|

시장보고서

상품코드

2064516

유럽의 HR 애널리틱스 시장 : 시장 점유율 분석, 산업 동향 및 통계 데이터, 성장 예측(2026-2031년)Europe HR Analytics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

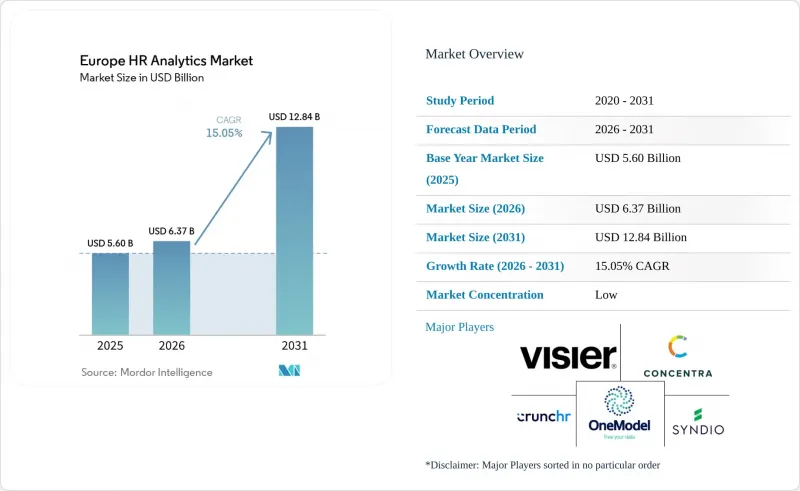

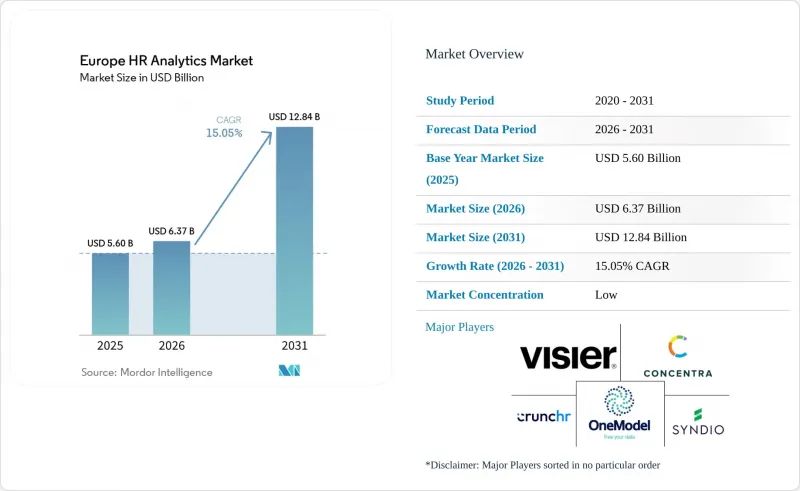

Mordor Intelligence에 의하면, 유럽의 HR 애널리틱스(인적 자본 분석) 시장 규모는 2025년에 56억 달러로 평가되었고, 2026년에 63억 7,000만 달러로 추정되며, 2031년까지 128억 4,000만 달러에 이를 것으로 예측됩니다.

2026-2031년 연평균 성장률(CAGR) 15.05%로 성장할 것으로 전망됩니다.

본 보고서는 구성 요소별(솔루션, 서비스), 도입 형태별(클라우드, 온프레미스, 하이브리드), 기업 규모별(대기업 등), 용도별(인재 채용 및 교육 등), 최종 사용자 산업 분야별(은행, 금융서비스 및 보험(BFSI), 의료 및 생명과학, IT 및 통신 등) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

유럽의 HR 애널리틱스 시장 동향 및 인사이트

클라우드 네이티브 HR 분석 도입이 플랫폼 통합을 가속화

클라우드 전환은 이 지역 전체의 소프트웨어 선정에 가장 큰 영향을 미치는 구조적 요인으로 자리 잡고 있습니다. SaaS를 통한 서비스는 보다 신속한 업데이트, 유지 관리 비용 절감, 그리고 새로운 분석 기능 도입을 위한 보다 간편한 경로를 제공하기 때문에 고용주들은 온프레미스 보고 환경에서 점차 전환하고 있습니다. 이러한 변화는 특히 독일에서 두드러지며, P and I사의 기업 가치는 2025년 3월 55억 유로(62억 2,000만 달러)에 달했으며, 동사의 기업 수익은 3억 유로(3억 3,900만 달러)를 돌파했고, 연간 성장률은 20%를 넘어섰습니다. 또한, 클라우드 전환을 통해 오랫동안 사일로화되어 있던 인사·급여 시스템 속에 숨겨져 있던 데이터 품질 문제도 드러나고 있습니다. 이러한 문제가 표면화되면, 조직은 통합, 거버넌스, 그리고 지속적인 모델 조정을 위한 추가적인 지원이 필요합니다. 유럽의 HR 애널리틱스 시장에서 이러한 추세는 초기 도입 이후 공급업체의 관여를 확대시키고, 서비스의 상업적 중요성을 높이고 있습니다.

데이터 기반의 인재 채용 및 재직률 최적화가 인재 경제의 양상을 바꾸고 있습니다.

유럽 전역에서 노동력 부족이 광범위하고 지속적으로 나타나고 있어, 채용 분석은 핵심 사업 계획에 가까워지고 있습니다. Cedefop의 ‘노동력·기술 부족 지수’는 고숙련, 중숙련, 저숙련 직종 전반에 걸쳐 압박이 발생하고 있음을 보여주고 있으며, 고용주는 더 이상 기본적인 채용 동향 파악에만 의존할 수 없게 되었습니다. 구매자들은 사내 인력 현황과 외부 노동 시장 동향, 그리고 향후 수요 전망을 비교할 수 있는 플랫폼을 더욱 중요하게 여기고 있습니다. 이에 따라 상업적 관심은 단순한 지원자 추적 도구에서 더 광범위한 인재 인텔리전스 시스템으로 옮겨가고 있습니다. 희소 인재의 이직 방지가 어려워짐에 따라, 고용주들은 조기에 경고 신호를 파악할 필요가 있어 이직률 분석도 같은 흐름을 따르고 있습니다. 따라서 유럽의 HR 애널리틱스 시장은 기술 격차, 채용의 질, 사내 이동을 단일 워크플로우로 통합한 보다 종합적인 ‘채용 수익’의 정의로부터 혜택을 보고 있습니다.

GDPR(EU 개인정보보호규정)과 민감한 직원 데이터 거버넌스가 분석의 걸림돌이 되고 있습니다.

데이터 거버넌스는 유럽 전역의 수많은 도입 사례에서 여전히 가장 시급한 운영상의 제약 요인으로 남아 있습니다. 인사 부서는 기술적으로 필요한 데이터를 보유하고 있는 경우가 많지만, 새로운 법적 근거나 보다 강력한 관리 체제가 없다면 급여 계산, 성과 평가, 채용, 퇴직과 관련된 워크플로우 간에 해당 데이터를 재사용할 수 있다고 단정할 수는 없습니다. 고용주가 프로파일링, 특별 범주 데이터 또는 국경을 넘는 데이터 처리에 착수하는 경우, 이러한 이용 사례는 보다 상세한 검토와 더 엄격한 문서화가 필요하기 때문에 문제는 더욱 복잡해집니다. 각국의 규제 역시 중요한 요소가 됩니다. 특히, 고용 분야에서 사생활 보호에 대한 기대가 높고, 내부 협의 요건이 보다 형식적인 시장에서 그러합니다. 따라서 벤더는 프로젝트 초기 단계부터 ‘프라이버시 바이 디자인(Privacy by Design)’ 아키텍처, 데이터 접근 제한, 그리고 보다 세분화된 권한 설정을 요구받게 될 것입니다. 유럽의 HR 애널리틱스 시장에서 이러한 관리 조치는 장기적인 신뢰를 뒷받침하는 한편, 도입 주기를 길게 만들고 단기적인 도입 비용을 상승시키는 요인이 되기도 합니다.

부문별 분석

2025년 기준으로, 솔루션 부문은 유럽 HR 애널리틱스 시장에서 62.37%의 점유율을 차지했으나, 서비스 부문은 2031년까지 연평균 성장률(CAGR) 16.94%로 확대될 것으로 전망됩니다. 이러한 차이는 계약 가치의 기반을 여전히 소프트웨어가 담당하고 있는 한편, 프로젝트의 성공이나 계약 갱신의 질을 결정짓는 요소로서 서비스의 중요성이 커지고 있는 시장 구조를 반영하고 있습니다. 벤더들이 예측 이직 모델, 생성형 AI 어시스턴트, 스킬 그래프 기능을 추가함에 따라 도입 요건은 점점 더 전문화되고 있습니다. 구매자들은 현재 도입을 일회성 설치로 간주하는 경향이 줄어들고, 지속적인 운영 프로그램으로 인식하는 경향이 강해지고 있습니다.

이러한 변화로 인해 전문 서비스 분야가 혜택을 보고 있습니다. 왜냐하면 고용주는 데이터 마이그레이션, 모델 보정, 변경 관리, 거버넌스에 관한 지원이 필요하기 때문입니다. 이는 특히 조직이 광범위한 HCM 보고서를 바탕으로, 기존 인사 정보 시스템(HRIS) 및 급여 계산 시스템과 연동해야 하는 전용 인력 인텔리전스 플랫폼으로 전환할 때 두드러지게 나타납니다. 유럽의 HR 애널리틱스 시장에서는 소프트웨어와 심층적인 자문 기능을 결합할 수 있는 벤더들이 높은 평가를 받고 있습니다. 왜냐하면 가치는 라이선스 이용 권한뿐만 아니라 도입 현황이나 성과 품질에도 크게 좌우되게 되었기 때문입니다. 소프트웨어는 여전히 매출의 대부분을 차지하고 있으며, 특히 대기업 및 공공 부문 고객과의 다년 계약형 SaaS에서 그 경향이 두드러집니다. 동시에, P와 I의 성장 및 평가액 추이가 상징하듯이 독일 클라우드 HR 시장의 성장세는 플랫폼 도입에 따라 서비스의 중요성이 왜 높아지고 있는지를 보여주고 있습니다.

2025년에는 시장의 68.41%를 클라우드 도입이 차지했으며, SaaS가 신규 HR 애널리틱스 도입 결정에 있어 사실상 표준 아키텍처가 되었음이 입증되었습니다. 클라우드 시스템이 매력적인 이유는 공급업체가 제품 업데이트를 더 신속하게 제공할 수 있고, 실시간 데이터 파이프라인을 더 쉽게 지원할 수 있으며, 고객 측에서 대규모 업그레이드 주기를 거치지 않고도 규정 준수 변경 사항에 대응할 수 있기 때문입니다. 하이브리드 차량 도입은 가장 빠르게 성장하고 있는 모델로, 2026-2031년 연평균 성장률(CAGR) 17.86%로 성장을 지속할 전망입니다. 이는 일부 고용주가 스택의 일부를 여전히 더 엄격한 내부 통제 하에 두어야 하기 때문입니다. 이러한 경향은 데이터 저장 장소, 조달 규정 또는 기존 인프라 비용이 여전히 중요하게 여겨지는 은행, 의료, 정부 기관 및 기타 규제 대상 분야에서 가장 두드러집니다.

온프레미스 부문의 상대적 비중은 줄어들고 있지만, 이 분야에서 완전히 사라지는 것은 아닙니다. 특히 독일에서는 유서 깊은 공공기관이나 산업 단체들이 기밀성이 높은 직원 기록이나 오랫동안 운영되어 온 IT 자산에 대해 여전히 내부 호스팅을 유지하고 있습니다. 따라서 하이브리드 환경은 단순한 일시적인 예외가 아니라, 조직이 데이터 아키텍처 전체를 한꺼번에 재구축하지 않고도 분석 기능을 현대화할 수 있게 해주기 때문에 가교 역할을 하고 있습니다. 유럽의 HR 애널리틱스 시장에서는 클라우드로의 전환이 진행되고 있지만, 그 전환 상황은 업종이나 국가에 따라 여전히 차이가 있습니다. 유연한 도입 옵션, 주권적인 호스팅 체계, 그리고 강력한 통합 레이어를 갖춘 공급업체는 규제 대상 직원이나 국경 간 거래를 확보하는 데 유리한 입장에 있습니다.

기타 혜택 :

- Excel 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 분석 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJYAccording to Mordor Intelligence, the europe hR analytics market size is projected to be USD 5.60 billion in 2025, USD 6.37 billion in 2026, and reach USD 12.84 billion by 2031, growing at a CAGR of 15.05% from 2026 to 2031.

This report is Segmented by Component (Solutions, and Services), Deployment Mode (Cloud, On-Premises, and Hybrid), Enterprise Size (Large Enterprises, and More), Application (Talent Acquisition and Onboarding, and More), End-User Industry (BFSI, Healthcare and Life Sciences, Information Technology and Telecom, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Europe HR Analytics Market Trends and Insights

Cloud-Native HR Analytics Adoption Accelerates Platform Consolidation

Cloud migration has become the strongest structural force shaping software selection across the region. Employers are moving away from on-premises reporting environments because SaaS delivery provides faster updates, lower maintenance costs, and a simpler path to rolling out new analytics features. That shift is especially visible in Germany, where P and I's valuation reached EUR 5.5 billion (USD 6.22 billion) in March 2025, and the company's revenue moved past EUR 300 million (USD 339 million) with annual growth above 20%. Cloud migration is also exposing data-quality issues that had been hidden inside siloed HR and payroll systems for years. Once those issues surface, organizations need more support for integration, governance, and ongoing model tuning. In the Europe HR analytics market, that dynamic is extending vendor involvement after the initial deployment and raising the commercial importance of services.

Data-Driven Recruitment and Retention Optimization Reshapes Talent Economics

Recruitment analytics is moving closer to core business planning because labor shortages remain broad and persistent across Europe. Cedefop's Labor and Skills Shortage Index shows pressure across high-, medium-, and low-skilled occupations, indicating that employers can no longer rely solely on basic vacancy tracking. Buyers are placing more value on platforms that can compare internal skills inventories with external labor signals and expected future demand. That is shifting commercial traction away from narrow applicant-tracking tools and toward broader talent-intelligence systems. Retention analytics is following the same path because employers need earlier warning signs as scarce talent becomes harder to retain. The European HR analytics market is therefore benefiting from a broader definition of recruiting return, encompassing skill gaps, hiring quality, and internal mobility within a single workflow.

GDPR and Sensitive Employee Data Governance Creates Analytics Friction

Data governance remains the most immediate operating constraint for many deployments across Europe. HR teams often hold the data they need in technical terms, but they cannot always reuse it across payroll, performance, recruiting, and attrition workflows without a fresh legal basis or stronger controls. The issue becomes more complex when employers move into profiling, special-category data, or cross-border processing, because those use cases can trigger deeper review and heavier documentation. National overlays also matter, especially in markets where employment privacy expectations are stricter and internal consultation requirements are more formal. That pushes vendors toward privacy-by-design architecture, narrower data access, and more granular permissions from the start of the project. In the Europe HR analytics market, these controls support long-term trust, but they also lengthen implementation cycles and raise near-term delivery costs.

Other drivers and restraints analyzed in the detailed report include:

- Predictive Workforce Planning Addresses EU-Wide Skills Shortages

- Employee Experience and Engagement Analytics Expansion Targets Continuous Listening

- Fragmented Multicountry Data Estates Constrain Cross-Border Workforce Intelligence

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Solutions held 62.37% of the Europe HR analytics market share in 2025, while services are projected to expand at a 16.94% CAGR through 2031. That spread reflects a market structure in which software still anchors contract value, but services increasingly determine project success and renewal quality. As vendors add predictive attrition models, generative AI assistants, and skills graph capabilities, implementation demands are becoming more specialized. Buyers are now less likely to treat deployment as a one-time setup and more likely to view it as a continuous operating program.

Professional services are benefiting from that shift because employers need support for data migration, model calibration, change management, and governance. This is particularly true when organizations are moving from broad HCM reporting to dedicated workforce intelligence platforms that must connect with existing HRIS and payroll stacks. The European HR analytics market is rewarding vendors that can pair software with advisory depth, because value now depends on adoption and output quality as much as on license access. Software still accounts for the larger revenue pool, especially in multi-year SaaS contracts with large enterprises and public-sector clients. At the same time, Germany's cloud-HR momentum, illustrated by P and I's growth and valuation trajectory, shows why service intensity is rising alongside platform adoption

Cloud deployment accounted for 68.41% of the market in 2025, which confirms that SaaS has become the default architecture for most new HR analytics buying decisions. Cloud systems are attractive because vendors can push product updates faster, support real-time data pipelines more easily, and handle compliance changes without large customer-side upgrade cycles. Hybrid deployment is the fastest-growing model, with a 17.86% CAGR from 2026 to 2031, because some employers still need part of the stack to remain under tighter internal control. That pattern is strongest in banking, healthcare, government, and other regulated settings where data residency, procurement rules, or sunk infrastructure costs still matter.

The on-premises segment is losing relative weight, but it is not disappearing from the region. Established public institutions and industrial organizations, especially in Germany, still maintain internal hosting for sensitive employee records and long-governed IT estates. Hybrid environments, therefore, act as a bridge, not simply as a temporary exception, because they let organizations modernize analytics without rewriting the full data architecture at once. The European HR analytics market is seeing a rise in cloud concentration, but the transition remains uneven across sectors and countries. Vendors with flexible deployment options, sovereign hosting arrangements, and strong integration layers are better placed to win regulated accounts and cross-border deals.

List of Companies Covered in this Report:

- Visier, Inc.

- One Model Inc.

- Crunchr B.V.

- Concentra Analytics Limited

- Syndio Solutions, Inc.

- Eightfold AI, Inc.

- Culture Amp Pty Ltd.

- Hi Bob, Inc.

- Beamery Inc.

- Humanyze, Inc.

- Leapsome GmbH

- Degreed, Inc.

- peopleIX GmbH

- functionHR GmbH

- HumanPanel Sp. z o.o.

- Firstmind ApS

- Scorius B.V.

- Panalyt Inc.

- 365Talents SAS

- retrain.ai Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Cloud-Native HR Analytics Adoption

- 4.2.2 Data-Driven Recruitment and Retention Optimization

- 4.2.3 Predictive Workforce Planning for Skills Shortages

- 4.2.4 Employee Experience and Engagement Analytics Expansion

- 4.2.5 EU Pay Transparency Directive Compliance Readiness

- 4.2.6 CSRD and ESRS S1 Workforce Disclosure Requirements

- 4.3 Market Restraints

- 4.3.1 GDPR and Sensitive Employee Data Governance Complexity

- 4.3.2 Fragmented Multicountry HRIS and Payroll Data Estates

- 4.3.3 Works Council Consultation Requirements for Monitoring-Adjacent Analytics

- 4.3.4 EU AI Act Compliance Burden for High-Risk Employment AI

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Buyers

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Comptetive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Solutions

- 5.1.2 Services

- 5.2 By Deployment Mode

- 5.2.1 Cloud

- 5.2.2 On-Premises

- 5.2.3 Hybrid

- 5.3 By End User Enterprise Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium-Sized Enterprises

- 5.4 By Application

- 5.4.1 Talent Acquisition and Onboarding

- 5.4.2 Retention and Attrition Management

- 5.4.3 Workforce Planning

- 5.4.4 Performance and Productivity Management

- 5.4.5 Compensation and Pay Equity

- 5.4.6 Employee Engagement and Experience

- 5.4.7 Learning and Skills Analytics

- 5.4.8 DEI and Workforce Compliance Analytics

- 5.4.9 Other Applications

- 5.5 By End User Industry

- 5.5.1 BFSI

- 5.5.2 Healthcare and Life Sciences

- 5.5.3 Information Technology and Telecom

- 5.5.4 Retail and E-commerce

- 5.5.5 Industrial Manufacturing

- 5.5.6 Government and Public Sector

- 5.6 By Geography

- 5.6.1 Germany

- 5.6.2 United Kingdom

- 5.6.3 France

- 5.6.4 Italy

- 5.6.5 Spain

- 5.6.6 Russia

- 5.6.7 Netherlands

- 5.6.8 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments).

- 6.4.1 Visier, Inc.

- 6.4.2 One Model Inc.

- 6.4.3 Crunchr B.V.

- 6.4.4 Concentra Analytics Limited

- 6.4.5 Syndio Solutions, Inc.

- 6.4.6 Eightfold AI, Inc.

- 6.4.7 Culture Amp Pty Ltd.

- 6.4.8 Hi Bob, Inc.

- 6.4.9 Beamery Inc.

- 6.4.10 Humanyze, Inc.

- 6.4.11 Leapsome GmbH

- 6.4.12 Degreed, Inc.

- 6.4.13 peopleIX GmbH

- 6.4.14 functionHR GmbH

- 6.4.15 HumanPanel Sp. z o.o.

- 6.4.16 Firstmind ApS

- 6.4.17 Scorius B.V.

- 6.4.18 Panalyt Inc.

- 6.4.19 365Talents SAS

- 6.4.20 retrain.ai Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and unmet-need assessment