|

시장보고서

상품코드

2063946

효소 재활용 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Enzymatic Recycling - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

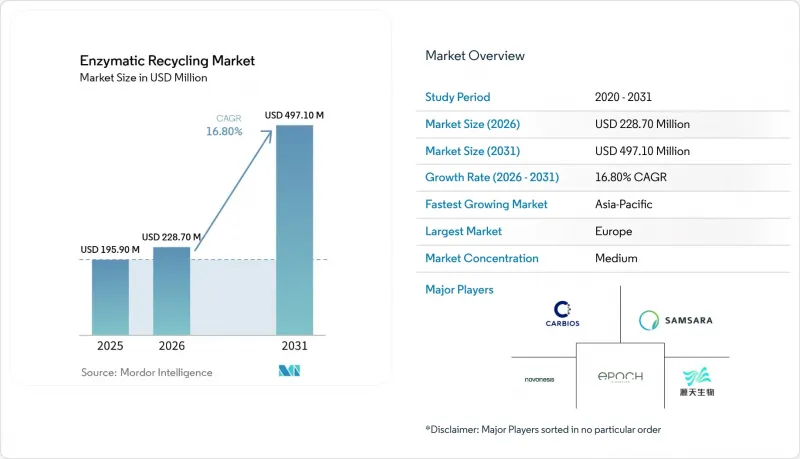

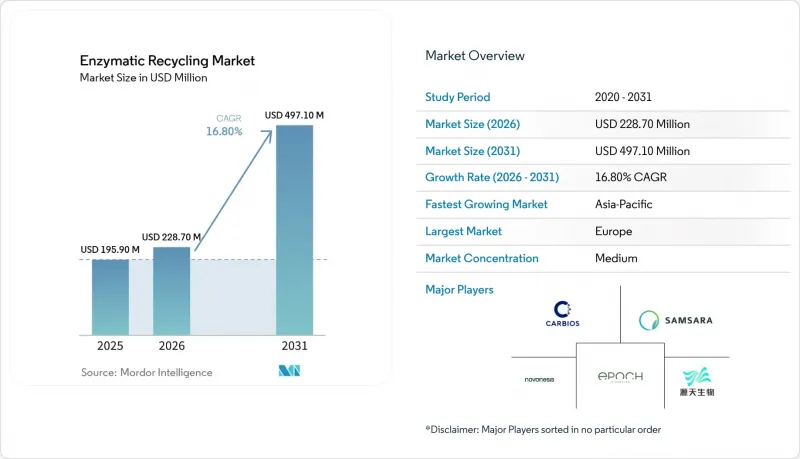

Mordor Intelligence에 의하면, 효소 재활용 시장 규모는 2025년 1억 9,590만 달러로 평가되었고, 2026년 2억 2,870만 달러로 추정되고, 2031년까지 4억 9,710만 달러로 확대될 전망이며, 2026-2031년 CAGR 16.80%를 나타낼 것으로 예측됩니다.

본 보고서는 폴리머 및 원료 유형별(폴리에틸렌 테레프탈레이트, 기타), 효소 유형별(가수분해 효소, 기타), 용도별(식음료 포장, 의류 및 섬유, 기타), 기술별(자유 효소 시스템, 고정화 효소 시스템, 기타), 지역별(북미, 유럽, 기타)로 분류되어 있습니다. 시장 전망은 금액(달러)과 수량(톤)으로 제시되어 있습니다.

세계의 효소 재활용 시장 동향 및 인사이트

기술의 발전에 따라, 버진 플라스틱 생산에 대한 경제적 우위

검토를 거친 공정 설계와 검증된 시범 테스트를 통해, 효소 재활용 폴리에틸렌 테레프탈레이트(PET)의 비용은 버진 PET와 동등하거나 그 이하로 낮아졌으며, 이에 따라 효소 재활용 시장에서의 도입이 가속화되고 있습니다. 2025년, 미국 국립재생에너지연구소(NREL)와 공동 연구진은 기질의 비정질화, 수산화암모늄을 통한 pH 조절, 회수에 필요한 에너지 수요 감소를 통해 효소 재활용 PET의 비용이 1kg당 1.51달러인 반면, 미국 내 버진 PET는 1kg당 1.87달러라고 보고했습니다. 상업적 규모에서는 사업자들이 원가 균형 범위를 예측하고 있으며, 정책에 연동된 프리미엄 및 확대 생산자 책임(EPR) 수수료 조정을 통해 실제 원료 조건 하에서도 매력적인 이익률을 확보할 수 있을 것으로 전망됩니다. 탄소 가격 책정 및 국경 조정이 확대됨에 따라, 저온에서 용매 사용량이 적은 효소 분해법은 화석 연료에 기반한 기존 기술에 비해 비교 우위를 더욱 공고히 하고 있습니다. 이러한 우위는 고정화 효소의 재사용과 결합함으로써 더욱 증폭됩니다. 이를 통해 촉매 비용을 여러 사이클에 분산시켜 반응기의 생산성을 높일 수 있기 때문입니다. 이러한 개선 사항들이 어우러져, 당초 구상은 첫 번째 상업용 플랜트에서 수익성을 확보할 수 있는 사업으로 탈바꿈했습니다.

플라스틱 폐기물 관리에 관한 엄격한 환경 규제

재활용 함량 및 생산자 책임 확대와 관련된 전 세계적인 규제 강화로 인해, 효소 재활용 시장 수요에 대한 구조적 하한선이 상향 조정되고 있습니다. EU의 일회용 플라스틱 지침에서는 PET 음료병의 재활용 함량을 2025년까지 25%, 2030년까지 30%로할 것을 의무화하고 있으며, 2025년에는 유럽 집행위원회가 병에 대한 화학적 재활용 함량 산입에 관한 협의를 시작하여, 고도 재활용에 적용될 규제 방향을 제시했습니다. 프랑스는 2025년 9월, 식품과 직접 접촉하는 포장재에 사용되는 바이오 재활용 플라스틱에 대해 톤당 1,000유로(약 1,080달러)의 인센티브를 도입하여, 식품 등급의 효소 분해 rPET의 모델화된 이익률을 개선했습니다. 중국은 2025년에 재활용 플라스틱에 관한 국가 기준과 로드맵을 수립하고, 효소 분해를 화학적 재활용의 개발 단계로 규정했습니다. 이러한 정책적 신호는 장기적인 수거를 촉진하고, 최초의 상업시설에 대한 자금 조달을 지원함과 동시에, 효소 기반 공정의 차별화된 장점인 배출량 및 순도 면에서의 이점을 강화합니다. 규제 당국이 폐기물 처리 기준 및 추적성 체계를 더욱 정교화함에 따라, 인증된 CoC(생산 이력 관리)는 효소 유래 단량체를 우선시하는 조달 기준과 직접적으로 연계될 가능성이 있습니다.

막대한 설비 투자와 긴 회수 기간

최초의 상업용 효소 분해 플랜트는 기계적 재활용 시설보다 더 많은 설비 투자가 필요하기 때문에 효소 재활용 시장에서 수익성을 확보하기 위해서는 오프테이크 계약, 정책 지원, 자금 조달을 적절히 조합하는 것이 매우 중요합니다. 카르비오스(Carbios)는 롱라빌(Longlaville) 공장 건설 비용으로 2억 3,000만 유로(약 2억 4,800만 달러)를 발표하고, 공사 완료 시기를 2026년으로 연기했습니다. 이 회사는 2028년 가동을 목표로 하고 있으나, 최종 단계의 자금 조달을 완료해야 하는 상황이며, 이는 설계·조달·시공(EPC)에 수반되는 시간적 제약을 여실히 드러내고 있습니다. 중국의 프로젝트에서는 향후 확장에 따른 위험을 완화하기 위해 설계된 1만 톤 규모의 핵심 라인을 중심으로 단계적인 설비 투자가 이루어지고 있습니다. 이러한 방식은 고정비를 분산시키는 한편, 완전한 규모의 경제 실현을 지연시키게 됩니다. 투자 회수 기간은 여전히 게이트 수수료, 효소 비용, 재생 재료 함유 프리미엄에 좌우되며, 그 결과는 규제의 지속성과 직결됩니다. 착공 전에 브랜드와 여러 해 분량의 인수 계약을 체결하면 자금 조달의 확실성은 높아지지만, 금리 변동은 여전히 프로젝트 일정에 영향을 미칩니다.

부문별 분석

PET(폴리에틸렌 테레프탈레이트)는 효소 재활용 시장을 독점하고 있으며, 2025년에는 78.2%의 시장 점유율을 차지한 것으로 평가되었습니다. 또한 효소 공정과의 높은 친화성과 확립된 회수 시스템에 힘입어 2031년까지 연평균 성장률(CAGR) 18.7%로 성장할 것으로 전망됩니다. 시장은 계속해서 PET의 에스테르 결합, 적절한 가공 조건, 품질 사양을 충족하는 병용 원료가 대량으로 안정적으로 공급되는 데 의존하고 있습니다. 지속적인 혁신을 통해 PET의 용도는 착색 PET나 섬유 유래 폐기물과 같은 더욱 복잡한 유동으로 확대되고 있으며, 효소 재활용을 통해 더 높은 회수 가치와 차별화를 실현할 수 있습니다.

동시에, 나일론 6,6 재활용 분야의 초기 개발을 비롯해 폴리우레탄 및 폴리아미드용 효소 기술의 발전으로 인해, 해당 산업의 장기적인 기질 범위는 점차 확대되고 있습니다. 그러나 이러한 분야는 여전히 초기 단계에 있으며, 효소의 안정성 및 혼합 물질의 취급과 관련된 규모 확대의 과제에 직면해 있습니다. 그 결과, PET는 당분간 가장 규모가 크고 가장 빠르게 성장하는 부문으로 자리매김하며 상용화의 기반이 되는 한편, 신흥 폴리머 유형에 대한 점진적인 다각화를 뒷받침할 것으로 예측됩니다.

2025년에는 PET에 대한 안정적인 성능과 산업적으로 실용적인 온도 범위에서의 반응 속도 향상에 힘입어, 가수분해 효소가 시장의 74.32%를 차지했습니다. 효소 재활용 시장은 지향적 진화 및 공정 정보를 반영한 설계를 통해 최적화된 쿠티나아제 및 PETase의 파생 효소로부터 지속적인 혜택을 받고 있습니다. 산화환원효소는 가장 빠르게 성장하고 있는 그룹으로, 2031년의 연평균 성장률(CAGR)은 19.2%를 나타낼 것으로 전망됩니다. 이는 사업자가 오염 물질의 전처리나 처리가 어려운 폐기물 흐름의 공동 처리를 위해 캐스케이드 반응을 검토하고 있기 때문입니다. EU 컨소시엄의 표준화된 벤치마크를 통해 실험실 간 비교 가능성이 향상되었으며, 파일럿 시스템으로의 실용화가 가속화되었습니다. 이러한 변화로 인해 가수분해 효소가 여전히 중심적인 위치를 차지하는 한편, 효소 재활용 산업 분야에서 혼합 기질 및 연속 운전용 툴킷이 확대되고 있습니다.

가수분해 효소를 대상으로 하는 효소 재활용 시장은 여전히 최대 규모를 유지하고 있지만, 산화환원 효소는 산업용 반응기에서 향후 다중 효소 아키텍처의 입지를 다져가고 있습니다. 고정화 전략은 재사용성을 높이고 촉매 활성을 안정화함으로써 천연 가수분해 효소의 장점을 보완하고, 사이클당 비용 절감을 지원합니다. 데이터셋이 축적되고 모델이 개선됨에 따라, 더 많은 효소가 산업용 인증 성능 기준을 충족하게 되어 기질 적합성과 적용 사례가 확대될 것으로 예측됩니다. 이와 동시에, 초기 상업 플랜트의 처리량 및 보존 안정성 요구 사항을 충족시키기 위해서는 공급업체의 생산 능력과 제형 기술의 발전이 필수적입니다.

지역별 분석

2025년 유럽은 38.7%의 점유율을 차지했으며, 이는 효소 재활용 시장의 세계 최초 플랜트에 대한 강력한 정책 지침과 초기 공공 자금 투입을 반영한 것입니다. PET 음료병의 재활용 재료 함유율에 관한 EU 규정과, 2025년 화학 재활용 원료 산정에 관한 협의는 첨단 재활용 기술이 기여할 수 있는 명확한 방향을 제시하고 있습니다. 식품 접촉용 포장재 분야에서 바이오 재활용 플라스틱에 대한 프랑스의 우대 조치는 식품 등급 용도의 경제성을 높여, 브랜드들의 채택을 촉진하고 있습니다. 칼비오스사는 론라빌에 위치한 연간 생산량 5만 톤 규모의 시설에 필요한 자금 조달을 추진하며, 2028년 생산 개시라는 목표를 확고히 하고, 상업화 분야에서 유럽의 선구자로서의 입지를 분명히 했습니다. WHITECYCLE 및 PET-Rezya와 같은 EU 자금 지원 프로젝트는 효소 라이브러리나 난연성 PET 등 특수 원료에 관한 국경을 초월한 협력을 심화하고 있습니다.

아시아태평양은 중국의 규격 발전, 톈진 TEDA의 섬유용 효소 PTA 신규 생산 능력, PET 해중합에 관한 전략적 라이선싱에 힘입어 2031년까지 연평균 성장률(CAGR)이 22.4%를 나타낼 것으로 예측되는 가장 빠르게 성장하는 지역입니다. 일본의 조사 결과는 매우 중요하며, PET2-21M과 관련된 내열성 효소는 적정 온도에서 높은 전환율과 확장 가능한 발현을 보여주고 있습니다. 이러한 요인들은 포장 및 섬유 부문에서 신속한 상용화를 뒷받침하는 ‘혁신에서 산업으로 이어지는 통로’를 형성하고 있습니다. 섬유 및 석유화학 밸류체인의 지역적 통합을 통해 원자재비와 물류 비용이 더욱 절감되면서, 플랜트의 가동 확대가 가속화되고 있습니다.

북미에서는 BOTTLE 컨소시엄과 미국 에너지부(DOE)의 지원에 힘입어 그 기세가 더욱 거세지고 있으며, 이로 인해 비용과 에너지 측면에서 획기적인 진전이 이루어졌습니다. 산업계, 학술 기관 및 국립 연구소의 협력을 통해 공정의 경제성이 향상되었으며, 개발자들은 2026-2028년 시범 단계에서 실증 단계로 전환하기 위한 견고한 기반을 마련하고 있습니다. 재활용 PET의 식품 접촉 용도에 대한 선행 사례는 품질이 입증되고 추적 가능성이 문서화된다면 포장 부문에서의 채택을 촉진할 것입니다. 주 차원의 EPR(확대 생산자 책임) 이니셔티브는 지속적으로 발전하고 있으며, 이러한 조화는 투자 속도와 수거 체계에 영향을 미칠 것으로 보입니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측(금액 : 달러, 수량 : 톤)

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.24According to Mordor Intelligence, the enzymatic recycling market size is projected to expand from USD 195.90 million in 2025 and USD 228.70 million in 2026 to USD 497.10 million by 2031, registering a CAGR of 16.80% between 2026 to 2031.

This report is Segmented by Polymer/Feedstock Type (Polyethylene Terephthalate and More), Enzyme Type (Hydrolases and More), Application (Food & Beverages Packaging, Clothing & Textiles, and More), Technology (Free Enzyme Systems, Immobilized Enzyme Systems, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Tons).

Global Enzymatic Recycling Market Trends and Insights

Economic Advantages Over Virgin Plastic Production as Technology Scales

Peer-reviewed process designs and validated pilots now place enzyme-recycled Polyethylene Terephthalate (PET) within or below the cost band of virgin PET, accelerating adoption in the enzymatic recycling market. In 2025, National Renewable Energy Laboratory (NREL) and collaborators reported USD 1.51 per kilogram for enzyme-recycled PET versus USD 1.87 per kilogram for United States domestic virgin PET, enabled by substrate amorphization, ammonium-hydroxide pH control, and lower energy demand for recovery. At commercial scale, operators project cost-parity ranges in which policy-linked premiums and Extended Producer Responsibility (EPR) fee modulation can secure attractive margins under real-world feedstock conditions. As carbon pricing and border adjustments expand, the comparative advantage of low-temperature, solvent-light enzymatic depolymerization grows against fossil incumbents. These gains compound when paired with the reuse of immobilized enzymes, which spreads catalyst costs across multiple cycles and increases reactor productivity. Together, these improvements turn prior aspirations into bankable economics at first-commercial plants.

Stringent Environmental Regulations on Plastic Waste Management

Tightening global rules on recycled content and extended producer responsibility are raising the structural floor for demand in the enzymatic recycling market. The EU Single-Use Plastics Directive requires 25% recycled content in PET beverage bottles in 2025 and 30% by 2030, and in 2025, the Commission opened a consultation on counting chemically recycled content in bottles, signaling regulatory pathways for advanced recycling. France added a EUR 1,000-per-tonne bonus (approximately USD 1,080 per tonne) for biorecycled plastics in sensitive-contact packaging in September 2025, improving modeled margins for food-grade enzymatic rPET. China advanced national standards and roadmaps for recycled plastics in 2025, positioning enzymatic depolymerization within chemical recycling development phases. These policy signals encourage long-term offtake, support financing for first-of-commercial facilities, and reinforce the emissions and purity advantages that differentiate enzyme-based routes. As regulators refine end-of-waste rules and traceability frameworks, certified chain-of-custody can translate directly into procurement criteria that favor enzymatic monomers.

High Capital Expenditure and Long Payback Periods

First-commercial enzymatic depolymerization plants require heavier capex than mechanical recyclers, placing a premium on offtakes, policy support, and finance blending to make returns viable in the enzymatic recycling market. Carbios disclosed EUR 230 million (approximately USD 248 million) for its Longlaville build and moved into 2026, needing to close the final portion while targeting a 2028 start, which underlines the timeframes involved in engineering, procurement, and construction. Chinese projects show staged capex with 10,000-tonne anchor lines designed to de-risk later expansions, a pattern that spreads fixed costs but delays full economies of scale. Payback horizons remain sensitive to gate fees, enzyme costs, and recycled-content premiums, which tie outcomes to regulatory continuity. Financing certainty improves when brands sign multi-year offtakes before groundbreak, yet interest-rate cycles still influence project timing.

Other drivers and restraints analyzed in the detailed report include:

- Growing Corporate Sustainability Commitments and Net-Zero Targets

- Technological Breakthroughs in Enzyme Engineering and Biocatalysis

- Competition from Established Chemical Recycling Technologies

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

PET (Polyethylene Terephthalate) dominates the enzymatic recycling market, accounting for a 78.2% market share in 2025, and is projected to grow at a CAGR of 18.7% through 2031, driven by its strong compatibility with enzymatic processes and well-established collection systems. The market continues to rely on PET's ester linkages, moderate processing conditions, and consistent availability of bottle-grade feedstocks that meet quality specifications at scale. Ongoing innovation is further expanding PET applications into more complex streams such as colored PET and textile-derived waste, where enzymatic recycling can unlock higher recovery value and differentiation.

At the same time, advancements in enzymes for polyurethane and polyamide, including early developments in nylon 6,6 recycling, are gradually expanding the industry's long-term substrate scope. However, these segments remain at an early stage and face scaling challenges related to enzyme stability and mixed-material handling. As a result, PET is expected to remain both the largest and fastest-growing segment in the near term, anchoring commercialization while supporting incremental diversification across emerging polymer types.

Hydrolases accounted for 74.32% in 2025, driven by consistent performance on PET and improved kinetics at industrially relevant temperatures. The enzymatic recycling market continues to benefit from cutinase and PETase derivatives tuned through directed evolution and process-informed design. Oxidoreductases are the fastest-growing group, with a 19.2% CAGR through 2031, as operators trial cascades to pre-treat contamination and co-process challenging waste streams. Standardized benchmarks in EU consortia improved cross-lab comparability and accelerated translation into pilot systems. These shifts keep hydrolases central while expanding the toolkit for mixed substrates and continuous operation within the enzymatic recycling industry.

The enzymatic recycling market for hydrolases remains the largest, while oxidoreductases gain ground toward future multi-enzyme architectures in industrial reactors. Immobilization strategies improve reuse and stabilize catalytic activity, complementing native hydrolase strengths and supporting a lower cost per cycle. As datasets grow and models improve, more enzymes will meet performance thresholds for industrial qualification, widening substrate compatibility and use cases. In parallel, supplier capacity and formulation advances will be essential to meet the volume and shelf-stability needs of early commercial plants.

Geography Analysis

Europe held 38.7% in 2025, reflecting strong policy mandates and early public financing for first-of-a-kind plants in the enzymatic recycling market. EU rules on recycled content in PET beverage bottles, and 2025 consultations on counting chemically recycled inputs frame a clear pathway for advanced recycling contributions. France's bonus for biorecycled plastics in sensitive-contact packaging enhances economics for food-grade applications and has supported brand adoption. Carbios advanced financing for a 50,000-tonne Longlaville facility, confirming the objective of starting production in 2028 and illustrating Europe's front-runner in commercialization. EU-funded projects such as WHITECYCLE and PET-Rezya have deepened cross-border collaboration on enzyme libraries and specialty feedstocks, such as flame-retardant PET.

Asia-Pacific is the fastest-growing region with a projected 22.4% CAGR to 2031, propelled by China's standards advances, new textile-focused enzymatic PTA capacity in Tianjin TEDA, and strategic licensing for PET depolymerization. Japan's research output has been pivotal, with PET2-21M and related heat-resistant enzymes demonstrating high conversion at moderate temperatures and scalable expression. These factors create an innovation-to-industry corridor that supports faster commercialization across packaging and textiles. Regional integration of textile and petrochemical value chains further compresses feedstock and logistics costs, which accelerates plant ramp-up.

North America is gaining momentum through the BOTTLE Consortium and DOE support, which have enabled cost and energy breakthroughs. Academic and national lab collaboration with industry has improved process economics, giving developers a stronger foundation for pilot-to-demonstration transitions through 2026-2028. Food-contact precedents for recycled PET support adoption in packaging when quality is proven, and traceability is documented. State-level EPR initiatives are evolving, and harmonization will influence investment pacing and offtake structures.

- Carbios

- Samsara Eco

- Epoch Biodesign

- Yuantian Biotechnology

- Novonesis

- Birch Biosciences

- Evoralis

- ESTER Biotech

- Landbell

- Covestro AG

- BioFuture Additives LLC

- Neoncorte Bio

- Greiner Packaging

- Vinnova

- Sustamize

- Entzimatiko

- CycleZyme

- Enzymity

- bioCIRCULAR LOOP

- Novozymes A/S

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Economic Advantages Over Virgin Plastic Production as Technology Scales

- 4.2.2 Stringent Environmental Regulations on Plastic Waste Management

- 4.2.3 Growing Corporate Sustainability Commitments and Net-Zero Targets

- 4.2.4 Technological Breakthroughs in Enzyme Engineering and Biocatalysis

- 4.2.5 Increasing Availability of Venture Capital and Strategic Funding

- 4.2.6 Rising Consumer Preference for Sustainable and Circular Products

- 4.3 Market Restraints

- 4.3.1 High Capital Expenditure and Long Payback Periods

- 4.3.2 Competition from Established Chemical Recycling Technologies

- 4.3.3 Limited Substrate Scope and Polymer Type Compatibility

- 4.3.4 Enzyme Production Costs and Supply Chain Complexities

- 4.4 Value / Supply-Chain Analysis

- 4.4.1 Biorefineries Processing Mixed Plastic-Biomass Streams

- 4.4.2 Co-production of Biofuels, Biochemicals, and Recycled Polymers

- 4.4.3 Enzymatic Upcycling to Higher-Value Specialty Polymers

- 4.4.4 Direct Polymer-to-Polymer Conversion

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

- 4.8 Impact of Artificial Intelligence-Powered Waste Collection on Service Providers' Revenue Growth

- 4.9 Consumer Behavior Shifts Toward Zero-Waste Lifestyles Influencing Service Demand

5 Market Size & Growth Forecasts (Value in USD & Volume in Tons)

- 5.1 By Polymer/Feedstock Type

- 5.1.1 PET (Polyethylene Terephthalate)

- 5.1.2 PEF (Polyethylene Furanoate)

- 5.1.3 PE (Polyethylene)

- 5.1.4 PU (Polyurethane)

- 5.1.5 Others

- 5.2 By Enzyme Type

- 5.2.1 Hydrolases

- 5.2.2 Oxidoreductases

- 5.2.3 Lyases

- 5.2.4 Isomerases/Ligases/Transferases

- 5.2.5 Others

- 5.3 By Application

- 5.3.1 Food & Beverages Packaging

- 5.3.2 Clothing & Textiles

- 5.3.3 Automotive

- 5.3.4 Construction

- 5.3.5 Consumer Goods & Electronics

- 5.3.6 Others

- 5.4 By Technology

- 5.4.1 Free Enzyme Systems

- 5.4.2 Immobilized Enzyme Systems

- 5.4.3 Whole-Cell Biocatalysis

- 5.4.4 Hybrid Processes

- 5.4.5 Others

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 Germany

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Russia

- 5.5.2.7 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 SouthEast Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines)

- 5.5.3.7 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 South Africa

- 5.5.5.5 Nigeria

- 5.5.5.6 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(Includes Global Level Overview, Market Level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)}

- 6.4.1 Carbios

- 6.4.2 Samsara Eco

- 6.4.3 Epoch Biodesign

- 6.4.4 Yuantian Biotechnology

- 6.4.5 Novonesis

- 6.4.6 Birch Biosciences

- 6.4.7 Evoralis

- 6.4.8 ESTER Biotech

- 6.4.9 Landbell

- 6.4.10 Covestro AG

- 6.4.11 BioFuture Additives LLC

- 6.4.12 Neoncorte Bio

- 6.4.13 Greiner Packaging

- 6.4.14 Vinnova

- 6.4.15 Sustamize

- 6.4.16 Entzimatiko

- 6.4.17 CycleZyme

- 6.4.18 Enzymity

- 6.4.19 bioCIRCULAR LOOP

- 6.4.20 Novozymes A/S

7 Market Opportunities & Future Outlook

- 7.1 Producer Responsibility Expansion

- 7.2 High-Priority Gap in Polyolefin Enzymes

- 7.3 Pre-Treatment Technology Gaps