|

시장보고서

상품코드

2073227

남미의 실내 농업 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)South America Indoor Farming - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

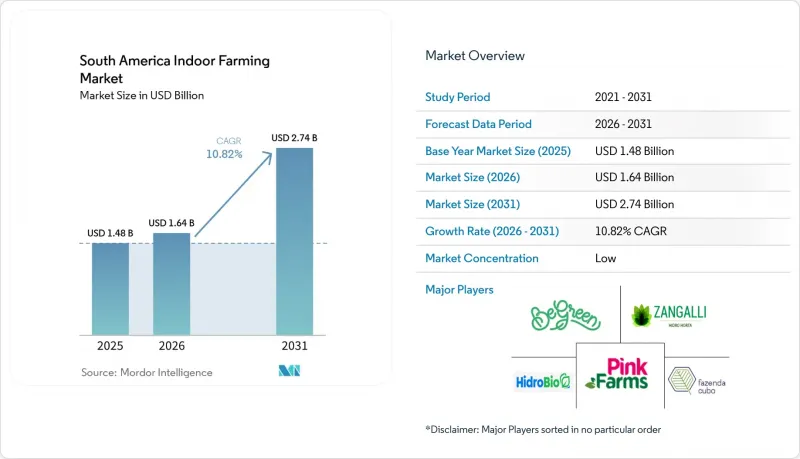

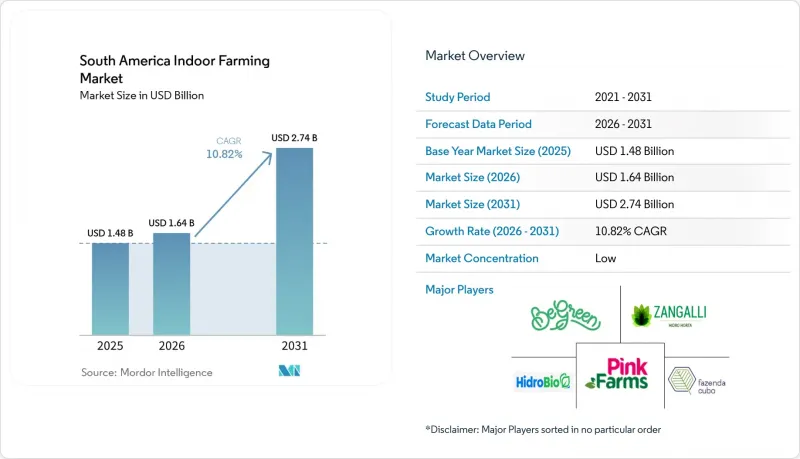

Mordor Intelligence에 의하면, 남미의 실내 농업 시장 규모는 2025년 14억 8,000만 달러로 평가되었습니다. 2026년 16억 4,000만 달러에서 2031년까지 27억 4,000만 달러로 확대되며 2026년부터 2031년까지 연평균 복합 성장률(CAGR)은 10.82%를 나타낼 전망입니다.

본 보고서는 재배 시스템별(에어로포닉스, 하이드로포닉스, 아쿠아포닉스 등), 시설 유형별(유리 또는 폴리카보네이트 온실, 실내 수직 농장, 컨테이너 농장 등), 작물 유형별(과일 및 채소, 허브·마이크로그린 등), 국가별(브라질, 아르헨티나, 칠레 등)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

남미의 실내 농업 시장 동향 및 인사이트

도시 지역의 신선식품에 대한 수요 증가

도시화로 인해 남미의 실내 농업 시장에서 신선식품을 구매하는 방식에 변화가 일어나고 있습니다. 2024년에 발표된 브라질 인구 조사에 따르면, 도시화율은 87.4%에 달하며, 인구의 매우 큰 비중이 계절적 가용성보다는 품질, 유통기한, 구매 빈도가 더 중요시되는 대도시권 공급권 내에 거주하고 있습니다. 라틴아메리카 및 카리브해 지역 전체에서도 유사한 경향이 나타나며, 인구의 81%가 도시 지역에 거주하고 있어 식량 불안에 대한 우려와 상업적 조달 결정 간의 거리가 좁혀졌습니다. 2026년 3월 브라질의 소매 데이터 역시 월간 매출액이 사상 최고치를 기록했음을 보여주고 있으며, 식품 부문은 소매 업계 전체를 웃도는 성장세를 보였습니다. 이는 정규 유통 경로를 통해 판매되는 신선식품에 대한 도시 지역 수요가 지속되고 있음을 시사합니다. 이는 남미의 실내 농업 시장에 있어 중요한 의미를 지닙니다. 왜냐하면 도시 지역의 슈퍼마켓이나 외식업계의 구매 담당자들은 연중 안정적인 공급량, 일관된 품질 기준, 그리고 추적 가능성을 필요로 하지만, 이러한 요건들은 노지 재배를 통한 공급으로는 반드시 보장될 수 없기 때문입니다. 가장 큰 수요는 더 이상 상파울루, 산티아고, 보고타에만 국한되지 않습니다. 쿠리치바, 헤시피, 메데인, 리마 노르테와 같은 지방 도시에서도 정식 소매망이 확대되고 있기 때문입니다. 이러한 도시권의 확대로 인해 실내 농업 사업자들은 소수의 주요 대도시에만 의존하는 것이 아니라, 수요의 중심지 근처에서 비즈니스 모델을 전개할 여지가 넓어지고 있습니다.

기후 변화의 심화가 보호재배 도입을 촉진

기후 변동성으로 인해 남미의 실내 농업 시장에서는 점점 더 많은 생산자와 투자자들이 보호 재배로 전환하고 있습니다. 2025년 3월에 발표된 국제통화기금(IMF)의 워킹페이퍼는 남미의 기상 스트레스를 반복되는 가뭄과 연관 지어, 엘니뇨 현상에 의해 증폭된 패턴 하에서는 브라질에서 연간 2회의 가뭄이 발생하고 있다고 기록했습니다. 2024년 12월에 발표된 브라질의 공식 작물 조사에 따르면, 해당 국가의 수확량은 전년 대비 크게 감소했으며, 이는 노지 재배에 수반되는 생산 위험을 뒷받침하는 것이었습니다. 또한 2025년에는 식량 물가 상승세도 가속화되어, 기상적 압박이 농장 차원에 그치지 않고 소비자와 소매업체로도 파급되고 있음이 밝혀졌습니다. 칠레에 위치한 AgroUrbana사의 키리쿠라 수직 농장은 실용적인 사례로 꼽히고 있습니다. 이 농장에서는 노지 재배에 비해 물 사용량을 95% 줄이면서도 연간 52회의 재배 주기를 달성하고 있으며, 통제된 환경 하에서는 생산량을 강우량 변동과 무관하게 유지할 수 있음을 입증하고 있습니다. 이러한 변화로 인해 농업 리스크의 가격 책정 방식도 점차 바뀌고 있습니다. 실내 시설은 식품 공급망에서 회복탄력성 인프라로서 그 중요성이 점점 더 부각되고 있기 때문입니다. 이러한 재분류로 인해 남미의 실내 농업 시장에 대한 자본 투자의 정당성이 더욱 높아졌으며, 특히 명확한 판로와 강력한 기술 관리 능력을 갖춘 사업자에게는 그 이점이 두드러집니다.

높은 자본 및 에너지 요구 사항

여전히 높은 초기 비용이 남미의 실내 농업 시장 전반에 걸친 보급 확대에 있어 가장 뚜렷한 장벽으로 작용하고 있습니다. Pink Farms의 공개 자료에 따르면, 2025년 운영비 중 에너지 비용이 40%를 차지했으며, 이 점만 보더라도 유리한 전력 공급 조건을 확보하지 못하는 한 많은 시설이 시범 규모를 넘어서는 확장에 어려움을 겪고 있는 이유를 설명할 수 있습니다. 차입 비용이 높고 장기 프로젝트 파이낸싱이 제한적인 시장에서는 자본 부담이 더욱 커집니다. 이로 인해 콜롬비아 내륙, 브라질 북부, 페루 일부 등 식량 불안이 심각함에도 불구하고 상업 자금 조달이 어려운 지역에서는 사업 확장 속도가 둔화되고 있습니다. 아르헨티나에서는 통화 약세 국면을 거치면서 수입되는 기후 제어 시스템과 조명의 비용이 대폭 상승함에 따라, 이와 유사한 문제가 더욱 심각한 형태로 발생하고 있습니다. 소규모 사업자는 온실 모델로 시장에 진입할 수 있지만, 고밀도 실내 수직 농장이 수익성을 확보할 수 있는 비용 수준에 도달하기 위해서는 여전히 막대한 투자가 필요합니다. 그 결과, 남미의 실내 농업 시장은 현지 생산을 통해 공급 격차를 가장 크게 해소할 수 있는 지역보다 부유한 도시 지역에서 더 빠르게 성장하고 있습니다.

부문별 분석

2025년, 남미의 실내 농업 시장에서 수경 재배는 48.2%의 점유율을 차지했으며, 상업용 온실 운영자들이 표준화된 영양분 공급, 더 짧은 재배 주기, 효율적인 물 관리 시스템을 선호함에 따라 그 주도적 지위를 유지했습니다. 한편, 토양을 이용한 실내 재배는 기술적 복잡성을 줄여주어, 유기농 재배와의 호환성을 추구하는 과도기 단계에 있는 온실 농가들 사이에서 지지를 얻었습니다. 그 결과, 제어 환경 하의 농업(CEF)에서 생산되는 잎채소, 허브 및 고급 원예 작물의 경우, 수경 재배 시스템이 상업적으로 여전히 주류를 차지하고 있습니다.

에어로포닉스는 2031년까지 연평균 성장률(CAGR) 15.1%로 성장할 것으로 추정되며, 남미의 실내 농업 시장에서 가장 빠르게 성장하고 있는 시스템입니다. 이러한 성장은 물 이용 효율, 정밀한 영양분 관리, 그리고 기후 변화에 강한 생산 시스템의 중요성이 점점 더 커지고 있는 데 기인합니다. 2026년 파라나주가 수경재배 인증 제도를 도입하고, 엠브라파(Embrapa)가 폐쇄형 에어로포닉스 재배에 관한 조사를 추진한 이래, 첨단 실내 재배 기술에 대한 상업적 신뢰는 꾸준히 높아지고 있습니다. 또한, 수경 재배의 안정성과 에어로포닉스 재배의 효율성을 결합한 하이브리드 재배 시스템은 해당 지역 전체에서 고부가가치 작물 생산을 위한 투자를 점점 더 많이 유치하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTHAccording to Mordor Intelligence, the south america indoor farming market size is projected to grow from USD 1.48 billion in 2025 and USD 1.64 billion in 2026 to USD 2.74 billion by 2031, registering a CAGR of 10.82% between 2026 and 2031.

This report is Segmented by Growing System (Aeroponics, Hydroponics, Aquaponics, and More), by Facility Type (Glass or Poly Greenhouses, Indoor Vertical Farms, Container Farms, and More), by Crop Type (Fruits and Vegetables, Herbs and Microgreens, and More), and by Country ( Brazil, Argentina, Chile, and More). The Market Forecasts are Provided in Terms of Value (USD).

South America Indoor Farming Market Trends and Insights

Rising Urban Demand for Fresh Produce

Urbanization is changing how fresh food is bought across the South America indoor farming market. Brazil's Census, published in 2024, showed an urbanization rate of 87.4%, which placed a very large share of the population inside metro supply zones where quality, shelf life, and frequency matter more than seasonal availability. The same broad pattern is visible across Latin America and the Caribbean, where 81% of people were urban, which narrowed the distance between food insecurity concerns and commercial sourcing decisions. March 2026 retail data in Brazil also showed record monthly sales, with the food segment outperforming broader retail activity, which signaled sustained urban demand for fresh products sold through formal channels. This matters for the South American indoor farming market because urban supermarkets and food-service buyers need year-round volumes, stable specifications, and traceability that open-field supply does not always provide. The strongest demand is no longer limited to Sao Paulo, Santiago, and Bogota, because secondary cities such as Curitiba, Recife, Medellin, and Lima Norte are also expanding their formal retail footprint. That widening urban map gives indoor operators more room to replicate their model near demand centers instead of depending only on a few primary metros.

Climate Volatility Increasing Protected Cultivation Adoption

Climate instability is pushing more growers and investors toward protected production in the South America indoor farming market. An International Monetary Fund working paper published in March 2025 linked South America's weather stress to recurring droughts, and it recorded Brazil at 2 drought events per year under an El Nino-amplified pattern. Brazil's official crop survey released in December 2024 showed that the country's harvest declined significantly year over year, which reinforced the production risk attached to open-field farming. Food inflation also increased in 2025, which showed that weather pressure was reaching consumers and retailers rather than staying only at the farm level. AgroUrbana's Quilicura vertical farm in Chile offers a practical counterpoint, because it reported 52 crop cycles per year with 95% less water than field farming, proving that controlled environments can separate output from rainfall volatility. This shift is changing how agricultural risk is priced, since indoor assets are increasingly treated as resilience infrastructure inside food supply chains. That reclassification improves the case for capital deployment in the South America indoor farming market, especially for operators with clear offtake and strong technical control.

High Capital and Energy Requirements

High upfront cost is still the clearest barrier to wider deployment across the South America indoor farming market. Pink Farms' disclosures showed that energy represented 40% of operating expenditure in 2025, and this alone explains why many facilities struggle to scale beyond pilot size without access to favorable power terms. The capital burden is even harder in markets where debt remains expensive and long-tenor project finance is limited. This slows expansion in places where food insecurity is strong but commercial funding is weak, including inland Colombia, northern Brazil, and parts of Peru. Argentina faces a sharper version of the same issue because imported climate systems and lighting become far more expensive after currency depreciation cycles. Smaller operators can enter with greenhouse models, but dense indoor vertical farms still need large investment before they reach a viable cost base. The result is that the South America indoor farming market grows faster in wealthier urban corridors than in the places where local production could solve the biggest supply gaps.

Other drivers and restraints analyzed in the detailed report include:

- Expanding Greenhouse and Hydroponic Investments

- Improving Light Emitting Diode and Automation Cost Economics

- Limited Controlled-Environment Agronomy Expertise

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hydroponics accounted for 48.2% of the South America indoor farming market share in 2025, maintaining its leading position due to the preference of commercial greenhouse operators for standardized nutrient delivery, faster crop cycles, and efficient water management systems. At the same time, soil-based indoor cultivation gained traction among transitional greenhouse farms seeking lower technological complexity and compatibility with organic cultivation. As a result, hydroponic systems remained commercially dominant for leafy vegetables, herbs, and premium horticultural crops produced within controlled-environment farming operations.

Aeroponics is estimated to grow at a 15.1% CAGR through 2031, making it the fastest-growing system in the South America indoor farming market. This growth is driven by increasing prioritization of water efficiency, precision nutrient management, and climate-resilient production systems. Since Parana introduced hydroponic certification pathways in 2026 and Embrapa advanced research on closed-loop aeroponic cultivation, commercial confidence in advanced indoor growing technologies has steadily increased. Additionally, hybrid cultivation systems that combine hydroponic stability with aeroponic efficiency are attracting growing investment for high-value crop production across the region.

Complete Report Scope:

- By Growing System

- Hydroponics

- Aeroponics

- Aquaponics

- Soil-based

- Hybrid

- By Facility Type

- Glass or Poly Greenhouses

- Indoor Vertical Farms

- Container Farms

- Indoor Deep-Water Culture Systems

- Other Facility Type

- By Crop Type

- Fruits and Vegetables

- Leafy Greens

- Tomato

- Cucumber

- Bell Pepper and Chili Pepper

- Strawberry

- Other Fruits and Vegetables

- Herbs and Microgreens

- Basil

- Mint

- Parsley and Cilantro

- Other Herbs and Microgreens

- Flowers and Ornamentals

- Cut Flowers

- Potted Ornamentals

- Others

- Fruits and Vegetables

- By Country

- Brazil

- Argentina

- Chile

- Colombia

- Peru

- Rest of South America

List of Companies Covered in this Report:

- Pink Farms

- BeGreen Fazendas Urbanas

- AgroUrbana

- HidroBio S.A.

- Raiz Vertical Farms Inc.

- Aguap Fazenda Urbana

- Cubo Farm

- Hidrohorta Zangalli

- Colheita Urbana

- VerdeVida

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising urban demand for fresh produce

- 4.2.2 Climate volatility increasing protected cultivation adoption

- 4.2.3 Expanding greenhouse and hydroponic investments

- 4.2.4 Improving LED and automation cost economics

- 4.2.5 Growing modern retail and foodservice expansion

- 4.2.6 Adoption of tropicalized hybrid seed varieties

- 4.3 Market Restraints

- 4.3.1 High capital and energy requirements

- 4.3.2 Limited controlled-environment agronomy expertise

- 4.3.3 Currency volatility affecting imported technologies

- 4.3.4 Inconsistent infrastructure and electricity availability

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Bargaining Power of Buyers

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Growing System

- 5.1.1 Hydroponics

- 5.1.2 Aeroponics

- 5.1.3 Aquaponics

- 5.1.4 Soil-based

- 5.1.5 Hybrid

- 5.2 By Facility Type

- 5.2.1 Glass or Poly Greenhouses

- 5.2.2 Indoor Vertical Farms

- 5.2.3 Container Farms

- 5.2.4 Indoor Deep-Water Culture Systems

- 5.2.5 Other Facility Type

- 5.3 By Crop Type

- 5.3.1 Fruits and Vegetables

- 5.3.1.1 Leafy Greens

- 5.3.1.2 Tomato

- 5.3.1.3 Cucumber

- 5.3.1.4 Bell Pepper and Chili Pepper

- 5.3.1.5 Strawberry

- 5.3.1.6 Other Fruits and Vegetables

- 5.3.2 Herbs and Microgreens

- 5.3.2.1 Basil

- 5.3.2.2 Mint

- 5.3.2.3 Parsley and Cilantro

- 5.3.2.4 Other Herbs and Microgreens

- 5.3.3 Flowers and Ornamentals

- 5.3.3.1 Cut Flowers

- 5.3.3.2 Potted Ornamentals

- 5.3.4 Others

- 5.3.1 Fruits and Vegetables

- 5.4 By Country

- 5.4.1 Brazil

- 5.4.2 Argentina

- 5.4.3 Chile

- 5.4.4 Colombia

- 5.4.5 Peru

- 5.4.6 Rest of South America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Pink Farms

- 6.4.2 BeGreen Fazendas Urbanas

- 6.4.3 AgroUrbana

- 6.4.4 HidroBio S.A.

- 6.4.5 Raiz Vertical Farms Inc.

- 6.4.6 Aguap Fazenda Urbana

- 6.4.7 Cubo Farm

- 6.4.8 Hidrohorta Zangalli

- 6.4.9 Colheita Urbana

- 6.4.10 VerdeVida