|

시장보고서

상품코드

2064016

미국의 고출력 LED 패키지 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)United States High-Power LED Package - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

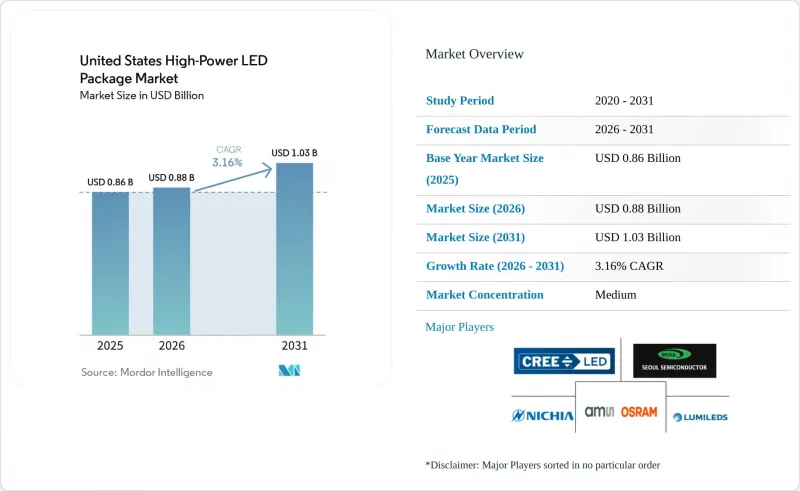

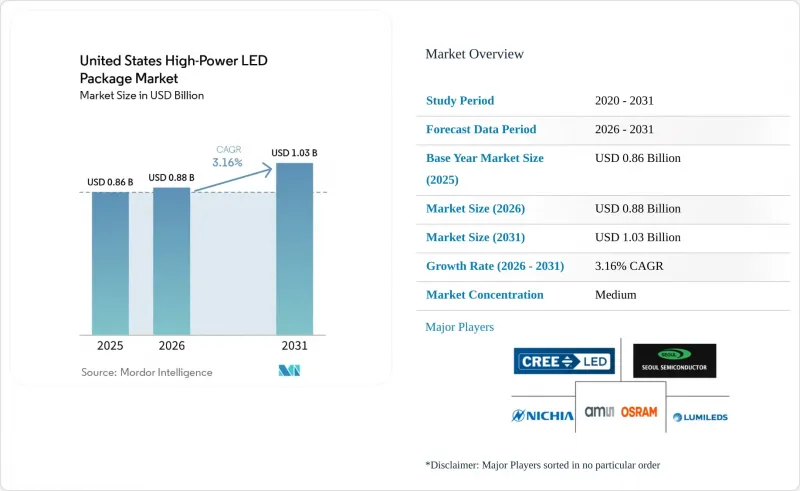

Mordor Intelligence에 의하면, 미국 고출력 LED 패키지 시장 규모는 2025년 8억 6,000만 달러에서 2026년에는 8억 8,000만 달러로 확대되어 2031년까지 10억 3,000만 달러에 이를 것으로 예측되며, 2026년부터 2031년까지 CAGR 3.16%로 성장할 전망입니다.

본 보고서는 출력 범위(1W-3W, 3W-10W, 10W 이상), 아키텍처(싱글 다이 패키지, 멀티 다이 패키지, COB 등) 및 용도(일반 조명, 자동차용 조명, 디스플레이 및 백라이트 등)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

미국 고출력 LED 패키지 시장 동향 및 인사이트

원예용 조명에 소형 고출력 LED 채택 급증

환경 제어형 농업에서 벽면 콘센트 효율이 80% 이상의 소형 LED 패키지로의 전환이 수직 농업의 경제성을 재구축하고 있습니다. 이러한 첨단 패키지는 2,000µmol m?² s?¹을 초과하는 광합성 광자 플럭스 밀도를 실현했으며, 2세대 이미터는 현재 4.1µmol J?¹이라는 놀라운 수치를 달성하고 있습니다. 그 결과, 생산자는 필요한 조명 기구의 수를 줄일 수 있고, 효율 향상으로 인해 공조 부하를 낮출 수 있으며, 18개월 미만의 투자 회수 기간을 실현할 수 있기 때문에 고성능 LED는 지속 가능한 실내 농업의 기반이 되고 있습니다.

상업용 빌딩의 리모델링 수요를 견인하는 에너지 효율 규제

미국 에너지부는 일반용 램프에 대해 1와트당 45루멘이라는 최저 기준을 설정하고 있습니다. 캘리포니아주에서는 타이틀 24의 공개 ADR 규정과 광범위한 전력회사 리베이트 제도가 결합되어, 주 인구의 78%에게 인센티브를 제공하는 데 성공했습니다. 이러한 조치로 인해 네트워크화된 조명 기기로의 전환이 크게 촉진되고 있습니다. 이러한 첨단 조명 기구에는 현재 일반적으로 수요 반응 기능을 갖춘 3-10와트짜리 패키지가 탑재되어 있습니다. 이러한 변화로 인해, 2026년 6월에 섹션 179D 공제 혜택이 종료될 전망임에도 불구하고, 초기 비용을 더 신속하게 회수할 수 있게 되었습니다.

10W를 초과할 경우 발생하는 열 관리 문제가 신뢰성을 제한합니다.

10와트 임계값을 초과하는 패키지는 알루미늄 질화물(AlN)이나 실리콘 질화물(Si3N4)과 같은 첨단 기판이 없으면 방열이 비선형적으로 이루어지기 때문에 심각한 열 관리 문제에 직면하게 됩니다. 이러한 기판이 없는 경우, 접합부 온도가 10°C 상승할 때마다 발광 효율이 약 5% 저하될 우려가 있으며, 이는 요구 사항이 까다로운 용도에서 성능을 직접적으로 저하시킬 수 있습니다. 또한, 이러한 열적 스트레스는 장기적인 신뢰성을 저해하며, LM-80 시험에서는 바람직한 50,000시간의 L90 수명을 예측하기 어려운 경우가 많기 때문에 기판 선택은 효율과 내구성을 모두 결정짓는 중요한 요소가 됩니다.

부문별 분석

2025년 기준으로, 1W-3W 패키지는 성숙한 실적와 가격 경쟁력을 중시하는 다운라이트 및 트로퍼에 힘입어 미국 고출력 LED 패키지 시장 점유율의 48.77%를 차지했습니다. 그러나 성장은 상위권으로 이동하고 있습니다. 수직 농업 및 매트릭스식 헤드램프가 우수한 광자 밀도를 추구함에 따라, 10W 초과 대역은 2031년까지 연평균 성장률(CAGR) 3.58%의 성장 궤도에 올라 있습니다. 10W 초과급 미국 고출력 LED 패키지 시장 규모는 알루미늄 질화물 기판으로 인해 발생한 40-60%의 재료비 상승을 상쇄하는 프리미엄 가격 책정의 혜택을 받고 있습니다.

캘리포니아주와 애리조나주의 환경 제어형 재배업자들은 발광 효율이 단 1퍼센트 포인트만 향상되어도 연간 에너지 비용을 8,000-1만 2,000달러 절감할 수 있기 때문에 더 높은 설비 투자를 감수하고 있습니다. 자동차 OEM 제조업체들도 비슷한 추세를 보이고 있으며, 테슬라의 2026년형 매트릭스 시스템에서는 수십 개의 고휘도 다이(die)를 채택하여 눈부심 없는 광속을 구현하고 있는데, 이는 저전력 디바이스에서는 불가능한 기능입니다. 따라서, 높은 전도성을 갖춘 기판을 확보하고 AEC-Q102 규격을 충족할 수 있는 공급업체는 범용 패키지 제조업체를 능가하고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.23According to Mordor Intelligence, the united states high-power LED package market size is expected to increase from USD 0.86 billion in 2025 to USD 0.88 billion in 2026 and reach USD 1.03 billion by 2031, growing at a CAGR of 3.16% over 2026-2031.

This report is Segmented by Power Range (1 W To 3 W, 3 W To 10 W, and Above 10 W), Architecture (Single-Die Packages, Multi-Die Packages, COB, and More), and Application (General Lighting, Automotive Lighting, Display and Backlighting, and More). The Market Forecasts are Provided in Terms of Value (USD).

United States High-Power LED Package Market Trends and Insights

Surge In Miniaturized High-Power LED Adoption For Horticulture Lighting

In controlled-environment agriculture, the shift toward compact LED packages with wall-plug efficiencies above 80% is reshaping vertical farming economics. These advanced packages deliver photosynthetic photon flux densities exceeding 2,000 µmol m-2 s-1, while second-generation emitters now achieve an impressive 4.1 µmol J-1. As a result, growers can reduce the number of fixtures required, lower HVAC loads due to improved efficiency, and realize payback periods of less than 18 months, making high-performance LEDs a cornerstone of sustainable indoor farming.

Energy-Efficiency Mandates Driving Retrofit Demand In Commercial Buildings

The Department of Energy has set a minimum standard of 45 lumens per watt for general-service lamps. In California, Title 24's open-ADR rules, combined with widespread utility rebates, have successfully incentivized 78% of the state's population. These measures have led to a significant pivot towards networked luminaires. These advanced luminaires now commonly integrate 3 to 10-watt packages equipped with demand-response capabilities. This shift is enabling quicker recovery of initial costs, even with the impending June 2026 expiration of Section 179D deductions.

Thermal Management Challenges Above 10 W Limiting Reliability

Packages that cross the 10-watt threshold face significant thermal management challenges, as heat dissipation becomes non-linear without advanced substrates like aluminum nitride (AlN) or silicon nitride (Si3N4). When these substrates are absent, the elevated junction temperatures can cause luminous efficacy to decline by roughly 5% for every 10 °C increase, which directly undermines performance in demanding applications. This thermal stress also compromises long-term reliability, with LM-80 testing often failing to project the desired 50,000-hour L90 lifetime, making substrate choice a critical determinant of both efficiency and durability.

Other drivers and restraints analyzed in the detailed report include:

- Declining Cost Of High Thermal Conductivity Substrates

- Advances In Flip-Chip Architecture Enabling Higher Lumen Density

- Patent Litigation Risk Around CSP And Flip-Chip Packages

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Packages of 1 W-3 W retained 48.77% of the United States high-power LED package market share in 2025, anchored in downlights and troffers that value mature footprints and price competition. Growth, however, is shifting upward: the above 10 W band is on a 3.58% CAGR trajectory to 2031 as vertical farms and matrix headlamps demand superior photon density. The United States high-power LED package market size for the above 10 W class benefits from premium pricing that offsets the 40-60% material uplift tied to aluminum nitride substrates.

Controlled-environment cultivators in California and Arizona tolerate higher capex because a single-percentage-point jump in efficacy can shave USD 8,000-12,000 from annual energy bills. Automotive OEMs echo this dynamic, Tesla's 2026 matrix system deploys dozens of high-flux dies to paint glare-free beams, a feature impossible with lower-wattage devices. Suppliers that can secure high-conductivity substrates and meet AEC-Q102 grades are therefore outpacing commodity package makers.

List of Companies Covered in this Report:

- Nichia Corporation

- Cree LED, an SGH Company

- Lumileds Holding B.V.

- Osram Opto Semiconductors GmbH

- Seoul Semiconductor Co., Ltd.

- Samsung Electronics Co., Ltd.

- LG Innotek Co., Ltd.

- Everlight Electronics Co., Ltd.

- Luminus Devices, Inc.

- Bridgelux, Inc.

- Lite-On Technology Corporation

- Toyoda Gosei Co., Ltd.

- Epistar Corporation

- Dominant Opto Technologies Sdn. Bhd.

- Edison Opto Corporation

- Citizen Electronics Co., Ltd.

- ProPhotonix Limited

- Crystal IS Inc.

- TT Electronics plc

- Advanced Optoelectronic Technology Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Industry Supply-Chain Analysis

- 4.3 Market Drivers

- 4.3.1 Surge in Miniaturized High-Power LED Adoption for Horticulture Lighting

- 4.3.2 Energy-Efficiency Mandates Driving Retrofit Demand in Commercial Buildings

- 4.3.3 Declining Cost of High Thermal Conductivity Substrates

- 4.3.4 Advances in Flip-Chip Architecture Enabling Higher Lumen Density

- 4.3.5 Automotive Adaptive Headlamp Regulations (FMVSS-108 Updates)

- 4.3.6 Integration of Smart Controls with High-Power LED Modules in Street Lighting

- 4.4 Market Restraints

- 4.4.1 Thermal Management Challenges Above 10 W Limiting Reliability

- 4.4.2 Patent Litigation Risk Around CSP and Flip-Chip Packages

- 4.4.3 Volatility in Gallium Nitride Wafer Pricing

- 4.4.4 Slowdown in LCD Backlight Replacement Cycle Due to OLED Penetration

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Power Range

- 5.1.1 1 W - 3 W

- 5.1.2 3 W - 10 W

- 5.1.3 Above 10 W

- 5.2 By Architecture

- 5.2.1 Single-die Packages (SMD / Discrete)

- 5.2.2 Multi-die Packages (SMD)

- 5.2.3 COB (Chip-on-Board)

- 5.2.4 Others (CSP, Flip-Chip, Hybrid Modules)

- 5.3 By Application

- 5.3.1 General Lighting

- 5.3.2 Automotive Lighting

- 5.3.3 Display and Backlighting

- 5.3.4 Specialty / Niche

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Nichia Corporation

- 6.4.2 Cree LED, an SGH Company

- 6.4.3 Lumileds Holding B.V.

- 6.4.4 Osram Opto Semiconductors GmbH

- 6.4.5 Seoul Semiconductor Co., Ltd.

- 6.4.6 Samsung Electronics Co., Ltd.

- 6.4.7 LG Innotek Co., Ltd.

- 6.4.8 Everlight Electronics Co., Ltd.

- 6.4.9 Luminus Devices, Inc.

- 6.4.10 Bridgelux, Inc.

- 6.4.11 Lite-On Technology Corporation

- 6.4.12 Toyoda Gosei Co., Ltd.

- 6.4.13 Epistar Corporation

- 6.4.14 Dominant Opto Technologies Sdn. Bhd.

- 6.4.15 Edison Opto Corporation

- 6.4.16 Citizen Electronics Co., Ltd.

- 6.4.17 ProPhotonix Limited

- 6.4.18 Crystal IS Inc.

- 6.4.19 TT Electronics plc

- 6.4.20 Advanced Optoelectronic Technology Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment