|

시장보고서

상품코드

2064401

계란 포장 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Egg Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

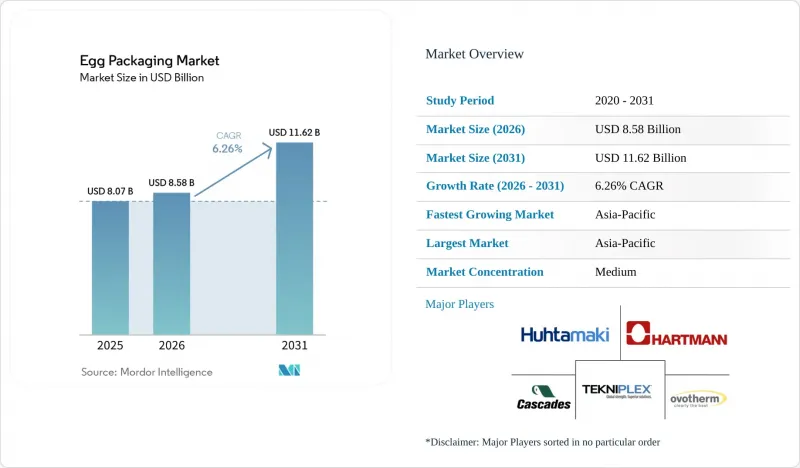

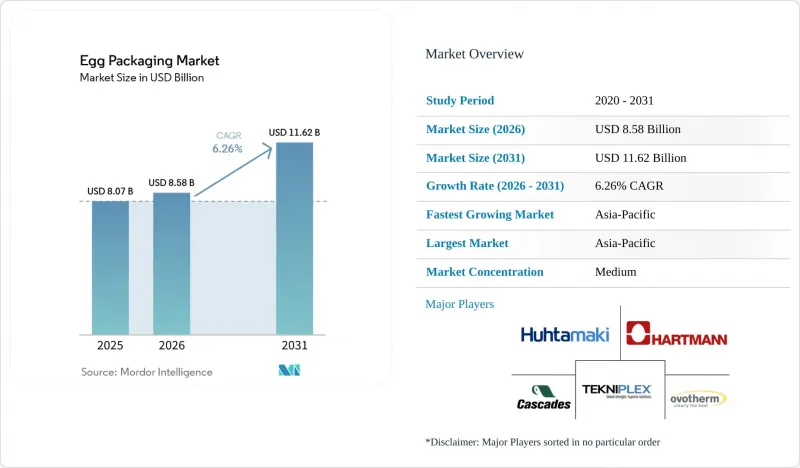

Mordor Intelligence에 의하면, 계란 포장 시장 규모는 2025년에 80억 7,000만 달러, 2026년에 85억 8,000만 달러, 2031년까지 116억 2,000만 달러에 이를 것으로 예측되며, 2026년부터 2031년까지 CAGR 6.26%로 성장할 전망입니다.

본 보고서는 제품 유형(상자, 트레이, 컨테이너 등), 소재 유형(플라스틱, 종이, 성형 섬유 등), 유통 채널(슈퍼마켓 및 하이퍼마켓, 편의점, 온라인 소매, 전문점), 지역(북미, 남미, 유럽, 아시아태평양, 중동 및 아프리카)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계 계란 포장 시장 동향과 인사이트

세계 계란 소비량과 가금류 생산량 증가

2023년 전 세계 계란 생산량은 9,100만 톤을 넘어섰으며, 일부 생산 지역에서 가금류 사육 손실이 발생했음에도 불구하고 계란 포장 시장 수요는 견조하게 유지되었습니다. 아시아는 전 세계 계란 생산량의 70% 이상을 차지하며, 중국만 해도 전 세계 생산량의 거의 절반을 차지하고 있어, 아시아는 포장 수요 성장의 중심지로 자리매김하고 있습니다. ‘OECD-FAO 농업 전망 2025-2034’에 따르면, 중저소득국에서 육류, 유제품, 계란을 통한 단백질 소비는 계속해서 증가할 것으로 예상되며, 소매 시스템이 정비됨에 따라 포장 수요가 더욱 확대될 것으로 보입니다. 인도는 2023년 계란 생산량에서 세계 2위(점유율 8%)를 차지했으며, 개별 판매에서 소매용 포장 판매로의 전환에 따라 생산량 증가만으로는 예상되는 것보다 더 빠른 속도로 포장재 사용량이 증가하고 있습니다. 또한, 2022년부터 2024년까지 발생한 고병원성 조류인플루엔자(HPAI) 유행은 무역 흐름을 변화시켰으며, 국경을 넘는 운송에서 표준화된 보호용 포장의 역할을 강화하는 동시에 계란 포장 시장의 장기적인 수요 동향을 뒷받침했습니다.

성형 섬유 및 재활용 가능한 포장재로의 전환 가속화

소매업체, 규제 당국, 소비자들이 재활용이 가능하고 플라스틱 사용량이 적은 포장을 더욱 중요하게 여기게 됨에 따라, 계란 포장 시장은 성형 섬유 및 종이 기반 형태로 전환되고 있습니다. 유럽연합(EU)에서는 마케팅 및 포장 관련 규제로 인해 기존 플라스틱 포장재에 대한 규정 준수 부담이 지속적으로 증가하고 있으며, 이는 달걀 포장재 분야에서 섬유 기반 대체재로의 광범위한 전환을 촉진하고 있습니다. 독일에서는 2024년에 계란 생산량이 4.2% 증가했으며, 방목 및 유기농 계란의 생산량도 늘었습니다. 이로 인해, 프리미엄성과 지속가능성을 중시하는 진열 방식에 적합한 패키지 형태가 더욱 확산되었습니다. 일본에서도 정책 주도의 포장 전환이 진행되고 있으며, 플라스틱 자원 순환 대책과 소매업체의 탈탄소화 프로그램에 힘입어 성형 펄프 포장재에 대한 관심이 높아지고 있습니다. 카스케이드사는 2024년 6월, 성형 펄프로 만든 베이스와 재생 보드로 만든 슬리브를 결합한 하이브리드 설계의 ‘Fresh GUARD EnVision’을 출시하며, 이러한 방향성을 한층 더 강화했습니다. 이는 계란 포장 시장이 단순히 원자재를 1대 1로 교체하는 것이 아니라, 통합된 지속 가능한 형태로 전환되고 있음을 보여줍니다.

펄프, 재생지, 수지의 가격 변동

원자재 비용의 변동은 계란 포장 시장에서 여전히 가장 뚜렷한 사업적 제약 요인 중 하나입니다. 왜냐하면 섬유, 종이, 수지의 가격 변동은 고객과의 계약 조건이 조정되기보다 더 빨리 가공업체의 이익률에 영향을 미칠 가능성이 있기 때문입니다. Fastmarkets의 보고서에 따르면, 2025년에 이르기까지 유럽의 종이 포장 비용 지수가 급등했습니다. 이는 에너지 및 섬유 원료 가격이 포장 제조업체에 얼마나 급격하게 불리한 방향으로 변동하고 있는지를 반영하고 있습니다. 북미에서는 Packaging Dive가 2025년에 들어서 컨테이너보드 가격이 톤당 최대 70달러 상승했다고 보도했으며, 이로 인해 골판지 및 종이 포장재의 수익성에 지속적인 압박이 가해지고 있습니다. PaperIndex는 또한 펄프가 크라프트지 생산 비용의 40-60%를 차지하는 것이 일반적이라고 지적하고 있습니다. 이것이 바로 섬유 가격이 단기간에 급등하는 것만으로도 제지 공장의 출하 가격이나 컨버터의 이익률에 즉각적인 영향을 미치는 이유를 설명해 줍니다. 이러한 사이클이 장기화되면 소규모 지역 변환기는 더 큰 영향을 받기 쉬워집니다. 왜냐하면 그들은 대개 구매력이나 헤지 능력이 낮고, 계란 포장 시장 내에서 원자재의 균형을 조정할 수 있는 선택지도 적기 때문입니다.

부문별 분석

2025년 기준으로 달걀 포장 시장 점유율의 59.16%를 카톤이 차지했으나, 트레이는 2026년부터 2031년까지 7.63%라는 가장 높은 연평균 성장률(CAGR)을 나타낼 전망입니다. 카톤은 강력한 브랜드 인지도, 소비자에게 친숙하고 다루기 쉬운 점, 그리고 슈퍼마켓, 대형마트, 전문점 등 진열 형태에 관계없이 폭넓은 호환성을 제공하기 때문에 소매 중심공급망에서 여전히 핵심적인 역할을 수행하고 있습니다. 트레이의 인기가 급속히 높아지고 있는 배경에는 케이지 프리 및 방목 사육 시스템에서 농장에서 선별장으로의 이동, 외식 산업으로공급, 그리고 대량 처리 과정에서 30개입 운송 포맷에 대한 의존도가 높다는 점이 꼽힙니다. 또한, 고속 선별 장치도 제품 설계에 영향을 미치고 있습니다. 예를 들어, SANOVO사의 OptiGrader 600은 시간당 최대 21만 6,000개의 계란을 처리할 수 있으므로, 치수가 안정적이고 확실한 탈상 성능을 갖춘 포장이 요구되고 있습니다. 컨테이너 및 기타 형태는 프리미엄 및 스페셜티 제품 프로그램에서 여전히 존재하지만, 예측 기간 동안 계란 포장 시장의 전반적인 구조를 바꾸지는 않을 것입니다.

운영 측면에서 중요한 점은 케이지 프리 방식에서는 기존의 케이지 사육에 비해 달걀 크기의 편차가 커지는 경향이 있으므로, 초기 취급 단계에서 충격 흡수성이 뛰어난 트레이 형태가 더욱 유용하다는 점입니다. 이러한 추세는 계란이 브랜드 소매용 팩에 담기기 전 단계에서도 트레이 수요를 뒷받침하고 있으며, 성장의 원동력은 판촉상의 선호도가 아니라 생산 관행에 내재되어 있다고 할 수 있습니다. 계란 포장 시장에서는 제품 개발 역시 운송 시의 보호 기능과 브랜드 상품의 진열 효과를 하나의 포장으로 모두 충족시키는 하이브리드 구조로 전환되고 있습니다. 캐스케이드사는 ‘Fresh GUARD EnVision’을 통해 그 방향성을 제시했습니다. 이 제품은 성형 펄프로 만든 베이스와 코팅 처리된 재생 보드로 만든 슬리브를 결합한 것으로, 고부가가치 포맷에서 트레이와 카톤의 기능이 어떻게 서로 중첩되기 시작하고 있는지를 보여줍니다. 따라서 계란 포장 업계에서는 전환 작업을 줄이고, 자동화를 지원하며, 별도의 포장 시스템을 강요하지 않으면서도 소매 진열과 유통 시 보호라는 두 가지 요건을 모두 충족할 수 있는 디자인이 더욱 중요시되고 있습니다.

지역별 분석

아시아태평양은 2025년에 계란 포장 시장 점유율의 42.64%를 차지해, 2031년까지 연평균 성장률(CAGR) 7.38%로 성장할 것으로 전망됩니다. FAO의 자료에 따르면, 중국은 전 세계 계란 생산량의 약 49%를 차지하고 있으며, 해당 지역에 트레이와 카톤에 대한 매우 큰 국내 수요 기반을 제공하고 있어 여전히 핵심적인 위치를 차지하고 있습니다. 인도는 생산량의 8%를 차지하며 세계 2위를 기록하고 있으며, 개별 판매에서 체계적인 소매 패키지 판매로의 전환이 진행됨에 따라 도시 및 도시 주변 지역의 유통 채널에서 구조적인 포장 수요가 발생하고 있습니다. 한편, 일본은 다른 수요 양상을 보이고 있으며, 플라스틱 사용에 대한 정책적 압력과 소매업체의 탈탄소화 프로그램으로 인해 성형 포장재와 종이 포장재의 사용이 확대되고 있습니다. 아시아태평양의 전체 계란 포장 시장에서는 소매업의 체계화와 식품 안전에 대한 인식 제고로 인해, 오픈 트레이 판매가 점차 라벨이 부착된 소비자용 포장 방식으로 전환되고 있습니다.

북미와 유럽은 수량 면에서는 아시아태평양에 미치지 못했지만, 추적성, 케이지 프리 전환, 그리고 프리미엄 판매 기준이 이미 확립되어 있었기 때문에 계란 포장 시장에서 여전히 가장 높은 가치를 지닌 지역 중 하나로 남아 있었습니다. 독일의 계란 생산량은 2024년에 4.2% 증가해 137억 개를 기록했으며, 방목 및 유기농 계란 생산이 더욱 강력한 성장세를 보이며 프리미엄 성형 섬유 포장재에 대한 수요를 뒷받침했습니다. 유럽에서는 규제 동향이 생산 및 표시 기준의 강화에 계속해서 기여했습니다. 한편, 미국에서는 FDA의 추적성 체계에 따라 포장 공급업체에 로트 코드 및 추적 기능을 지원하도록 하는 압박이 지속되었습니다. 2025년에 시행된 미국 일부 주의 케이지 프리 법도 동물 복지 주장 및 차별화된 소매 포지셔닝과 연계되어, 고부가가치 포장 용기에 대한 수요 증가를 촉진했습니다.

남미, 중동 및 아프리카는 포장 보급률이 성숙 시장에 비해 여전히 낮고 지역 간 격차도 크지만, 계란 포장 시장에서 다음 단계의 구조적 성장을 이끌 새로운 성장 동력으로 떠오르고 있습니다. 브라질과 아르헨티나에서는 슈퍼마켓의 확대, 콜드체인의 개선, 도시 지역의 소비 확대라는 혜택을 누리고 있으며, 이러한 요인들이 맞물려 개별 판매에서 소분 포장으로의 전환을 촉진하고 있습니다. 중동에서는 국내 가금류 자급자족 프로그램과 수출 주도형 무역 흐름에 따라 표준화된 보호 포장의 필요성이 높아지고 있습니다. 또한, 2025년 긴급 계란 수출에서 튀르키예가 수행한 역할은 무역 혼란이 운송 대응형 포장에 대한 수요를 얼마나 신속하게 확대시킬 수 있는지를 보여주었습니다. 아프리카에서는 상업적 양계 사업이 확대되고 있지만, 인프라 격차와 재생 섬유 생산 능력의 한계로 인해 당분간은 저비용 플라스틱 포장재가 주류를 이루는 한편, 예측 기간 후반에는 성형 섬유 제품의 성장 여지가 남아 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.23According to Mordor Intelligence, the egg packaging market size is projected to be USD 8.07 billion in 2025, USD 8.58 billion in 2026, and reach USD 11.62 billion by 2031, growing at a CAGR of 6.26% from 2026 to 2031.

This report is Segmented by Product Type (Cartons, Trays, Containers, and More), Material Type (Plastic, Paper, Molded Fiber, and More), Distribution Channel (Supermarkets and Hypermarkets, Convenience Stores, Online Retail, and Specialty Stores), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Egg Packaging Market Trends and Insights

Rising Global Egg Consumption and Poultry Output

Global hen egg production exceeded 91 million MT in 2023, which kept the base demand floor for the egg packaging market broad, even when flock losses affected some producing regions. Asia accounted for more than 70% of global egg output, and China alone accounted for nearly half of global production, keeping Asia at the center of packaging demand growth. The OECD-FAO Agricultural Outlook 2025-2034 stated that protein consumption from meat, dairy, and eggs will continue rising in lower-middle-income countries, which supports additional packaging demand as retail systems formalize. India ranked second globally in egg production in 2023, with an 8% share, and its shift from loose egg sales to packaged retail formats is increasing packaging intensity faster than production alone would suggest. HPAI also changed trade flows between 2022 and 2024, increasing the role of standardized protective packs in cross-border shipments and strengthening the long-term demand profile of the egg packaging market.

Accelerating Shift Toward Molded Fiber and Recyclable Packs

The egg packaging market is moving toward molded fiber and paper-based formats as retailers, regulators, and consumers place greater emphasis on recyclable, lower-plastic packaging. In the European Union, marketing and packaging rules have continued to increase the compliance burden on conventional plastic formats, supporting a broader migration toward fiber-based alternatives in egg packs. Germany reported a 4.2% increase in egg production in 2024, while free-range and organic output also grew, which supported formats that better match premium and sustainability-led shelf positioning. Japan has also been moving through a policy-led packaging transition, with plastic resource circulation measures and retailer decarbonization programs drawing more attention to molded pack formats. Cascades reinforced this direction in June 2024 when it launched Fresh GUARD EnVision, a hybrid design that combines a molded pulp base with a recycled-board sleeve, showing that the egg packaging market is moving toward integrated sustainable formats rather than a simple one-for-one material switch.

Pulp, Recycled Paper, and Resin Price Volatility

Input cost volatility remains one of the clearest operating restraints in the egg packaging market because fiber, paper, and resin swings can pass through converter margins faster than customer contracts adjust. Fastmarkets reported a sharp rise in European paper packaging cost indices during 2025, which reflected how quickly energy and fiber inputs can move against pack producers. In North America, Packaging Dive reported containerboard price increases of up to USD 70 per ton entering 2025, which continued to put pressure on corrugated and paper-based packaging economics. PaperIndex also noted that pulp commonly accounts for 40-60% of kraft paper production costs, which explains why even short spikes in fiber pricing quickly affect mill-gate economics and converter margins. Smaller regional converters are more exposed when these cycles persist, because they usually have less buying leverage, less hedging capacity, and fewer options to rebalance between materials within the egg packaging market.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Modern Grocery Retail and Online Grocery Fulfillment

- Tightening Food Safety, Labeling, and Traceability Requirements

- Rising Compliance Costs for Food-Contact and Packaging-Waste Rules

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cartons held 59.16% of the egg packaging market share in 2025, while trays are projected to record the fastest CAGR at 7.63% from 2026 to 2031. Cartons remain central to retail-led supply chains because they offer strong brand visibility, familiar consumer handling, and broad compatibility across supermarket, hypermarket, and specialty shelf formats. Trays are gaining popularity faster because cage-free and free-range systems rely heavily on 30-egg transport formats for farm-to-grader movement, food-service supply, and higher-volume handling. High-speed grading equipment is also shaping product design, as SANOVO's OptiGrader 600 can process up to 216,000 eggs per hour and therefore requires packs with stable dimensions and reliable denesting performance. Containers and other formats remain present in premium and specialty programs, but they do not alter the broad structure of the egg packaging market during the forecast period.

What matters operationally is that cage-free systems often produce wider egg-size variation than conventional cage operations, which makes shock-absorbing tray geometry more useful in earlier handling stages. That pattern supports tray demand even before eggs reach branded retail packs, so the growth driver is embedded in production practices rather than in merchandising preferences. Within the egg packaging market, product development is also moving toward hybrid structures that combine transport protection with branded shelf appeal in a single pack. Cascades illustrated that direction with Fresh GUARD EnVision, which paired a molded pulp base with a coated recycled-board sleeve and showed how tray and carton functions are starting to overlap in higher-value formats. The egg packaging industry is therefore placing more value on designs that can reduce changeovers, support automation, and serve both retail presentation and distribution protection without forcing separate packaging systems.

Geography Analysis

Asia-Pacific held 42.64% of the egg packaging market share in 2025 and is projected to expand at a 7.38% CAGR through 2031. China remained the core anchor because FAO data showed it accounted for nearly 49% of global egg production, providing the region with a very large domestic demand base for trays and cartons. India ranked second globally with an 8% share of output, and its ongoing move from loose egg sales toward organized packaged retail is adding structural packaging demand in urban and peri-urban channels. Japan has a different demand profile, as policy pressure on plastic use and retailer decarbonization programs are driving greater adoption of molded packs and paper-based formats. Across the wider Asia-Pacific egg packaging market, retail formalization and food-safety awareness are gradually converting open-tray sales into labeled consumer packs.

North America and Europe did not match Asia-Pacific in volume, but they remained among the highest-value parts of the egg packaging market because traceability, cage-free conversion, and premium merchandising standards were already well established. Germany's egg production rose 4.2% in 2024 to 13.7 billion eggs, with stronger growth in free-range and organic output, which supported demand for premium molded-fiber formats. In Europe, the regulatory path continued to support tighter production and labeling standards, while in the United States the FDA traceability framework kept pressure on packaging suppliers to support lot coding and tracking capability. Several U.S. state cage-free laws that took effect in 2025 also supported stronger demand for higher-value cartons tied to animal welfare claims and differentiated retail positioning.

South America, the Middle East, and Africa represent the next structural growth frontier for the egg packaging market, even though packaging penetration remains lower and more uneven than in mature markets. Brazil and Argentina are benefiting from supermarket expansion, cold-chain improvement, and urban consumption growth, which together support movement from bulk presentation toward pre-packed formats. In the Middle East, domestic poultry self-sufficiency programs and export-led trade flows are strengthening the need for standardized protective packaging, and Turkey's role in emergency egg exports during 2025 showed how trade disruptions can quickly expand demand for transport-ready pack formats. In Africa, commercial poultry operations are expanding, but infrastructure gaps and limited recycled fiber capacity still favor lower-cost plastic formats in the near term while leaving room for molded-fiber growth later in the forecast period.

- Hartmann Packaging A/S

- Huhtamaki Oyj

- Tekni-Plex, Inc.

- Cascades Inc.

- Ovotherm International Handels GmbH

- CKF Inc.

- Primapack

- EUROPACK, a.s.

- Dispak Ltd.

- Omni-Pac Group

- Nippon Molding Co., Ltd.

- GREENLINK GROUP CORP.

- Keyes Packaging Group

- Eipack Barneveld B.V.

- Eggbox GmbH

- EnviroPAK Corporation

- Henry Molded Products, Inc.

- Carton Packaging Pty Ltd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Global Egg Consumption and Poultry Output

- 4.2.2 Accelerating Shift Toward Molded Fiber and Recyclable Packs

- 4.2.3 Expansion of Modern Grocery Retail and Online Grocery Fulfillment

- 4.2.4 Tightening Food Safety, Labeling, and Traceability Requirements

- 4.2.5 Premium Packaging Demand for Cage-Free, Organic, and Functional Eggs

- 4.2.6 Automation-Ready Pack Designs for High-Speed Grading and Fulfillment

- 4.3 Market Restraints

- 4.3.1 Pulp, Recycled Paper, and Resin Price Volatility

- 4.3.2 Rising Compliance Costs for Food-Contact and Packaging-Waste Rules

- 4.3.3 Avian Influenza-Driven Egg Supply Swings and Carton Demand Volatility

- 4.3.4 Food-Contact PCR Scarcity and Approval Bottlenecks

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Cartons

- 5.1.2 Trays

- 5.1.3 Containers

- 5.1.4 Other Product Types

- 5.2 By Material Type

- 5.2.1 Plastic

- 5.2.2 Paper

- 5.2.3 Molded Fiber

- 5.2.4 Other Material Types

- 5.3 By Distribution Channel

- 5.3.1 Supermarkets and Hypermarkets

- 5.3.2 Convenience Stores

- 5.3.3 Online Retail

- 5.3.4 Specialty Stores

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Argentina

- 5.4.2.3 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 Rest of Europe

- 5.4.4 Asia-Pacific

- 5.4.4.1 China

- 5.4.4.2 Japan

- 5.4.4.3 South Korea

- 5.4.4.4 India

- 5.4.4.5 Australia and New Zealand

- 5.4.4.6 Rest of Asia-Pacific

- 5.4.5 Middle East and Africa

- 5.4.5.1 Middle East

- 5.4.5.1.1 Saudi Arabia

- 5.4.5.1.2 United Arab Emirates

- 5.4.5.1.3 Turkey

- 5.4.5.1.4 Rest of Middle East

- 5.4.5.2 Africa

- 5.4.5.2.1 South Africa

- 5.4.5.2.2 Nigeria

- 5.4.5.2.3 Rest of Africa

- 5.4.5.1 Middle East

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Hartmann Packaging A/S

- 6.4.2 Huhtamaki Oyj

- 6.4.3 Tekni-Plex, Inc.

- 6.4.4 Cascades Inc.

- 6.4.5 Ovotherm International Handels GmbH

- 6.4.6 CKF Inc.

- 6.4.7 Primapack

- 6.4.8 EUROPACK, a.s.

- 6.4.9 Dispak Ltd.

- 6.4.10 Omni-Pac Group

- 6.4.11 Nippon Molding Co., Ltd.

- 6.4.12 GREENLINK GROUP CORP.

- 6.4.13 Keyes Packaging Group

- 6.4.14 Eipack Barneveld B.V.

- 6.4.15 Eggbox GmbH

- 6.4.16 EnviroPAK Corporation

- 6.4.17 Henry Molded Products, Inc.

- 6.4.18 Carton Packaging Pty Ltd

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment