|

시장보고서

상품코드

2066543

감염증 치료제 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Infectious Disease Drugs - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

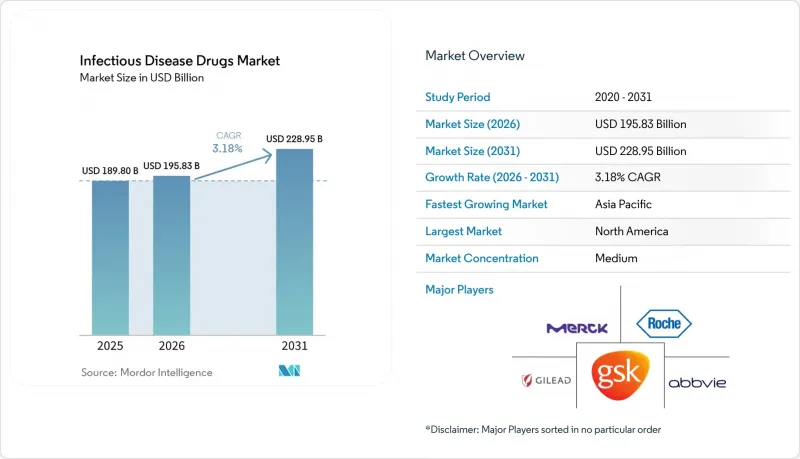

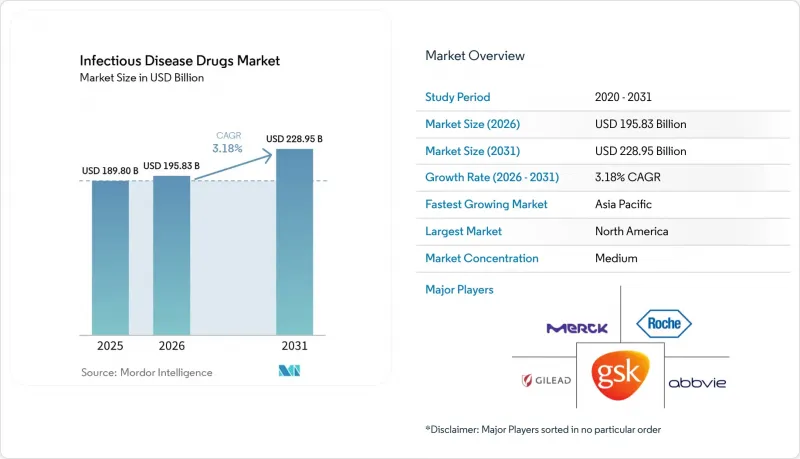

Mordor Intelligence에 의하면, 감염증 치료제 시장 규모는 2025년에 1,898억 달러로 평가되었고 2026년 1,958억 3,000만 달러에서 2031년까지 2,289억 5,000만 달러에 이를 것으로 추정되고 있어 예측 기간(2026-2031년) CAGR은 3.18%를 나타낼 전망입니다.

본 보고서는 질환별(HIV, 인플루엔자, 간염 등), 치료 분류별(항바이러스제, 항균제, 항기생충제 등), 약제 유형별(저분자 약물, 생물학적 제제/단일클론 항체 등), 투여 경로별(경구, 주사 등), 유통 채널별(병원 약국, 소매·체인 약국 등), 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계 감염증 치료제 시장 동향과 인사이트

감염증 유병률 증가

항생제 내성 병원체로 인해 매년 약 70만 명이 목숨을 잃고 있으며, 이에 따라 더 우수한 의약품에 대한 구조적인 수요가 부각되고 있습니다. 결핵은 현재 1,080만 명에게 영향을 미치고 있으며, 내성 균주가 급속히 확산되고 있습니다. 르완다와 탄자니아에서는 아르테미시닌 내성 말라리아가 확인되어, 그동안 이룬 공중보건상의 성과가 위협받고 있습니다. 우간다에서 실시된 감시 조사에 따르면, 소아의 11%가 1차 말라리아 치료제에 대해 부분적인 내성을 가지고 있는 것으로 나타났습니다. 고령화, 암에 따른 면역 억제, 기후 변화로 인한 매개생물의 서식지 변화 등이 감염증 치료제 시장에 대한 수요를 더욱 부추기고 있습니다. 이러한 역학적 요인들이 복합적으로 작용하여, 적정 사용에 대한 규제가 있음에도 불구하고 전문 치료제 시장은 한 자릿수 중반대의 성장세를 유지하고 있습니다.

