|

시장보고서

상품코드

2066540

수의용 영상 진단 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Veterinary Diagnostic Imaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

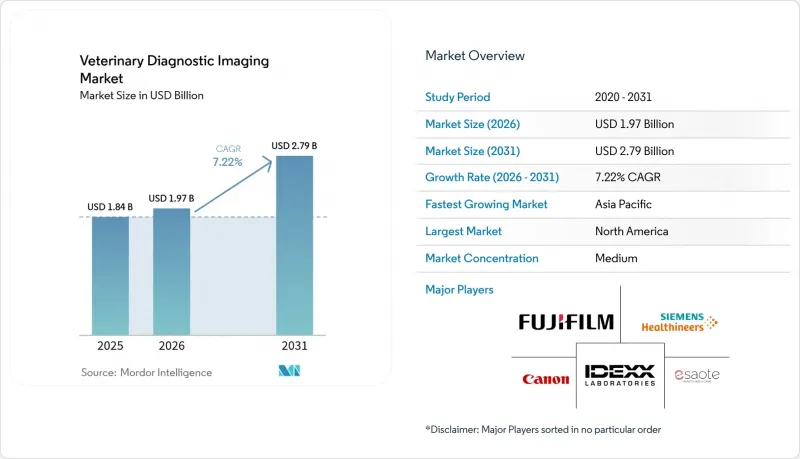

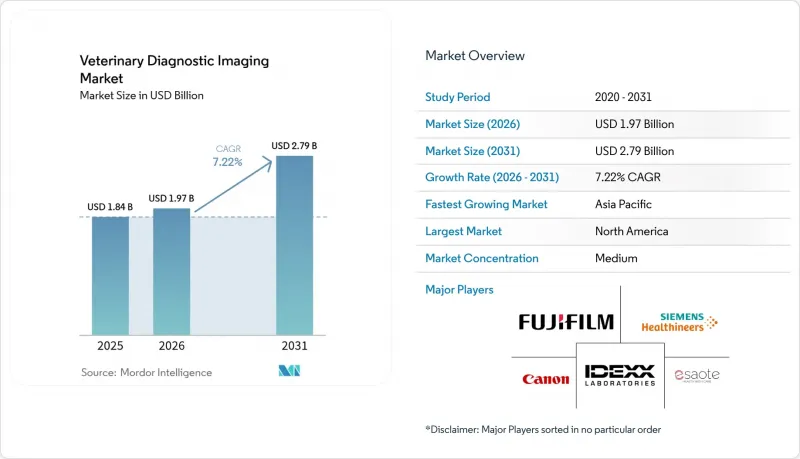

Mordor Intelligence에 의하면, 수의용 영상 진단 시장 규모는 2025년에 18억 4,000만 달러로 평가되었습니다. 2026년 19억 7,000만 달러에서 2031년까지 27억 9,000만 달러에 이를 것으로 예상되며, 예측 기간(2026-2031년) CAGR은 7.22%를 나타낼 전망입니다.

본 보고서는 기기별(X선 촬영 시스템, 초음파 영상 진단 시스템 등), 용도별(순환기학, 종양학, 신경학 등), 동물 종별(소동물, 대동물), 최종 사용자별(동물병원 및 진료소, 진단센터 등), 지역별(북미, 유럽 등)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 수의용 영상 진단 시장 동향 및 인사이트

전 세계 반려동물 수 증가가 첨단 영상 진단 기술에 대한 지출을 촉진하고 있습니다.

젊은 층 가구의 반려동물 사육은 지출 우선순위를 변화시키고 있으며, 급성기 의료를 넘어 일상적인 영상 진단에 대한 수요를 높이고 있습니다. X선 및 MRI 비용을 보상해 주는 반려동물 보험은 비용 장벽을 낮추고 있으며, MRI 보상액이 2,500달러에서 6,000달러에 달하기 때문에 임상 현장에서의 보다 광범위한 활용이 촉진되고 있습니다. 아시아, 특히 중국과 인도에서 반려동물 수가 급증함에 따라 고객 기반이 확대되고 있으며, 이국적인 동물 및 전문 서비스를 대상으로 한 틈새 시장이 개척되고 있습니다. 쿠알라룸푸르의 ‘오하나 베테리너리’와 같은 동물병원에서는 이미 AI 기반 분석 시스템을 도입하여 혈액 데이터와 영상 데이터를 전 세계 데이터베이스와 대조해 평가하고 있으며, 이는 인구 동향의 변화가 기술 도입으로 직접 이어지고 있음을 보여줍니다. 지속적인 ‘반려동물의 인간화’라는 흐름이 검사 건수의 장기적인 증가를 뒷받침하고 있으며, 정밀 진단은 ‘최후의 수단’으로서의 검사가 아니라 일상적인 건강 관리의 일부로 자리 잡고 있습니다.

디지털 X선 촬영, 멀티슬라이스 CT, AI 기반 영상 분석 분야의 급속한 기술 혁신

Vetscan Imagyst 등의 시스템에 탑재된 딥러닝 알고리즘은 몇 초 이내에 이상을 감지하여 진단의 신뢰성을 높이고, 반려인의 협력 체계를 강화하고 있습니다. 현재 전문 기관들은 검증 및 투명성에 관한 지침을 발표하고 있으며, 이는 규제 당국과 혁신 기업 간의 협력이 진전되고 있음을 보여줍니다. 광자 계수 CT나 헬륨이 필요 없는 MRI 장비는 영상의 선명도를 높이는 동시에 방사선 피폭량과 유지보수의 복잡성을 줄여주어, 중규모 동물병원에서 그 매력을 높이고 있습니다. 초기 도입자들로부터 검사 처리 속도와 진단 정확도가 향상되었다는 보고가 나오고 있으며, 이로 인해 발생한 경쟁 격차로 인해 뒤처진 동물병원들은 인프라 업그레이드를 서둘러야 하는 상황에 처해 있습니다. 이러한 기술의 융합이 맞물려 장비의 교체 주기를 가속화하고 있으며, 수의용 영상 진단 시장에서 장비 매출의 점진적인 증가를 이끌고 있습니다.

전 세계적으로 공인 수의 방사선 전문의 및 훈련을 받은 영상진단 기사의 부족

영상진단 분야에 대한 취업 관심이 높아지고 있음에도 불구하고, 연수 수용 능력은 정체 상태를 이어가고 있어 인력 공급 부족을 초래하고 있습니다. 그 결과, 2032년까지 1만 7,000명 이상의 수의사가 부족할 우려가 있었으며, 그중에서도 영상진단 전문의는 부족 현상이 가장 심각한 직종 중 하나입니다. 이러한 인력 부족으로 인해 검사 결과 보고까지 걸리는 시간이 길어질 뿐만 아니라, 소규모 진료소가 제공할 수 있는 서비스의 범위도 제한받고 있습니다. 의료기관은 서비스 수준을 유지하기 위해 원격 방사선 진단 제휴 및 AI를 활용한 예비 판독에 대한 의존도를 높이고 있습니다. 이러한 일시적인 대책을 통해 업무 부담은 일부 완화되었지만, 근본적인 인력 부족이 처리 능력의 한계가 되어 수의용 영상 진단 시장의 성장 잠재력을 충분히 발휘하지 못하는 상황이 계속되고 있습니다.

부문별 분석

2025년, X선 촬영 시스템은 매출의 35.21%를 차지하며 여전히 가장 큰 점유율을 유지해, 반려동물 진료 분야에서 주력 영상 진단 기법으로서의 역할을 입증했습니다. 디지털 플랫폼이 제공하는 직관적인 워크플로우, 거의 즉각적인 영상 확보, 그리고 낮은 방사선 노출량은 동물병원이 기존의 필름식 장비를 대체하도록 촉진하고 있으며, 수의용 영상 진단 시장의 핵심 축을 계속해서 지탱하고 있습니다. 초음파 진단은 휴대용 프로브와 클라우드 기반 AI 분류 시스템의 지원을 받아, 1차 진료 현장과 농장 방문 진료에서 활용 기회가 확대되고 있습니다.

설치 면적을 최소화한 콘빔 CT 장치는 일반 진료 현장에서 치과, 정형외과, 종양학 분야의 증례에 대한 3D 영상 진단을 가능하게 하고 있습니다. MRI는 비용이 비싸긴 하지만, 특히 헬륨 공급 위험을 줄이고 운영 비용을 절감하는 ‘제로 헬륨 자석’과 같은 혁신 기술을 통해 전문 의뢰 병원의 차별화 요소로 자리 잡고 있습니다. 연평균 성장률(CAGR) 8.63%를 나타낼 것으로 예측되는 비디오 내시경은 저침습 수술 증가와 소화기 질환의 복잡화 추세로 인해 혜택을 보고 있습니다. 이러한 동향들이 맞물리면서 시장 상황은 계속해서 역동적인 변화를 보이고 있으며, 이는 수의용 영상 진단 시장에서 장비의 지속적인 업그레이드를 촉진하고 있습니다.

정형외과 분야는 2025년 매출의 34.02%를 차지했으며, 특히 십자인대, 팔꿈치 관절 형성 부전, 골절 관리 분야에서 소동물 의뢰 진료의 핵심 역할을 계속하고 있습니다. 디지털 X선 촬영을 통해 수술 후 신속한 경과 관찰이 가능해지며, 3D-CT는 가상 템플릿을 활용한 수술 전 계획의 정확도를 높여줍니다. 반면, 종양학 분야는 조기 검진 프로토콜이 정기 검진에 널리 보급됨에 따라 연평균 성장률(CAGR) 9.35%라는 가장 빠른 성장세를 보이고 있습니다. AI 분할 도구는 mm 단위의 해상도로 폐 결절이나 복부 종괴를 식별하여, 치료 방침 결정 및 예후 설명을 지원합니다.

순환기 분야에서는 호흡이나 심장 박동이 있어도 정확한 데이터를 얻을 수 있는 운동 보정 알고리즘의 도움으로, 심초음파 검사나 심혈관 CT를 통해 안정적인 수요를 유지하고 있습니다. 신경학 분야에서는 말과 대형견을 대상으로 한 입식 MRI가 활용되어, 마취의 위험과 검사 후 회복 시간을 줄이고 있습니다. 치과 및 소화기내과에서는 휴대용 X선 장비와 고해상도 내시경을 활용하여 진료 현장에서의 검사 역량을 확대되고 있습니다. 영상 진단과 검사실의 바이오마커를 분야를 초월하여 융합함으로써, 수의용 영상 진단 시장에서 다중 모달 진단의 핵심 축으로서 영상 진단의 입지가 확고해지고 있습니다.

지역별 분석

북미는 2025년에도 41.35%의 점유율을 유지했습니다. 이는 1인당 반려동물 관련 지출이 높고, 보험 가입률이 성숙 단계에 이르렀으며, 전문 병원 네트워크가 밀집되어 있다는 점이 뒷받침하고 있습니다. 미국에서는 디지털 인프라의 업그레이드와 AI 도입이 진행되고 있지만, 한편으로는 심각한 방사선과 전문의 부족 문제에 직면해 있으며, 이로 인해 원격 방사선 진단 업무의 아웃소싱이 가속화되고 있습니다. 캐나다에서는 엄격한 방사선 안전 기준으로 인해 설치까지의 기간이 길어지고 있지만, 직원과 동물의 복지는 보장되고 있습니다.

유럽에서는 엄격한 규제와 보상 제도 덕분에 꾸준한 진전이 나타나고 있습니다. 독일과 프랑스에서는 의료기기 교체 주기가 유지되고 있는 반면, 영국에서는 방사선과 전문의 부족 문제가 정책 논의를 촉발시켜 AI 시범 프로그램이 증가하고 있습니다. EU 차원의 동물 보건 전략은 국경을 초월한 지식 교류를 촉진하고, 기준의 일관성을 강화하는 한편, 지역 공급업체를 지원하고 있습니다.

아시아태평양에서는 가처분 소득 증가와 밀레니얼 세대의 반려동물 건강 중시 경향에 힘입어 연평균 성장률(CAGR) 9.08%로 성장을 주도하고 있습니다. 중국의 도시 시장에서는 체인 동물병원들이 차별화 요소로 CT를 도입하고 있는 반면, 인도의 신흥 중산층은 초음파 검사 및 디지털 X선 검사에 대한 기본적인 수요를 끌어올리고 있습니다. 일본은 고령 반려동물 돌봄에 주력하며, 휴대용 영상 진단 장비를 갖춘 방문 진료 서비스를 제공합니다. 호주 및 뉴질랜드에서는 정부의 프로그램에 따라 수출 수입원을 보호하기 위해 가축 영상 진단 체계가 강화되고 있습니다. 이러한 동향들이 맞물려 해당 지역의 수의용 영상 진단 시장의 지속적인 성장을 뒷받침하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.29According to Mordor Intelligence, the veterinary diagnostic imaging market size was valued at USD 1.84 billion in 2025 and estimated to grow from USD 1.97 billion in 2026 to reach USD 2.79 billion by 2031, at a CAGR of 7.22% during the forecast period (2026-2031).

This report is Segmented by Equipment (Radiography (X-Ray) Systems, Ultrasound Imaging Systems, and More), Application (Cardiology, Oncology, Neurology, and More), Animal Type (Small Animals, Large Animals), End User (Veterinary Hospitals & Clinics, Diagnostic Centers, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Veterinary Diagnostic Imaging Market Trends and Insights

Growing Global Companion-Animal Population Fuelling Expenditure on Advanced Imaging Modalities

Pet ownership among younger households is reshaping spending priorities and lifting routine demand for imaging beyond acute care. Pet insurance that reimburses X-rays and MRI lowers cost barriers, with MRI reimbursements ranging between USD 2,500 and USD 6,000, encouraging broader clinical use. Asia's rapid rise in pet numbers, particularly in China and India, extends the customer base and opens niches for exotics and specialty services. Clinics such as Ohana Veterinary in Kuala Lumpur already employ AI-driven analyzers that benchmark blood and image data against global databases, demonstrating how demographic change directly translates into technology adoption. The sustained humanization narrative underpins long-term procedure volume growth, making advanced diagnostics part of routine wellness care rather than last-resort investigations.

Rapid Technological Innovations in Digital Radiography, Multi-slice CT and AI-based Image Analytics

Deep-learning algorithms embedded in systems such as Vetscan Imagyst flag abnormalities within seconds, raising diagnostic confidence and reinforcing client compliance. Professional bodies now publish guidance on validation and transparency, signaling an alignment between regulators and innovators. Photon-counting CT and zero-helium MRI units improve image clarity while trimming radiation dose and maintenance complexity, widening appeal among mid-sized practices. Early adopters report faster throughput and higher diagnostic yield, creating a competitive gap that presses lagging clinics to upgrade infrastructure. Collectively, technology convergence accelerates the replacement cycle and drives incremental equipment revenue within the veterinary diagnostic imaging market.

Global Shortage of Board-Certified Veterinary Radiologists and Trained Imaging Technicians

Despite rising interest in imaging careers, training capacity remains flat, leading to a constrained talent pipeline that could leave a shortfall of more than 17,000 veterinarians by 2032, with imaging specialists among the scarcest. The scarcity lengthens report turnaround times and limits the range of services smaller clinics can provide. Providers increasingly turn to teleradiology partnerships and AI-based preliminary reads to maintain service levels. While stop-gaps partly offset workload pressure, the underlying shortage continues to cap throughput, restraining the full growth potential of the veterinary diagnostic imaging market.

Other drivers and restraints analyzed in the detailed report include:

- Rising Burden of Chronic & Orthopedic Disorders in Pets Necessitating Early Diagnostic Imaging

- Government-Led Livestock Disease Surveillance Programs Mandating Imaging-Based Screening

- High Capital & Lifecycle Cost of High-Field MRI and Multi-slice CT Systems for Smaller Practices

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Radiography systems retained the largest revenue slice at 35.21% in 2025, demonstrating their role as the workhorse modality across companion-animal practice. The intuitive workflows, near-instant image availability, and lower radiation dose that accompany digital platforms encourage clinics to replace legacy film units, sustaining a vital pillar of the veterinary diagnostic imaging market. Ultrasound, bolstered by handheld probes and cloud-based AI triage, broadens access in first-opinion settings and farm calls.

Cone-beam CT units packaged in compact footprints unlock 3-D imaging for dental, orthopedic, and oncology cases within general practice environments. MRI, though premium in cost, differentiates referral centers, especially with innovations such as zero-helium magnets that mitigate helium supply risk and lower operational overhead. Video endoscopy, forecast to climb at an 8.63% CAGR, benefits from rising minimally invasive procedures and GI case complexity. Together, these trends keep the equipment landscape dynamic and spur continuous upgrades within the veterinary diagnostic imaging market

Orthopedics controlled 34.02% of 2025 revenue and remains core in small-animal referral workups, particularly for cruciate ligament, elbow dysplasia, and fracture management. Digital radiography allows rapid follow-up post-surgery, while 3-D CT refines pre-operative planning through virtual templating. In contrast, oncology claims the fastest trajectory with a 9.35% CAGR as early screening protocols penetrate routine check-ups. AI segmentation tools locate pulmonary nodules or abdominal masses at millimeter resolution, supporting treatment decisions and prognosis discussions.

Cardiology maintains stable demand through echocardiography and cardiovascular CT, helped by motion-compensating algorithms that capture accurate data despite respiratory and heart movement. Neurology benefits from standing MRI in equine and large breed dogs, mitigating anesthesia risk and post-procedure recovery time. Dentistry and gastroenterology leverage portable X-ray and high-definition endoscopes that broaden point-of-care capabilities. Cross-discipline blending of imaging and lab biomarkers solidifies imaging as the central pillar in multimodal diagnostics for the veterinary diagnostic imaging market.

Geography Analysis

North America retained a 41.35% share in 2025, anchored by high per-capita pet expenditures, mature insurance uptake, and dense specialty hospital networks. The United States continues to upgrade its digital infrastructure and adopt AI, yet it also grapples with acute radiologist shortages that accelerate teleradiology outsourcing. Canada's strict radiation-safety codes prolong installation timelines but safeguard staff and animal welfare.

Europe delivers steady progress thanks to robust regulation and reimbursement structures. Germany and France sustain equipment renewal cycles, while the United Kingdom's radiologist gap triggers policy discussion and increased AI pilot programs. EU-wide animal health strategies encourage cross-border knowledge exchange, reinforcing homogeneity in standards and supporting regional vendors.

Asia Pacific leads growth at a 9.08% CAGR as disposable incomes rise and millennials prioritize pet wellness. China's urban market sees chain clinics adopting CT as a differentiator, whereas India's emerging middle class lifts baseline demand for ultrasound and digital X-ray. Japan targets geriatric pet care, rolling out home-visit services equipped with portable imaging. Government programs across Australia and New Zealand strengthen livestock imaging to protect export revenue streams. Together, these dynamics underpin sustained expansion of the veterinary diagnostic imaging market in the region.

- Canon

- GE Healthcare

- FUJIFILM

- IDEXX

- Siemens Healthineers

- Esaote S.p.A.

- Carestream Health

- Hallmarq Veterinary Imaging Ltd.

- Cuattro

- Epica Animal Health

- Bionet America, Inc

- Antech Diagnostics (Mars, Inc.)

- Sedecal USA

- Agfa-Gevaert

- Mindray

- Koninklijke Philips

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Global Companion-Animal Population Fuelling Expenditure on Advanced Imaging Modalities

- 4.2.2 Rapid Technological Innovations in Digital Radiography, Multi-slice CT and AI-based Image Analytics

- 4.2.3 Rising Burden of Chronic & Orthopedic Disorders in Pets Necessitating Early Diagnostic Imaging

- 4.2.4 Government-Led Livestock Disease Surveillance Programs Mandating Imaging-based Screening

- 4.2.5 Increasing Availability of Pet Insurance Policies Covering High-value Diagnostic Procedures

- 4.2.6 Expansion of Telemedicine and Remote Consultations

- 4.3 Market Restraints

- 4.3.1 Global Shortage of Board-Certified Veterinary Radiologists and Trained Imaging Technicians

- 4.3.2 High Capital & Lifecycle Cost of High-Field MRI and Multi-slice CT Systems for Smaller Practices

- 4.3.3 Stringent Radiation-Safety Regulations and Licensing Requirements Extending Installation Timelines

- 4.3.4 Limited Pet Insurance and Cost Sensitivity

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Equipment

- 5.1.1 Radiography (X-ray) Systems

- 5.1.1.1 Digital X-ray Systems

- 5.1.1.2 Analog X-ray Systems

- 5.1.2 Ultrasound Imaging Systems

- 5.1.2.1 2-D Ultrasound

- 5.1.2.2 Doppler Ultrasound

- 5.1.2.3 3-D/4-D Ultrasound

- 5.1.3 Computed Tomography Imaging Systems

- 5.1.3.1 Multi-slice CT

- 5.1.3.2 Cone-Beam CT

- 5.1.4 Magnetic Resonance Imaging Systems

- 5.1.4.1 Low-field MRI

- 5.1.4.2 High-field MRI

- 5.1.5 Video Endoscopy Imaging Systems

- 5.1.6 Other Equipment (Fluoroscopy, Nuclear Imaging)

- 5.1.1 Radiography (X-ray) Systems

- 5.2 By Application

- 5.2.1 Cardiology

- 5.2.2 Oncology

- 5.2.3 Neurology

- 5.2.4 Orthopedics

- 5.2.5 Dentistry

- 5.2.6 Gastroenterology

- 5.3 By Animal Type

- 5.3.1 Small Animals

- 5.3.1.1 Dogs

- 5.3.1.2 Cats

- 5.3.2 Large Animals

- 5.3.2.1 Equine

- 5.3.2.2 Bovine

- 5.3.2.3 Swine & Others

- 5.3.1 Small Animals

- 5.4 By End User

- 5.4.1 Veterinary Hospitals & Clinics

- 5.4.2 Diagnostic Imaging Centers

- 5.4.3 Academic & Research Institutes

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Canon Medical Systems Corporation

- 6.3.2 GE HealthCare

- 6.3.3 Fujifilm Holdings Corporation

- 6.3.4 IDEXX Laboratories, Inc.

- 6.3.5 Siemens Healthineers AG

- 6.3.6 Esaote S.p.A.

- 6.3.7 Carestream Health, Inc.

- 6.3.8 Hallmarq Veterinary Imaging Ltd.

- 6.3.9 Cuattro

- 6.3.10 Epica Animal Health

- 6.3.11 Bionet America, Inc

- 6.3.12 Antech Diagnostics (Mars, Inc.)

- 6.3.13 Sedecal USA

- 6.3.14 Agfa-Gevaert Group

- 6.3.15 Shenzhen Mindray Bio-Medical Electronics Co., Ltd

- 6.3.16 Koninklijke Philips N.V.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment