|

시장보고서

상품코드

2065560

건설용 ERP 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Construction Enterprise Resource Planning - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

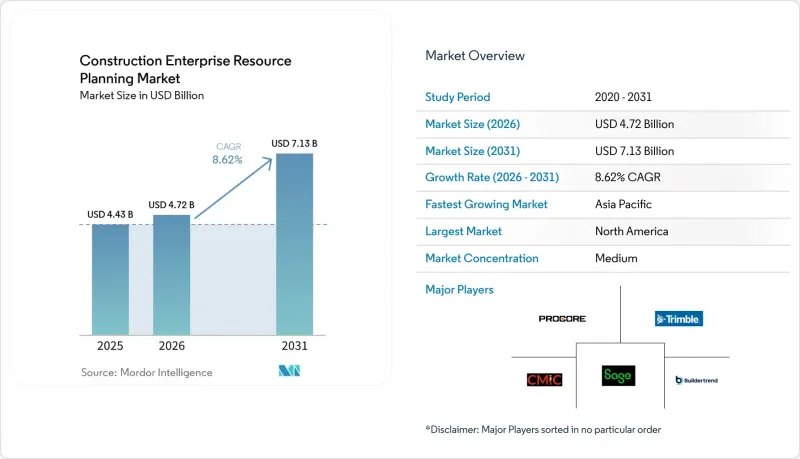

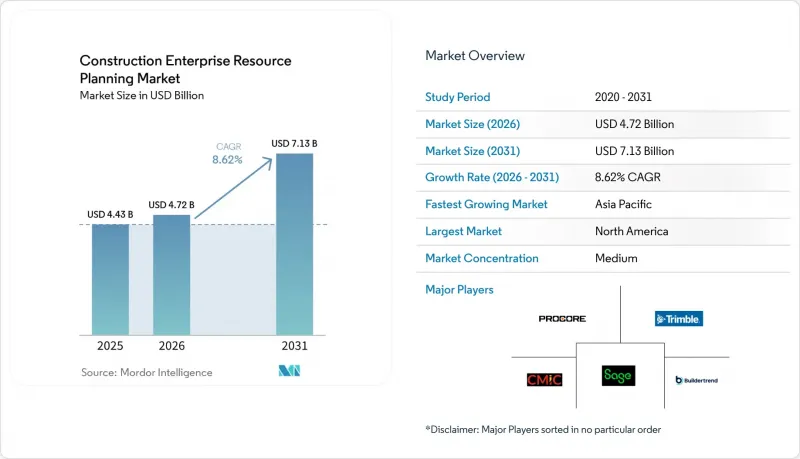

Mordor Intelligence에 의하면, 건설용 ERP 시장 규모는 2025년 44억 3,000만 달러로 평가되었고, 2026년 47억 2,000만 달러로 추정되고, 2031년까지 71억 3,000만 달러로 확대될 것으로 예측되며, 2026-2031년 연평균 복합 성장률(CAGR)은 8.62%를 나타낼 전망입니다.

본 보고서는 배포 방식별(클라우드, 온프레미스, 하이브리드), 기업 규모별(중소기업, 대기업), 솔루션별(소프트웨어 및 서비스), 최종 용도별(주택 건설, 상업용 건설, 인프라·토목 공사, 산업용 건설), 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 건설용 ERP 시장 동향 및 인사이트

클라우드 ERP 솔루션 도입 확대

2025년에는 클라우드 도입이 매출의 61.10%를 차지했고, 연평균 성장률(CAGR) 11.20%로 성장하고 있으며, 이는 건설 ERP 시장 전체의 성장률을 300 베이시스 포인트 가까이 상회하는 수치입니다. 구독형 가격 책정을 통해 자본 지출이 운영비로 전환되어, 설비 및 인건비에 충당할 자금이 확보됩니다. 2025년 미국 재향군인부가 171개 의료 센터를 통합 클라우드 플랫폼으로 이전한 사례에서 볼 수 있듯이, 공공 기관 역시 클라우드의 신뢰성을 인정하고 있습니다. 현재 각 벤더사는 멀티테넌트 기능과 역할 기반 포털을 패키지화하여, 하청업체의 온보딩을 몇 분 만에 완료하고 이메일 교환을 줄일 수 있게 되었습니다. 2025년에 Procore가 획득한 연방 위험 및 승인 관리 프로그램(FedRAMP) 인증은 미국 연방 프로젝트에서 필수 요건으로 규정되어 있습니다. 유럽의 중소기업들도 이러한 흐름에 동참하고 있습니다. 유로스타트의 데이터에 따르면, 중소기업과 대기업 간의 도입률 차이는 48퍼센트포인트에 달하지만, 각 벤더사들은 프로젝트별 종량제 요금제를 도입함으로써 이러한 격차를 점차 좁혀가고 있습니다.

건설 분야의 정부 인프라 지출 증가

지출 증가세가 뚜렷합니다. 미국의 ‘인프라 투자 및 고용법’에 따라 5년간 1조 2,000억 달러가 투입되는 한편, 영국의 2025년도 예산에서는 주요 교통 회랑에 17억 파운드(21억 5,000만 달러)가 추가로 배정되었습니다. 중동 및 북아프리카에서는 2025년 1-3분기에 1,570억 달러 상당의 계약이 발주되었으며, 그중 사우디아라비아만으로도 31%를 차지하고 있습니다. 인도의 ‘국가 인프라·파이프라인’ 및 ‘스마트 시티 미션’에 따라, 투자액은 2025년 1,907억 달러에서 2030년까지 2,806억 달러로 증가할 전망입니다. 이러한 메가 프로젝트에는 일반적인 소프트웨어 제품군으로는 제공할 수 없는 합작 사업 회계, 획득 가치 분석, 다중 통화 연결 모듈이 필요합니다.

초기 도입 및 맞춤 설정 비용의 높음

벤치마크 조사에 따르면, 직원 50명을 둔 기업이 2025년에 도입 첫해에 지출한 비용은 기회 비용을 제외하고 14만-21만 달러였습니다. 순이익률이 2%-4%인 상황에서 6자리 숫자에 달하는 지출은 많은 입찰자들을 주저하게 만들고 있습니다. Buildertrend나 Projul의 입문용 구독 요금제는 초기 비용 부담을 줄여주지만, 고급 연동 기능이나 API 기능이 제외되어 있어 대부분의 경우 3년 이내에 비용이 드는 플랫폼으로 전환할 수밖에 없습니다.

부문별 분석

2025년에는 클라우드 솔루션이 매출의 61.10%를 차지했으며, 연평균 성장률(CAGR) 11.20%로 성장하고 있습니다. 이러한 강점은 서버 및 백업에 대한 책임을 공급업체 측으로 이전하는 구독 모델에 기반을 두고 있으며, 이를 통해 설비 투자를 절감할 수 있다는 점에 있습니다. 공공 기관들이 연방 고속도로나 의료시설을 위해 FedRAMP 인증 도구를 도입함에 따라, 클라우드 도입과 관련된 건설 ERP 시장 규모가 급격히 확대될 것으로 전망됩니다. 대역폭이 좁은 지역에서는 계약업체들이 재무 관리의 핵심 기능을 온프레미스에 유지하면서 현장 협업을 클라우드로 전환하고 있기 때문에 하이브리드 구성이 급속히 확대되고 있습니다. 벤더들이 영구 라이선스를 단계적으로 폐지함에 따라 온프레미스 도입은 축소되는 추세이지만, 엄격한 데이터 주권 규정에 얽매여 있는 방위 관련 계약업체들 사이에서는 여전히 자리 잡고 있습니다.

현재 건설 ERP 시장에서는 신속한 프로비저닝 기능을 탑재한 공급업체들이 우위를 점하고 있습니다. Procore의 FedRAMP 인증은 수익성이 높은 연방 정부 시장을 개척해 주었으며, 경쟁사들은 유사한 인증을 획득하기 위해 12-18개월의 투자를 감수해야만 합니다. 멀티테넌트 아키텍처를 통해 종합 건설사는 하도급업체용 포털을 즉시 개설할 수 있으며, 이메일을 통한 RFI(정보 요청)가 필요 없어집니다. 로우코드 워크플로우 엔진을 통해, 표준적인 원가 가산 방식이나 단가 방식의 프로젝트에서 도입 기간이 더욱 단축됩니다.

2025년에는 수백 건의 진행 중인 프로젝트를 아우르는 다년 계약에 힘입어 대기업이 매출 점유율의 58.20%를 차지했습니다. 그러나 중소기업은 2031년까지 연평균 성장률(CAGR) 10.40%를 기록하며 성장하고 있어, 그동안의 도입 격차를 점차 좁혀가고 있습니다. 정부가 디지털화 지원금을 도입함에 따라, 중소기업이 차지하는 건설 ERP 시장 점유율은 상승할 것으로 예측됩니다. 말레이시아에서는 현재 소프트웨어 비용의 50%가 지원 대상입니다. 그러나 자금 조달에 대한 제약은 여전히 남아 있어, 2025년에는 유럽 중소기업의 44%가 신용 관련 어려움을 호소했습니다. Buildertrend와 Projul의 단계별 가격 책정 방식 덕분에 엔트리 레벨의 연간 이용료는 1만 달러 미만이지만, 통합 기능이나 차량 관리 모듈이 포함되지 않은 경우 숨겨진 업그레이드 비용이 발생할 수 있습니다.

도입에 따른 부담은 여전히 현실적인 과제입니다. 직원 50명의 기업의 경우, 6개월간의 도입 기간 동안 핵심 직원의 근무 시간 중 10%-20%를 할애하게 되어, 수익 창출에 직결되는 업무에 차질이 생깁니다. 이에 대응하기 위해 각 벤더사는 주택 리모델링, 상업시설 인테리어 공사, 대규모 토목 공사에 사용할 수 있도록 사전 설정된 템플릿을 함께 제공하고 있으며, 중소기업이 8주 이내에 시스템을 가동할 수 있도록 함으로써 현금 흐름을 보호하고 가치 실현까지 걸리는 시간을 단축하고 있습니다.

지역별 분석

2025년, 북미는 전 세계 매출의 43.70%를 차지했습니다. 이는 미국 교통부의 2026년도 예산에 책정된 1,471억 달러라는 막대한 예산과, 엄격한 데이비스-베이컨법에 근거한 인정 급여 규정에 힘입은 결과입니다. 캐나다는 ‘Investing in Canada Plan(캐나다 투자 계획)’을 통해 12년 동안 총 1,800억 캐나다 달러(1,330억 달러)를 투자하여, 지역 매출의 약 8%-10%를 차지하고 있습니다. 멕시코에서는 니어쇼어링을 원동력으로 한 공장 건설 붐에 힘입어 대형 도급업체들 사이에서 ERP 시범 도입이 진행되고 있지만, 중소규모 기업에서는 여전히 스프레드시트가 선호되고 있습니다. 미국의 금리 인상으로 주택 착공 건수는 둔화되고 있지만, 건설 ERP 시장은 계약 갱신 및 모듈 추가를 통한 안정적인 유지관리 수익을 계속해서 의지하고 있습니다.

아시아태평양은 가장 빠르게 성장하는 지역으로, 2031년까지의 연평균 성장률(CAGR)은 9.60%로 전망됩니다. 인도는 2030년까지 건설 지출을 2,806억 달러로 늘리겠다는 목표를 세웠으며, 사우디아라비아의 건설 파이프라인은 2030년까지 연평균 성장률(CAGR) 8.7%를 기록하며 1,744억 달러에 달할 전망이며, 아랍어 지원 및 부가가치세(VAT) 대응 시스템에 대한 수요를 뒷받침하고 있습니다. 중국에서는 ‘Golden Tax’와의 통합이나 데이터 소재지에 관한 법률과 같은 장애물로 인해 ERP 도입 현황은 여전히 편차를 보이고 있습니다. 일본의 대형 건설사 5곳은 엔터프라이즈 스위트를 표준화했으며, 현재는 예측 유지보수를 추진하기 위해 디지털 트윈을 시범 운영 중입니다. 동남아시아에서는 중소기업을 대상으로 한 보조금이 활용되고 있으며, 통신 환경의 개선에 따라 건설 ERP 시장의 확산이 진행되고 있습니다.

2025년, 유럽은 전 세계 매출의 상당 부분을 차지했습니다. 영국에서는 로어 템즈 크로싱(Lower Thames Crossing) 등의 프로젝트를 통해 17억 파운드(21억 5,000만 달러)가 추가로 투입되면서, 하청업체들의 규정 준수 자동화에 대한 수요가 촉진되었습니다. 독일과 프랑스에서는 각국의 상법에 따라 청구서 자동화가 추진되고 있으며, ISO 19650-4에 따라 BIM에서 ERP로의 데이터 교환이 의무화되어 있습니다. 중동에서는 2025년에 사우디아라비아와 아랍에미리트가 합쳐서 전 세계 건설 ERP 시장 매출의 상당 부분을 차지할 것으로 예상되며, 아랍어 팩과 다중 통화 원장을 통합한 플랫폼을 선호하는 메가 프로젝트가 진행 중입니다. 남미와 아프리카는 여전히 초기 단계이지만, EVOP이나 SYNEco와 같은 현지 벤더들이 지역 세무 포털과의 전자 청구서 연동 기능을 통해 틈새 시장을 개척하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJYAccording to Mordor Intelligence, the construction eRP market size is projected to expand from USD 4.43 billion in 2025 and USD 4.72 billion in 2026 to USD 7.13 billion by 2031, registering an 8.62% CAGR between 2026 and 2031.

This report is Segmented by Deployment Mode (Cloud-Based, On-Premise, and Hybrid), Enterprise Size (Small and Medium Enterprises and Large Enterprises), Solution (Software and Services), End Use (Residential Construction, Commercial Construction, Infrastructure and Civil Engineering, and Industrial Construction), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Construction Enterprise Resource Planning Market Trends and Insights

Growing Adoption of Cloud-Based ERP Solutions

Cloud deployment accounted for 61.10% of revenue in 2025 and is growing at a 11.20% CAGR, nearly 300 basis points above the Construction ERP market. Subscription pricing converts capital expenditures into operating expenses, freeing cash for equipment and labor. Public agencies validate cloud reliability, as seen when the United States Department of Veterans Affairs migrated 171 medical centers to a unified cloud platform in 2025. Vendors now package multi-tenancy and role-based portals so subcontractors can be onboarded in minutes, reducing email back-and-forth. The Federal Risk and Authorization Management Program (FedRAMP) certification, secured by Procore in 2025, has become mandatory for U.S. federal projects. European small firms are also entering the fold: Eurostat shows a 48-percentage-point adoption gap between small and large companies, which vendors are narrowing through pay-per-project tiers.

Increasing Government Infrastructure Spending on Construction

Spending momentum is pronounced. The United States Infrastructure Investment and Jobs Act channels USD 1.2 trillion over five years, while the United Kingdom's 2025 Budget added GBP 1.7 billion (USD 2.15 billion) for major transport corridors. In the Middle East and North Africa, USD 157 billion in contracts were let during the first three quarters of 2025, with Saudi Arabia alone accounting for 31%. India's National Infrastructure Pipeline and Smart Cities Mission underpin a rise from USD 190.7 billion in 2025 to USD 280.6 billion by 2030. These mega-projects demand joint-venture accounting, earned-value analysis, and multicurrency consolidation modules that generic suites cannot supply.

High Upfront Implementation and Customization Costs

Benchmarking shows a 50-person firm spent USD 140,000-210,000 on first-year deployment in 2025, excluding opportunity cost. With net margins at 2%-4%, six-figure outlays deter many bidders. Entry-level subscriptions from Buildertrend and Projul lower sticker shock but omit advanced consolidation and API features, often forcing a costly re-platform within three years.

Other drivers and restraints analyzed in the detailed report include:

- Rising Demand for Mobile-First and Remote Collaboration Capabilities

- Stricter Regulatory Compliance for Construction Accounting and Reporting

- Cybersecurity and Data-Privacy Concerns

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud solutions accounted for 61.10% of revenue in 2025 and are growing at a 11.20% CAGR. This strength is anchored in subscription models that shift servers and backups to the vendor's responsibility, thereby reducing capital outlays. The Construction ERP market size for cloud deployments is forecast to climb sharply as public bodies adopt FedRAMP-authorized tools for federal highways and healthcare facilities. Hybrid configurations are growing rapidly because contractors in low-bandwidth regions keep financial cores on-premises while shifting field collaboration to the cloud. On-premise is contracting as vendors phase out perpetual licenses, yet it persists among defense contractors bound by strict data-sovereignty rules.

The Construction ERP market now rewards suppliers that embed rapid provisioning. Procore's FedRAMP authority has opened lucrative federal channels, forcing rivals to invest 12-18 months to earn similar clearance. Multi-tenant architectures allow general contractors to spin up subcontractor portals immediately, eliminating email-based RFIs. Low-code workflow engines further compress implementation timelines for standard cost-plus or unit-price projects.

Large enterprises held 58.20% of revenue share in 2025, buoyed by multi-year enterprise agreements covering hundreds of active projects. However, SMEs are advancing at a 10.40% CAGR to 2031, narrowing historical adoption gaps. The Construction ERP market share commanded by SMEs is expected to climb as governments launch digitalization grants. Malaysia now subsidizes 50% of software costs. Yet financing constraints linger: 44% of European SMEs reported credit difficulties in 2025. Tiered pricing from Buildertrend and Projul brings entry-level annual fees below USD 10,000, although missing consolidation and fleet modules can create hidden upgrade costs.

Implementation fatigue remains real. A 50-person company allocates 10%-20% of key staff hours during a six-month rollout, disrupting billable work. To compete, vendors are bundling pre-configured templates for residential remodeling, tenant improvement, or heavy civil so SMEs can go live in under eight weeks, thus protecting cash flow and improving time-to-value.

Geography Analysis

North America generated 43.70% of global revenue in 2025, energized by USD 147.1 billion in the United States Department of Transportation's 2026 budget and stringent Davis-Bacon certified payroll rules. Canada contributes roughly 8%-10% of regional sales through its Investing in Canada Plan, totaling CAD 180 billion (USD 133 billion) over 12 years. Mexico's nearshoring-driven factory boom is sparking ERP pilots among tier-one contractors, although smaller firms still favor spreadsheets. U.S. interest-rate hikes temper residential starts, but the Construction ERP market continues to bank on steady maintenance income from renewals and module add-ons.

Asia-Pacific is the fastest-growing region, with a 9.60% CAGR through 2031. India targets USD 280.6 billion in construction outlay by 2030, and Saudi Arabia's pipeline is slated to reach USD 174.4 billion at 8.7% CAGR by 2030, catalyzing demand for Arabic-language, VAT-ready systems. China's ERP adoption remains fragmented due to integration hurdles with Golden Tax and data-residency laws. Japan's Big Five contractors have standardized on enterprise suites and now pilot digital twins to drive predictive maintenance. Southeast Asia enjoys SME-friendly grants and is seeing Construction ERP market penetration grow as connectivity improves.

Europe captured significant percentage of global sales in 2025. The United Kingdom added GBP 1.7 billion (USD 2.15 billion) for projects such as the Lower Thames Crossing, spurring demand for subcontractor compliance automation. Germany and France automate invoicing under national commercial codes, while ISO 19650-4 drives BIM-to-ERP data exchange mandates. In the Middle East, Saudi Arabia and the United Arab Emirates together represented a notable percentage of global Construction ERP market revenue in 2025, with mega-projects that favor platforms embedding Arabic language packs and multicurrency ledgers. South America and Africa remain early-stage, but localized vendors such as EVOP and SYNEco are carving niches with e-invoicing connectors to regional tax portals.

- Procore Technologies, Inc.

- Trimble Inc. (Viewpoint Division)

- CMiC Global Inc.

- Sage Group plc

- Jonas Construction Software Inc.

- Foundation Software, LLC

- Buildertrend Solutions, Inc.

- RedTeam Software, LLC

- Penta Technologies, Inc.

- Deltek, Inc.

- B2W Software, Inc.

- Explorer Software Group

- Eque2 Limited

- e-Builder, Inc.

- Projectmates (Systemates, Inc.)

- RIB Software GmbH

- UDA Technologies, Inc.

- Premier Construction Software

- COINS Global Limited

- Acumatica, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Adoption of Cloud-Based ERP Solutions

- 4.2.2 Increasing Government Infrastructure Spending on Construction

- 4.2.3 Rising Demand for Mobile-First and Remote Collaboration Capabilities

- 4.2.4 Stricter Regulatory Compliance for Construction Accounting and Reporting

- 4.2.5 Emergence of AI-Powered Predictive Modules Reducing Rework

- 4.2.6 Integration of BIM Digital Twin Data with ERP Workflows

- 4.3 Market Restraints

- 4.3.1 High Upfront Implementation and Customization Costs

- 4.3.2 Cybersecurity and Data-Privacy Concerns

- 4.3.3 Legacy Data Migration Complexity

- 4.3.4 Shortage of Skilled Construction-Specific ERP Talent

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Buyers

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Mode

- 5.1.1 Cloud-Based

- 5.1.2 On-Premise

- 5.1.3 Hybrid

- 5.2 By Enterprise Size

- 5.2.1 Small and Medium Enterprises

- 5.2.2 Large Enterprises

- 5.3 By Solution

- 5.3.1 Software

- 5.3.2 Services

- 5.4 By End Use

- 5.4.1 Residential Construction

- 5.4.2 Commercial Construction

- 5.4.3 Infrastructure and Civil Engineering

- 5.4.4 Industrial Construction

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 ASEAN

- 5.5.4.6 Australia and New Zealand

- 5.5.4.7 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Procore Technologies, Inc.

- 6.4.2 Trimble Inc. (Viewpoint Division)

- 6.4.3 CMiC Global Inc.

- 6.4.4 Sage Group plc

- 6.4.5 Jonas Construction Software Inc.

- 6.4.6 Foundation Software, LLC

- 6.4.7 Buildertrend Solutions, Inc.

- 6.4.8 RedTeam Software, LLC

- 6.4.9 Penta Technologies, Inc.

- 6.4.10 Deltek, Inc.

- 6.4.11 B2W Software, Inc.

- 6.4.12 Explorer Software Group

- 6.4.13 Eque2 Limited

- 6.4.14 e-Builder, Inc.

- 6.4.15 Projectmates (Systemates, Inc.)

- 6.4.16 RIB Software GmbH

- 6.4.17 UDA Technologies, Inc.

- 6.4.18 Premier Construction Software

- 6.4.19 COINS Global Limited

- 6.4.20 Acumatica, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment