|

시장보고서

상품코드

2064404

아시아태평양의 GPU 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Asia-Pacific GPU - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

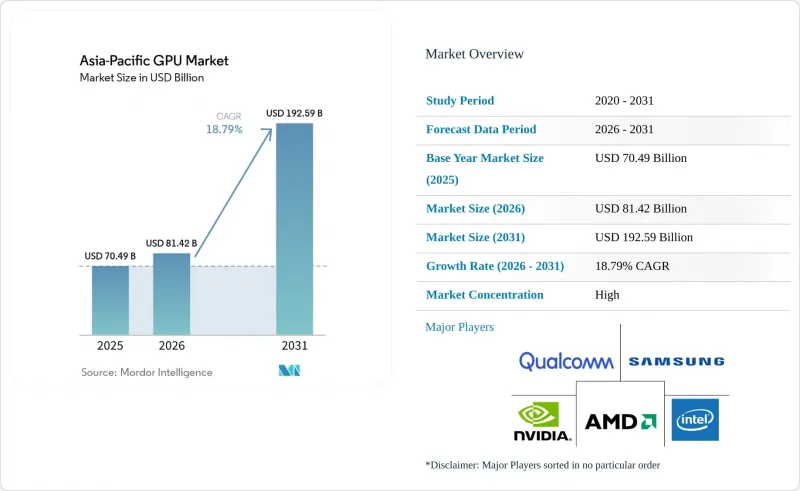

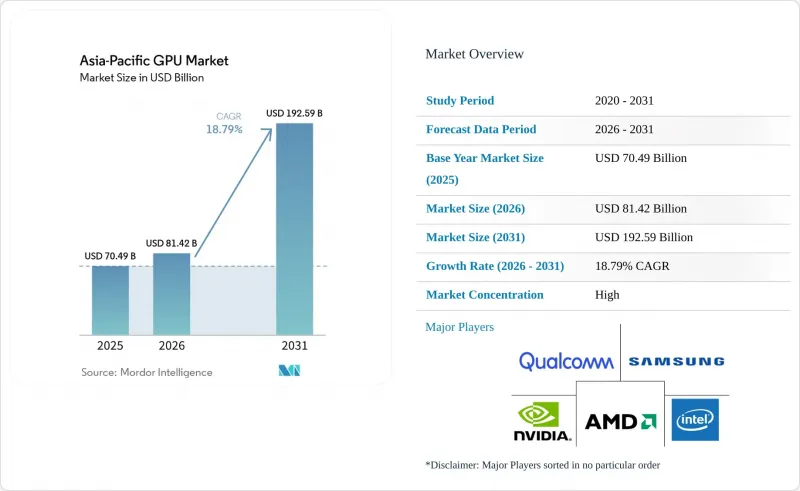

Mordor Intelligence에 의하면, 아시아태평양 GPU 시장 규모는 2025년 704억 9,000만 달러에서 2026년에는 814억 2,000만 달러로 확대되어 2026년부터 2031년까지 CAGR 18.79%로 성장을 지속하여, 2031년까지 1,925억 9,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 통합형(통합형 GPU 및 디스크리트 GPU), 기기 용도(모바일 기기 및 태블릿, PC 및 워크스테이션, 서버 및 데이터센터 가속기, 게임기 및 휴대용 기기, 자동차 및 ADAS, 기타), 그리고 지역(중국, 일본, 한국, 인도, 기타)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제공됩니다.

아시아태평양 GPU 시장 동향 및 인사이트

데이터센터에서의 AI 가속화 수요 증가

이 지역의 하이퍼스케일 사업자들은 페타플롭급 정밀도로 대규모 언어 모델의 훈련 및 서비스 제공이 가능한 GPU 클러스터를 지속적으로 확장하고 있습니다. 차세대 가속기의 수주량은 캠퍼스당 1만 대를 넘는 것이 일상화되어, 공급업체들은 소비자용 그래픽스 제품보다 데이터센터용 제품을 우선시할 수밖에 없는 상황입니다. 베트남, 태국, 말레이시아에서는 클라우드 서비스 제공업체의 실질적인 설비 투자 비용을 절감해 주는 다년간의 세제 혜택 조치가 도입되어, 수냉식 GPU 포드를 핵심으로 하는 300메가와트 규모의 캠퍼스 건설이 잇따르고 있습니다. 중국에서는 반도체 수입에 대한 정책적 제한으로 인해 화웨이 어센드 기기의 도입이 가속화되고 있으며, 2026년 생산 목표인 60만 대는 2025년 생산량의 거의 2배에 달할 것으로 전망됩니다. 인도에서도 수요가 확대되고 있으며, 100억 달러 규모의 반도체 우대 조치 중 데이터센터용 가속기에 막대한 예산이 배정되어 있습니다. 전반적으로 볼 때, 그 규모와 현지화 노력, 그리고 워크로드의 다양화 덕분에 AI 서버는 아시아태평양의 GPU 시장에서 여전히 가장 빠르게 성장하고 있는 최종 용도로 자리 잡고 있습니다.

클라우드 게임 플랫폼의 보급

5G 독립형 네트워크와 도시 지역 엣지 노드의 구축을 통해 주요 도시의 평균 지연 시간이 20밀리초 미만으로 줄어들었으며, 최소한의 압축만으로 1080p 고화질 게임 스트리밍이 가능해졌습니다. 중국의 퍼블리셔들은 콘솔에 거부감을 느끼는 사용자층을 공략하기 위해 출시일과 동시에 클라우드 버전을 제공하고 있는 반면, 일본의 기존 기업들은 피크 시간대의 사용자 경험을 유지하기 위해 지역별 엣지 캐시를 도입하고 있습니다. 무제한 5G 통신과 구독형 액세스를 결합한 통신사의 번들 요금제는 콘솔을 처음 구매하는 고객의 전환율을 높여 통신사의 사용자당 평균 수익(ARPU)과 플랫폼 보급률을 향상시키고 있습니다. GPU에 대한 수요는 두 가지 측면에서 발생하고 있습니다. 렌더링 클러스터용 추가 데이터센터용 카드와, 스로틀링 없이 레이 트레이싱 처리된 스트림을 디코딩할 수 있는 스마트폰 내장 GPU입니다. 따라서 클라우드 게임은 계속해서 해당 지역의 GPU 출하량에 의미 있는 긍정적 견인력을 발휘하고 있습니다.

중국으로의 고성능 GPU 수출 규제 강화

미국은 2023년 말, 더욱 엄격한 라이선스 기준을 도입하여 최상위급 가속기의 출하를 제한했습니다. 2026년 1월 부분적인 규제 완화로 인해 특정 모델에 대해서는 사례별로 수출이 허용되었으나, ‘AI 오버워치 법’ 등의 입법안으로 인해 전면적인 금지 조치가 재도입될 가능성이 있습니다. 지역 유통업체들은 규정 준수 비용 증가에 직면해 있는 반면, 중국의 하이퍼스케일러 기업들은 성능 면에서 뒤처져 있음에도 불구하고 국내산 반도체에 대한 이중 조달을 점점 더 확대되고 있습니다. 그 결과 발생하는 시장 분할은 미국 공급업체의 단기 수익 실현을 지연시키고, 자본을 현지 대체품으로 돌리게 함으로써 해당 지역의 연평균 성장률(CAGR) 전망치를 몇 포인트 낮추는 요인이 되고 있습니다.

부문별 분석

2025년, AI 훈련의 도입 확대에 힘입어 디스크리트 가속기는 아시아태평양 GPU 시장 점유율의 64.81%를 차지했습니다. 하이퍼스케일러들이 700와트의 열설계 전력(TDP)과 수 테라바이트급 HBM 용량을 갖춘 독립형 카드를 지정함에 따라, 아시아태평양의 디스크리트 GPU 시장 규모는 2031년까지 연평균 성장률(CAGR) 19.26%를 기록하며 통합형 GPU를 능가하는 성장을 보일 것으로 전망됩니다. 상호 연결 대역폭과 메모리 중심 아키텍처의 지속적인 강화 덕분에, 디스크리트 GPU는 엔터프라이즈 워크로드 통합에 있어 여전히 가장 선호되는 선택지로 자리 잡고 있습니다.

열 설계 및 비용 제약이 주된 요인으로 작용하는 모바일 기기, 초슬림 노트북, 보급형 데스크톱의 경우, 통합형 솔루션은 여전히 필수적입니다. 애플의 커스텀 실리콘이나 퀄컴 스냅드래곤 X 시리즈는 많은 소비자용 작업에서 동등한 성능을 발휘하고 있지만, 레이 트레이싱을 많이 사용하는 게임이나 기반 모델의 추론을 장시간 수행하는 경우에는 여전히 별도의 그래픽 카드에 대한 수요가 발생하고 있습니다. 예측 기간 동안 GPU 치플릿을 CPU 타일과 함께 통합하는 하이브리드 시스템 온 패키지(SoP) 접근 방식에 따라 그 경계가 모호해질 가능성은 있지만, 아시아태평양 GPU 시장의 총 매출 집중도는 계속해서 디스크리트 설계에 치우칠 것으로 보입니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.23According to Mordor Intelligence, the asia-Pacific gPU market size is expected to grow from USD 70.49 billion in 2025 to USD 81.42 billion in 2026 and is forecast to reach USD 192.59 billion by 2031 at 18.79% CAGR over 2026-2031.

This report is Segmented by Integration Type (Integrated GPUs and Discrete GPUs), Device Application (Mobile Devices and Tablets, Pcs and Workstations, Servers and Datacenter Accelerators, Gaming Consoles and Handhelds, Automotive and ADAS, and More), and Geography (China, Japan, South Korea, India, and More). The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific GPU Market Trends and Insights

Rising Demand for AI Acceleration in Data Centers

Hyperscale operators across the region continue to scale GPU clusters capable of training and serving large language models at petaflop precision. Orders for next-generation accelerators routinely exceed 10,000 units per campus, forcing suppliers to prioritize data-center products over consumer graphics. Vietnam, Thailand, and Malaysia have issued multi-year tax holidays that lower effective capital outlay for cloud-service providers, prompting new builds of 300-megawatt campuses designed around liquid-cooled GPU pods. In China, policy limits on imported silicon are accelerating the adoption of Huawei Ascend devices, whose 2026 production target of 600,000 units is almost double 2025 output. Demand is also expanding in India, where semiconductor incentives worth USD 10 billion earmark a significant tranche for data-center accelerators. Altogether, the scale, localization push, and diversified workloads keep AI servers as the fastest-growing end use for the Asia-Pacific GPU market.

Proliferation of Cloud Gaming Platforms

The rollout of 5G standalone networks and metropolitan edge nodes has driven average latency below 20 milliseconds in major cities, enabling premium game streaming at 1080p with minimal compression. Chinese publishers now launch day-and-date cloud versions to reach console-averse segments, while Japanese incumbents deploy regional edge caches to preserve user experience during peak hours. Telecom bundles that pair unlimited 5G with subscription access have increased conversion rates for first-time console customers, aligning operator average revenue per user and platform attach metrics. GPU demand arises on two fronts: additional datacenter cards for rendering clusters and integrated smartphone GPUs that can decode ray-traced streams without throttling. Accordingly, cloud gaming continues to exert a meaningful positive pull on regional GPU shipments.

Stricter Export Controls on High-Performance GPUs to China

The United States implemented more rigorous license thresholds in late 2023, constraining shipments of top-bin accelerators. A partial relaxation in January 2026 allowed case-by-case export of certain models, yet legislative proposals such as the AI OVERWATCH Act could reinstate blanket prohibitions. Regional distributors face elevated compliance costs, and Chinese hyperscalers increasingly dual-source with domestic silicon despite lagging performance. The resulting fragmentation slows near-term revenue recognition for United States suppliers and redirects capital toward local alternatives, shaving several points off the regional CAGR forecast.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Mobile Gaming Ecosystem in Asia-Pacific

- Emergence of Chiplet-Based GPU Architectures

- Supply-Chain Volatility for Advanced Packaging Materials

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Discrete accelerators captured 64.81% of the Asia-Pacific GPU market share in 2025 on the back of escalating AI training deployments. The Asia-Pacific GPU market size for discrete devices is expected to outpace integrated alternatives at a 19.26% CAGR to 2031 as hyperscalers specify stand-alone cards with 700-watt thermal envelopes and multi-terabyte HBM capacity. Continuous enhancements in interconnect bandwidth and memory-centric architectures keep discrete GPUs as the default choice for enterprise workload consolidation.

Integrated solutions remain indispensable in mobile devices, ultrathin laptops, and entry-level desktops where thermal and cost constraints prevail. Apple's custom silicon and Qualcomm Snapdragon X series illustrate performance parity for many consumer tasks, yet sustained ray-traced gaming or foundation-model inference still triggers demand for discrete add-in boards. Over the forecast period, a hybrid system-on-package approach that embeds GPU chiplets alongside CPU tiles may blur definitions, but overall revenue concentration will continue to skew toward discrete designs in the Asia-Pacific GPU market.

List of Companies Covered in this Report:

- NVIDIA Corporation

- Advanced Micro Devices Inc.

- Intel Corporation

- Qualcomm Technologies Inc.

- Samsung Electronics Co. Ltd.

- Apple Inc.

- ARM Ltd.

- Imagination Technologies Ltd.

- MediaTek Inc.

- Huawei Technologies Co. Ltd. (HiSilicon)

- Zhaoxin Semiconductor Corporation Limited

- VeriSilicon Holdings Co. Ltd.

- VIA Technologies Inc.

- Unisoc Technologies Co. Ltd.

- Renesas Electronics Corporation

- Rockchip Electronics Co. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Proliferation of Cloud Gaming Platforms

- 4.2.2 Rising Demand for AI Acceleration in Data Centers

- 4.2.3 Expansion of Mobile Gaming Ecosystem in Asia-Pacific

- 4.2.4 Increasing Graphics Requirements for PC Content Creation

- 4.2.5 Government Incentives for Domestic GPU Design Startups

- 4.2.6 Emergence of Chiplet-Based GPU Architectures

- 4.3 Market Restraints

- 4.3.1 Supply-Chain Volatility for Advanced Packaging Materials

- 4.3.2 Rising Average Selling Prices Limiting Mass-Market Adoption

- 4.3.3 Escalating Data-Center Energy Tariffs in Japan and South Korea

- 4.3.4 Stricter Export Controls on High-Performance GPUs to China

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Integration Type

- 5.1.1 Integrated GPUs (iGPU)

- 5.1.2 Discrete GPUs (dGPU)

- 5.2 By Device Application

- 5.2.1 Mobile Devices and Tablets

- 5.2.2 PCs and Workstations

- 5.2.3 Servers and Datacenter Accelerators

- 5.2.4 Gaming Consoles and Handhelds

- 5.2.5 Automotive / ADAS

- 5.2.6 Other Embedded and Edge Devices

- 5.3 By Geography

- 5.3.1 China

- 5.3.2 Japan

- 5.3.3 South Korea

- 5.3.4 India

- 5.3.5 Southeast Asia

- 5.3.6 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 NVIDIA Corporation

- 6.4.2 Advanced Micro Devices Inc.

- 6.4.3 Intel Corporation

- 6.4.4 Qualcomm Technologies Inc.

- 6.4.5 Samsung Electronics Co. Ltd.

- 6.4.6 Apple Inc.

- 6.4.7 ARM Ltd.

- 6.4.8 Imagination Technologies Ltd.

- 6.4.9 MediaTek Inc.

- 6.4.10 Huawei Technologies Co. Ltd. (HiSilicon)

- 6.4.11 Zhaoxin Semiconductor Corporation Limited

- 6.4.12 VeriSilicon Holdings Co. Ltd.

- 6.4.13 VIA Technologies Inc.

- 6.4.14 Unisoc Technologies Co. Ltd.

- 6.4.15 Renesas Electronics Corporation

- 6.4.16 Rockchip Electronics Co. Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment