd.

- 6.4.11 Serco Group plc

- 6.4.12 Aramark Corporation

- 6.4.13 Quess Corp Limited

- 6.4.14 Aden Services

- 6.4.15 Atalian Global Services

- 6.4.16 Sinar Jernih Sdn Bhd

- 6.4.17 UEMS Solutions Pte Ltd.

- 6.4.18 NIPPON KANZAI Co., Ltd.

- 6.4.19 Keppel Land Limited (Keppel Infrastructure Services)

- 6.4.20 SIS Limited

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment