|

시장보고서

상품코드

2066514

유전자 합성 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Gene Synthesis - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

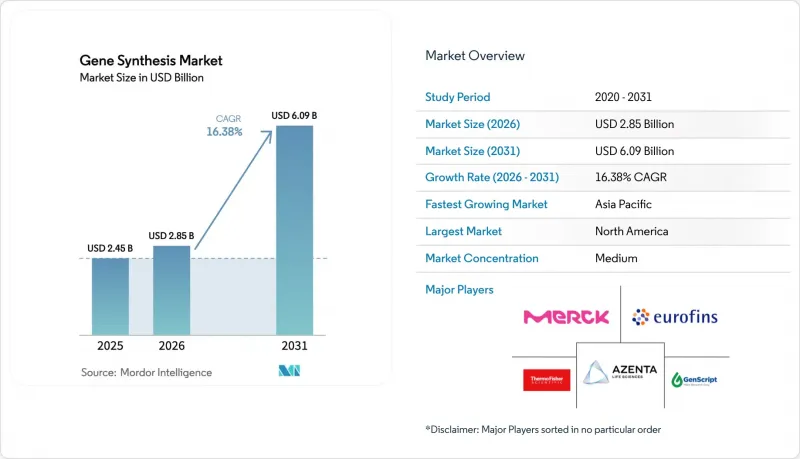

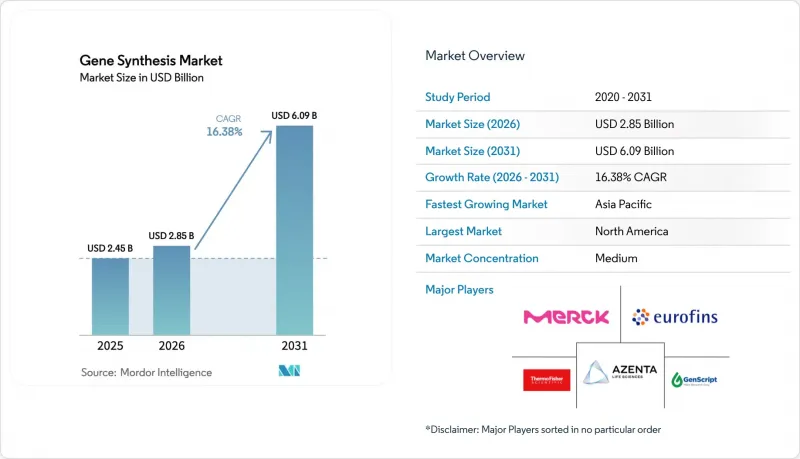

Mordor Intelligence에 의하면, 유전자 합성 시장 규모는 2025년에 24억 5,000만 달러로 평가되었고, 2026년 28억 5,000만 달러로 추정되고, 2031년까지 60억 9,000만 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 16.38%를 나타낼 전망입니다.

본 보고서는 합성 방법별(화학적 올리고뉴클레오티드 합성 및 유전자 조립(PCR 매개형 및 라이게이션 매개형)), 서비스 유형별(항체 DNA 합성 등), 용도별(유전자 및 세포 치료제 개발 등), 최종 사용자별(바이오의약품 기업 등), 지역별(북미, 유럽, 아시아태평양 등)로 분류되어 있습니다. 시장 규모 및 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 유전자 합성 시장 동향 및 인사이트

유전체학 및 NGS에 힘입어 급증하는 연구개발 파이프라인

현재 북미에서는 900건 이상의 진행 중인 임상시험에서 합성 DNA 구축체가 채택되고 있으며, 차세대 염기서열 분석(NGS)이 연구소에 더 높은 처리량의 구축 능력을 요구하도록 부추기고 있다는 사실이 부각되고 있습니다. CEPI는 DNA Script사의 템플릿 생산을 자동화하기 위해 470만 달러를 지원했으며, 이를 통해 백신 개발자들은 설계 단계에서 실험 단계로의 전환을 몇 주가 아닌 며칠 만에 완료할 수 있게 될 것입니다. 학술적 진전 또한 이러한 촉진요인을 뒷받침하고 있습니다. 하와이 대학교 연구진은 고충실도 템플릿을 사용하여 96%의 편집 성공률을 달성했으며, 합성 품질과 치료 효과 사이에 직접적인 상관관계가 있음을 입증했습니다. 또한, NHGRI가 다중 올리고 합성에 지원한 220만 달러의 연구비는 합성 DNA를 중요한 연구 인프라로 더욱 확고히 자리매김하게 할 것입니다. 이러한 요소들이 복합적으로 작용하여 샘플의 처리 대기량이 증가하고 있으며, 주문 시 오류 없는 배열을 보장할 수 있는 공급업체에게는 매우 매력적인 비즈니스 기회가 생겨나고 있습니다.

바이오의약품 분야에서 합성 유전자에 대한 수요 증가

현재 바이오의약품 파이프라인은 세포 치료제, mRNA 백신, 항체-약물 복합체(ADC)용 맞춤형 유전자에 의존하고 있습니다. FDA는 2024년에 최초의 CRISPR 유전자 편집 치료법을 포함한 5가지 유전자 치료법을 승인했는데, 이러한 승인 사례 하나하나가 고정밀도이며 바이러스 벡터와 호환되는 삽입체에 대한 상업적 수요를 입증하고 있습니다. GSK는 자사의 mRNA 백신 포트폴리오에 적합한 선형 DNA를 확보하기 위해 Elegen사에 3,500만 달러를 투자했습니다. 임상 측면에서 Casgevy는 치료를 받은 겸상적혈구증 환자의 93.5%에서 중증 혈관폐쇄성 위기를 예방했으며, 정확한 템플릿 설계가 치료 성공으로 이어진다는 사실을 입증했습니다. 투자자들의 심리가 수요를 반영한 가운데, 합성 유전체학이 전 세계적인 펩타이드 부족 현상을 해소할 것으로 기대되는 상황에서 Constructive Bio는 시리즈 A 투자 라운드에서 5,800만 달러를 조달했습니다. 이러한 진전에 따라 개발 기간이 단축되는 한편, 신뢰할 수 있는 합성 파트너를 확보하기 위한 경쟁이 치열해지고 있습니다.

숙련된 합성생물학 인재 부족

합성생물학은 분자생물학, 공학, 계산과학을 융합한 분야이지만, 많은 학술 교육 과정에서는 여전히 기존의 실험실 실습 기술이 중시되고 있습니다. NHGRI는 인력의 다양성을 촉진하기 위해 525만 달러를 배정하고 있으며, 이는 인력 부족 문제가 제도적으로 인식되고 있음을 보여줍니다. 유럽의 생명공학 산업은 GDP에 310억 유로를 기여하고 있지만, 이미 인력 부족 문제에 직면해 있어 스타트업의 규모 확대를 저해하고 있습니다. 일본의 벤처 자금 조달 규모는 미국에 비해 여전히 낮은 수준에 머물러 있지만, 그 원인 중 하나는 창업가층의 규모가 제한적이라는 점에 있습니다. 효소 플랫폼은 인을 기반으로 하는 화학에 비해 새로운 기술 역량이 필요하기 때문에 지속적인 재교육이 필수적입니다. 충분한 자격을 갖춘 인력이 확보되지 않으면 생산 라인의 가동률이 떨어질 위험이 있으며, 유전자 합성 시장의 수익 확대가 둔화될 우려가 있습니다.

부문별 분석

화학적 올리고뉴클레오티드 합성은 수십 년에 걸친 공정 최적화와 신뢰성 높은 공급망 덕분에 2025년에도 유전자 합성 시장 점유율 54.82%를 유지했습니다. 단쇄 합성에서는 고상 포스포라미다이트 반응이 여전히 표준적인 기법으로 사용되고 있으며, 마이크로칩을 활용한 접근 방식을 통해 배치 처리 능력이 향상되고 있습니다. 그러나 CRISPR 및 바이러스 벡터 분야에서 더 긴 구축체에 대한 수요가 증가하고 있는 것을 배경으로, 어셈블리 기술이 2031년까지 연평균 성장률(CAGR) 17.06%를 기록함에 따라 유전자 합성 시장은 전환기를 맞이하고 있습니다.

DNA Script사의 SYNTAX와 같은 효소 플랫폼은 몇 시간 이내에 최대 96개의 올리고뉴클레오티드를 생성하며, 유독한 용매를 사용하지 않아 연구실에서 즉시 활용할 수 있도록 합니다. Molecular Assemblies사의 완전 효소 흐름 기술은 오류율을 더욱 낮추면서 리드 길이를 연장하고 있어, 기존 방식 시장 점유율을 빼앗을 입장에 있습니다. 짧은 프라이머에는 화학 합성 방식을, 긴 유전자에는 효소를 이용한 조립 방식을 결합한 하이브리드 전략이 등장함에 따라, 유전자 합성 시장은 단일 기술로 수렴되지 않고 계속해서 다양화될 것으로 확실시되고 있습니다.

항체 DNA 합성은 항체-약물 복합체(ADC) 파이프라인의 확대와 CAR-T 세포에 대한 관심 증가로 인해 2025년 유전자 합성 시장 규모의 47.76%를 차지했습니다. mRNA 플랫폼과 바이러스 벡터가 백신 및 유전자 치료 분야를 주도하고 있는 만큼, 바이러스 유전자 합성 시장은 연평균 성장률(CAGR) 17.06%를 나타낼 것으로 전망됩니다.

CEPI의 자동 템플릿 제조에 대한 자금 지원은 백신 연구 개발 주기를 단축해야 할 전략적 시급성을 뒷받침하는 것이었습니다. 존슨앤드존슨과 GenScript 간의 승인된 CAR-T 치료법 관련 제휴는 독자적인 항체 서열이 어떻게 지속적인 수주를 창출하는지 보여주는 좋은 사례입니다. 배열 설계, 효소 합성, AI 기반 최적화를 하나의 패키지로 제공할 수 있는 서비스 제공업체는 고부가가치 계약을 수주하여 유전자 합성 시장 전체의 수익 확대에 기여할 것으로 전망됩니다.

지역별 분석

북미는 강력한 벤처 캐피털의 유입, 성숙한 바이오의약품 클러스터, 그리고 지원적인 규제 환경 덕분에 2025년 유전자 합성 시장 규모의 41.88%를 차지했습니다. NHGRI가 플랫폼 기술에 연간 150만 달러를 지원함으로써 민관 협력을 촉진하고 있는 반면, FDA의 조정된 유전자 치료 심사 절차는 규제상의 불확실성을 해소하고 있습니다. 민간 기업들도 이러한 정책에 대한 신뢰를 반영하고 있으며, 서모피셔사는 2028년까지 국내 생산 능력 확대에 20억 달러를 투자하고 있습니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR) 17.29%를 나타낼 것으로 예측되며, 유전자 합성 시장에서 가장 빠르게 성장하고 있는 지역입니다. 중국은 생명공학을 전략적 핵심 분야로 삼고, 합성유전학 벤처 기업에 막대한 보조금을 지원하고 있습니다. 인도의 ‘BioE3’ 정책은 정밀 바이오 치료제를 우선시하며, 현지 바이오 파운드리들이 전 세계 고객에게 서비스를 제공할 수 있도록 자리매김하고 있습니다. 일본은 2028년까지 민간 부문의 신약 개발 투자를 두 배로 늘릴 계획이며, 유도 만능 줄기세포(iPS 세포) 프로젝트에서는 긴 합성 염기서열이 요구되고 있습니다. 한국의 세포 치료 관련 노력은 이 지역의 성장세를 더욱 강화하고 있습니다.

유럽은 EU 바이오경제 전략 등 협력적인 정책 체계가 산업용 생명공학을 뒷받침하고 있어, 계속해서 꾸준한 성장의 원동력이 되고 있습니다. SYNBEE 보조금은 스타트업이 AI와 DNA 설계를 결합할 수 있도록 지원하고 있으며, 한편 유럽의 대형 제약사들은 안정적인 수주량을 확보하고 있습니다. 중동 및 아프리카 및 남미는 도입 주기의 초기 단계에 있지만, 의료 관련 지출 증가와 농업 생명공학에 대한 수요 증가로 인해 유전자 합성 시장의 잠재 고객 기반은 점차 확대되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.24According to Mordor Intelligence, the gene synthesis market size was valued at USD 2.45 billion in 2025 and is estimated to grow from USD 2.85 billion in 2026 to reach USD 6.09 billion by 2031, at a CAGR of 16.38% during the forecast period (2026-2031).

This report is Segmented by Synthesis Method (Chemical Oligonucleotide Synthesis and Gene Assembly[PCR-Mediated and Ligation-Mediated), Service Type (Antibody DNA Synthesis and More), Application (Gene and Cell Therapy Developments and More), End User (Biopharmaceutical Companies and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market and Forecasts are Provided in Terms of Value (USD).

Global Gene Synthesis Market Trends and Insights

Surging Genomics & NGS-Driven R&D Pipelines

More than 900 active clinical trials in North America now incorporate synthetic DNA constructs, underscoring how next-generation sequencing pushes laboratories toward higher-throughput build capabilities. CEPI has committed USD 4.7 million to automate DNA Script's template production so vaccine developers can move from design to bench in days rather than weeks . Academic progress supports the driver: University of Hawaii researchers achieved 96% editing success when using high-fidelity templates, demonstrating direct links between synthesis quality and therapeutic efficacy . NHGRI's USD 2.2 million grant for multiplex oligo synthesis further embeds synthetic DNA as critical research infrastructure. Together, these elements enlarge sample backlogs and create premium opportunities for providers able to guarantee error-free sequences on demand.

Expanding Biopharma Demand for Synthetic Genes

Biopharmaceutical pipelines now depend on custom genes for cell therapies, mRNA vaccines, and antibody-drug conjugates. The FDA cleared five gene therapies in 2024, including the first CRISPR-edited treatment, and each approval validates commercial need for precise, viral-vector-ready inserts. GSK invested USD 35 million in Elegen to secure linear DNA that fits its mRNA vaccine portfolio. Clinically, Casgevy prevented severe vaso-occlusive crises in 93.5% of treated sickle-cell patients, proving that accurate template design translates into therapeutic success. Investor sentiment mirrors demand; Constructive Bio attracted USD 58 million in Series A funding as synthetic genomics promises to ease global peptide shortages. These developments shorten development timelines and intensify competition for trustworthy synthesis partners.

Scarcity of Skilled Synthetic-Biology Workforce

Synthetic biology blends molecular biology, engineering, and computation, yet most academic curricula still emphasize traditional wet-lab skills. NHGRI earmarked USD 5.25 million to boost workforce diversity, signalling institutional recognition of the shortage. European biotechnology contributes EUR 31 billion to GDP but already suffers talent bottlenecks that curtail start-up scaling. Japan's venture funding remains low relative to the United States, partly because of limited entrepreneurial depth. Continuous retraining is essential because enzymatic platforms require new skill sets compared with phosphorus-based chemistry. Without enough qualified staff, production lines risk under-utilization, slowing revenue accrual for the gene synthesis market.

Other drivers and restraints analyzed in the detailed report include:

- Government Genomics-Funding Initiatives

- Rapid Drop in DNA-Synthesis Cost & Turnaround

- High Capital Cost for Large-Scale Synthesis Capacity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Chemical oligonucleotide synthesis retained 54.82% gene synthesis market share in 2025 thanks to decades of process optimization and reliable supply chains. Solid-phase phosphoramidite reactions remain standard for short strands, and microchip-based approaches improve batch throughput. Yet the gene synthesis market is pivoting as assembly technologies post a 17.06% CAGR through 2031, propelled by the need for longer constructs in CRISPR and viral vectors.

Enzymatic platforms such as DNA Script's SYNTAX produce up to 96 oligos within hours, offering laboratories instant access without toxic solvents. Molecular Assemblies' fully enzymatic flow technology further reduces error rates while extending read length, positioning it to steal share from incumbent methods. Hybrid strategies that combine chemical speed for short primers with enzymatic assembly for long genes are emerging, ensuring the gene synthesis market continues to diversify rather than converge on a single technique.

Antibody DNA synthesis contributed 47.76% of the gene synthesis market size in 2025 because of rising antibody-drug conjugate pipelines and CAR-T cell interest. Viral gene synthesis is set for a 17.06% CAGR as mRNA platforms and viral vectors dominate vaccine and gene-therapy arenas.

CEPI funding of automated template production confirmed strategic urgency to shorten vaccine R&D cycles. Johnson & Johnson's collaboration with GenScript on approved CAR-T therapies exemplifies how proprietary antibody sequences generate recurring orders. Service providers capable of bundling sequence design, enzymatic synthesis, and AI-based optimization stand to capture premium contracts, expanding overall revenue for the gene synthesis market.

Geography Analysis

North America commanded 41.88% of the gene synthesis market size in 2025 because of strong venture capital flows, mature biopharmaceutical clusters, and supportive regulation. The NHGRI's USD 1.5 million annual commitment to platform technologies fosters public-private partnerships, while the FDA's coordinated gene-therapy review pathway removes regulatory uncertainty. Private firms mirror policy confidence; Thermo Fisher is spending USD 2 billion on domestic capacity expansions through 2028.

Asia-Pacific is projected to log a 17.29% CAGR through 2031 and is the fastest-growing region in the gene synthesis market. China classifies biotechnology as a strategic pillar and channels generous subsidies into synthetic genetics ventures. India's BioE3 policy prioritizes precision biotherapeutics and positions local biofoundries to serve global clients. Japan plans to double private drug-discovery investment by 2028, with induced pluripotent stem-cell projects demanding long synthetic sequences. South Korea's cell-therapy initiatives further reinforce regional momentum.

Europe remains a steady growth contributor as coordinated policy frameworks such as the EU Bioeconomy Strategy back industrial biotechnology. SYNBEE grants help startups combine AI and DNA design, while the continent's pharmaceutical giants deliver consistent order volumes. Middle East and Africa along with South America are early in adoption cycles, yet rising healthcare spending and agricultural biotech needs are widening the addressable base for the gene synthesis market.

- ATUM

- Bio Basic

- Beijing SBS Genetech Co.

- Eurofins

- Azenta Life Sciences (Genewiz)

- GenScript Biotech

- Merck KGaA (Sigma GeneArts)

- OriGene Technologies

- Thermo Fisher Scientific (GeneArt)

- Integrated DNA Technologies

- Twist Bioscience

- DNA Script

- Ansa Biotechnologies

- Evonetix

- Telesis Bio

- Synbio Technologies

- Bioneer

- ProteoGenix

- Bio-Synthesis

- ATLATL Innovations

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging genomics & NGS-driven R&D pipelines

- 4.2.2 Expanding biopharma demand for synthetic genes

- 4.2.3 Government genomics-funding initiatives

- 4.2.4 Rapid drop in DNA-synthesis cost & turnaround

- 4.2.5 Emerging enzymatic DNA-synthesis platforms

- 4.2.6 Venture-capital rush into bio-foundries & cloud labs

- 4.3 Market Restraints

- 4.3.1 Scarcity of skilled synthetic-biology workforce

- 4.3.2 High capital cost for large-scale synthesis capacity

- 4.3.3 IP-ownership uncertainty for de-novo constructs

- 4.3.4 Biosecurity & dual-use regulatory scrutiny

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porters Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Synthesis Method

- 5.1.1 Chemical Oligonucleotide Synthesis

- 5.1.1.1 Solid-Phase Phosphoramidite

- 5.1.1.2 Microchip-based Oligonucleotide Synthesis

- 5.1.2 Gene Assembly

- 5.1.2.1 PCR-mediated

- 5.1.2.2 Ligation-mediated

- 5.1.1 Chemical Oligonucleotide Synthesis

- 5.2 By Service Type

- 5.2.1 Antibody DNA Synthesis

- 5.2.2 Viral Gene Synthesis

- 5.2.3 Others

- 5.3 By Application

- 5.3.1 Gene and Cell Therapy Developments

- 5.3.2 Vaccine Development

- 5.3.3 Disease Diagnosis

- 5.3.4 Others

- 5.4 By End User

- 5.4.1 Biopharmaceutical Companies

- 5.4.2 Academic & Government Institutes

- 5.4.3 CROs and CDMOs

- 5.4.4 Others

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 ATUM (DNA2.0 Inc.)

- 6.3.2 Bio Basic Inc.

- 6.3.3 Beijing SBS Genetech Co.

- 6.3.4 Eurofins Genomics

- 6.3.5 Azenta Life Sciences (Genewiz)

- 6.3.6 GenScript Biotech

- 6.3.7 Merck KGaA (Sigma GeneArts)

- 6.3.8 OriGene Technologies

- 6.3.9 Thermo Fisher Scientific (GeneArt)

- 6.3.10 Integrated DNA Technologies

- 6.3.11 Twist Bioscience

- 6.3.12 DNA Script

- 6.3.13 Ansa Biotechnologies

- 6.3.14 Evonetix

- 6.3.15 Telesis Bio

- 6.3.16 Synbio Technologies

- 6.3.17 Bioneer

- 6.3.18 ProteoGenix

- 6.3.19 Bio-Synthesis Inc.

- 6.3.20 ATLATL Innovations

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment