|

시장보고서

상품코드

2065442

미국의 반려동물 건강 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)U.S. Companion Animal Health - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

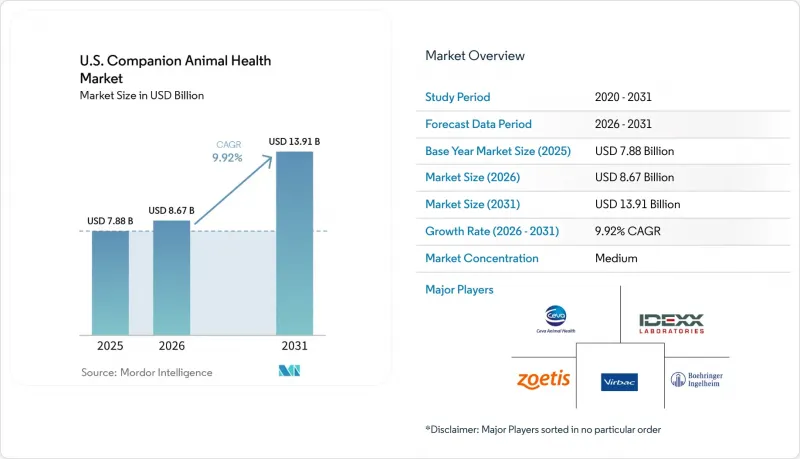

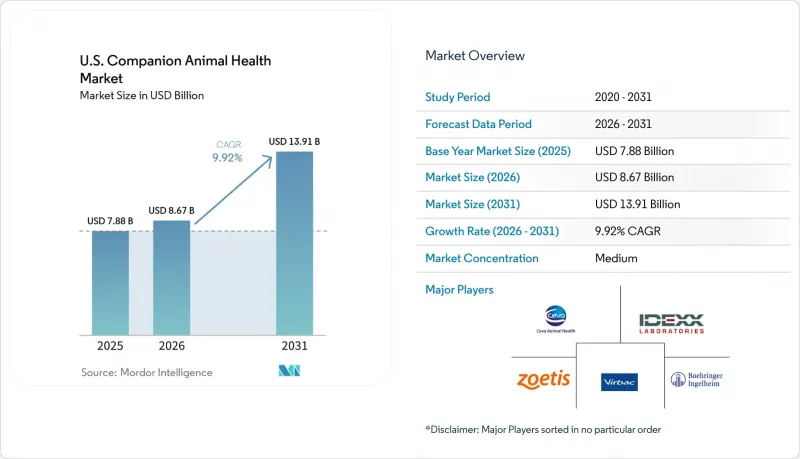

미국의 반려동물 건강 시장 규모는 2025년에 78억 8,000만 달러로 평가되었고, 2026년에 86억 7,000만 달러로 추정되고, 2031년까지 139억 1,000만 달러에 이를 것으로 예측되며, 2026-2031년 CAGR 9.92%로 성장할 전망입니다.

본 보고서는 동물 종별(개, 고양이, 말, 기타 반려동물), 제품 유형별(치료제, 진단제, 디지털 헬스 및 서비스), 적응증별(감염증 등), 유통 채널별(동물병원 및 진료소 내 약국 등)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

미국의 반려동물 건강 시장 동향 및 인사이트

반려동물 건강 관리의 프리미엄화와 인간화

미국의 반려동물 건강 시장은 각 가정에서 반려동물을 점점 더 중요하게 여기고 그 관리에 투자하게 됨에 따라 변화를 겪고 있습니다. 2025년까지 반려동물 산업 지출은 1,580억 달러에 달한 것으로 평가되었으며, 그중 수의학 분야가 414억 달러를 차지해 주요 부문으로 자리매김하고 있습니다. 이러한 추세에 따라 일상적인 건강 관리에 그치지 않고, 정밀 진단, 만성 질환 치료, 전문 서비스에 대한 수요가 증가하고 있습니다. 동물병원에서는 종합적인 치료 계획이 도입되는 한편, 제약사 및 서비스 제공업체들은 종양학, 통증 관리, 피부과, 장기 모니터링 분야에서 프리미엄 서비스를 확대되고 있습니다.

반려동물 보험의 확대와 자금 조달을 통한 치료 수용

미국의 반려동물 건강 시장에서 반려동물 보험은 치료 수용을 촉진하는 중요한 요인으로 자리 잡고 있습니다. 2025년에는 직접 보험료 수입이 54억 7,000만 달러에 달했으며, 두 자릿수 성장률을 기록했습니다. 보상 범위가 확대됨에 따라 반려동물 주인들은 특히 고액의 치료가 필요한 경우, 첨단 영상 진단, 전문의 의뢰 및 다제 병용 요법을 이용할 수 있게 되었습니다. 진료소의 금융 도구는 치료 결정 단계에서 고액 의료 서비스를 보다 쉽게 이용할 수 있도록 함으로써 이러한 추세를 더욱 뒷받침하고 있습니다.

고액의 본인 부담 치료비

미국의 반려동물 건강 시장에서 비용 부담 가능성은 여전히 중요한 과제로 남아 있습니다. 치료비 급등으로 인해 건강검진 시기가 늦어지거나, 진단 후의 사후 관리가 미흡해지거나, 임상적 필요성이 있음에도 불구하고 전문의에 의한 처치가 제한되는 경우가 있습니다. 정기 검진을 받지 않는 것은 서비스 수입 및 관련 상품 매출에 영향을 미칩니다. 특히 전문 의료의 경우, 비용이 가계 예산을 초과하기 때문에 고품질 서비스 이용이 제한되어 가장 큰 압박에 직면해 있습니다. 보험이나 자금 조달의 선택지가 확대되지 않는 한, 본인 부담 비용은 고소득 가구를 제외한 시장의 성장을 앞으로도 계속해서 제약할 것입니다.

부문별 분석

2025년, 미국 반려동물 건강 시장에서 개가 59.35%의 점유율을 차지했습니다. 이는 정형외과, 치과, 심장내과 등의 분야에서 치료 횟수가 증가한 데 기인합니다. 생물학적 제제의 도입도 수익을 더욱 끌어올렸으며, 2025년 초까지 100만 마리 이상의 개가 ‘리브렐라(Librela)’로 치료를 받게 되어, 고부가가치 통증 관리 제품의 급속한 보급이 확인되었습니다. 성장이 안정화되는 추세임에도 불구하고, 개는 여전히 주요 수익원입니다.

고양이 시장은 2026-2031년 연평균 성장률(CAGR) 11.15%를 나타낼 것으로 예측되며, 미국 반려동물 건강 시장에서 가장 빠르게 성장하는 부문이 될 전망입니다. 이러한 성장은 림프종 검출에서 97%의 특이도를 보이는 고양이용 액체 생검 프로토타입과 ‘RapidRead Dental for Feline’의 출시 등, 고양이에 특화된 혁신을 통해 뒷받침되고 있습니다. 말 및 기타 반려동물에 대해서는 예방 의료와 전문적인 치료를 통해 안정적인 수요가 유지되고 있습니다.

치료제는 만성 질환 및 전문 질환에 대한 신규 승인 및 적응증 확대의 혜택을 받아, 2025년 미국 반려동물 건강 시장 매출의 43.25%를 차지했습니다. 주요 발전 사항으로는 VETMEDIN이 전임상 단계의 점액종성 승모판 질환에 대한 승인을 획득한 것과, NUMELVI가 개의 가려움증 치료제로 승인된 것을 들 수 있습니다. 초점은 통증 관리, 단일클론 항체, 그리고 만성 질환 치료로 점차 옮겨가고 있습니다.

진단 분야는 2026-2031년 연평균 성장률(CAGR) 12.75%를 기록하며 가장 빠르게 성장하는 제품 카테고리가 될 것으로 전망됩니다. 동물병원에서는 Catalyst 화학 프로파일에 통합된 SDMA 신장 바이오마커 검사 등, 업무 흐름을 효율화하는 도구의 도입이 활발히 진행되고 있습니다. 디지털 헬스 플랫폼이 등장하는 가운데, 진단 분야는 워크플로우 통합을 통해 수익 성장의 주요 원동력으로 두각을 나타내고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.26According to Mordor Intelligence, the u.S. companion animal health market size is projected to be USD 7.88 billion in 2025, USD 8.67 billion in 2026, and reach USD 13.91 billion by 2031, growing at a CAGR of 9.92% from 2026 to 2031.

This report is Segmented by Animal Type (Dogs, Cats, Equine, Other Companion Animals), Product Type (Therapeutics, Diagnostics, Digital Health & Services), Indication (Infectious Diseases, Dand More), Distribution Channel (Veterinary Hospital & Clinic Pharmacies, and More). The Market Forecasts are Provided in Terms of Value (USD).

U.S. Companion Animal Health Market Trends and Insights

Premiumization and Humanization of Pet Healthcare

The United States companion animal health market is experiencing a shift as households increasingly prioritize pets and invest in their care. By 2025, the pet industry spending reached USD 158 billion, with veterinary care contributing USD 41.4 billion, making it a key category. This trend drives demand for advanced diagnostics, chronic disease treatments, and specialty services, moving beyond routine wellness. Clinics are adopting comprehensive treatment plans, while manufacturers and service providers expand premium offerings in oncology, pain management, dermatology, and long-term monitoring.

Pet Insurance Expansion and Financing-Led Care Acceptance

Pet insurance is becoming a critical driver of treatment acceptance in the United States companion animal health market. In 2025, direct premiums written reached USD 5.47 billion, reflecting double-digit growth. Expanding coverage enables pet owners to access advanced imaging, specialist referrals, and multi-drug protocols, particularly in high-cost treatments. Financing tools at clinics further support this trend by making expensive care more accessible at the decision point.

High Out-of-Pocket Treatment Costs

Affordability remains a key challenge in the United States companion animal health market. High treatment costs delay wellness visits, reduce diagnostic follow-through, and limit specialist procedure adoption despite clinical demand. Missed routine visits impact service revenue and related product sales. Specialty care faces the greatest pressure as costs outpace household budgets, restricting access to premium offerings. Without broader insurance and financing options, out-of-pocket expenses will continue to constrain growth outside higher-income households.

Other drivers and restraints analyzed in the detailed report include:

- AI-Enabled Diagnostics and Workflow Integration

- Vector-Borne Disease Preparedness and Screwworm Resilience

- Consolidator Formulary Discipline and Online Pharmacy Competition

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, dogs held 59.35% of the United States companion animal health market share, driven by higher treatment frequency in areas like orthopedics, dental care, and cardiology. The adoption of biologic therapies further boosted revenue, with over 1 million dogs treated with Librela by early 2025, showcasing the rapid scaling of high-value pain management products. Dogs remain the primary revenue anchor, even as growth stabilizes.

Cats are projected to grow at an 11.15% CAGR from 2026 to 2031, making them the fastest-growing segment in the United States companion animal health market. This growth is supported by species-specific innovations, such as a feline liquid biopsy prototype with 97% specificity for lymphoma detection and the launch of RapidRead Dental for Feline. Equine and other companion animals maintain stable demand through preventive care and specialized treatments.

Therapeutics accounted for 43.25% of the United States companion animal health market revenue in 2025, benefiting from new approvals and label expansions for chronic and specialty conditions. Key developments include VETMEDIN's clearance for preclinical myxomatous mitral valve disease and NUMELVI's approval for managing pruritus in dogs. The focus is shifting toward pain management, monoclonal antibodies, and chronic disease treatments.

Diagnostics is forecast to grow at a 12.75% CAGR from 2026 to 2031, becoming the fastest-growing product category. Clinics are adopting tools that streamline workflows, such as SDMA kidney biomarker testing integrated into Catalyst chemistry profiles. While digital health platforms are emerging, diagnostics stands out as a key driver of revenue growth through workflow integration.

List of Companies Covered in this Report:

- Anivive Lifesciences, Inc.

- Antech Diagnostics

- Bimeda

- Boehringer Ingelheim Animal Health USA Inc.

- Cencora, Inc. (MWI Animal Health)

- Ceva Animal Health, LLC

- Covetrus

- Dechra Veterinary Products LLC

- Elanco

- HIPRA USA, Inc.

- IDEXX

- Intervet Inc. d/b/a Merck Animal Health

- Mars, Incorporated (Science & Diagnostics)

- Norbrook, Inc.

- Nutramax Laboratories Veterinary Sciences, Inc.

- Patterson Companies, Inc. (Patterson Veterinary)

- PetIQ, LLC

- Vetoquinol USA, Inc.

- Virbac S.A.

- Zoetis

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Premiumization and Humanization of Pet Healthcare

- 4.2.2 Preventive Parasiticide and Vaccine Compliance

- 4.2.3 Pet Insurance Expansion and Financing-Led Care Acceptance

- 4.2.4 AI-Enabled Diagnostics and Workflow Integration

- 4.2.5 Vector-Borne Disease Preparedness and Screwworm Response Demand

- 4.3 Market Restraints

- 4.3.1 High Out-of-Pocket Treatment Costs

- 4.3.2 Affordability Gaps and Uneven Routine-Care Access

- 4.3.3 Consolidator Formulary Discipline and Online Pharmacy Leakage

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of new entrants

- 4.7.2 Bargaining power of suppliers

- 4.7.3 Bargaining power of buyers

- 4.7.4 Threat of substitutes

- 4.7.5 Intensity of rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Animal Type

- 5.1.1 Dogs

- 5.1.2 Cats

- 5.1.3 Equine

- 5.1.4 Other Companion Animals

- 5.2 By Product Type

- 5.2.1 Therapeutics

- 5.2.1.1 Vaccines

- 5.2.1.2 Parasiticides

- 5.2.1.3 Anti-Infectives

- 5.2.1.4 NSAIDs & Pain Management

- 5.2.1.5 Monoclonal Antibodies

- 5.2.1.6 Medical Feed Additives

- 5.2.1.7 Other Therapeutics

- 5.2.2 Diagnostics

- 5.2.2.1 Immunodiagnostic Tests

- 5.2.2.2 Molecular Diagnostics

- 5.2.2.3 Diagnostic Imaging

- 5.2.2.4 Point-of-Care Devices

- 5.2.2.5 Other Diagnostics

- 5.2.3 Digital Health & Services

- 5.2.3.1 Tele-medicine Platforms

- 5.2.3.2 Practice-Management Software

- 5.2.3.3 Wearable Monitoring Devices

- 5.2.1 Therapeutics

- 5.3 By Indication

- 5.3.1 Infectious Diseases

- 5.3.2 Dermatology/Allergy

- 5.3.3 Pain & Inflammation

- 5.3.4 Endocrine & Metabolic Disorders

- 5.3.5 Oncology

- 5.3.6 Cardiology

- 5.3.7 Others

- 5.4 By Distribution Channel

- 5.4.1 Veterinary Hospital and Clinic Pharmacies

- 5.4.2 Retail Pharmacies

- 5.4.3 E-commerce and Online Pharmacies

- 5.4.4 Others

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Anivive Lifesciences, Inc.

- 6.3.2 Antech Diagnostics

- 6.3.3 Bimeda, Inc.

- 6.3.4 Boehringer Ingelheim Animal Health USA Inc.

- 6.3.5 Cencora, Inc. (MWI Animal Health)

- 6.3.6 Ceva Animal Health, LLC

- 6.3.7 Covetrus, Inc.

- 6.3.8 Dechra Veterinary Products LLC

- 6.3.9 Elanco Animal Health Incorporated

- 6.3.10 HIPRA USA, Inc.

- 6.3.11 IDEXX Laboratories, Inc.

- 6.3.12 Intervet Inc. d/b/a Merck Animal Health

- 6.3.13 Mars, Incorporated (Science & Diagnostics)

- 6.3.14 Norbrook, Inc.

- 6.3.15 Nutramax Laboratories Veterinary Sciences, Inc.

- 6.3.16 Patterson Companies, Inc. (Patterson Veterinary)

- 6.3.17 PetIQ, LLC

- 6.3.18 Vetoquinol USA, Inc.

- 6.3.19 Virbac S.A.

- 6.3.20 Zoetis Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment