|

시장보고서

상품코드

2065752

바이오테크놀러지 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Biotechnology - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

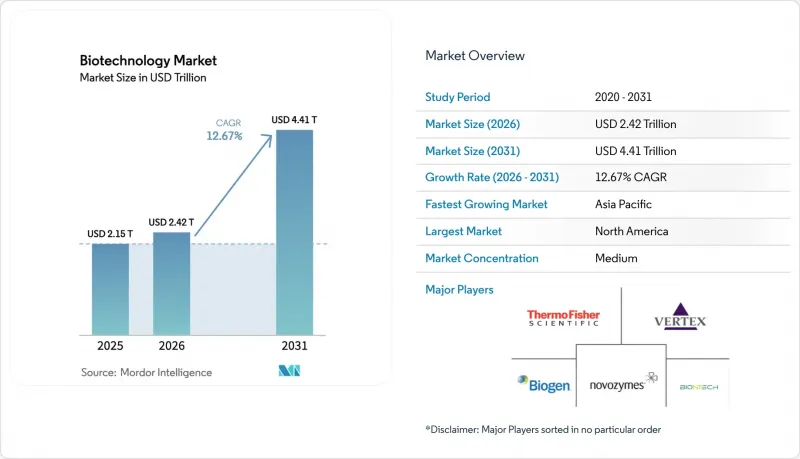

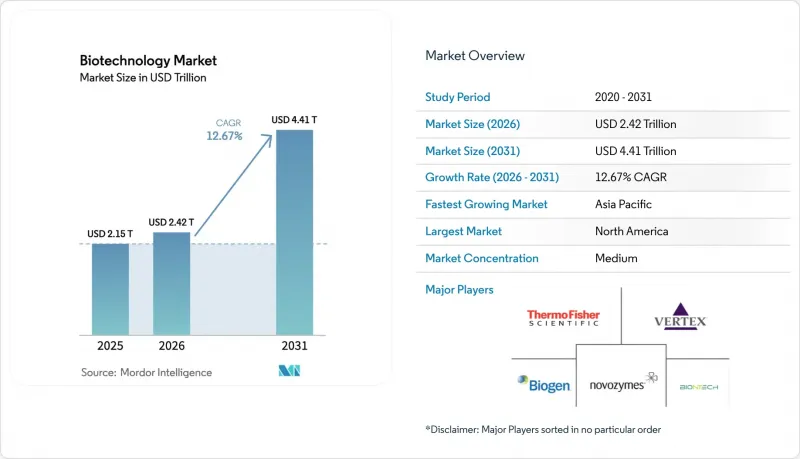

Mordor Intelligence에 의하면, 바이오테크놀러지 시장 규모는 2025년 2조 1,500억 달러로 평가되었고, 2026년 2조 4,200억 달러로 추정되고, 2031년까지 4조 4,100억 달러로 확대할 전망이며, 2026-2031년 연평균 복합 성장률(CAGR)은 12.67%를 나타낼 전망입니다.

본 보고서에서는 업계를 기술별(DNA 시퀀싱, 나노바이오기술 등), 용도별(헬스케어 및 레드바이오기술, 식품 및 농업 등), 최종 사용자별(바이오의약품 및 바이오기술 기업, CMO 및 CRO 등), 제품 유형별(바이오의약품, 바이오프로세스 장비 및 소모품 등), 그리고 지역별로 분류하고 있습니다.

세계의 생명공학 시장 동향 및 인사이트

신규 바이오의약품 및 유전자 치료제에 대한 수요 증가

최근 희귀질환에 대한 ‘퍼스트-인-클래스’ 유전자 치료제가 승인된 것은 유전자 치료가 상용화 단계로 접어들었음을 입증하는 것이며, 이에 따라 각 제약사는 연속 바이오프로세스 처리 능력 확대와 전환 시간 단축 및 오염 위험 저감으로 이어지는 일회용 기술에 대한 투자를 가속화하고 있습니다. 재생의료 제품의 높은 가격 책정: Humacyte사의 SYMVESS 용기는 대당 2만 9,500달러에 판매되고 있으며, 이는 신규 진출기업이나 자본을 유치할 수 있는 경제적 잠재력을 보여줍니다. AI를 활용한 환자 군 분류 도구는 임상시험의 성공률을 높이고 있으며, Genmab사의 에프코리타맙 병용 요법이 난치성 림프종에서 87%의 반응률을 달성한 것이 그 대표적인 사례입니다. 이러한 요인들이 복합적으로 작용하여 생명공학 시장의 매출 규모 상한선을 끌어올렸으며, 파이프라인의 각 단계별 수요 전망이 더욱 명확해지고 있습니다.

고속 시퀀싱 비용의 급격한 하락

시퀀싱 비용의 급격한 하락은 이 분야가 대규모 진단 및 실시간 병원체 감시로 전환되는 기반이 되고 있습니다. 일루미나(Illumina)가 4억 2,500만 달러에 소마로직(SomaLogic)을 인수한 것은 단백질체학 데이터 스트림과 유전체학을 통합하여 멀티오믹스 분석을 수행하겠다는 전략적 의도를 보여줍니다. 머신러닝을 활용한 분류 알고리즘은 현재 암 아형 감지에서 90% 이상의 정확도를 달성하고 있으며, 멀티오믹스 통합을 일상적인 임상 워크플로우로 확대되고 있습니다. 시약 수율 향상과 실험실 자동화를 통해 시료당 비용이 더욱 절감됨에 따라, 학술 연구소 및 중소기업의 활용 기회가 확대되고, 생명공학 시장에서의 혁신 민주화가 진전되고 있습니다.

바이오프로세스용 일회용 시스템 전문가 부족

시설의 급속한 확장이 인력 증가를 앞지르고 있어, 노보노르디스크가 노스캐롤라이나주에서 1,000명의 고용을 확대했음에도 불구하고 일회용 기술 운영 인력이 심각하게 부족합니다. 이러한 기술 격차로 인해 시설 검증 일정이 지연되면서, 제품이 예정대로 출시될 수 있을지 불투명해졌습니다. 그 때문에 기업들은 대학과 제휴하여 맞춤형 교육 과정을 마련하거나 사내 연수 프로그램을 강화할 수밖에 없는 실정입니다. 신흥 시장에서는 교육 인프라가 제한적이라는 점이 이러한 제약을 더욱 심화시켜, 생명공학 시장의 인프라 활용도와 단기적인 수익 실현을 저해하고 있습니다.

부문별 분석

2025년, 조직 공학 및 재생 의학은 생명공학 시장 매출의 20.55%를 차지했습니다. 이는 인공 조직 구조체가 실험실의 시제품 단계에서 임상 현장에서 보험 적용을 받는 제품으로 전환되었음을 반영합니다. 휴마사이트사의 ‘SYMVESS’ 혈관 등에 대한 승인은 상용화를 위한 길을 열었으며, 투자자들의 신뢰를 높였습니다. 혈관 손상에서 장기 복구에 이르기까지, 이 부문의 치료 대상 범위가 확대되고 있는 만큼, 2031년까지 그 주도적 지위가 더욱 공고해질 것으로 전망됩니다.

차세대 염기서열 분석 시장은 연평균 성장률(CAGR) 21.4%를 나타낼 것으로 예측되며, 이는 모든 기술 분야 중 가장 높은 성장률입니다. 유전체당 비용이 지속적으로 하락하는 가운데, 시퀀싱 플랫폼에는 변이 분석을 가속화하는 AI 모듈이 점점 더 많이 통합되면서, 종양학, 감염병 감시, 농업 유전체학 분야에서 광범위한 도입이 촉진되고 있습니다. 이와 동시에, CRISPR 및 유전자 편집 툴킷은 규제 심사의 원활화와 제조 프로토콜의 성숙화에 힘입어, 생명공학 시장 전체에서 점유율을 확대되고 있습니다.

헬스 바이오테크놀러지는 바이오의약품에 대한 견조한 수요와 생명을 구하는 치료법에 대한 높은 보험 급여 수준에 힘입어 2025년 매출의 48.85%를 차지했습니다. 유전자 편집 치료 및 세포 치료가 고가 제품군으로 상용화됨에 따라, 이 부문의 우위는 앞으로도 지속될 것으로 예측됩니다. 옴닉스 데이터를 통합한 디지털 헬스 플랫폼은 환자 계층화를 촉진하고 치료 성과를 향상시킴으로써 보험사의 지지를 더욱 공고히 하고 있습니다.

연평균 성장률(CAGR) 22.1%를 나타낼 것으로 예측되는 바이오정보학 및 오믹스 분야는 데이터 중심의 가치 창출로 나아가고 있는 이 분야의 변화를 잘 보여주고 있습니다. AI를 활용한 멀티오믹스 플랫폼은 표적 발견 및 진단상의 의사결정을 효율화하고, 정밀 의학을 위한 새로운 서비스 모델을 촉진하고 있습니다. 디지털 도구의 보급에 따라 그 응용 범위가 확대되면서, 생명공학 시장의 기회 폭을 더욱 넓히고 있습니다.

지역별 분석

북미는 밀집된 혁신 클러스터, 유리한 지적재산권 제도, 신속한 규제 승인의 뒷받침을 받아 2025년에는 전 세계 매출의 44.90%를 차지했습니다. 일라이 릴리사의 45억 달러 규모의 ‘Medicine Foundry’와 같은 대표적 투자는 국내 공급망의 안정성에 대한 제조업체의 신뢰를 여실히 보여주고 있습니다. 바이오 관련 시설에 대한 연방 정부의 대출 보증과 정부 기관에 의한 협력적인 감독 체계는 자금 조달 위험을 더욱 낮추고, 제품 출시 주기를 단축시키며, 바이오기술 시장 전반에서 해당 지역의 리더십을 공고히 하고 있습니다.

아시아태평양은 막대한 공적 자금과 낮은 운영 비용에 힘입어 연평균 성장률(CAGR) 16.95%를 기록하며 가장 빠르게 성장하고 있는 지역입니다. 1,100억 엔 규모의 일본 재생의료 프로그램은 ‘신약 개발 강국’이 되겠다는 전략적 포부를 보여주고 있는 반면, 중국의 정책 지원과 인도의 녹색 전환 의제가 제조 거점 확장을 뒷받침하고 있습니다. 국경을 초월한 파트너십은 기술 이전을 가속화하고, 생명공학 시장에서 해당 지역의 점유율을 확대하는 역동적인 환경을 조성하고 있습니다.

유럽은 견고한 인프라, 높은 윤리 기준, 그리고 승인 절차의 효율화를 목표로 향후 시행될 예정인 ‘생명공학법’의 혜택을 누리고 있습니다. 독일에서 생명공학 분야에 대한 자금 조달이 78% 증가한 19억 1,700만 유로에 달한 것은 투자자들의 활발한 투자 의지를 여실히 보여주고 있습니다. 베링거 인겔하임과 사노피가 추진한 대규모 생산 능력 확충은 유럽의 제조거점을 강화하고 있습니다. 유럽이 지속 가능한 생명공학에 주력하고 있는 것은 친환경 분야에서의 경쟁 우위를 강화하고 세계 생명공학 시장에서의 입지를 공고히 하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

LSH 26.06.24According to Mordor Intelligence, the biotechnology market size is projected to expand from USD 2.15 trillion in 2025 and USD 2.42 trillion in 2026 to USD 4.41 trillion by 2031, registering a CAGR of 12.67% between 2026 to 2031.

This report Segments the Industry Into by Technology (DNA Sequencing, Nanobiotechnology and More), Application (Health & Red Biotechnology, Food and Agriculture and More), End User (Biopharma & Biotechnology Companies, Cmos & CROs and More), Product Type (Biopharmaceuticals, Bioprocess Equipment & Consumables and More), and Geography.

Global Biotechnology Market Trends and Insights

Accelerated Demand for Novel Biologics and Gene-Based Therapeutics

Recent approvals of first-in-class gene therapies for rare diseases validate genetic medicine's transition into commercial practice, spurring manufacturers to scale continuous bioprocessing capacities and invest in single-use technologies that cut changeover times and reduce contamination risks. Premium pricing for regenerative products Humacyte's SYMVESS vessel sells for USD 29,500 per unit-illustrates the economic potential that attracts new entrants and capital. AI-powered patient stratification tools are boosting trial success, highlighted by Genmab's epcoritamab combination achieving 87% response in refractory lymphomas. Together these factors raise the ceiling on the biotechnology market revenue pool and reinforce demand visibility across pipeline stages.

Rapid Cost Decline in High-Throughput Sequencing

Sequencing-cost freefalls underpin the sector's shift into population-scale diagnostics and real-time pathogen surveillance. Illumina's USD 425 million SomaLogic acquisition signals strategic intent to merge proteomic data streams with genomics for multi-omic analytics. Machine-learning-driven classifiers now surpass 90% accuracy in cancer subtype detection, propelling multi-omic integration into routine clinical workflows. Improved reagent yields and lab automation further cut per-sample cost, widening access for academic labs and smaller firms, thereby democratizing innovation within the biotechnology market.

Shortage of Bioprocessing Single-Use-Systems Specialists

Rapid facility build-outs have outpaced human-capital growth, producing acute shortages in single-use-technology operators despite Novo Nordisk's 1,000-job expansion in North Carolina. The skills gap slows facility validation and jeopardizes on-time product launches, pushing firms to partner with universities for bespoke curricula and ramp up internal training programs. In emerging markets, limited educational pipelines exacerbate the constraint, tempering infrastructure utilization and near-term revenue realization within the biotechnology market.

Other drivers and restraints analyzed in the detailed report include:

- Government Bio-Economy Stimulus and Pandemic-Era R&D Tax Credits

- M&A Race for AI-Driven Drug-Discovery Platforms

- Regulatory Lag on Multi-Omic Companion Diagnostics

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Tissue Engineering and Regeneration captured 20.55% of biotechnology market revenue in 2025, reflecting the transition of engineered-tissue constructs from laboratory prototypes to clinically reimbursed products. Approvals such as Humacyte's SYMVESS vessel validated commercial pathways and enhanced investor confidence. The segment's expanding therapeutic breadth, spanning vascular trauma and organ repair, is projected to reinforce its leadership position through 2031.

Next-Generation Sequencing is forecast to register a 21.4% CAGR, the fastest across technologies. As cost per genome continues to fall, sequencing platforms increasingly integrate AI modules that accelerate variant interpretation, propelling broad adoption in oncology, infectious-disease surveillance, and agricultural genomics. In parallel, CRISPR and gene-editing toolkits benefit from smoother regulatory reviews and mature manufacturing protocols, elevating their share in the overall biotechnology market.

Health biotechnology accounted for 48.85% of 2025 revenue, anchored by strong biopharmaceutical demand and high reimbursement levels for life-saving therapies. This segment's dominance is expected to persist as gene-edited treatments and cell therapies commercialize at premium price points. Digital health platforms that integrate omics data are boosting patient stratification, improving outcomes, and thereby reinforcing payer support.

Bioinformatics and Omics, projected to climb at 22.1% CAGR, embodies the field's shift toward data-centric value creation. AI-enabled multi-omics platforms streamline target discovery and diagnostic decision-making, catalyzing new service models for precision medicine. As digital tools proliferate, application diversity expands, further enlarging the biotechnology market opportunity landscape.

Geography Analysis

North America retained 44.90% of global revenue in 2025, supported by dense innovation clusters, favorable intellectual-property regimes, and swift regulatory approvals. Flagship investments, such as Eli Lilly's USD 4.5 billion Medicine Foundry, illustrate manufacturers' confidence in domestic supply-chain stability. Federal loan guarantees for bio-based facilities and coordinated agency oversight further lower financing risk and accelerate product launch cycles, cementing regional leadership across the biotechnology market.

Asia-Pacific represents the fastest-growing region with 16.95% CAGR, catalyzed by significant public funding and lower operating costs. Japan's JPY 110 billion regenerative-medicine program demonstrates strategic ambition to become a "land of drug discovery," while China's policy support and India's green-transition agenda underpin manufacturing expansion. Cross-border partnerships accelerate technology transfer, fostering a dynamic environment that enhances the region's share of the biotechnology market.

Europe benefits from robust infrastructure, high ethical standards, and the forthcoming Biotech Act designed to streamline approvals. Germany's 78% jump in biotechnology financing to EUR 1.917 billion underscores investor appetite. Major capacity additions by Boehringer Ingelheim and Sanofi augment the continent's manufacturing base. Europe's focus on sustainable biotechnology reinforces its competitive advantage in green applications, strengthening its position in the global biotechnology market.

- Amgen Inc.

- Biogen Inc.

- Gilead Sciences Inc.

- Illumina Inc.

- Thermo Fisher Scientific Inc.

- Regeneron Pharmaceuticals Inc.

- Moderna Inc.

- BioNTech SE

- Vertex Pharmaceuticals Inc.

- CSL Ltd.

- Lonza Group AG

- Novozymes A/S

- Catalent Inc.

- Charles River Laboratories International Inc.

- Genmab A/S

- CRISPR Therapeutics AG

- Editas Medicine Inc.

- Intellia Therapeutics Inc.

- Sangamo Therapeutics Inc.

- Alnylam Pharmaceuticals Inc.

- Sarepta Therapeutics Inc.

- Bluebird Bio Inc.

- Gingko Bioworks Holdings Inc.

- Zymergen Inc.

- Twist Bioscience Corp.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerated demand for novel biologics and gene-based therapeutics

- 4.2.2 Rapid cost decline in high-throughput sequencing

- 4.2.3 Government bio-economy stimulus and pandemic-era R&D tax credits

- 4.2.4 M&A race for AI-driven drug-discovery platforms

- 4.2.5 Emergence of cell-free biomanufacturing micro-plants

- 4.2.6 Synthetic biology-enabled carbon-negative materials

- 4.3 Market Restraints

- 4.3.1 Shortage of bioprocessing single-use-systems specialists

- 4.3.2 Regulatory lag on multi-omic companion diagnostics

- 4.3.3 Rising bio-geopolitical export controls on genetic data

- 4.3.4 Volatility in venture funding for platform-only start-ups

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Technology

- 5.1.1 DNA Sequencing

- 5.1.2 Nanobiotechnology

- 5.1.3 Tissue Engineering & Regeneration

- 5.1.4 PCR Technology

- 5.1.5 Fermentation

- 5.1.6 Chromatography

- 5.1.7 Gene Amplification Technologies

- 5.1.8 Synthetic Biology

- 5.1.9 CRISPR & Gene-Editing Tools

- 5.1.10 Biochips & Microarrays

- 5.1.11 Others

- 5.2 By Application

- 5.2.1 Health & Red Biotechnology

- 5.2.1.1 Biopharmaceuticals

- 5.2.1.2 Diagnostics

- 5.2.1.3 Gene Therapy

- 5.2.1.4 Personalised Medicine

- 5.2.2 Food & Agriculture (Green)

- 5.2.3 Industrial Processing (White)

- 5.2.4 Environmental & Natural Resources (Grey)

- 5.2.5 Bioinformatics & Omics

- 5.2.6 Others

- 5.2.1 Health & Red Biotechnology

- 5.3 By End User

- 5.3.1 Biopharma & Biotechnology Companies

- 5.3.2 CMOs & CROs

- 5.3.3 Academic & Research Institutes

- 5.3.4 Hospitals & Diagnostic Centres

- 5.3.5 Agricultural Corporations

- 5.3.6 Environmental Agencies & NGOs

- 5.4 By Product Type

- 5.4.1 Biopharmaceuticals

- 5.4.2 Bioprocess Equipment & Consumables

- 5.4.3 Reagents & Kits

- 5.4.4 Bioservices

- 5.4.5 Bioinformatics Platforms & Software

- 5.4.6 Others

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East

- 5.5.4.1 Israel

- 5.5.4.2 Saudi Arabia

- 5.5.4.3 United Arab Emirates

- 5.5.4.4 Turkey

- 5.5.4.5 Rest of Middle East

- 5.5.5 Africa

- 5.5.5.1 South Africa

- 5.5.5.2 Egypt

- 5.5.5.3 Nigeria

- 5.5.5.4 Rest of Africa

- 5.5.6 South America

- 5.5.6.1 Brazil

- 5.5.6.2 Argentina

- 5.5.6.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials, Strategic Info, Rank/Share, Products & Services, Recent Developments)

- 6.4.1 Amgen Inc.

- 6.4.2 Biogen Inc.

- 6.4.3 Gilead Sciences Inc.

- 6.4.4 Illumina Inc.

- 6.4.5 Thermo Fisher Scientific Inc.

- 6.4.6 Regeneron Pharmaceuticals Inc.

- 6.4.7 Moderna Inc.

- 6.4.8 BioNTech SE

- 6.4.9 Vertex Pharmaceuticals Inc.

- 6.4.10 CSL Ltd.

- 6.4.11 Lonza Group AG

- 6.4.12 Novozymes A/S

- 6.4.13 Catalent Inc.

- 6.4.14 Charles River Laboratories International Inc.

- 6.4.15 Genmab A/S

- 6.4.16 CRISPR Therapeutics AG

- 6.4.17 Editas Medicine Inc.

- 6.4.18 Intellia Therapeutics Inc.

- 6.4.19 Sangamo Therapeutics Inc.

- 6.4.20 Alnylam Pharmaceuticals Inc.

- 6.4.21 Sarepta Therapeutics Inc.

- 6.4.22 Bluebird Bio Inc.

- 6.4.23 Gingko Bioworks Holdings Inc.

- 6.4.24 Zymergen Inc.

- 6.4.25 Twist Bioscience Corp.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment