|

시장보고서

상품코드

2066512

미국의 유기 비료 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)United States Organic Fertilizers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

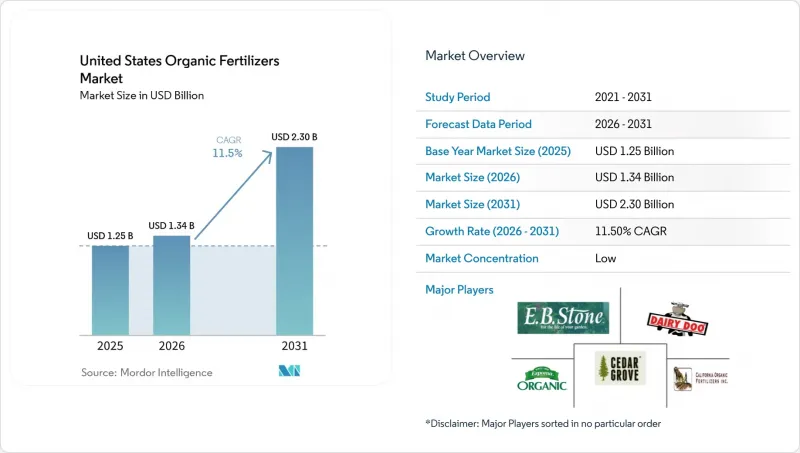

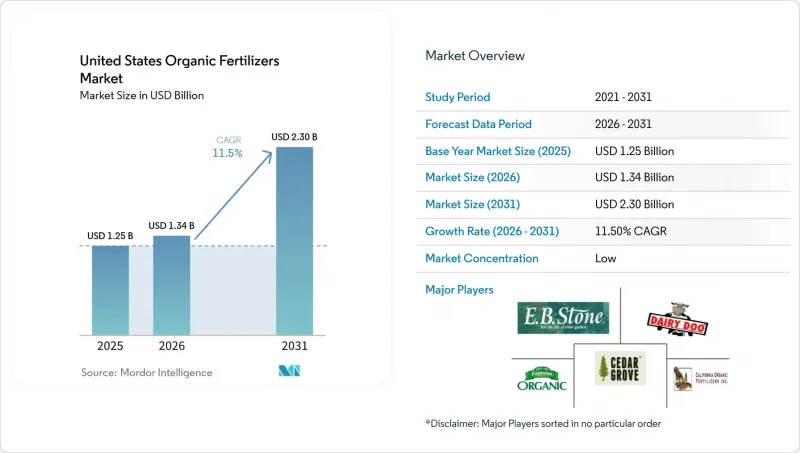

Mordor Intelligence에 의하면, 미국의 유기 비료 시장 규모는 2025년 12억 5,000만 달러로 평가되었고, 2026년에는 13억 4,000만 달러로 추정되고, 2031년까지 23억 달러에 이를 것으로 예측되며, 2026-2031년 CAGR 11.5%로 성장할 전망입니다.

본 보고서는 형태별(퇴비, 곡물박 계열 비료 등) 및 작물 유형별(현금작물, 원예작물 등)로 분류되어 있습니다. 시장 전망은 금액(달러) 및 수량(메트릭 톤) 단위로 제시되어 있습니다.

미국 유기비료 시장 동향 및 인사이트

인증된 유기농 농지의 급속한 확대

미국 농무부의 자료에 따르면, 기상 조건으로 인한 인증 지연이 있음에도 불구하고, 보조금을 통한 기술 지원이 농지의 유기농 전환을 가속화하고 있는 것으로 확인되었습니다. 3억 달러 규모의 ‘유기농 전환 이니셔티브’는 검사 및 감사 비용의 최대 75%를 부담하고 있으며, 이를 통해 중규모 농장에서도 유기농 재료 심사 협회(OMRI)에 등록된 자재를 경제적으로 활용할 수 있게 되었습니다. 유기농 수입품에 대해 새로 제정된 조화관세표(HTS) 코드에 따라, 추적성에 관한 규정이 강화되고 부당한 경쟁이 감소함에 따라, 간접적으로 국내 생산자들에게 이익이 되고 있습니다. 1에이커당 기준 충족도가 높아짐에 따라 합성 질소 비료의 사용이 금지되므로, 미국 유기 비료 시장의 기초 수요가 증가하여 수년에 걸친 구매 계약이 체결될 것입니다.

화학 물질을 사용하지 않은 농산물에 대한 소비자 수요 증가

유기농 무역 협회(OTA)의 보고서에 따르면, 인플레이션으로 인해 가계 예산이 압박받고 있음에도 불구하고 2024년 매출액은 전년 대비 5.2% 증가한 716억 달러를 기록했습니다. 현재 소매 계약에서는 연중 유기농 농산물공급이 요구되고 있어, 생산자들은 미국 유기농 프로그램(NOP)의 기준을 충족하는 신뢰할 수 있는 공급원을 확보할 수밖에 없는 실정입니다. 유기농 농산물의 가격은 일반 농산물에 비해 여전히 20%-50%의 프리미엄이 붙기 때문에 농가들은 이익률을 떨어뜨리지 않으면서도 유기농 농산물의 1에이커당 높은 비용을 상쇄할 수 있습니다. 이러한 지출의 견조함으로 인해 비료 수요는 상품 주기의 영향보다 소비자 심리에 더 크게 좌우되게 되었으며, 미국의 유기비료 시장은 전 세계 합성비료 가격 변동으로부터 보호받고 있습니다.

합성 비료에 비해 낮은 영양 밀도

일반적인 유기비료의 배합에서는 NPK 비율이 5-5-5 미만이기 때문에 합성 질소비료와 동등한 효과를 얻으려면 10-15배의 시비량이 필요합니다. 이러한 물류상의 부담으로 인해 운송 비용이 증가하고, 재배 기간이 제한된 시기에는 노동력에 대한 부담도 커집니다. 혈분 등 고농도 제품은 효율을 높여주지만, 소매 가격이 요소의 3-5배에 달하기 때문에 그 사용은 고급화를 지향하는 농장에 한정되어 있습니다. 비용 대비 효과가 높은 농축 기술이 보급되기 전까지는 이러한 농도 격차가 미국 유기비료 시장 전체의 성장을 저해할 것으로 보입니다.

부문별 분석

2025년, 가축 분뇨 유래 제품은 미국 유기 비료 시장에서 46.9%라는 최대 점유율을 확보한 것으로 평가되었으며, 2026-2031년 12.5%라는 가장 높은 연평균 성장률(CAGR)을 기록하며 계속해서 주도적인 위치를 유지할 것으로 전망됩니다. 가축 분뇨는 영양 밀도가 낮고 유기물을 공급한다는 점에서 재생 농업의 기준에 부합하며, 토양 건강 프로그램에서 중요한 투입 자재로 활용되고 있습니다. 운송 비용 문제를 해결하기 위해 생산자들은 가축 분뇨를 펠릿화하고 있으며, 이를 통해 유기농 재료 심사 협회(OMRI)의 인증을 유지하면서 밀도를 약간 높일 수 있게 되었습니다.

사료박을 원료로 한 비료, 유박 및 혼합 퇴비 제품은 소매 시장에서 높은 점유율을 차지하고 있습니다. 그러나 사료 비용의 상승으로 인해 원자재의 조달이 제한되고, 가격 상한선이 상승하고 있습니다. 유박 제품은 균형 잡힌 주요 영양소 비율을 갖추고 있어 채소 재배자들에게 인기가 높지만, 그 공급량은 압착 공장에서 생산되는 제품별 양에 좌우되며, 바이오연료 수요 변동의 영향을 받습니다. 바이오숯과 미생물 접종제를 배합한 특수 퇴비 블렌드는 탄소 크레딧 기준을 충족하도록 설계되어, 미국의 유기 비료 시장을 더욱 다각화하고 있습니다. 오염 물질에 대한 규제 당국의 감시가 강화되는 가운데, 수직 통합형 공급망이 제공하는 추적 가능성의 이점은 시장에서 확고한 입지를 다진 기업의 경쟁 우위를 높여주고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 주요 요약 및 주요 조사 결과

제3장 개 보고서의 내용

제4장 주요 업계 동향

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 농업 바이오 분야 CEO를 향한 중요 전략적 과제

AJY 26.06.24According to Mordor Intelligence, the united states organic fertilizers market size is anticipated to increase from USD 1.25 billion in 2025 to USD 1.34 billion in 2026 and reach USD 2.30 billion by 2031, growing at a CAGR of 11.5% over 2026-2031.

This report is Segmented by Form (Manure, Meal-Based Fertilizers, and More) and by Crop Type (Cash Crops, Horticultural Crops, and More). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

United States Organic Fertilizers Market Trends and Insights

Rapid Growth of Certified Organic Farmland

United States Department of Agriculture data confirm that grant-funded technical support is accelerating acreage conversion despite weather-related certification backlogs. The USD 300 million Organic Transition Initiative covers up to 75% of testing and audit fees, making Organic Materials Review Institute-listed inputs financially accessible for midsize farms. Newly issued Harmonized Tariff Schedule codes for organic imports tighten traceability rules, which indirectly benefit domestic growers by reducing fraudulent competition. As each acre enters compliance, baseline demand for the United States organic fertilizers market rises because synthetic nitrogen is prohibited, locking in multi-year purchasing commitments.

Rising Consumer Demand for Chemical-Free Produce

The Organic Trade Association reported a 5.2% year-over-year sales increase to USD 71.6 billion in 2024, even as inflation constrained household budgets Retail contracts now require year-round organic supply, forcing growers to secure reliable nutrient sources that meet National Organic Program standards. Because price premiums remain 20%-50% over conventional equivalents, farmers can absorb the higher per-acre cost of organic products without eroding margins. This spending resilience ties fertilizer demand more tightly to consumer sentiment than to commodity cycles, insulating the United States organic fertilizers market from global synthetic price swings.

Limited Nutrient Density Versus Synthetic Alternatives

Typical organic formulations offer NPK ratios under 5-5-5, forcing 10-15 times greater application volumes to match synthetic nitrogen delivery. The logistics burden inflates hauling costs and strains labor during tight planting windows. Higher-density options such as blood meal improve efficiency but retail for three to five times the cost of urea, restricting adoption to premium operations. Until cost-effective concentration technologies scale, density gaps will moderate growth across the United States organic fertilizers market.

Other drivers and restraints analyzed in the detailed report include:

- Federal Cost-Share Incentives for Transitioning Farms

- Expansion of Organic Livestock Operations

- Slow-Release Profile Unsuitable for Certain Cash Crops

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Manure-based products secured the largest United States organic fertilizers market share of 46.9% in 2025 and are projected to maintain their leadership position, registering the fastest CAGR of 12.5% during 2026-2031. Although manure has a low nutrient density, its contribution of organic matter aligns with regenerative agriculture standards, making it a key input for soil health programs. To address transportation costs, producers are pelletizing manure, which slightly increases its density while maintaining Organic Materials Review Institute (OMRI) approval.

Meal-based fertilizers, oilcakes, and blended compost products occupy premium positions in the retail market. However, rising feed costs are limiting raw material availability and pushing price ceilings higher. Oilcake products offer balanced macronutrient ratios and appeal to vegetable growers, but their supply depends on byproduct volumes from crush plants, which are influenced by fluctuations in biofuel demand. Specialty compost blends, incorporating biochar and microbial inoculants, are designed to meet carbon-credit protocols, further diversifying the organic fertilizer market in the United States. As regulatory scrutiny on contaminants increases, the traceability benefits of vertically integrated supply chains enhance the competitive advantage of established market players.

List of Companies Covered in this Report:

- Cedar Grove Composting Inc.

- EB Stone & Son Inc.

- The Espoma Company

- California Organic Fertilizers Inc.

- Morgan Composting Inc.

- Atlas Organics (Generate Upcycle)

- Sustane Natural Fertilizer Inc.

- Cascade Agronomics LLC

- The Richlawn Company LLC

- Walts Organic Fertilizers Co.

- Darling Ingredients (Nature Safe)

- Midwestern BioAg

- BioFlora

- Perfect Blend LLC

- Synagro Technologies, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

- 1.3 Research Methodology

2 EXECUTIVE SUMMARY AND KEY FINDINGS

3 REPORT OFFERS

4 KEY INDUSTRY TRENDS

- 4.1 Area Under Organic Cultivation

- 4.2 Per Capita Spending on Organic Products

- 4.3 Regulatory Framework

- 4.4 Value Chain and Distribution Channel Analysis

- 4.5 Market Drivers

- 4.5.1 Rapid growth of certified organic farmland

- 4.5.2 Rising consumer demand for chemical-free produce

- 4.5.3 Federal cost-share incentives for transitioning farms

- 4.5.4 Expansion of organic livestock operations

- 4.5.5 Carbon-credit monetization for compost use

- 4.5.6 Emerging state soil-health mandates favoring organic amendments

- 4.6 Market Restraints

- 4.6.1 Limited nutrient density versus synthetic alternatives

- 4.6.2 Volatility in feedstock supply prices

- 4.6.3 Slow-release profile unsuitable for certain cash crops

- 4.6.4 Stringent state-level pathogen regulations increasing compliance costs

5 MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

- 5.1 By Form

- 5.1.1 Manure

- 5.1.2 Meal-Based Fertilizers

- 5.1.3 Oilcakes

- 5.1.4 Other Organic Fertilizer

- 5.2 By Crop Type

- 5.2.1 Cash Crops

- 5.2.2 Horticultural Crops

- 5.2.3 Row Crops

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.3.1 Cedar Grove Composting Inc.

- 6.3.2 EB Stone & Son Inc.

- 6.3.3 The Espoma Company

- 6.3.4 California Organic Fertilizers Inc.

- 6.3.5 Morgan Composting Inc.

- 6.3.6 Atlas Organics (Generate Upcycle)

- 6.3.7 Sustane Natural Fertilizer Inc.

- 6.3.8 Cascade Agronomics LLC

- 6.3.9 The Richlawn Company LLC

- 6.3.10 Walts Organic Fertilizers Co.

- 6.3.11 Darling Ingredients (Nature Safe)

- 6.3.12 Midwestern BioAg

- 6.3.13 BioFlora

- 6.3.14 Perfect Blend LLC

- 6.3.15 Synagro Technologies, Inc.