|

시장보고서

상품코드

2065777

인도의 재활용 시장 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)India Recycling - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

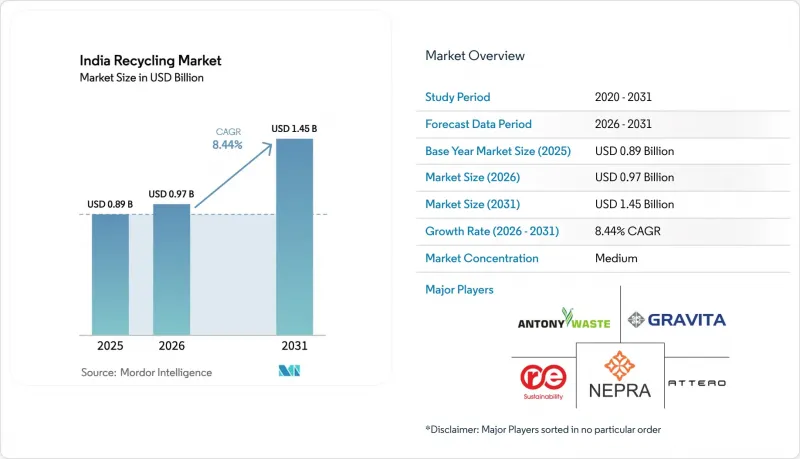

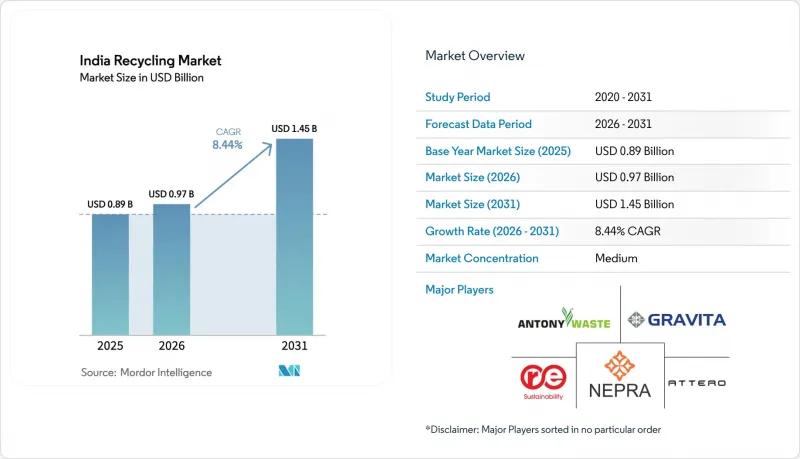

Mordor Intelligence에 의하면, 인도 재활용 시장 규모는 2025년에 8억 9,000만 달러로 평가되었고 2026년 9억 7,000만 달러에서 2031년까지 14억 5,000만 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 8.44%를 나타낼 전망입니다.

본 보고서는 소재 유형(플라스틱, 금속, 종이 및 골판지, 유리, 기타), 발생원(도시 쓰레기, 산업 폐기물, 의료 폐기물, 건설 폐기물, 기타 발생원), 기술(기계적 재활용, 화학적 재활용, 생물학적 재활용, 기타 기술) 및 지역(인도)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

인도 재활용 시장 동향과 인사이트

플라스틱 및 전자기기 분야의 확대된 EPR(확대 생산자 책임) 의무

‘2022년 플라스틱 폐기물 관리 규정’ 및 ‘2022년 전자 폐기물 관리 규정’에 따르면, 2025-2026년도까지 전자 폐기물 회수율을 60%로 하고, 2027-2028년도까지 80%로 높이는 것, 또한 2027-2028년도까지 리튬 이온 배터리의 회수율을 70%로 달성하도록 의무화하고 있습니다. 환경 보상 부과금은 1톤당 5,000루피에서 20,000루피 사이이며, 규정을 준수하지 않을 경우 비용 면에서 큰 부담이 됩니다. 신용 가격은 폴리머 등급 및 지역별 수급 상황에 따라 1Kg당 8루피에서 25루피 사이에서 변동하고 있습니다. 마하라슈트라 주와 타밀나두 주에서는 분기별로 감사를 실시하고 있으며, 이를 통해 체계적인 재활용 사업자들이 ISO 14001 인증을 취득한 수거 시설로 전환하도록 장려하고 있습니다. 배터리 관련 규제로 인해 전기차(EV) OEM 각사는 폐쇄형 네트워크 구축이 의무화되었으며, 이에 따라 Attero 및 Gravita와의 역물류 제휴가 가속화되고 있습니다.

도시 지역의 일반 폐기물(MSW) 양 증가와 매립지 부족

인도에서는 매일 16만-17만 톤의 도시 고형 폐기물(MSW)이 발생하고 있지만, ‘스와치 바라트 미션 2.0’의 일환으로 2,421곳에 달하는 노후 매립지 중 복구가 완료된 곳은 고작 474곳에 불과합니다. 토지가 부족한 대도시권에서는 매립 처리 비용이 톤당 800-1,200루피를 초과하기 때문에 매립 처리보다 재활용이 더 경제적입니다. 2026년까지 중앙정부로부터 1,41,600 크롤(170억 달러)이 배정되어, 자원 회수 시설 및 폐기물 발전소 건설에 사용되고 있습니다. 그러나 2급 도시의 발생원별 분리수거율은 여전히 30% 미만에 그치고 있으며, 그 결과 분리수거된 폐기물의 경우 70-80%인 반면, 분리되지 않은 폐기물의 폴리머 회수율은 40-50%에 그치고 있습니다. ‘사하스 제로 웨이스트(Saahas Zero Waste)’와 같은 분산형 처리 사업자들은 지자체의 병목 현상을 해소하기 위해 마이크로 퇴비화기를 도입하고 있습니다.

단편적이고 비공식적인 수집 생태계

소규모 도시에서 ‘퍼스트 마일’ 수거의 60-70%는 비공식 수거업자 네트워크를 통해 이루어지고 있으며, 이들은 세제나 노동법의 틀 밖에서 운영되고 있습니다. 이로 인해 추적성이 저해되고, 브랜드 소유자가 요구하는 ISO 14021에 기반한 자체 선언의 신뢰성이 훼손되고 있습니다. 비공식 중개업자들이 규정 준수 비용을 회피하고 있기 때문에 공식 재활용 업체들은 원료 구매에 15-25% 더 높은 비용을 지불하고 있습니다. 신분증, 보험, 고정 임금을 제공하는 지자체의 시범 프로그램조차도 관료적 지연으로 인해 근로자의 20% 미만을 대상으로 하고 있습니다. 20-30%에 달하는 혼입률로 인해 추가 세척이 필요해지면서 처리 비용이 상승하고 있습니다.

부문별 분석

현재 플라스틱은 인도 재활용 시장 점유율의 36.86%를 차지하고 있지만, 포장재 시장의 성장 둔화와 단일 소재 설계의 보급으로 인해 처리량은 제한되고 있습니다. 아테로(Atero)사의 7,600만 달러 자금 조달은 배터리용 금속 재활용 순환 체계에 대한 신뢰도가 높음을 보여주는 한편, 화학 재활용 업체가 생산한 고품질 rPET는 코카콜라 인디아와의 다년간 공급 계약을 충족시키고 있습니다. 종이 재활용은 전자상거래로 인한 골판지 수요 증가의 호재를 타고 있으며, 타이어 열분해는 ‘기타 소재’라는 틈새 시장을 확대되고 있습니다. 금속 분야는 60만 톤에 달할 것으로 예상되는 폐배터리 유입량의 급증에 힘입어, 2031년까지 연평균 성장률(CAGR) 8.94%를 기록하며 성장할 것으로 전망됩니다.

힌두스탄 징크(Hindustan Zinc)나 그라비타 인디아(Gravita India)와 같은 통합형 생산업체들이 스크랩 사업을 1차 제련 과정에 통합함에 따라, 인도의 금속 재활용 시장 규모는 확대될 전망입니다. 플라스틱은 규모의 경제를 유지하고 있지만, 밸류체인 내에서 식품 접촉 적합성을 확보해야 한다는 압박에 직면해 있습니다. 화학적 재활용을 통해 생산된 고품질 폴리머는 기계적 재활용 제품에 비해 2배의 이익률을 기록하고 있으며, 구자라트주와 타밀나두주에서의 생산 능력 확대를 뒷받침하고 있습니다. 유리와 복합재료는 물류 비용이 높고 칼렛 수요가 적어 여전히 소규모로 머물러 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.29According to Mordor Intelligence, the india recycling market size was valued at USD 0.89 billion in 2025 and is estimated to grow from USD 0.97 billion in 2026 to reach USD 1.45 billion by 2031, at a CAGR of 8.44% during the forecast period (2026-2031).

This report is Segmented by Material Type (Plastics, Metals, Paper and Cardboard, Glass, and Others), Source (Municipal, Industrial, Medical Waste, Construction Waste, and Other Sources), Technology (Mechanical Recycling, Chemical Recycling, Biological Recycling, and Other Technologies), and Geography (India). The Market Forecasts are Provided in Terms of Value (USD).

India Recycling Market Trends and Insights

Extended EPR Mandates Across Plastics and Electronics

Plastic Waste Management Rules 2022 and E-Waste Management Rules 2022 impose 60% e-waste collection for 2025-2026, rising to 80% by 2027-2028, and 70% lithium-ion battery recovery by 2027-2028. Environmental compensation levies range from Rs 5,000 to Rs 20,000 per ton, turning non-compliance into a costly option. Credit prices fluctuate between Rs 8 and Rs 25 per kilogram, depending on the polymer grade and regional supply and demand. Maharashtra and Tamil Nadu conduct quarterly audits that encourage organized recyclers to transition toward ISO 14001-certified recovery facilities. Battery rules compel electric-vehicle OEMs to establish closed-loop networks, accelerating reverse-logistics partnerships with Attero and Gravita.

Rising Urban MSW Volumes and Landfill Shortages

India produces 160,000-170,000 tons of municipal solid waste (MSW) daily, yet only 474 of the 2,421 legacy landfills have been remediated under the Swachh Bharat Mission 2.0. Tipping fees in land-scarce metros exceed Rs 800-Rs 1,200 per ton, making recycling more economical than dumping. Central allocations of Rs 1,41,600 crore (USD 17 billion) through 2026 fund material recovery and waste-to-energy plants. However, source segregation remains below 30% in tier-2 cities, resulting in polymer recovery yields of 40-50% compared to 70-80% for segregated streams. Decentralized processors such as Saahas Zero Waste deploy micro-composters that bypass municipal bottlenecks.

Fragmented, Informal Collection Ecosystem

Informal picker networks handle 60-70% of first-mile collection in smaller cities, operating outside tax and labor frameworks. This curtails traceability, undermining ISO 14021 self-declarations sought by brand owners. Formal recyclers pay 15-25% more for feedstock because informal agents circumvent compliance costs. Municipal pilot programs offering IDs, insurance, and fixed prices cover under 20% of workers due to bureaucratic delays. Contamination rates of 20-30% force extra washing and raise processing costs.

Other drivers and restraints analyzed in the detailed report include:

- Surge in Recycled-Content Demand from FMCG and Packaging Majors

- Fiscal Incentives and Lithium-Ion Battery End-of-Life Wave

- Limited Domestic End-Markets for Lower-Grade Recyclate & Scrap Price Volatility

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Plastics currently account for 36.86% of India's recycling market share, yet slower packaging growth and mono-material design are limiting volumes. Attero's USD 76 million raise underscores confidence in battery-metal loops, while premium rPET from chemical recyclers satisfies Coca-Cola India's multi-year off-takes. Paper recycling leverages e-commerce corrugate demand, and tire pyrolysis expands the niche for "other materials." Metals are expected to grow at a 8.94% CAGR to 2031, driven by soaring end-of-life battery flows that are projected to reach 600,000 tons.

The Indian recycling market size for metals is poised to grow as integrated producers such as Hindustan Zinc and Gravita India integrate scrap operations into primary smelting. Plastics retain scale advantages but face pressure from the value chain to deliver food-contact compliance. Premium chemical-route polymers command a double margin over mechanically recycled grades, incentivizing capacity additions in Gujarat and Tamil Nadu. Glass and composites remain small due to high logistics costs and low cullet demand.

List of Companies Covered in this Report:

- A2Z Group

- Antony Waste Handling Cell Limited

- Attero

- Cerebra Integrated Technologies Ltd.

- Dalmia Polypro Industries Pvt. Ltd.

- Eco Recycling

- Gravita India

- Greenko Group

- Hindustan Zinc

- NEST

- Ramky Enviro Engineers

- Rapidue Technologies Pvt. Ltd.

- Saahas Zero Waste

- Sampurn(e)arth Environment Solutions Pvt. Ltd.

- The Shakti Plastic Industries

- UltraTech Cement Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Extended EPR mandates across plastics and electronics

- 4.2.2 Rising urban MSW volumes and landfill shortages

- 4.2.3 Surge in recycled-content demand from FMCG and packaging majors

- 4.2.4 Fiscal incentives (GST concessions, PLI) for recycling plants

- 4.2.5 Lithium-ion battery end-of-life wave from Electric Vehicle adoption

- 4.3 Market Restraints

- 4.3.1 Fragmented, informal collection ecosystem

- 4.3.2 Limited domestic end-markets for lower-grade recycled polymers

- 4.3.3 Volatility in scrap prices linked to global commodity cycles

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Consumers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Material Type

- 5.1.1 Plastics

- 5.1.2 Metals

- 5.1.3 Paper and Cardboard

- 5.1.4 Glass

- 5.1.5 Others

- 5.2 By Source

- 5.2.1 Municipal (Residential and Commercial)

- 5.2.2 Industrial

- 5.2.3 Medical Waste

- 5.2.4 Construction Waste

- 5.2.5 Other Sources

- 5.3 By Technology

- 5.3.1 Mechanical Recycling

- 5.3.2 Chemical Recycling

- 5.3.3 Biological Recycling

- 5.3.4 Other Technologies

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 A2Z Group

- 6.4.2 Antony Waste Handling Cell Limited

- 6.4.3 Attero

- 6.4.4 Cerebra Integrated Technologies Ltd.

- 6.4.5 Dalmia Polypro Industries Pvt. Ltd.

- 6.4.6 Eco Recycling

- 6.4.7 Gravita India

- 6.4.8 Greenko Group

- 6.4.9 Hindustan Zinc

- 6.4.10 NEST

- 6.4.11 Ramky Enviro Engineers

- 6.4.12 Rapidue Technologies Pvt. Ltd.

- 6.4.13 Saahas Zero Waste

- 6.4.14 Sampurn(e)arth Environment Solutions Pvt. Ltd.

- 6.4.15 The Shakti Plastic Industries

- 6.4.16 UltraTech Cement Ltd.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment