|

시장보고서

상품코드

2064015

유럽의 고출력 LED 패키지 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Europe High-Power LED Package - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

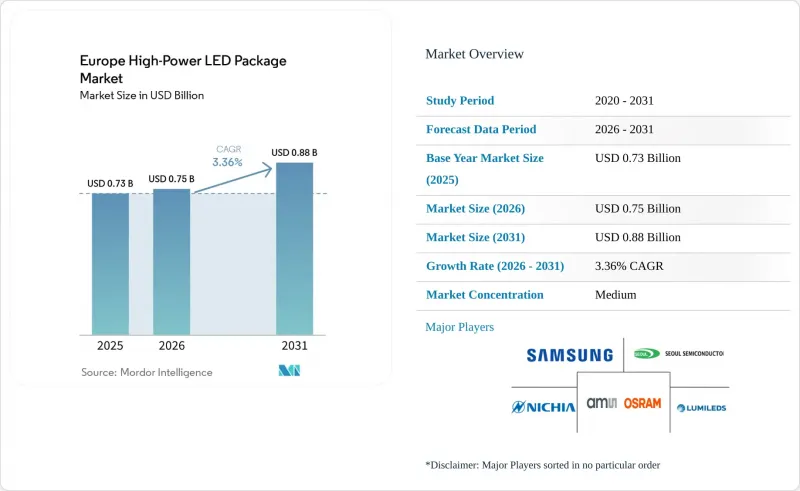

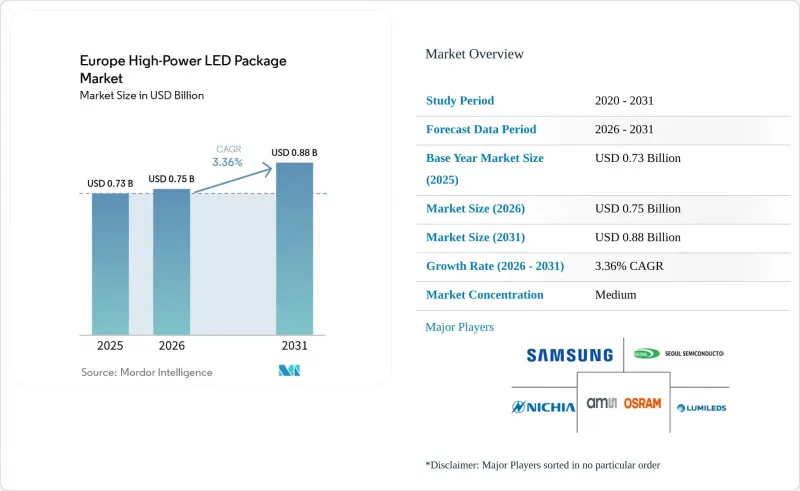

Mordor Intelligence에 의하면, 유럽 고출력 LED 패키지 시장 규모는 2025년에 7억 3,000만 달러로 평가되었고 2026년 7억 5,000만 달러에서 2031년까지 8억 8,000만 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 3.36%를 나타낼 전망입니다.

본 보고서는 출력 범위(1W-3W, 3W-10W, 10W 이상), 아키텍처(싱글 다이 패키지, 멀티 다이 패키지 등), 용도(일반 조명, 자동차용 조명, 디스플레이 및 백라이트 등), 그리고 국가(영국, 독일 등)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

유럽 고출력 LED 패키지 시장 동향 및 인사이트

고출력 패키지의 $/lm(루멘당 가격)의 급격한 하락

중국의 갈륨 질화물 웨이퍼 공급 과잉과 형광체 변환 효율의 향상이 맞물리면서, 고출력 LED 패키지의 가격은 연간 약 15% 하락하고 있습니다. 유럽의 조명 기구 제조업체들은 발광 소자의 수를 줄이고 더 밝은 소자를 채택한 설계로 전환하고 있으며, 이로 인해 부품 비용은 절감되는 반면 공급업체의 이익률은 줄어들고 있습니다. 형광체의 지적 재산권(IP)을 보유한 수직 통합형 공급업체는 웨이퍼 가격 변동을 상쇄할 수 있지만, 반면 범용 조립업체는 즉시 상품화 문제에 직면하게 됩니다. 2025년 2월에 출시된 Lumileds사의 LUXEON HL2X-V는 접합부 온도 85℃에서 200 lm/W를 달성함으로써, 산업용 하이베이 조명 개조 시 시스템 비용을 절감하여 이러한 변화를 여실히 보여주고 있습니다. 조달 부서는 표면상의 발광 효율보다 ‘1루멘당 비용’이라는 지표를 중시하는 경향이 강해지고 있으며, 이는 계약 주기의 단축과 설계 변경의 가속화로 이어지고 있습니다.

중국과 일본에서 자동차용 LED 보급률의 급증

중국 승용차의 LED 보급률은 2025년에 70%를 넘어설 전망이며, 일본에서는 2025년 3월에 초박형 헤드램프용 마이크로 LED 어레이가 승인되었습니다. 현재 유럽의 자동차 제조업체들은 EU 안전 기준을 충족하고 프리미엄 등급의 차별화를 꾀하기 위해 이러한 아키텍처를 도입하고 있으며, 칩 온 보드(COB) 모듈이 해당 지역공급망에 통합되어 있습니다. 포르비아 산하의 헤라는 전기차의 에너지 소비를 40% 절감하는 질화갈륨-실리콘카바이드 패키지를 바탕으로, 2023년 조명 부문 매출이 30억 유로(33억 9,000만 달러)에 달했으며, 유럽 프리미엄 헤드램프 시장에서 25%의 점유율을 확보했다고 발표했습니다. 그러나 아시아의 비용 기준이 유럽 내 협상의 틀이 되고 있어, 공급업체들은 더욱 엄격한 비닝 기준과 신뢰성 지표를 충족하면서도 아시아태평양의 단위 경제성에 맞추어야만 하는 상황에 처해 있습니다.

치열한 경쟁으로 인한 이익률 하락

가동률 85% 이상으로 운영되는 중국의 파운드리 업체들은 유럽 가격보다 최대 30% 낮은 가격을 책정함으로써, 매출 총이익률을 지속 가능한 수준 이하로 떨어뜨리고 있습니다. 2025년 8월 루미레즈가 산안 광전자(San'an Optoelectronics)에 2억 3,900만 달러에 매각된 사례는 업스트림 공정의 웨이퍼 통합이 가져다주는 생존 경쟁 우위를 여실히 보여주고 있습니다. 그 때문에 유럽공급업체들은 AEC-Q102 인증을 받은 자동차용 패키지, 원예용 스펙트럼, 초고 CRI 박물관용 모듈과 같은 틈새 시장으로 발을 빼고 있습니다. 그러나 생산량 감소는 고정비 충당을 제한하여, 이익률에 대한 지속적인 압박과 방어적 통합이라는 악순환을 초래하고 있습니다.

부문별 분석

10W를 초과하는 패키지는 2031년까지 연평균 성장률(CAGR) 3.98%로 성장하고 있으며, 현재 유럽의 고출력 LED 패키지 시장을 독점하고 있는 저출력 등급을 상회하고 있습니다. 2025년에 47.13%의 점유율을 차지한 1W-3W 대역은 비용과 형상의 적합성이 구매 결정 요인이 되는 일반 조명 개조 용도에서 여전히 인기를 끌고 있습니다. 그러나 2025년까지 대규모 창고와 사무실의 대부분에서 LED로의 전환이 완료되었고, 현재는 교체 주기에 접어들었기 때문에 성장세가 둔화되고 있습니다. 3W-10W급 패키지는 자동차 주간 주행등 및 가로등에 적용되며, 루멘 출력과 관리 가능한 열 부하 간의 균형을 맞추고 있습니다.

GaN-on-SiC 기판 및 2상식 베퍼 챔버 분야의 기술적 돌파구 덕분에, 200 W/cm²의 광속 하에서도 접합부 온도를 125 °C 이하로 억제할 수 있게 되어, 10 W를 초과하는 모듈이 경기장 투광 조명이나 항만 크레인용 조명 기구에 보급되고 있습니다. Lumileds사의 LUXEON HL2X-V는 이러한 변화를 상징하는 제품으로, 12% 더 높은 발광 효율과 감소된 열저항을 동시에 실현하고 있습니다. IEC 62471 규격에서는 청색 성분이 많은 스펙트럼에 대한 구동 전류의 상한이 규정되어 있으며, 이로 인해 절대 효율에 제한이 가해지기 때문에 공급업체들은 목표 휘도를 유지하면서 위험 그룹 1의 요건을 충족할 수 있도록 형광체 배합을 조정하고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.23According to Mordor Intelligence, the europe high-Power lED package market size was valued at USD 0.73 billion in 2025 and is estimated to grow from USD 0.75 billion in 2026 to reach USD 0.88 billion by 2031, at a CAGR of 3.36% during the forecast period (2026-2031).

This report is Segmented by Power Range (1 W To 3 W, 3 W To 10 W, and Above 10 W), Architecture (Single-Die Packages, Multi-Die Packages, and More), Application (General Lighting, Automotive Lighting, Display and Backlighting, and More), and Country (United Kingdom, Germany, and More). The Market Forecasts are Provided in Terms of Value (USD).

Europe High-Power LED Package Market Trends and Insights

Rapid Decline in $/lm for High-Power Packages

High-power LED package prices are falling roughly 15% a year as oversupply in China's gallium-nitride wafer capacity converges with efficiency gains in phosphor conversion. European luminaire makers are redesigning fixtures around fewer, brighter emitters, cutting bill-of-materials costs but shrinking supplier margins. Vertically integrated vendors that own phosphor IP can absorb wafer volatility, whereas merchant assemblers face immediate commoditization. Lumileds' LUXEON HL2X-V, launched February 2025, underscores this shift by delivering 200 lm W-1 at 85 °C junction temperature and lowering system cost for industrial high-bay retrofits. Procurement teams increasingly emphasize dollar-per-lumen benchmarks over headline efficacy, tightening contract cycles and accelerating design revisions.

Soaring Automotive LED Penetration in China and Japan

LED penetration in Chinese passenger cars topped 70% in 2025, and Japan cleared micro-LED arrays for ultrathin headlamps in March 2025. European automakers are now importing these architectures to meet EU safety rules and differentiate premium trims, bringing chip-on-board modules into regional supply chains. Hella, part of Forvia, cited lighting revenue of EUR 3 billion (USD 3.39 billion) for 2023 and a 25% share of Europe's premium headlamp segment, on the back of gallium-nitride-on-silicon-carbide packages that cut EV energy draw by 40%. Asian cost baselines, however, frame European negotiations, forcing suppliers to match APAC unit economics while meeting stricter binning and reliability metrics.

Margin Erosion from Intense Price Competition

Chinese foundries running at 85%+ utilization undercut European pricing by up to 30%, compressing gross margins below sustainable thresholds. Lumileds' August 2025 sale to San'an Optoelectronics for USD 239 million illustrated the survival advantage of upstream wafer integration. European vendors, therefore, retreat to niches such as AEC-Q102-qualified automotive packages, horticulture spectra, and ultra-high-CRI museum modules. Yet lower volume limits fixed-cost absorption, creating a feedback loop of continuing margin pressure and defensive consolidation.

Other drivers and restraints analyzed in the detailed report include:

- Energy-Efficiency Mandates Across ASEAN

- Industrial Retrofits to High-Bay LED Fixtures

- Volatile Sapphire Substrate Supply

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Above-10-W packages are advancing at a 3.98% CAGR to 2031, outpacing lower-power classes that currently dominate the Europe high-power LED package market. The 1 W-3 W bracket, which held a 47.13% share in 2025, remains popular for general lighting retrofits, where cost and form-factor familiarity drive purchasing. Growth, however, is flattening as most large warehouses and offices have completed LED conversions by 2025 and now enter replacement cycles. Packages in the 3 W-10 W tier support automotive daytime running lamps and streetlights, balancing lumen output against manageable heat loads.

Technology breakthroughs in GaN-on-SiC substrates and two-phase vapor chambers now keep junction temperatures below 125 °C at 200 W cm-2 flux, enabling above-10-W modules to invade stadium floodlighting and port-crane luminaires. Lumileds' LUXEON HL2X-V exemplifies this shift, pairing 12% higher efficacy with reduced thermal resistance. IEC 62471 rules that cap drive currents for blue-rich spectra impose limits on absolute efficacy, prompting suppliers to tweak phosphor blends to meet Risk Group 1 while preserving target brightness.

List of Companies Covered in this Report:

- Nichia Corporation

- ams-OSRAM AG

- Seoul Semiconductor Co., Ltd.

- Lumileds Holding B.V.

- Samsung Electronics Co., Ltd.

- Cree LED, Inc.

- Everlight Electronics Co., Ltd.

- LG Innotek Co., Ltd.

- Lextar Electronics Corporation

- Broadcom Inc.

- Brightek Optoelectronic Co., Ltd.

- Dominant Opto Technologies Sdn. Bhd.

- Stanley Electric Co., Ltd.

- Lite-On Technology Corporation

- Refond Optoelectronics Co., Ltd.

- Hongli Zhihui Group Co., Ltd.

- NationStar Optoelectronics Co., Ltd.

- TDK Electronics AG

- Wurth Elektronik GmbH & Co. KG

- Vishay Intertechnology, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid Decline in $/lm for High-Power Packages

- 4.2.2 Soaring Automotive LED Penetration in China and Japan

- 4.2.3 Energy-Efficiency Mandates Across ASEAN

- 4.2.4 Industrial Retrofits to High-Bay LED Fixtures

- 4.2.5 Thermal-Management Breakthroughs Enabling 10 W+ Packages*

- 4.2.6 India's PLI Incentives for GaN-on-SiC LED Foundries*

- 4.3 Market Restraints

- 4.3.1 Margin Erosion from Intense Price Competition

- 4.3.2 Volatile Sapphire Substrate Supply

- 4.3.3 Photobiological Safety Norms Limiting Drive Current

- 4.3.4 Inadequate End-of-Life Recycling Streams*

- 4.4 Regulatory Landscape

- 4.5 Impact of Macroeconomic Factors

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS

- 5.1 By Power Range

- 5.1.1 1 W - 3 W

- 5.1.2 3 W - 10 W

- 5.1.3 Above 10 W

- 5.2 By Architecture

- 5.2.1 Single-die Packages (SMD / Discrete)

- 5.2.2 Multi-die Packages (SMD)

- 5.2.3 COB (Chip-on-Board)

- 5.2.4 Others (CSP, Flip-chip, Hybrid Modules)

- 5.3 By Application

- 5.3.1 General Lighting

- 5.3.2 Automotive Lighting

- 5.3.3 Display and Backlighting

- 5.3.4 Specialty / Niche

- 5.4 By Europe

- 5.4.1 United Kingdom

- 5.4.2 Germany

- 5.4.3 France

- 5.4.4 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Nichia Corporation

- 6.4.2 ams-OSRAM AG

- 6.4.3 Seoul Semiconductor Co., Ltd.

- 6.4.4 Lumileds Holding B.V.

- 6.4.5 Samsung Electronics Co., Ltd.

- 6.4.6 Cree LED, Inc.

- 6.4.7 Everlight Electronics Co., Ltd.

- 6.4.8 LG Innotek Co., Ltd.

- 6.4.9 Lextar Electronics Corporation

- 6.4.10 Broadcom Inc.

- 6.4.11 Brightek Optoelectronic Co., Ltd.

- 6.4.12 Dominant Opto Technologies Sdn. Bhd.

- 6.4.13 Stanley Electric Co., Ltd.

- 6.4.14 Lite-On Technology Corporation

- 6.4.15 Refond Optoelectronics Co., Ltd.

- 6.4.16 Hongli Zhihui Group Co., Ltd.

- 6.4.17 NationStar Optoelectronics Co., Ltd.

- 6.4.18 TDK Electronics AG

- 6.4.19 Wurth Elektronik GmbH & Co. KG

- 6.4.20 Vishay Intertechnology, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space And Unmet-Need Assessment