|

시장보고서

상품코드

2064371

횡단성 척수염 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Transverse Myelitis - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

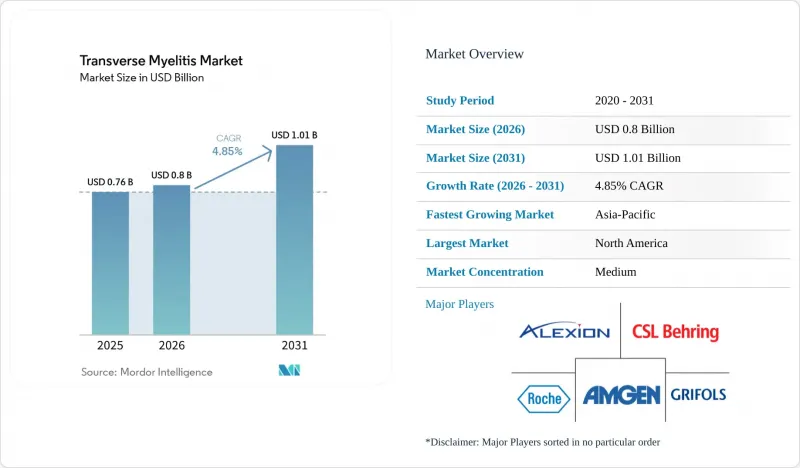

Mordor Intelligence에 의하면, 횡단성 척수염 시장 규모는 2025년 7억 6,000만 달러에서 2026년에는 8억 달러로 확대되어 2026년부터 2031년까지 CAGR 4.85%로 성장을 지속하여, 2031년까지 10억 1,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 유형별(진단(MRI, 요추 천자/뇌척수액 검사, 혈액 검사, 항체 검사), 치료법별(급성기 약물 요법, 급성기 응급 처치 등)), 원인별(특발성, 감염 후, 자가면역질환 관련 등), 최종 사용자(병원, 신경면역학 클리닉 등), 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

전 세계 횡단성 척수염 시장 동향 및 인사이트

MRI, 뇌척수액 검사, 항체 검사의 신속화로 진단까지 걸리는 기간이 단축됨

횡단성 척수염 시장은 MRI, 뇌척수액 검사 및 항체 검사를 통해 환자들이 더 조기에 명확한 치료 경로로 안내받게 됨에 따라, 진단 워크플로우의 신속화라는 이점을 누리고 있습니다. 가돌리늄을 이용한 고자기장 척추 MRI 및 STIR 시퀀싱는 NMOSD나 MOGAD를 시사하는 세로 방향으로 광범위하게 퍼진 병변과, 더 짧은 염증성 병변을 구별하는 데 여전히 핵심적인 역할을 하고 있습니다. 2026년에 발표된 MENACTRIMS 지침에서는 AQP4-IgG 검출에 있어 ELISA보다 세포 기반 분석법(CBA)을 공식적으로 권장했습니다. 그 이유로, CBA의 민감도가 76.7%인 반면 ELISA는 47%이며, CBA의 특이도는 100%에 달할 가능성이 있다는 점이 꼽히고 있습니다. 이러한 전환은 횡단성 척수염 시장에서 상업적으로 중요한 의미를 지닙니다. 이는 항체의 식별 정확도가 향상됨에 따라 진단이 불분명한 사례의 수가 줄어들고, 자가면역형 또는 탈수초형 아형으로 분류할 수 있는 환자의 비율이 증가하기 때문입니다. 또한, 진단이 단순한 초기 단계에 그치지 않고 의사가 일상 진료에서 활용할 수 있는 치료법으로 이어지는 직접적인 통로가 되기 때문에 검사실의 역량과 후속 치료에 대한 접근성 간의 연관성도 더욱 강화됩니다. 따라서 진단 주기의 단축은 횡단성 척수염 시장의 환자 수와 시장 규모 모두를 뒷받침하게 될 것입니다. 특히, 검사와 치료 결정이 밀접하게 연계되어 있는 3차 신경과 의료 시스템에서는 그 효과가 두드러집니다.

NMOSD 및 MOGAD에 대한 횡단성 척수염(TM) 관련 생물학적 제제의 도입이 치료 경제성을 재편하고 있습니다.

이 시장에는 주요 적응증에 대한 전용 승인 약물은 존재하지 않지만, 현재 혈청 양성 환자의 치료에 영향을 미치고 있는 NMOSD용 생물학적 제제 덕분에 치료 경제학이 재편되고 있습니다. 현재 NMOSD 치료에는 AQP4-IgG 양성 질환에 대한 에크리주맙, 라브리주맙, 이네빌리주맙, 사트랄리주맙이 포함되어 있으며, 이러한 약물은 해당 혈청학적 기준에 부합하는 횡단성 척수염 증상을 보이는 환자에서 재발 예방에 대한 기대를 바꾸었습니다. 독일의 다기관 코호트 연구에 따르면, 릿크시맙과 아자티오프린이 여전히 임상 현장에서 주요 치료 옵션으로 자리 잡고 있는 반면, 새로 승인된 치료법은 2022년까지 치료 사례의 12.3%를 차지하게 되며 그 중요성이 계속해서 커지고 있습니다. 이러한 경향은 횡단성 척수염 시장에서 더 높은 가치를 지닌 계층이 존재함을 뒷받침하고 있습니다. 왜냐하면, 혈청 양성 판정을 받은 환자는 일반적인 급성기 관리에서 더 장기간에 걸친 생물학적 제제를 이용한 유지 요법으로 전환할 수 있기 때문입니다. MOGAD의 경우, 질환 특이적인 승인이 존재하지 않으며, IL-6를 표적으로 하는 치료법에 관한 현재의 근거도 소규모 데이터 세트나 관찰 연구에 기반을 두고 있어 여전히 불확실한 부분이 있지만, 그 방향성은 명확합니다. 혈청학적 검사가 더욱 일상화됨에 따라, 횡단성 척수염 시장에서는 ‘광범위한 특발성’이라는 분류가 아닌, 명확히 정의된 신경면역학적 프로토콜에 따라 관리되는 사례가 더 큰 비중을 차지하게 될 것입니다.

횡단성 척수염에 특화된 승인된 치료법이 없습니다는 점이 보험 급여의 회색지대를 초래하고 있습니다.

횡단성 척수염을 단독 적응증으로 FDA 또는 EMA가 승인한 치료법이 존재하지 않기 때문에 시장은 여전히 구조적인 한계에 직면해 있습니다. 표준적인 급성기 치료는 여전히 고용량 메틸프레드니솔론의 정맥 내 투여에 의존하고 있으며, 중증 또는 스테로이드 저항성 발작의 경우 조기에 혈장 교환술이 시행되지만, 장기적인 생물학적 제제 치료는 순수한 횡단성 척수염(TM)이라는 진단명이 아닌, 일반적으로 NMOSD의 혈청학적 상태를 바탕으로 이루어집니다. 그 결과, 횡단성 척수염 시장 내에서는 큰 상업적 격차가 발생하고 있습니다. AQP4-IgG 양성 판정을 받은 환자는 우수한 치료 경로를 이용할 수 있는 반면, 혈청 음성 또는 원인이 불분명한 사례는 대개 효과가 낮은 스테로이드 요법이나 지지 요법의 범위를 벗어나지 못하고 있기 때문입니다. 또한, MOGAD, 전신성 자가면역 질환 또는 기타 염증성 척수증과 중복되는 사례의 경우, 치료 방침을 결정하기 위해서는 유사 질환을 충분히 확신하고 배제해야 하므로 진단 부담도 더욱 커집니다. 횡단성 척수염에 특화된 임상시험이 성공하거나, 바이오마커를 기반으로 정의된 적응증이 더욱 확대되기 전까지는 횡단성 척수염 시장이 질병 부담을 치료 수익으로 충분히 전환하지 못하는 상황이 지속될 것입니다.

부문별 분석

2025년 기준으로, 횡단성 척수염 시장의 56.31%를 진단이 차지하고 있으며, 이는 치료 방침이 확정되기 전에 모든 의심 사례가 영상 검사, 뇌척수액 검사 및 임상 검사를 거칩니다는 점을 반영한 것입니다. MRI는 여전히 핵심적인 검사 도구이며, 척수 병변의 길이, 분포, 조영제 반응 양상을 통해 단거리 염증성 병변과 NMOSD나 MOGAD를 시사하는 세로 방향으로 광범위하게 퍼진 질환을 구별하는 데 도움이 됩니다. 또한, 뇌척수액 검사 역시 여전히 핵심적인 역할을 수행하고 있는데, 이는 세포 수 증가, 올리고클로날 밴드, IgG 지수, 그리고 감염증의 배제 등이 임상 양상과 감별 진단을 계속해서 뒷받침하고 있기 때문입니다. 진단 분야에서 가장 급속한 운영상의 변화는 AQP4-IgG 및 MOG-IgG 세포 기반 분석법의 활용 확대에 의해 가져왔습니다. 이에 따라 간호는 ‘증후군’이라는 범주에서 벗어나 보다 실용적인 질환 프레임워크로 전환되고 있습니다. 따라서 횡단성 척수염 분야는 진단 측면에서 여전히 양 중심적이며, 신규 또는 재발 환자 1명당 치료의 각 단계에 걸쳐 반복적인 검사 수요가 발생하기 때문입니다.

치료 분야는 여전히 규모가 작지만, 횡단성 척수염 시장에서 가장 가치가 높은 영역인 재발 예방 체계가 정비됨에 따라 2026년부터 2031년까지 연평균 성장률(CAGR) 7.38%로 성장할 것으로 전망됩니다. 급성기 치료는 여전히 스테로이드의 정맥 내 투여를 중심으로 이루어지며, 특히 중증이나 치료 반응이 낮은 횡단성 척수염의 경우, 치료 강화를 필요로 할 때 혈장 교환 요법이나 IVIG가 시행됩니다. 유지 요법에서는 항체 양성 판정을 받은 환자가 지속적인 재발 억제가 필요할 때, 릿시맙, 아자티오프린 및 새로운 NMOSD 생물학적 제제의 사용이 확대됨에 따라 수익성이 향상됩니다. 재활 및 증상 관리도 치료 부문에 포함됩니다. 이는 지속적인 보행 장애, 방광 장애, 통증, 경련, 성기능 장애와 같은 문제로 인해 급성 염증기가 지나도 치료비 지출이 계속되기 때문입니다. 이러한 구조 덕분에 횡단성 척수염 시장은 진단 건수의 다수와 고가치의 치료 사이에서 균형을 유지하고 있으며, 분류 정확도가 향상됨에 따라 후자의 성장이 가속화될 것으로 예측됩니다.

지역별 분석

2025년 현재, 북미는 횡단성 척수염 시장 규모의 39.24%를 차지하고 있으며, 전문적인 신경면역학 치료, 첨단 MRI 이용 편의성, 그리고 광범위한 항체 검사 인프라가 이미 구축되어 있어 이 지역은 계속해서 최대의 수익원으로 자리매김하고 있습니다. 미국은 밀집된 제3신경과 네트워크와 혈청 양성 횡단성 척수염의 관리에 영향을 미치는 체계적인 NMOSD 치료 알고리즘을 조기에 도입함으로써 이러한 입지를 공고히 하고 있습니다. 또한, 이 지역에서는 MRI, 뇌척수액 검사, 수액 요법, 혈장 교환술이 동일한 병원 생태계 내에 마련되어 있을 가능성이 높기 때문에 급성기 치료의 조정도 용이합니다. CHLA와 같은 의료기관 수준의 사례는 수액 요법, 혈장 교환, 재활, 가상 진료 및 전환 계획을 연계한 통합 프로그램을 통해 북미의 횡단성 척수염 시장이 어떻게 뒷받침되고 있는지를 보여줍니다. 이러한 요인들로 인해 북미는 진단 철저도와 고부가가치 유지 요법의 도입이라는 두 가지 측면에서 우위를 유지하고 있습니다.

유럽은 횡수막염 시장에서 2위를 차지하는 지역 클러스터이지만, 보험 급여 제도와 치료 접근성은 여전히 국가마다 차이가 있습니다. 독일과 영국은 여전히 중요한 기준점이 되고 있습니다. 이는 독일 내 19개 의료기관에서 수집된 실제 임상 데이터에 따르면, 리툭시맙이 치료의 중심에 자리 잡고 있는 반면, 새로 승인된 생물학적 제제가 치료 과정에서의 점유율을 꾸준히 확대하고 있는 것으로 나타났기 때문입니다. 프랑스, 이탈리아, 스페인에서는 학술적인 신경학 네트워크와 지역 지침에 반영된 EMA(유럽의약품청) 승인 신경면역요법에 대한 접근성을 통해 환자 수가 증가하고 있습니다. 동유럽 및 남유럽에서는 여전히 진단 건수가 과소평가되고 있으며, 불가리아의 NMOSD(비특이적 다발성 경화증 유사 질환)에 관한 합의문은 실제 질병 부담이 낮음을 시사하는 것이 아니라, 역학적 가시성을 높일 필요성을 강조하고 있습니다.

아시아태평양은 횡단성 척수염 시장에서 가장 빠르게 성장하고 있는 지역으로, 2026년부터 2031년까지 연평균 성장률(CAGR) 7.83%를 나타낼 것으로 전망됩니다. 일본이 두드러지는 점은 AQP4-IgG 양성 NMOSD에서 여성 대 남성의 비율이 10 대 1에 달하기도 하는데, 이는 NMOSD 관련 횡단성 척수염 치료와 관련된 환자 집단의 규모가 크다는 것을 시사하기 때문입니다. 주외제약의 사트랄리주맙에 대한 노력 또한 현지 개발과 브랜드의 입지를 통해 이 치료 분야에서 일본의 상업적 역할을 강화하고 있습니다. 중국과 인도에서는 병원의 현대화를 통해 진단 역량이 확대되고 있지만, 인도에서는 여전히 MOG-IgG 검사의 정확도와 판정 측면에서 실무상의 과제에 직면해 있습니다. 특히, 표현형이나 MRI와의 상관관계가 충분히 고려되지 않은 채 고정된 분석법이 사용될 경우, 이러한 경향이 두드러집니다. 중동 및 아프리카는 여전히 초기 단계의 기여에 그치고 있지만, 남미에서는 학계의 참여와 면역요법에 대한 인식 확산을 바탕으로 발전하고 있으며, 성장세가 나타나고 있음에도 불구하고, 첨단 진단 기술, 생물학적 제제, 재활 치료에 대한 접근성이 고르지 않아 그 성장은 여전히 제약을 받고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.23According to Mordor Intelligence, the transverse myelitis market size is expected to grow from USD 0.76 billion in 2025 to USD 0.8 billion in 2026 and is forecast to reach USD 1.01 billion by 2031 at 4.85% CAGR over 2026-2031.

This report is Segmented by Type (Diagnosis [MRI, Lumbar Puncture/CSF Analysis, Blood Tests and Antibody Testing], Treatment Type [Acute Pharmacotherapy, Acute Rescue Procedures, and More]), Etiology (Idiopathic, Post-Infectious, Autoimmune Disease-Associated, and More), End User (Hospitals, Neuroimmunology Clinics, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Transverse Myelitis Market Trends and Insights

Faster MRI, CSF, and Antibody Workups Compress Diagnostic Timelines

The transverse myelitis market is gaining from faster diagnostic workflows because MRI, CSF studies, and antibody testing are moving patients into defined care pathways sooner. High-field spinal MRI with gadolinium and STIR sequences remains central to distinguishing shorter inflammatory lesions from longitudinally extensive disease that points toward NMOSD or MOGAD. MENACTRIMS guidance published in 2026 formally favored cell-based assay testing over ELISA for AQP4-IgG, citing 76.7% sensitivity for CBA versus 47% for ELISA and specificity that can reach 100% for CBA. That shift matters commercially in the transverse myelitis market because better antibody resolution reduces the pool of poorly defined cases and increases the share of patients who can be classified into autoimmune or demyelinating subtypes. It also strengthens the link between laboratory capability and downstream treatment access because diagnosis is no longer only an entry step, but a direct gate for the therapies physicians are able to use in routine practice. Faster diagnostic cycles therefore support both volume and value in the transverse myelitis market, especially in tertiary neurology systems where testing and treatment decisions are closely integrated.

TM-Adjacent Biologic Adoption from NMOSD and MOGAD Reshapes Treatment Economics

The market has no dedicated approved drug for the core indication, yet treatment economics are being reshaped by NMOSD biologics that now influence care for seropositive patients. Current NMOSD practice includes eculizumab, ravulizumab, inebilizumab, and satralizumab for AQP4-IgG-positive disease, and these agents have changed expectations for relapse prevention in patients whose transverse myelitis presentation falls inside that serologic framework. The German multicenter cohort showed that rituximab and azathioprine remained the dominant real-world choices, while newly approved therapies rose to 12.3% of treatment episodes by 2022 and kept gaining relevance. That pattern supports a higher-value tier inside the transverse myelitis market because confirmed seropositive patients can move from generic acute management into longer-duration biologic maintenance pathways. MOGAD remains less settled because no disease-specific approval exists and current evidence for IL-6 targeting is still based on small or observational datasets, but the direction of travel is clear. As serostatus testing becomes more routine, the transverse myelitis market is likely to see a larger share of episodes managed under defined neuroimmunology protocols rather than broad idiopathic labels.

No TM-Specific Approved Therapies Sustains a Reimbursement Gray Zone

The market still faces a structural ceiling because no FDA-approved or EMA-approved therapy exists specifically for transverse myelitis as a standalone indication. Standard acute care still relies on high-dose intravenous methylprednisolone, with plasma exchange used early for severe or steroid-refractory attacks, while long-term biologic treatment is usually tied to NMOSD serostatus rather than to a pure TM label. That leaves a large commercial divide inside the transverse myelitis market because patients with confirmed AQP4-IgG positivity can access premium treatment pathways, while seronegative or unresolved cases often remain in lower-value steroid and supportive care tracks. The diagnostic burden is also heavier in cases that overlap with MOGAD, systemic autoimmune disease, or other inflammatory myelopathies, since treatment decisions depend on excluding close mimics with enough confidence. Until either TM-specific trials succeed or biomarker-defined indications widen further, the transverse myelitis market will continue to under-convert disease burden into treatment revenue.

Other drivers and restraints analyzed in the detailed report include:

- GFAP and NfL Workflow Commercialization Converts Inflammation Events into Structured Diagnostic Activity

- Tele-Neuroimmunology and Home-Infusion Access Shift Site of Care

- High Biologic, PLEX, and Rehabilitation Costs Constrain Market Penetration

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Diagnosis accounted for 56.31% of transverse myelitis market share in 2025, which reflects how every suspected case moves through imaging, CSF analysis, and laboratory testing before treatment direction becomes clear. MRI remains the core tool because spinal cord lesion length, distribution, and contrast behavior help separate short-segment inflammatory events from longitudinally extensive disease that is more suggestive of NMOSD or MOGAD. CSF workups also remain central because pleocytosis, oligoclonal bands, IgG index, and infection exclusion still shape the clinical picture and the differential diagnosis. Within diagnostics, the fastest operational change has come from higher use of AQP4-IgG and MOG-IgG cell-based assays, which move care away from a syndromic label and toward a more actionable disease framework. The transverse myelitis industry therefore remains volume-led on the diagnostic side because each new or relapsing patient generates repeat testing demand across different stages of care.

Treatment type remains smaller, but it is projected to grow at 7.38% CAGR from 2026 to 2031 as the highest-value layer of the transverse myelitis market gains more structure around relapse prevention. Acute care still centers on intravenous steroids first and plasma exchange or IVIG when escalation is needed, especially in severe or poorly responsive myelitis. Maintenance treatment is where revenue intensity rises because rituximab, azathioprine, and newer NMOSD biologics expand use when antibody-confirmed patients need ongoing relapse control. Rehabilitation and symptom management also belong inside the treatment segment because persistent gait, bladder, pain, spasticity, and sexual dysfunction needs keep spending active beyond the acute inflammatory event. This mix keeps the transverse myelitis market balanced between high-volume diagnosis and high-value therapy, with the latter expected to grow faster as classification improves.

Geography Analysis

North America held 39.24% share of the transverse myelitis market size in 2025, and the region remains the leading revenue contributor because specialist neuroimmunology care, advanced MRI access, and broad antibody testing infrastructure are already well established. The United States anchors this position through dense tertiary neurology networks and earlier adoption of structured NMOSD treatment algorithms that influence seropositive transverse myelitis management. Acute care is also easier to coordinate in the region because MRI, CSF studies, infusion support, and plasma exchange are more likely to sit within the same hospital ecosystem. Provider-level examples such as CHLA show how the transverse myelitis market in North America is supported by integrated programs that connect infusion services, plasmapheresis, rehabilitation, virtual care, and transition planning. These factors keep North America ahead on both diagnosis intensity and high-value maintenance therapy adoption.

Europe is the second-largest regional cluster in the transverse myelitis market, although reimbursement and treatment access still vary by country. Germany and the United Kingdom remain important reference points because real-world evidence from 19 German centers showed rituximab at the center of practice, while newer approved biologics were steadily increasing their share of treatment episodes. France, Italy, and Spain add volume through academic neurology networks and access to EMA-recognized neuroimmunology therapies reflected in regional guidance. Eastern and Southern Europe still show diagnostic undercount, and the Bulgarian NMOSD consensus highlights the need for stronger epidemiologic visibility rather than suggesting low true disease burden.

Asia-Pacific is the fastest-growing region in the transverse myelitis market, with a projected CAGR of 7.83% from 2026 to 2031. Japan stands out because the female-to-male ratio in AQP4-IgG seropositive NMOSD can reach 10 to 1, which points to a strong pool of patients relevant to NMOSD-associated transverse myelitis care. Chugai's position around satralizumab also reinforces Japan's commercial role in this treatment space through local development and brand presence. China and India are expanding diagnostic capacity through hospital modernization, but India still faces practical challenges in MOG-IgG testing accuracy and interpretation, especially when fixed assays are used without enough phenotype and MRI correlation. The Middle East and Africa remain earlier-stage contributors, while South America is building from academic participation and broader immunotherapy awareness, so growth there is present but still constrained by uneven access to advanced diagnostics, biologics, and rehabilitation.

- Alexion Pharmaceuticals

- Amgen

- B. Braun

- Baxter

- Chugai Pharmaceutical

- CSL Behring

- EUROIMMUN

- Fresenius

- Fujirebio

- GE Healthcare

- Genentech

- Grifols

- LabCorp

- Medtronic

- Quanterix

- Quest Diagnostics

- Roche

- Siemens Healthineers

- Takeda Pharmaceuticals

- Terumo

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Faster MRI, CSF, and Antibody Workups

- 4.2.2 TM-Adjacent Biologic Adoption from NMOSD and MOGAD

- 4.2.3 Expansion of Specialist Neuroimmunology Centers

- 4.2.4 Long-Tail Rehabilitation Demand

- 4.2.5 GFAP and NfL Workflow Commercialization

- 4.2.6 Tele-Neuroimmunology and Home-Infusion Access

- 4.3 Market Restraints

- 4.3.1 No TM-Specific Approved Therapies

- 4.3.2 High Biologic, PLEX, and Rehab Costs

- 4.3.3 PLEX Capacity Bottlenecks

- 4.3.4 Diagnostic Gray Zones Across TM, NMOSD, MOGAD, and GFAP Astrocytopathy

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Buyers

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Type

- 5.1.1 Diagnosis

- 5.1.1.1 MRI

- 5.1.1.2 Lumbar Puncture / CSF Analysis

- 5.1.1.3 Blood Tests and Antibody Testing

- 5.1.2 Treatment Type

- 5.1.2.1 Acute Pharmacotherapy

- 5.1.2.2 Acute Rescue Procedures

- 5.1.2.3 Maintenance and Relapse-Prevention Therapies

- 5.1.2.4 Rehabilitation Therapies

- 5.1.2.5 Symptom Management

- 5.1.1 Diagnosis

- 5.2 By Etiology

- 5.2.1 Idiopathic Transverse Myelitis

- 5.2.2 Post-infectious Transverse Myelitis

- 5.2.3 Autoimmune Disease-associated Transverse Myelitis

- 5.2.4 Demyelinating Disease-associated Transverse Myelitis

- 5.2.5 Paraneoplastic Transverse Myelitis

- 5.3 By End User

- 5.3.1 Hospitals

- 5.3.2 Specialty Neurology and Neuroimmunology Clinics

- 5.3.3 Rehabilitation Centers

- 5.3.4 Home Care Settings

- 5.3.5 Diagnostic Centers

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 Australia

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.3.1 Alexion Pharmaceuticals

- 6.3.2 Amgen

- 6.3.3 B. Braun

- 6.3.4 Baxter

- 6.3.5 Chugai Pharmaceutical

- 6.3.6 CSL Behring

- 6.3.7 EUROIMMUN

- 6.3.8 Fresenius Kabi

- 6.3.9 Fujirebio

- 6.3.10 GE HealthCare

- 6.3.11 Genentech

- 6.3.12 Grifols

- 6.3.13 Labcorp

- 6.3.14 Medtronic

- 6.3.15 Quanterix

- 6.3.16 Quest Diagnostics

- 6.3.17 F. Hoffmann-La Roche AG

- 6.3.18 Siemens Healthineers

- 6.3.19 Takeda

- 6.3.20 Terumo BCT

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment