|

시장보고서

상품코드

2065621

중동 및 아프리카의 실내 농업 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Middle East And Africa Indoor Farming - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

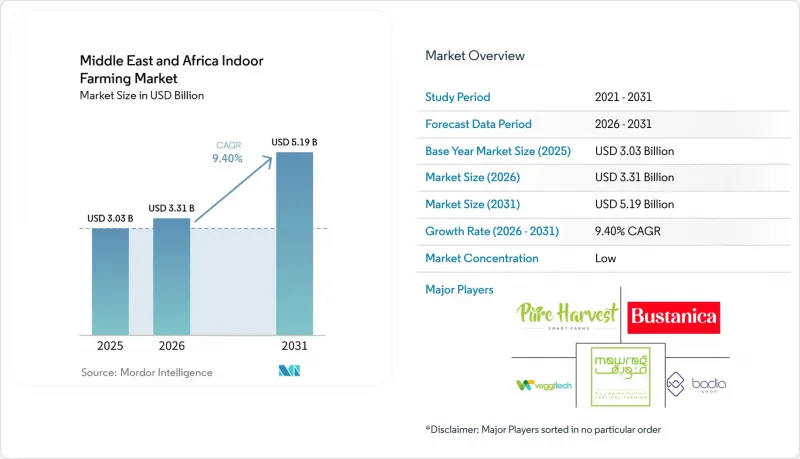

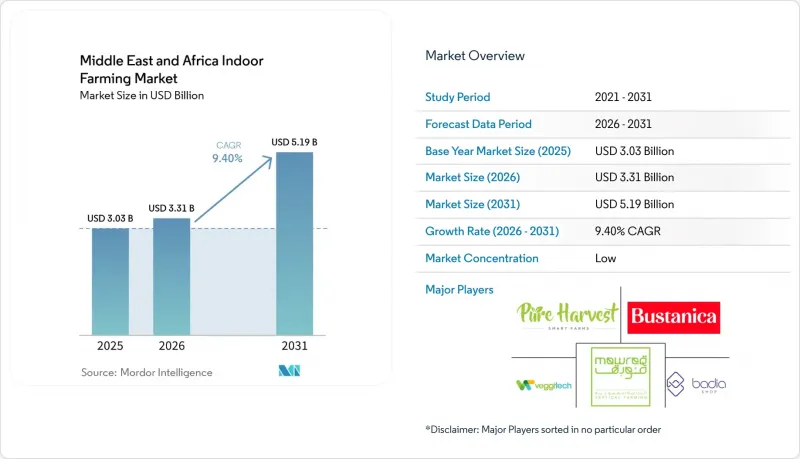

Mordor Intelligence에 의하면, 중동 및 아프리카의 실내 농업 시장 규모는 2025년 30억 3,000만 달러로 평가되었고, 2026년 33억 1,000만 달러로 추정되고, 2031년까지 51억 9,000만 달러로 확대할 전망이며, 2026-2031년 연평균 복합 성장률(CAGR)은 9.40%를 나타낼 전망입니다.

본 보고서는 시설 유형별(온실, 실내 수직 농업, 컨테이너 농업 등), 재배 시스템별(수경 재배, 에어로포닉스 등), 구성 요소별(하드웨어, 소프트웨어, 서비스), 작물 유형별(과일, 채소, 허브, 꽃 및 관상용 식물 등), 지역별(중동 및 아프리카)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

중동 및 아프리카의 실내 농업 시장 동향 및 인사이트

물 부족 및 경작지 제약

물 부족은 중동 및 아프리카의 실내 농업 시장을 크게 견인하고 있습니다. 경작 가능한 토지가 제한적이고 담수 자원도 부족한 이 지역에서는 자원 효율이 높은 식량 생산 시스템으로의 전환이 가속화되고 있습니다. 이러한 변화로 인해, 특히 걸프 연안 국가들을 중심으로 수경 재배 및 제어 환경 농업에 대한 투자가 촉진되고 있습니다. ‘태양광 발전식 RO 수경 재배 네트 하우스’에서 다룬 2025년 연구에서는 그 경제적 이점이 밝혀졌습니다. 수경 재배 방식의 토마토 재배용 태양광 발전식 역삼투(RO) 시스템은 관개용수를 1.05달러/m³의 비용으로 생산했습니다. 이에 반해, 기존 공공 상수도 공급 가격은 1m³당 2.52-3.20달러 수준이었으며, 이를 통해 물 비용을 58-68% 절감할 수 있었습니다. 이러한 경제적 및 자원적 효율성이 실내 농업의 도입을 촉진하고 있으며, 해당 지역의 식량 안보와 농업의 지속가능성을 강화하고 있습니다.

식량 안보 및 수입 대체 프로그램

식량 안보 및 수입 대체 프로그램은 중동 및 아프리카의 실내 농업 시장에서 중요한 성장 요인으로 부상하고 있습니다. 각국 정부는 식량 수입 의존도를 낮추기 위해 국내 농업 생산에 점점 더 주력하고 있습니다. 환경 제어형 농업, 온실 확충, 그리고 지역 밀착형 공급망 구축을 촉진하는 정책 덕분에 지역 전체에서 첨단 농업 기술에 대한 투자가 활성화되고 있습니다. 이러한 추세는 특히 아랍에미리트(UAE)에서 두드러지는데, 해당 국가의 ‘2051년 국가 식량 안보 전략’에서는 장기적인 식량 회복탄력성을 강화하기 위한 중요한 우선 과제로 지속 가능한 국내 식량 생산과 현대적인 농업 기술이 강조되고 있습니다. 이러한 정책적 노력을 통해 지역 전체적으로 실내 농업 프로젝트에 대한 자금 조달, 인프라 구축 및 상업적 신뢰도가 향상되고 있습니다.

높은 자본 집약도와 투자 회수 위험

막대한 초기 투자 비용은 중동 및 아프리카의 실내 농업 시장에 여전히 큰 과제로 남아 있습니다. 특히, 프로젝트 자금 확보가 더 어려운 해안 지역 이외의 지역에서는 이러한 경향이 두드러집니다. 실내 농업에서는 안정적인 수익을 창출하기 전에 온실 시설, 밀폐형 재배 시스템, 조명, 냉각, 관개, 자동화, 수확 후 처리 등에 막대한 초기 투자가 필요합니다. 이러한 재정적 부담은 정부의 지원을 받는 프로젝트가 많은 걸프 연안 국가들에서는 비교적 관리하기 쉬운 반면, 대출 접근성이 제한적이고 장기 공급 계약도 널리 보급되지 않은 많은 아프리카 시장과 비교하면 상황이 다릅니다. 문제는 초기 투자 규모뿐만 아니라, 조명 효율과 제어 소프트웨어의 발전으로 인해 현재 설비가 수년 내에 구식이 될 위험에도 있습니다. 모듈식 업그레이드 옵션을 갖추지 않은 고정식 시설을 건설하는 사업자는 더 첨단 시스템과 낮은 운영 비용을 갖춘 새로운 농장에 뒤처질 위험이 있습니다. 그 결과, 많은 개발업체들은 대규모 밀폐형 농장 설계보다는 단계적 확장, 소규모 진출 모델, 혹은 하이브리드 방식을 우선시하고 있습니다.

부문별 분석

2025년, 중동 및 아프리카의 실내 농업 시장에서 온실 부문의 점유율은 70.8%로 가장 높은 비중을 차지했습니다. 이는 해당 지역에서 생산 관리 측면에서 완전 밀폐형 수직 농장보다 운영상의 복잡성을 줄이면서도 균형을 잘 잡은 확장성이 뛰어난 보호 재배 시스템이 선호되고 있음을 반영합니다. 온실 도입은 특히 걸프 연안 국가들에서 두드러지게 나타나고 있으며, 고온과 물 부족이 기후 조절 재배에 대한 투자를 촉진하고 있습니다. 아랍에미리트(UAE)와 사우디아라비아에서는 상업용 수경재배 온실 운영업체들이 식량 안보 전략을 지원하고 연중 채소 공급을 확보하기 위해 생산 능력을 확대되고 있습니다. 또한, 대규모 온실 시스템은 더 넓은 재배 면적을 수용할 수 있고 단위당 인프라 비용이 낮기 때문에 주곡 생산에 있어 상업적으로 실현 가능성이 더 높다고 할 수 있습니다.

중동 및 아프리카의 컨테이너형 실내 농업 시장 규모는 도시 지역의 소비 거점 인근에서 운영 가능한 모듈식 실내 농업 시스템에 대한 수요 증가에 힘입어, 2026-2031년 연평균 성장률(CAGR) 12.8%라는 가장 높은 성장률을 기록하며 확대될 것으로 전망됩니다. 컨테이너형 농장의 유연성은 이용 가능한 토지가 제한된 시장, 자본 예산이 제한된 시장, 혹은 시범 규모로 확장할 계획이 있는 시장에서 그 매력을 더욱 높여주고 있습니다. 또한, 이러한 시스템은 대규모 온실이나 수직 농업 시설에 비해 더 신속하게 도입할 수 있습니다. 만안 국가들에서는 실내 수직 농업 방식이 주목을 받고 있지만, 그 확대는 주로 소매업체나 기관과 견고한 제휴 관계를 맺고 있으며 자금력이 풍부한 사업자를 중심으로 진행되고 있습니다. 심수 문화(DWC) 시스템과 같은 특수한 시설 형태는 계속해서 고급 농산물 시장, 연구용 재배 및 통제된 시범 용도로 활용되고 있습니다.

2025년에는 수경 재배가 59.8%라는 가장 높은 점유율을 차지했으며, 해당 지역의 환경 제어형 농업 사업에서 주요 재배 시스템으로서의 위상을 유지했습니다. 이 시스템은 예측 가능한 영양분 공급, 안정적인 작물 품질, 그리고 기존 토양 재배에 비해 물 소비량을 줄일 수 있다는 점 때문에 계속해서 널리 채택되고 있습니다. 수경 재배 시스템은 물 부족이나 극심한 기후 조건으로 인해 상업적 식량 생산에 있어 정밀한 관개가 필수적인 걸프 연안 국가들에서 특히 중요한 역할을 하고 있습니다. 이 기술은 사막 기후나 상업용 온실 환경에서 확실한 운영 실적을 보여주고 있기 때문에 생산자들은 토마토, 오이, 피망, 허브, 잎채소 등의 작물 재배에 있어 계속해서 수경재배에 의존하고 있습니다.

에어로포닉스는 고급 작물의 고효율 재배 시스템 및 도시 지역 식량 공급 용도에 대한 관심이 높아지는 것을 배경으로, 2026-2031년 15.6%라는 가장 높은 연평균 성장률(CAGR)을 기록하며 성장할 것으로 전망됩니다. 에어로포닉스 시스템은 미세한 영양분 미스트를 공급하는 방식을 채택하여, 물 사용량을 대폭 줄이는 동시에 작물의 재배 주기를 단축하고 고밀도 생산을 가능하게 합니다. 이 기술은 잎채소, 허브, 마이크로그린, 특산품, 특히 소매, 호텔 및 레스토랑, 외식 산업에 대한 공급 분야에서 그 중요성이 커지고 있습니다. 또한, 아쿠아포닉스나 하이브리드 재배 시스템도 지속 가능한 식량 생산에 초점을 맞춘 특정 프로젝트에서 주목을 받고 있지만, 대부분의 지역 시장에서 그 상업적 도입률은 수경 재배 시스템보다 여전히 낮은 상황입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

LSH 26.06.24According to Mordor Intelligence, the middle east and Africa Indoor Farming Market size is projected to expand from USD 3.03 billion in 2025 and USD 3.31 billion in 2026 to USD 5.19 billion by 2031, registering a CAGR of 9.40% between 2026 and 2031.

This report is Segmented by Facility Type (Greenhouses, Indoor Vertical Farms, Container Farms, and More), by Growing System (Hydroponics, Aeroponics, and More), by Component (Hardware, Software, and Services), by Crop Type (Fruits, Vegetables, and Herbs, Flowers and Ornamentals, and More), and by Geography (Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Middle East And Africa Indoor Farming Market Trends and Insights

Water Scarcity and Arable-Land Constraints

Water scarcity significantly drives the indoor farming market in the Middle East and Africa. With limited arable land and minimal freshwater resources, the region increasingly turns to resource-efficient food production systems. This shift has spurred investments in hydroponics and controlled-environment agriculture, particularly in Gulf economies. A 2025 study highlighted in "Solar-Powered RO-Hydroponic Net House" showcased the economic benefits: a solar-powered reverse osmosis system for hydroponic tomato farming generated irrigation-grade water at USD 1.05/m3. In contrast, conventional utility supplies ranged from USD 2.52 to 3.20/m3, marking a 58-68% reduction in water costs. Such economic and resource efficiencies are propelling the adoption of indoor farming, bolstering food security and agricultural sustainability in the region.

Food-Security and Import-Substitution Programs

Food security and import substitution programs are emerging as significant growth drivers for the indoor farming market in the Middle East and Africa. Governments are increasingly focusing on domestic agricultural production to reduce dependence on food imports. Policies promoting controlled-environment agriculture, greenhouse expansion, and localized supply chains are fostering investments in advanced farming technologies across the region. This trend is particularly evident in the United Arab Emirates (UAE), where the National Food Security Strategy 2051 emphasizes sustainable domestic food production and modern agricultural technologies as critical priorities for enhancing long-term food resilience. Such policy initiatives are improving access to financing, infrastructure development, and commercial confidence in indoor farming projects throughout the region.

High Capital Intensity and Payback Risk

High initial investment continues to be a significant challenge for the indoor farming market in the Middle East and Africa, particularly outside the Gulf region, where securing project financing is more difficult. Indoor farming requires substantial upfront expenditures for greenhouse structures, enclosed growing systems, lighting, cooling, irrigation, automation, and post-harvest handling before generating consistent revenue. This financial burden is more manageable in Gulf countries with sovereign-backed projects compared to many African markets, where access to credit is limited, and long-term supply contracts are less prevalent. The challenge is not only the scale of the initial investment but also the risk that current equipment may become outdated within a few years due to advancements in lighting efficiency and control software. Operators who construct rigid facilities without modular upgrade options risk falling behind newer farms equipped with more advanced systems and lower operating costs. As a result, many developers prioritize phased rollouts, smaller-scale entry models, or hybrid formats over large-scale enclosed farm designs.

Other drivers and restraints analyzed in the detailed report include:

- Demand for Local Fresh Pesticide-Residue-Free Produce

- AI, IoT, LED, and Automation Gains

- Cooling-Energy Intensity and Grid-Cost Exposure

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The Middle East and Africa indoor farming market share for the greenhouse segment accounted for the largest 70.8% in 2025, reflecting the region's preference for scalable protected cultivation systems that balance production control with lower operating complexity than fully enclosed vertical farms. Greenhouse adoption is particularly strong in Gulf countries, where high temperatures and water scarcity drive investments in climate-controlled cultivation. In the United Arab Emirates and Saudi Arabia, commercial hydroponic greenhouse operators are expanding production capacity to support food security strategies and ensure a year-round vegetable supply. Additionally, large greenhouse systems are more commercially viable for staple crop production due to their ability to support larger cultivation areas and lower per-unit infrastructure costs.

The Middle East and Africa indoor farming market size for container farms is projected to grow at the fastest CAGR of 12.8% from 2026 to 2031, supported by rising demand for modular indoor farming systems that can operate close to urban consumption centers. The flexibility of container farms makes them appealing in markets with limited land availability, smaller capital budgets, or pilot-scale expansion plans. These systems also enable faster deployment compared to large greenhouse or vertical farming facilities. While indoor vertical farms are gaining attention in Gulf countries, their expansion is primarily concentrated among well-funded operators with strong retail or institutional partnerships. Specialty facility formats, such as Deep Water Culture (DWC) systems, continue to serve premium produce markets, research cultivation, and controlled pilot applications.

Hydroponics accounted for the largest share of 59.8% in 2025, maintaining its position as the leading growing system in controlled-environment agriculture operations within the region. This system remains widely adopted due to its ability to ensure predictable nutrient delivery, consistent crop quality, and reduced water consumption compared to traditional soil-based cultivation. Hydroponic systems are particularly significant in Gulf countries, where water scarcity and extreme climate conditions necessitate precision irrigation for commercial food production. Growers continue to rely on hydroponics for crops such as tomatoes, cucumbers, peppers, herbs, and leafy greens, as the technology has demonstrated a strong operational track record in desert climates and commercial greenhouse environments.

Aeroponics is projected to grow at the highest CAGR of 15.6% from 2026 to 2031, driven by increasing interest in high-efficiency cultivation systems for premium crops and urban food supply applications. Aeroponic systems utilize fine nutrient mist delivery methods, which significantly reduce water usage while enabling rapid crop cycles and high-density production. This technology is gaining relevance for leafy greens, herbs, microgreens, and specialty produce, particularly for supply to retail, hospitality, and foodservice sectors. Additionally, aquaponics and hybrid growing systems are attracting attention in specific projects focused on sustainable food production, although their commercial adoption remains lower than hydroponic systems across most regional markets.

List of Companies Covered in this Report:

- Pure Harvest Smart Farms Ltd.

- Emirates Bustanica LLC (Emirates Flight Catering Co. LLC)

- VeggiTech Hydroponic Technologies Private Limited (SNASCO Holding Company)

- Mowreq Specialized Agriculture Company

- Badia Al Sahra Agricultural L.L.C.

- AeroFarms, LLC

- Crop One Holdings, Inc.

- Netafim Ltd. (Orbia Advance Corporation, S.A.B. de C.V.)

- Richel Group SAS

- Signify Holding B.V. (Signify N.V.)

- Argus Control Systems Limited (Conviron Group)

- Certhon Build B.V. (DENSO Corporation)

- KUBO Tuinbouwprojecten B.V.

- Priva Holding B.V.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Water scarcity and arable-land constraints

- 4.2.2 Food-security and import-substitution programs

- 4.2.3 Demand for local fresh pesticide-residue-free produce

- 4.2.4 AI, IoT, LED, and automation gains

- 4.2.5 Sovereign-wealth-backed agritech expansion

- 4.2.6 Utility-tariff support and arid-climate research localization

- 4.3 Market Restraints

- 4.3.1 High capital intensity and payback risk

- 4.3.2 Controlled-environment agronomy talent gaps

- 4.3.3 Cooling-energy intensity and grid-cost exposure

- 4.3.4 Imported inputs and non-harmonized CEA regulations

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Bargaining Power of Buyers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Facility Type

- 5.1.1 Greenhouses

- 5.1.2 Indoor Vertical Farms

- 5.1.3 Container Farms

- 5.1.4 Indoor Deep Water Culture Systems

- 5.1.5 Other Facility Types

- 5.2 By Growing System

- 5.2.1 Hydroponics

- 5.2.2 Aeroponics

- 5.2.3 Aquaponics

- 5.2.4 Soil-based

- 5.2.5 Hybrid

- 5.3 By Component

- 5.3.1 Hardware

- 5.3.2 Software

- 5.3.3 Services

- 5.4 By Crop Type

- 5.4.1 Fruits, Vegetables, and Herbs

- 5.4.2 Flowers and Ornamentals

- 5.4.3 Microgreens and Specialty Crops

- 5.5 By Geography

- 5.5.1 Middle East

- 5.5.1.1 Saudi Arabia

- 5.5.1.2 United Arab Emirates

- 5.5.1.3 Israel

- 5.5.1.4 Rest of Middle East

- 5.5.2 Africa

- 5.5.2.1 South Africa

- 5.5.2.2 Egypt

- 5.5.2.3 Kenya

- 5.5.2.4 Rest of Africa

- 5.5.1 Middle East

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Business Segments, Financials as Available, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments)

- 6.4.1 Pure Harvest Smart Farms Ltd.

- 6.4.2 Emirates Bustanica LLC (Emirates Flight Catering Co. LLC)

- 6.4.3 VeggiTech Hydroponic Technologies Private Limited (SNASCO Holding Company)

- 6.4.4 Mowreq Specialized Agriculture Company

- 6.4.5 Badia Al Sahra Agricultural L.L.C.

- 6.4.6 AeroFarms, LLC

- 6.4.7 Crop One Holdings, Inc.

- 6.4.8 Netafim Ltd. (Orbia Advance Corporation, S.A.B. de C.V.)

- 6.4.9 Richel Group SAS

- 6.4.10 Signify Holding B.V. (Signify N.V.)

- 6.4.11 Argus Control Systems Limited (Conviron Group)

- 6.4.12 Certhon Build B.V. (DENSO Corporation)

- 6.4.13 KUBO Tuinbouwprojecten B.V.

- 6.4.14 Priva Holding B.V.