AI를 활용한 항생제 신약 개발 플랫폼

머신러닝 엔진 덕분에 화합물 라이브러리의 스크리닝이 수년이 아닌 수 주 만에 완료될 수 있게 되었습니다. 일라이 릴리(Eli Lilly)가 OpenAI와 체결한 1억 달러 규모의 제휴는 항생제 내성 문제를 해결하기 위해 노력하는 제약 업계에서 단일 AI 투자로서는 최대 규모입니다. CRISPR로 최적화된 파지 ‘LBP-EC01’은 BARDA로부터 2,390만 달러의 자금을 지원받아 2상 임상시험에 들어갔습니다. SNIPR Biome사는 공생 미생물 군집을 손상시키지 않는 유전체 편집 항생제를 첫 번째 피험자에게 투여했습니다. 예측 알고리즘은 내성 경로를 조기에 파악하여, 생체 내에서 실패 위험이 낮은 화합물을 화학자에게 제시합니다. 플랫폼의 실증 사례가 축적됨에 따라 자금 흐름은 AI 네이티브 파이프라인 구축 기업으로 이동하고 있으며, 이는 감염증 치료제 시장의 혁신 지도를 재편하고 있습니다.

항생제의 적정 사용을 통한 처방 억제

현재 병원에서는 광범위 항생제 투여에 사전 승인이 의무화되어 있으며, 일부 의료 시스템에서는 사용량이 최대 30%까지 감소했습니다. 그러나 원격 의료를 통한 진찰은 많은 규제의 적용 대상에서 제외되어 있어, 새로운 감사 도구의 도입이 요구되고 있습니다. 유럽연합(EU)의 청사진이 전 세계로 확산되고 있으며, 1일 투여량 상한선과 치료 기간 상한선이 공식적으로 정해져 있습니다. 스튜어드십으로 인해 판매량은 감소하고 있지만, 내성 발생을 억제하는 것으로 평가되는 협역 스펙트럼 요법에 대한 수요를 촉진하고 있으며, 그 결과 감염증 치료제 시장의 수익 구조가 재편되고 있습니다.

부문별 분석

HIV 치료제는 2025년 매출의 36.10%를 차지하며, 감염증 치료제 시장에서 위험도가 높은 파이프라인에 대한 투자를 뒷받침하는 핵심 수익원이 되고 있습니다. 2개월마다 투여되는 지속형 카보테그라비르·릴피비린 자동 주사기는 실제 임상 현장에서 바이러스 억제율을 향상시켰으며, 평생에 걸친 복약 순응도와 매출의 안정성을 높였습니다. 반면, C형 간염 치료제는 D형 간염 임상시험에서 브레빌티드가 90%의 지속적인 바이러스학적 반응을 보인 데 힘입어 연평균 성장률(CAGR) 3.98%로 성장할 것으로 전망됩니다. 만성 간염으로 인한 합병증을 예방하는 것은 장기 이식 비용 절감을 목표로 하는 보험사에게 있어 최우선 과제입니다. 결핵 치료제 중 PurF 억제제인 JNJ-6640이 다제내성 균주에 대해 강력한 활성을 보인 데 따라, 정책적 시급성을 배경으로 시장이 확대되고 있습니다. 말라리아 치료제 포트폴리오는 동아프리카에서 확인된 아르테미시닌 내성을 상쇄하기 위해 3제 병용 요법에 중점을 두고 있습니다. 인플루엔자 항바이러스제는 코로나19 기간 동안 구축된 감시 시스템의 혜택을 받고 있는 반면, 기회감염 치료제는 암 치료에 따른 면역 억제 증가로 인해 수요가 증가하고 있습니다.

간염 환자 수가 급증함에 따라 치료 선택지가 확대되면서, HIV 분야보다 더 빨리 지역 제네릭 의약품 제조업체들이 시장에 진입하고 있지만, 2028년에 다가오는 지적재산권 보호 기간 만료로 인해 가격 책정 구조가 재편될 가능성이 있습니다. 한편, 결핵이나 말라리아 관련 파이프라인 자산은 비영리 단체의 공동 자금 지원에 의존하는 경우가 많아 상용화까지 시간이 걸리지만, 공중보건적 가치는 높다고 할 수 있습니다. HIV와 관련하여, 투여 빈도를 연 2회로 줄이는 것을 목표로 하는 차세대 광범위 중화항체가 주요 과제로 대두되고 있으며, 이러한 변화는 시장에서 기존 입지를 지킬 가능성을 내포하고 있습니다. 전반적으로, 질환별 동향에 따라 감염증 치료제 시장은 자금력이 풍부한 만성 질환 부문과 급성장 중인 급성 질환 부문 사이에서 균형을 유지하고 있습니다.

2025년 매출의 40.80%를 항바이러스제가 차지하고 있으며, 이는 HIV 및 간염 분야에서 확립된 사업 기반을 반영하고 있습니다. 그러나 파지나 CRISPR를 활용한 새로운 치료법은 연평균 성장률(CAGR) 5.41%의 속도로 발전하고 있으며, 신속한 미생물학적 결과를 측정하는 적응형 임상시험을 통해 임상적 유효성을 입증하기 위해 빠르게 진행되고 있습니다. Locus Biosciences사의 LBP-EC01은 요로 감염증에서 24시간 이내에 세균 수치가 현저히 감소하는 결과를 보였습니다. 항균제는 외래에서 투여가 가능한 지속형 글리코펩타이드를 통해 새로운 활로를 모색하고 있으며, 입원 기간 단축을 희망하는 보험사에게 매력적인 선택지가 되고 있습니다. 포스마노게픽스 등의 항진균제는 이식 환자들 사이에서 급증하고 있는 아스페르길루스 내성 문제에 대응하고 있습니다. 항기생충제는 현재 3상 임상시험 단계에 있는 3제 병용 요법을 통해 새롭게 발생하는 변이에 대응하고 있습니다.

신규 계열의 감염증 치료제 시장 규모는 현재로서는 여전히 작지만, 파이프라인의 충실도를 고려할 때 규제 당국이 대체 평가 지표를 승인한다면 급속한 성장이 예상됩니다. 성공의 열쇠는 병원체를 확인하는 동반 진단제로, 이를 통해 좁은 스펙트럼의 약물이 적절한 환자에게 확실하게 전달되고, 가치 기반 계약의 대상이 될 수 있도록 보장됩니다. 요컨대, 경쟁은 화학계 항바이러스제에 그치지 않고 정밀한 생물학적 치료법으로 확대되고 있습니다.

지역별 분석

북미는 2025년 매출의 36.20%를 차지하고 있으며, 후기 임상시험을 가속화하는 BARDA의 보조금과 입원을 줄이는 새로운 작용기전의 약물에 대해 보험 적용을 허용하는 보험사의 태도가 이를 뒷받침하고 있습니다. FDA의 신속 심사 제도가 조기 시판을 촉진하는 한편, 캐나다의 우선 심사 바우처 제도를 통해 이 모델이 지역 전체로 확대되고 있습니다. 미국은 여전히 API(유효 성분) 수입 위험에 노출되어 있으며, 국내 발효 공장에 대한 세액 공제를 요구하는 연방 정부의 제안이 추진되고 있습니다. 멕시코가 북미공급망에 임베디드됨에 따라 니어쇼어링을 통한 부담 경감이 이루어지고 있지만, 여전히 대규모 무균 제조 능력이 부족한 실정입니다.

아시아태평양은 규제 현대화와 중산층의 의료비 지출 증가에 힘입어 연평균 성장률(CAGR) 7.28%로 성장할 것으로 전망됩니다. 중국 국가의약품감독관리국(NMPA)은 다른 어떤 규제 당국보다 신속하게 항감염제 신약 승인 신청(NDA)을 승인하고 있으며, 이는 항생제 내성에 대한 정책적 시급성을 보여주고 있습니다. 싱가포르는 박테리오파지 연구 거점에 자금을 지원하고 있는 반면, 한국의 디지털 헬스 생태계는 온라인 항생제 처방을 지원하고 있습니다. 인도는 API 수출국인 동시에 대규모 의약품 소비국이라는 양면성을 지니고 있어, 품질 보증이 전략상 최우선 과제가 되고 있습니다. 세계에서 가장 높은 고령 인구 중앙값을 기록하고 있는 일본은 노인 요양 시설의 감염증 예방 대책에 자금을 투입하고 있으며, 이로 인해 감염증 치료제 시장에 안정적인 수요가 창출되고 있습니다.

유럽에서는 스튜어드십에 기반한 처방량 제한과, 치료 성과 향상이 입증된 고부가가치 치료법의 높은 보급률 사이에서 균형을 맞추고 있습니다. 독일과 영국은 플레밍 이니셔티브에서 볼 수 있듯이, 항생제 내성(AMR)에 관한 기초 연구에 자금을 지원하고 있습니다. EMA(유럽의약품청)과 HERA(유럽의약품청)은 최근 세팔로스포린 부족 사태에 대응하기 위해 재고를 조정하여 공급 부족 위험을 완화하고 있습니다. 동유럽 국가들은 바이오시밀러 항바이러스제의 도입을 촉진하기 위해 조달 규정을 현대화하고 있으며, 이로 인해 지역 내 경쟁이 심화되고 있습니다. 유럽 대륙의 통일된 규제 방침 덕분에 시장 출시 절차가 간소화되어, 기업들은 EU 전역에 걸쳐 단계적으로 사업을 전개할 수 있게 되었으며, 국가별 개별 신청보다 더 효율적으로 감염증 치료제 시장 규모를 확대할 수 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.29According to Mordor Intelligence, the infectious disease drugs market size was valued at USD 189.80 billion in 2025 and is estimated to grow from USD 195.83 billion in 2026 to reach USD 228.95 billion by 2031, at a CAGR of 3.18% during the forecast period (2026-2031).

This report is Segmented by Disease (HIV, Influenza, Hepatitis and More), Treatment Class (Antiviral, Antibacterial, Antiparasitic, and More), Drug Type (Small-Molecule, Biologic/MAb and More), Route of Administration (Oral, Injectable and More), Distribution Channel (Hospital Pharmacies, Retail & Chain Pharmacies and More) Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Infectious Disease Drugs Market Trends and Insights

Growing Prevalence of Infectious Diseases

Drug-resistant pathogens claim around 700,000 lives every year, underscoring a structural demand for better medicines. Tuberculosis now affects 10.8 million people, with resistant strains spreading quickly.Artemisinin-resistant malaria has been confirmed in Rwanda and Tanzania, jeopardizing earlier public-health gains. Surveillance in Uganda shows 11% of children harbor partial resistance to front-line malaria therapy. Aging populations, cancer-related immunosuppression, and climate-shifted vector habitats layer further demand on the infectious disease drugs market. Collectively, these epidemiological pressures sustain mid-single-digit growth for specialized therapies despite stewardship curbs.

AI-Driven Antimicrobial Discovery Platforms

Machine-learning engines now sift chemical libraries in weeks, not years. Eli Lilly's USD 100 million pact with OpenAI illustrates pharma's largest single AI commitment to tackle resistance. CRISPR-optimized phage LBP-EC01 is entering Phase 2 trials with USD 23.9 million in BARDA funding. SNIPR Biome dosed the first volunteers with a genome-edited antibiotic that spares commensal flora. Predictive algorithms flag resistance pathways early, guiding chemists toward compounds less likely to fail in vivo. As platform proof points accumulate, capital flows tilt toward AI-native pipeline builders, reshaping the infectious disease drugs market's innovation map.

Antimicrobial Stewardship Curbing Prescriptions

Hospitals now require pre-authorization for broad-spectrum antibiotics, cutting usage by up to 30% in some systems. Remote telehealth visits, however, escape many controls, prompting fresh audit tools. The European Union blueprint is spreading worldwide, formalizing daily-dose caps and treatment-length ceilings. While stewardship slows units sold, it is catalyzing demand for narrow-spectrum therapies positioned as resistance-sparing, thus reshaping revenue composition inside the infectious disease drugs market.

Other drivers and restraints analyzed in the detailed report include:

- Expanding Funding & R&D Investments

- Accelerated Regulatory Pathways Post-COVID-19

- API Supply-Chain Fragility & Geopolitics

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

HIV therapies held 36.10% of 2025 revenue, giving the infectious disease drugs market a core cash generator that funds riskier pipeline bets. Long-acting cabotegravir-rilpivirine autoinjectors, administered every two months, improved real-world viral suppression rates, lifting lifetime adherence and revenue consistency. In contrast, hepatitis treatments are projected to grow at a 3.98% CAGR, courtesy of bulevirtide's 90% sustained virologic response in hepatitis D trials.Eliminating chronic hepatitis outcomes is a priority for payers aiming to curb organ-transplant costs. Tuberculosis therapies ride policy urgency as PurF inhibitor JNJ-6640 posts potent activity against multidrug-resistant strains. Malaria portfolios focus on triple combination regimens to offset artemisinin resistance documented in East Africa. Influenza antivirals gain from surveillance systems built during COVID-19, while opportunistic infection drugs rise with cancer-therapy-driven immunosuppression.

The hepatitis surge widens therapy choice, attracting regional generic entrants faster than in HIV, yet intellectual-property cliffs in 2028 could reshape pricing. Meanwhile, pipeline assets for tuberculosis and malaria often rely on nonprofit co-funding, implying slower commercialization but high public-health value. For HIV, the challenge is next-generation broadly neutralizing antibodies that aim to cut dosing to twice yearly, a shift with potential to defend market incumbency. Collectively, disease-specific dynamics keep the infectious disease drugs market balanced between cash-rich chronic segments and fast-rising acute segments.

Antivirals generated 40.80% of 2025 revenue, reflecting entrenched HIV and hepatitis franchises. Yet novel phage and CRISPR-enabled treatments are on track for a 5.41% CAGR, racing to clinical proof via adaptive trials that measure rapid microbiological outcomes. Locus Biosciences' LBP-EC01 achieved significant bacterial load reduction in urinary tract infections within 24 hours. Antibacterials find fresh life through long-acting glycopeptides that permit outpatient dosing, appealing to payers eager to cut hospital stays. Antifungals like fosmanogepix address the surge in Aspergillus resistance among transplant recipients. Antiparasitics counter emergent mutations with triple-drug blends now in Phase 3.

The infectious disease drugs market size for novel classes remains small today, yet pipeline density suggests rapid upside as regulators validate surrogate endpoints. Success will depend on companion diagnostics that confirm pathogen identity, ensuring narrow-spectrum agents reach the right patients and qualify for value-based contracts. In short, the competitive field is widening beyond chemical antivirals to include precision biological modalities.

Geography Analysis

North America retained 36.20% of 2025 sales, powered by BARDA grants that expedite late-stage trials and by insurers willing to reimburse novel mechanisms that reduce hospitalization. Accelerated FDA pathways encourage early launch, while Canada's priority review vouchers extend the model region-wide. The United States remains exposed to API import risks, pushing federal proposals for tax credits on domestic fermentation plants. Mexico's inclusion in continental supply chains offers near-shoring relief but still lacks large-scale sterile capacity.

Asia-Pacific is forecast to grow at a 7.28% CAGR, lifted by regulatory modernization and rising middle-class healthcare spend. China's NMPA is clearing anti-infective NDAs faster than any peer agency, showing policy urgency on resistance. Singapore bankrolls bacteriophage hubs, while South Korea's digital health ecosystem supports online antibiotic dispensing. India straddles its role as both API exporter and large therapy consumer, making quality assurance a strategic imperative. Japan, faced with the world's oldest population median, funds infection prophylaxis in elder-care settings, adding steady volume to the infectious disease drugs market.

Europe balances stewardship-driven volume limits with high adoption of premium therapies that prove outcome gains. Germany and the United Kingdom bankroll basic AMR science, exemplified by the Fleming Initiative. EMA and HERA coordinate stockpiles to blunt shortage risk, a response to recent cephalosporin gaps. Eastern European states modernize procurement rules to attract biosimilar antivirals, boosting regional competitive intensity. The continent's unified regulatory stance simplifies launch sequences, allowing companies to stage pan-EU rollouts that lift the infectious disease drugs market size more efficiently than piecemeal national filings.

- Abbvie

- Boehringer Ingelheim

- Gilead Sciences

- GlaxoSmithKline

- Johnson & Johnson

- Merck

- Novartis

- Roche

- Sanofi

- Takeda Pharmaceuticals

- AstraZeneca

- Pfizer

- Cipla

- Viatris

- Dr. Reddy's Laboratories Ltd.

- Hikma Pharmaceuticals

- Sun Pharma Industries Ltd.

- Lupin

- Hookipa Pharma

- Bajaj Healthcare Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Awareness Initiatives By Governments & Ngos

- 4.2.2 Growing Prevalence Of Infectious Diseases

- 4.2.3 Expanding Funding & R&D Investments

- 4.2.4 Accelerated Regulatory Pathways Post-COVID-19

- 4.2.5 Long-Acting Injectables Boosting Adherence

- 4.2.6 AI-Driven Antimicrobial Discovery Platforms

- 4.3 Market Restraints

- 4.3.1 Low Diagnosis & Treatment Penetration In Developing Regions

- 4.3.2 Adverse Side-Effects And Toxicity Profiles

- 4.3.3 Antimicrobial-Stewardship Curbing Prescriptions

- 4.3.4 API Supply-Chain Fragility & Geopolitics

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technology Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value-USD)

- 5.1 By Disease

- 5.1.1 HIV

- 5.1.2 Influenza

- 5.1.3 Hepatitis (A, B, C, D & E)

- 5.1.4 Tuberculosis

- 5.1.5 Malaria

- 5.1.6 Opportunistic & other infections

- 5.2 By Treatment Class

- 5.2.1 Antiviral

- 5.2.2 Antibacterial

- 5.2.3 Antiparasitic

- 5.2.4 Antifungal

- 5.2.5 Novel phage & CRISPR-based therapeutics

- 5.3 By Drug Type

- 5.3.1 Small-molecule

- 5.3.2 Biologic / mAb

- 5.3.3 Vaccine-derived therapeutics

- 5.4 By Route of Administration

- 5.4.1 Oral

- 5.4.2 Injectable (IV, IM, SC)

- 5.4.3 Transdermal & Inhalational

- 5.5 By Distribution Channel

- 5.5.1 Hospital Pharmacies

- 5.5.2 Retail & Chain Pharmacies

- 5.5.3 Online Pharmacies

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 Australia

- 5.6.3.5 South Korea

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East and Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.3.1 AbbVie Inc.

- 6.3.2 Boehringer Ingelheim GmbH

- 6.3.3 Gilead Sciences Inc.

- 6.3.4 GlaxoSmithKline plc

- 6.3.5 Johnson & Johnson

- 6.3.6 Merck & Co., Inc.

- 6.3.7 Novartis AG

- 6.3.8 F. Hoffmann-La Roche Ltd.

- 6.3.9 Sanofi SA

- 6.3.10 Takeda Pharmaceutical Co. Ltd.

- 6.3.11 AstraZeneca plc

- 6.3.12 Pfizer Inc.

- 6.3.13 Cipla Ltd.

- 6.3.14 Viatris Inc.

- 6.3.15 Dr. Reddy's Laboratories Ltd.

- 6.3.16 Hikma Pharmaceuticals PLC

- 6.3.17 Sun Pharma Industries Ltd.

- 6.3.18 Lupin Ltd.

- 6.3.19 Hookipa Pharma Inc.

- 6.3.20 Bajaj Healthcare Ltd.

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment