|

시장보고서

상품코드

2065443

미국의 투석 서비스 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)U.S. Dialysis Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

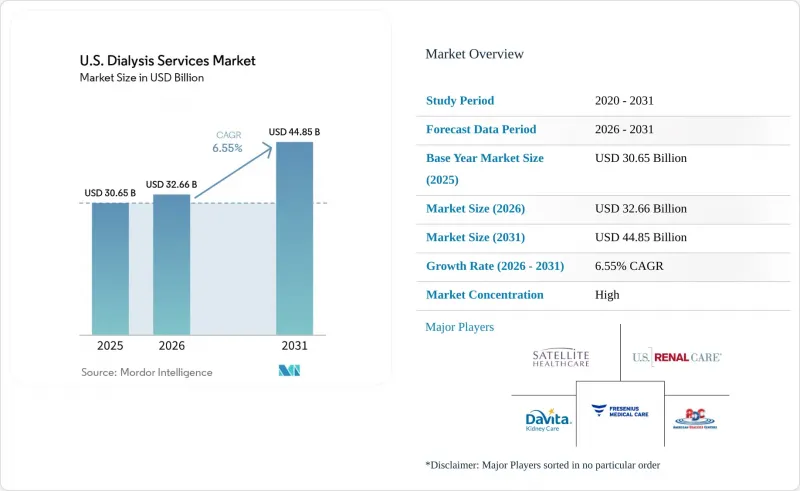

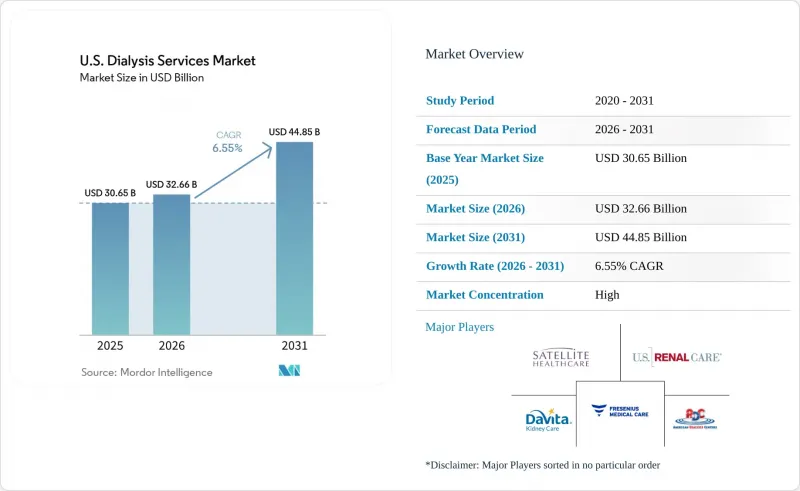

Mordor Intelligence에 의하면, 미국의 투석 서비스 시장 규모는 2025년 306억 5,000만 달러로 평가되었고, 2026년 326억 6,000만 달러로 추정되고, 2031년까지 448억 5,000만 달러로 확대될 전망이며, 2026-2031년 연평균 복합 성장률(CAGR)은 6.55%를 나타낼 전망입니다.

본 보고서는 치료 방법별(시설 내 혈액투석, 재택 혈액투석, 복막투석), 치료 실시 장소별(독립형 시설, 병원 내, 특별양로원, 환자 자택), 서비스 유형별(치료 제공, 재택 훈련, 급성기, 급성기 후, 케어 조정, 기타), 그리고 제공업체 유형별(LDO, 독립계, 비영리, 병원계, 신장 전문의 소유)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

미국의 투석 서비스 시장 동향 및 인사이트

말기 신부전(ESKD) 환자 수 증가가 구조적 수요를 견인하고 있습니다.

미국의 투석 서비스 시장은 장기적인 신장 대체 요법에 대한 수요가 증가함에 따라 꾸준히 성장하고 있습니다. 2002년부터 2022년 사이에 말기 신장 질환(ESKD)의 환자 수는 31.3% 증가했으며, 유병자 수는 매년 2만 명씩 증가하고 있습니다. 80만 8,000명 이상의 미국인이 말기 신부전(ESKD)을 앓고 있으며, 이 중 68%가 투석에 의존하고 있어 안정적인 수요가 발생하고 있습니다. 메디케어의 급여가 경제적 안정을 보장하는 한편, CMS(미국 의료보험·의료보조 서비스 센터)는 2026년까지 7,600곳의 ESRD(말기 신부전) 시설에 60억 달러가 지급될 것으로 전망하고 있으며, 이는 임상 인프라에 대한 투자를 촉진하고 있습니다. 다양한 환경에서 장기 요양 관리에 주력하는 의료 제공업체는 성장을 위해 더 유리한 입장에 있습니다.

고령화와 당뇨병 유병률이 환자 수 증가를 가속화

미국에서 당뇨병과 고혈압은 여전히 신장 질환의 주요 원인이며, 고령화가 진행됨에 따라 그 부담은 더욱 커지고 있습니다. 아프리카계 미국인은 백인 미국인에 비해 말기 신부전(ESKD) 발병 위험이 4배 이상 높으며, 히스패닉계 및 아메리카 원주민 인구는 발병 가능성이 2배 이상 높습니다. 이러한 격차가 특정 지역 수요를 형성하고 있으므로, 의료 제공업체는 인력 배치, 의뢰 체계, 지원 서비스를 지역의 필요에 맞추어 조정해야 합니다. 개별적인 요구에 맞춘 시설 확충 및 치료 계획 조정을 통해, 부담이 큰 환자층을 돌보는 운영 사업자는 증가하는 환자 수를 관리하고 양질의 치료 성과를 확보하는 데 있어 더 유리한 입장에 있습니다.

간호사 및 기술자 부족이 치료 역량 확대를 제약하고 있습니다.

2026년에도 투석 서비스 제공은 숙련된 간호사, 기술자 및 지원 인력에 의존하고 있기 때문에 인력 부족이 계속해서 미국의 투석 서비스 시장을 제약하고 있습니다. 상근 신장병 사회복지사의 25% 가까이가 1년 이내에 퇴직할 예정이며, 이는 직접적인 돌봄 업무에만 국한되지 않는 인력 배치상의 문제를 여실히 드러내고 있습니다. CMS의 ‘적용 조건(Conditions for Coverage)’에 따르면, 말기 신부전(ESRD) 시설에 대해 특정 인력 배치 및 치료 프로토콜이 의무화되어 있으며, 인력 부족은 일정 관리, 규정 준수, 환자의 접근성에 영향을 미치는 중대한 문제가 되고 있습니다. 지방 지역은 인재 확보의 기반이 제한적이고 통근 거리도 길기 때문에 가장 큰 영향을 받고 있습니다. 반면, 소규모 사업체의 경우 직원을 재배치할 자원이 부족하여 곤경에 처해 있습니다. 특히 취약한 지역 시장의 경우, 만성적인 인력 부족이 치료 역량 확대를 저해할 우려가 있습니다.

부문별 분석

2025년, 시설 내 혈액투석은 확립된 인프라, 의사가 익숙하게 시행해 온 치료법, 그리고 운영 관행에 힘입어 미국 투석 서비스 시장의 65.35%를 차지했습니다. 많은 환자들은 재택 치료로 전환하기 전에 의료기관에서 치료를 시작하여 상태를 안정시킵니다. 프레제니우스 메디컬 케어의 보고에 따르면, 미국 내 시설 내 투석 장치의 90% 가까이가 이 기업의 제품인 것으로 나타나, 장비 표준화의 중요성이 부각되고 있습니다. 복막투석 시장 점유율은 작지만, 의료기관 밖에서 치료를 받으면서도 의료 제공업체와 환자 간의 관계를 유지할 수 있기 때문에 여전히 중요한 위치를 차지하고 있습니다.

재택 혈액투석은 2031년까지 연평균 성장률(CAGR) 7.12%를 나타낼 것으로 예측되며, 가장 빠르게 성장하는 치료법이 될 전망입니다. CMS가 2025 회계연도 ESRD PPS 규정에 따라 급성 신장 손상 환자에 대한 재택 및 자가 투석 교육에 대한 지급 범위를 확대함에 따라, 비용 측면의 장벽이 낮아져 의료 제공업체들이 재택 치료 시스템에 대한 투자를 촉진하고 있습니다. 의료 시장은 치료 제공뿐만 아니라 환자의 준비와 재택 지원을 중시하는 균형 잡힌 치료법 조합으로 점차 전환되고 있습니다. 프레제니우스사는 네트워크 및 기술 최적화를 반영하여, 2026년에 실적이 부진한 클리닉에서 철수하는 한편, 5008X CAREsystem 도입을 추진할 예정입니다.

2025년, 독립형 외래 투석 센터는 69.67%의 시장 점유율을 차지했으며, ESRD PPS 체계 하에서의 운영 효율성과 규모 면에서의 우위를 바탕으로 미국 투석 서비스 시장에서 주도적인 위치를 유지했습니다. CMS에 따른 2026년 보수 인상률은 병원 부속 시설의 경우 1.5%인 반면, 독립형 센터는 2.2%로 나타나, 이로 인해 독립형 센터의 경제적 입지가 더욱 강화되고 있습니다. 병원 내 투석 센터는 중증도가 높은 환자나 보다 세심한 모니터링이 필요한 입원 환자의 투석 시작에 있어 여전히 없어서는 안 될 존재입니다.

재택 투석은 보험 급여 제도의 개선, 연수비 지원, 그리고 이동성 향상에 힘입어 2031년까지 연평균 성장률(CAGR) 8.35%로 성장할 것으로 전망됩니다. 2025년 ESRD PPS 규정에 따른 급성 신장 손상에 대한 재택 투석 적용 범위 확대가 이러한 성장을 뒷받침하고 있습니다. 숙련된 간호 시설이나 급성기 후 돌봄 시설 역시, 특히 여러 돌봄 환경을 오가는 고령 환자나 복잡한 병세를 가진 환자에게 중요한 역할을 하고 있습니다. 향후 돌봄 제공 장소의 동향은 재택 치료의 시작, 이송 및 사후 관리 간의 원활한 연계에 달려 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

LSH 26.06.24According to Mordor Intelligence, the u.S. dialysis services market size is projected to expand from USD 30.65 billion in 2025 and USD 32.66 billion in 2026 to USD 44.85 billion by 2031, registering a CAGR of 6.55% between 2026 to 2031.

This report is Segmented by Modality (In-Center HD, Home HD, Peritoneal Dialysis), Site of Care (Freestanding, Hospital-Based, SNF, Patient Home), Service Type (Treatment Delivery, Home Training, Acute, Post-Acute, Care Coordination, Others), and Provider Type (LDOs, Independent, Nonprofit, Hospital-Affiliated, Nephrologist-Owned). The Market Forecasts are Provided in Terms of Value (USD).

U.S. Dialysis Services Market Trends and Insights

Rising ESKD Treatment Population Drives Structural Demand

The United States dialysis services market is growing steadily due to the increasing need for long-term renal replacement therapy. Between 2002 and 2022, end-stage kidney disease (ESKD) cases rose by 31.3%, with prevalence increasing by 20,000 cases annually. Over 808,000 Americans live with ESKD, and 68% depend on dialysis, creating a stable demand. Medicare coverage ensures financial stability, while CMS projects USD 6 billion in payments to 7,600 ESRD facilities by 2026, driving investments in clinical infrastructure. Providers focusing on long-term care management across diverse settings are better positioned for growth.

Aging Demographics and Diabetes Prevalence Compound Patient Volumes

Diabetes and hypertension remain key drivers of renal disease in the United States, with aging demographics further compounding the burden. Black Americans face over four times the risk of developing ESKD compared to White Americans, while Hispanic and Native American populations are more than twice as likely to be affected. These disparities shape demand in specific regions, requiring providers to align staffing, referrals, and support services with local needs. Operators addressing high-burden populations through tailored expansions and care coordination are better equipped to manage growing patient volumes and ensure quality outcomes.

Nurse and Technician Shortages Constrain Treatment Capacity Expansion

In 2026, workforce shortages continue to constrain the United States dialysis services market, as dialysis delivery relies on skilled nurses, technicians, and support staff. Nearly 25% of full-time nephrology social workers plan to resign within the year, highlighting staffing challenges that extend beyond direct care roles. CMS Conditions for Coverage mandate specific staffing and care protocols for ESRD facilities, making staffing gaps a critical issue affecting scheduling, compliance, and patient access. Rural areas face the greatest impact due to limited recruitment pools and travel distances, while smaller operators struggle with fewer resources to reassign staff. Persistent shortages may hinder capacity growth, particularly in fragile local markets.

Other drivers and restraints analyzed in the detailed report include:

- Home Dialysis Adoption Push Reconfigures the Care Delivery Footprint

- Medicare Advantage ESRD Enrollment Transforms Payer Dynamics

- Medicare Reimbursement Structure Limits Margin Recovery

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, In-Center Hemodialysis accounted for 65.35% of the United States dialysis services market, driven by established infrastructure, physician familiarity, and operational routines. Many patients begin and stabilize treatment in clinical settings before transitioning to home options. Fresenius Medical Care reported that nearly 90% of in-center dialysis machines in the United States are their devices, highlighting the role of equipment standardization. Peritoneal dialysis, while smaller in share, remains relevant as it enables treatment outside clinics while maintaining provider-patient relationships.

Home Hemodialysis is projected to grow at a 7.12% CAGR through 2031, making it the fastest-growing modality. CMS's expansion of home and self-dialysis training payments for acute kidney injury patients under the CY2025 ESRD PPS rule reduces cost barriers, encouraging providers to invest in home treatment systems. The market is shifting toward a balanced modality mix, emphasizing patient preparation and home support alongside treatment delivery. Fresenius plans to exit underperforming clinics in 2026 while advancing its 5008X CAREsystem rollout, reflecting network and technology optimization.

Freestanding Outpatient Dialysis Centers held a 69.67% share in 2025, maintaining their lead in the United States dialysis services market due to operational efficiency and scale under the ESRD PPS framework. CMS's 2026 payment increase of 2.2% for freestanding centers, compared to 1.5% for hospital-based facilities, further strengthens their economic position. Hospital-Based Dialysis Centers remain essential for higher-acuity patients and inpatient starts requiring closer monitoring.

Patient Home Dialysis is forecasted to grow at an 8.35% CAGR through 2031, driven by improved reimbursement, training payments, and portability. The CY2025 ESRD PPS rule's expansion of acute kidney injury home dialysis coverage supports this growth. Skilled nursing and post-acute settings also play a role, particularly for older and complex patients transitioning through multiple care settings. Future site-of-care dynamics will depend on seamless coordination of home onboarding, transport, and follow-up care.

List of Companies Covered in this Report:

- American Dialysis Centers

- Arizona Kidney Disease & Hypertension Centers

- Atlantic Dialysis Management Services, LLC

- Centers for Renal Dialysis

- Central Dialysis

- Concerto Renal Services

- DaVita

- Dialysis Care Center

- Dialysis Clinic, Inc.

- Dialyze Direct

- Fresenius Medical Care AG

- Innovative Renal Care

- Northwest Kidney Centers

- Premier Dialysis

- Puget Sound Kidney Centers

- Rendevor Dialysis

- Satellite Healthcare

- Southeastern Renal Dialysis

- U.S. Renal Care

- United Renal Services

- Universal Kidney Centers

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising ESKD Treatment Population

- 4.2.2 Aging and Diabetes-Linked Renal Burden

- 4.2.3 Home Dialysis Adoption Push

- 4.2.4 Medicare Base-Rate Support for ESRD Services

- 4.2.5 Staff-Assisted Home Dialysis Expansion

- 4.2.6 Medicare Advantage ESRD Enrollment Scale-Up

- 4.3 Market Restraints

- 4.3.1 Nurse and Technician Shortages

- 4.3.2 Medicare-Heavy Reimbursement Pressure

- 4.3.3 Oral Drug Bundle Cost Absorption Risk

- 4.3.4 Certificate-of-Need and Referral Lock-in Barriers

- 4.4 Supply/ Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining power of suppliers

- 4.7.2 Bargaining power of buyers

- 4.7.3 Threat of new entrants

- 4.7.4 Threat of substitutes

- 4.7.5 Intensity of competitive rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Modality

- 5.1.1 In-Center Hemodialysis

- 5.1.2 Home Hemodialysis

- 5.1.3 Peritoneal Dialysis

- 5.2 By Site of Care

- 5.2.1 Freestanding Outpatient Dialysis Centers

- 5.2.2 Hospital-Based Dialysis Centers

- 5.2.3 Skilled Nursing Facility Dialysis

- 5.2.4 Patient Home Dialysis

- 5.3 By Service Type

- 5.3.1 Dialysis Treatment Delivery Services

- 5.3.2 Home Dialysis Training and Support Services

- 5.3.3 Acute and Inpatient Dialysis Services

- 5.3.4 Post-Acute and Nursing Home Dialysis Services

- 5.3.5 Renal Care Coordination Services

- 5.3.6 Others

- 5.4 By Provider Type

- 5.4.1 Large Dialysis Organizations

- 5.4.2 Independent Regional Providers

- 5.4.3 Nonprofit Dialysis Providers

- 5.4.4 Hospital and Health-System Affiliated Providers

- 5.4.5 Nephrologist-Owned and Joint-Venture Providers

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 American Dialysis Centers

- 6.3.2 Arizona Kidney Disease & Hypertension Centers

- 6.3.3 Atlantic Dialysis Management Services, LLC

- 6.3.4 Centers for Renal Dialysis

- 6.3.5 Central Dialysis

- 6.3.6 Concerto Renal Services

- 6.3.7 DaVita Inc.

- 6.3.8 Dialysis Care Center

- 6.3.9 Dialysis Clinic, Inc.

- 6.3.10 Dialyze Direct

- 6.3.11 Fresenius Medical Care AG

- 6.3.12 Innovative Renal Care

- 6.3.13 Northwest Kidney Centers

- 6.3.14 Premier Dialysis

- 6.3.15 Puget Sound Kidney Centers

- 6.3.16 Rendevor Dialysis

- 6.3.17 Satellite Healthcare

- 6.3.18 Southeastern Renal Dialysis

- 6.3.19 U.S. Renal Care

- 6.3.20 United Renal Services

- 6.3.21 Universal Kidney Centers

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment