|

시장보고서

상품코드

2072886

크로모블라스토미코시스 치료 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Chromoblastomycosis Treatment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

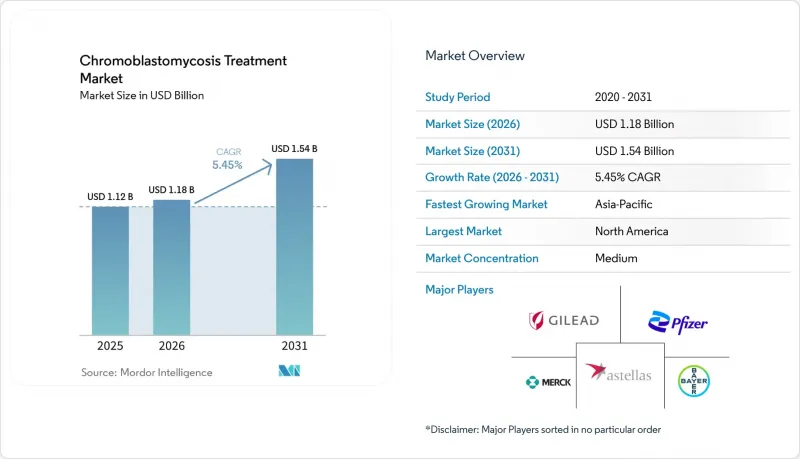

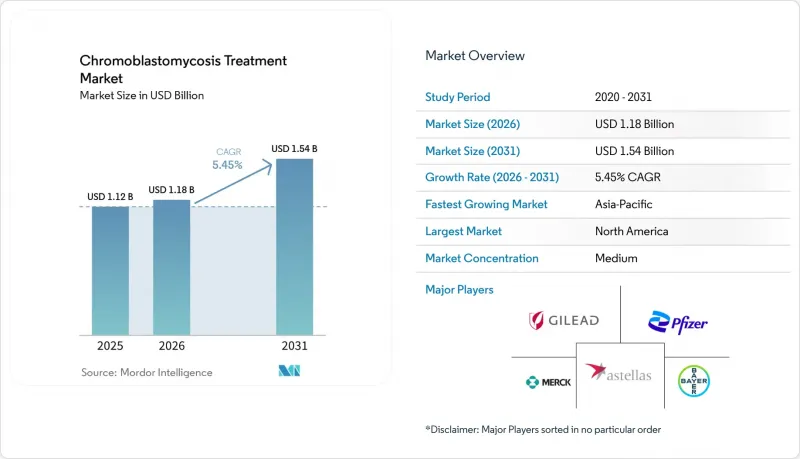

Mordor Intelligence에 의하면, 크로모블라스토미코시스 치료 시장 규모는 2025년 11억 2,000만 달러, 2026년 11억 8,000만 달러에서 2031년까지 15억 4,000만 달러로 확대한다고 예측되고 있어 2026년부터 2031년까지 연평균 복합 성장률(CAGR)은 5.45%를 나타낼 전망입니다.

본 보고서는 치료법별(항진균 요법, 외과적 절제, 냉동 요법, 온열 요법, 병용 요법), 약물 분류별(아졸계, 알릴아민계, 폴리엔계, 보조 요법), 투여 경로별(경구, 외용, 비경구), 최종 사용자(병원, 피부과 클리닉, 전문 의료, 재택치료), 지역(북미, 유럽, 아시아태평양, 기타)별로 분류되어 있습니다. 예상치는 금액(달러)으로 표시되어 있습니다.

전 세계 크로모블라스토미코시스 치료 시장 동향 및 인사이트

장기적인 전신 항진균 요법에 대한 수요 증가

크로모블라스토미코시스 치료 시장은 대부분의 환자에게 장기간의 치료가 필요하다는 점 덕분에 혜택을 보고 있습니다. 표준 치료 기간은 8-36개월이며, 이트라코나졸은 보통 1일 200-400 mg의 용량으로 투여됩니다. 이러한 장기적인 치료 계획으로 인해 환자 1인당 누적 의약품 수요가 크게 증가합니다. 이트라코나졸은 경증부터 중증 사례에 이르기까지 여전히 주요 약제로 사용되고 있지만, 테르비나핀은 병용 요법에서 빈번하게 사용되고 있습니다. 이트라코나졸 단독 요법의 완치율은 15%에서 80% 사이이며, 대부분의 경우 치료 기간 연장, 2차 치료 또는 병용 요법이 필요하기 때문에 시장 수요를 더욱 부추기고 있습니다. 이러한 추세로 인해 소비량이 장기간에 걸쳐 누적되므로, 급성 감염병에 비해 안정적인 수요 패턴이 유지되고 있습니다.

난치성 병변에 대한 병용 요법의 활용 확대

시장에서는 중등도에서 중증의 사례에서 병용 요법으로 전환되는 추세가 나타나고 있습니다. 폰세카-에어-페드로소이 감염증의 경우, 이트라코나졸과 테르비나핀을 병용하면 치료 결과가 개선된다는 것이 밝혀졌습니다. 데발킹, 병변 내 암포테리신 B 투여, 그리고 경구용 테르비나핀을 병용하는 DAT 요법은 표준 치료에 반응하지 않는 환자를 위한 근치적 치료 옵션으로 부상하고 있습니다. 보조적인 광역학 요법의 경우, 6회 시술 후 병변 크기가 80%에서 90%까지 축소된다는 사실이 입증되어, 의료기기를 활용한 치료법의 역할이 커지고 있음이 부각되고 있습니다. 동결 요법, 이트라코나졸, 그리고 외용 5-플루오로우라실을 병용하는 등 다각적인 접근법이 임상적으로 점차 받아들여지고 있으며, 수개월 이내에 병변이 현저하게 소실되는 결과를 보이고 있습니다.

치료 기간의 장기화와 복약 순응도의 저하

크로모블라스토미코시스 치료 시장에서 약물 복용 순응도가 낮은 것은 여전히 큰 과제로 남아 있습니다. 8-36개월에 걸쳐 이트라코나졸을 매일 투여하거나 펄스 요법을 시행할 경우, 비용, 부작용 및 병변의 초기 반응이 더딘 탓에 치료가 중단되는 경우가 종종 있습니다. 치료 중단은 선택압을 유발하며, 연구에 따르면 치료 중인 분리주에서 이트라코나졸의 최소억제농도(MIC)가 상승하는 것으로 나타났는데, 이는 치료 주기의 불완전성으로 인한 내성을 시사합니다. 이로 인해 임상적 성공률이 낮아지고, 1차 치료법의 신뢰성이 떨어집니다. 일반적인 이트라코나졸은 식사의 영향을 쉽게 받는 특성이 있어, 자원이 부족한 환경에서는 더욱 큰 과제가 되고 있습니다. 한편, 이 문제를 해결하기 위해 개발된 초고생체이용률형 이트라코나졸은 많은 유행 지역에서 여전히 가격이 부담스러운 실정입니다.

부문별 분석

2025년, 항진균제 요법은 크로모블라스토미코시스 치료 시장의 58.45%를 차지하고 있으며, 다양한 중증도의 질환을 관리하기 위해 전신용 아졸계 약물 및 알릴아민계 약물에 대한 의존도가 지속되고 있음이 드러났습니다. 여기에는 국소성 증례에 대한 이트라코나졸 단독 요법 및 만성 또는 중증 병변에 대한 복합 경구 투여 요법이 포함됩니다. 단일 요법만으로는 충분하지 않은 경우, 다제 병용이나 다각적인 접근 방식으로의 전환이 촉진요인이 되어, 병용 요법은 2026년부터 2031년까지 연평균 성장률(CAGR) 5.66%를 나타낼 것으로 예측됩니다.

발표된 증거에 따르면, 중등도에서 중증의 사례에서 전신 약물을 냉동 요법, 레이저 치료 또는 병변 내 암포테리신 B와 병용할 경우 치료 결과가 개선되는 것으로 나타났습니다. 또한, 치료가 어려운 병변의 경우 전신용 아졸계 약물과 함께 외용 이미키모드 등의 면역조절제 사용이 증가하고 있어, 감염증 치료와 피부과 치료의 가교 역할을 하고 있습니다. 국소성 증례의 경우, 외과적 절제나 냉동 요법이 여전히 유효하지만, 시장은 의약품을 중심으로 한 병용 요법으로 전환되고 있으며, 물리 요법은 이를 보완하는 선택지로 자리 잡고 있습니다. 예측 기간 동안에는 약물 기반 치료 프로토콜이 시장을 독점할 것으로 예측됩니다.

2025년 기준으로, 아졸계 약제는 크로모블라스토미코시스 치료 시장에서 71.75%의 점유율을 차지하고 있으며, 이는 주요 약물군으로서의 위상을 반영하고 있습니다. 이트라코나졸은 유행 지역에서의 확립된 처방 패턴에 힘입어 여전히 전 세계적으로 1차 치료제로 자리 잡고 있습니다. 주요 2차 치료제인 아졸계 항진균제인 포사코나졸은 크로모블라스토미코시스 및 마이세토마에 대해 규제 당국의 승인을 받았으며, 사례 데이터에 따르면 11명의 환자 중 9명에서 양호한 치료 결과가 나타났습니다.

테르비나핀을 비롯한 알릴아민계 약제는 병용 요법이나 특정 단일 요법에서의 유효성으로 인해 주목받고 있으며, F. pedrosoi 감염증의 경우 12개월 동안 66%의 완전 치유율이 보고되었습니다. 암포테리신 B와 같은 폴리엔계 약물은 독성 우려로 인해 중증 환자에게만 제한적으로 사용되지만, 플루시토신이나 외용 이미키모드 등의 보조 약물은 특정 분야에서 중요한 역할을 하고 있습니다. 약제 용도 전환에 관한 노력을 통해 이트라코나졸과 시너지 효과를 기대할 수 있는 화합물이 확인되었으며, 이는 시장 내 다양화가 서서히 진행되고 있음을 시사하고 있습니다.

지역별 분석

2025년, 북미는 크로모블라스토미코시스 치료 시장에서 38.95%의 점유율을 차지하며, 지역별 최대 기여 지역으로서의 위상을 유지했습니다. 이 지역은 고도의 피부과 의료 인프라, 포사코나졸이나 볼리코나졸과 같은 브랜드 아졸계 약물에 대한 접근성, 그리고 많은 풍토병이 유행하는 저소득 국가 시장에 비해 다제 병용 요법 채택률이 높다는 등의 장점이 있습니다. 미국에는 여행 및 이민 관련 사례를 전문으로 다루는 대학 병원이 존재하기 때문에 이 시장의 가치 대부분을 차지하고 있습니다. 캐나다와 멕시코의 기여도는 비교적 적지만, 멕시코 북부의 반건조 지역에서는 Fonsecaea pedrosoi에 의한 감염 양상이 습윤 지역의 질병과는 다른 모습을 보입니다. 또한 유럽에서도 아프리카나 라틴아메리카 출신 이민자와 관련된 비유행 지역에서의 사례가 증가하고 있어, 전문적인 열대의학 분야 밖에서 적시에 진단하는 데 어려움이 부각되고 있습니다.

아시아태평양은 2026년부터 2031년까지 연평균 성장률(CAGR) 7.88%를 나타낼 것으로 예측되며, 크로모블라스토미코시스 치료 시장에서 가장 빠르게 성장하는 지역이 될 전망입니다. 인도, 중국, 한국 및 동남아시아에서 사례 감지 능력이 향상됨에 따라, 그동안 보고되지 않았던 사례에 대한 대응이 진행되고 있습니다. WHO 자료에 따르면, 2024년까지 아시아에서 1,394건의 사례가 기록되었으며, 그중 인도에서 169건, 일본에서 71건이 보고되었으나, 감시 체계가 불완전하기 때문에 실제 환자 수는 이보다 더 많을 것으로 추정됩니다. 2026년 케랄라주에서 실시된 연구에서는 F. nubica가 주요 균종으로 확인되었으며, 해당 지역에 특화된 치료 접근법의 필요성이 강조되었습니다. 인도의 강력한 제네릭 의약품 부문은 진단 건수 증가에 따라 이트라코나졸과 테르비나핀을 비용 대비 효과가 높은 형태로 공급하고 있습니다.

라틴아메리카는 크로모블라스토미코시스 치료 시장에서 여전히 주요 질병 부담의 중심지이며, 브라질은 전 세계적으로도 가장 많은 환자 수를 기록하는 국가 중 하나입니다. 브라질에서는 침윤성 진균증 대책을 위한 전용 프로그램을 통해 이트라코나졸이 공적으로 공급되고 있기 때문에 공급업체 입장에서는 판매량을 파악하기가 쉬워지지만, 프리미엄 가격 책정에는 제약이 따릅니다. 라틴아메리카 및 카리브해 지역에서 보고된 사례의 84.1%는 Fonsecaea pedrosoi에 의한 것으로, 아시아나 아프리카에 비해 보다 표준화된 치료 프로토콜을 적용할 수 있게 되었습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHSAccording to Mordor Intelligence, the chromoblastomycosis treatment market size is projected to expand from USD 1.12 billion in 2025 and USD 1.18 billion in 2026 to USD 1.54 billion by 2031, registering a CAGR of 5.45% between 2026 to 2031.

This report is Segmented by Treatment Type (Antifungal Therapy, Surgical Excision, Cryotherapy, Thermotherapy, Combination), Drug Class (Azoles, Allylamines, Polyenes, Adjunctive), Route of Administration (Oral, Topical, Parenteral), End User (Hospitals, Dermatology Clinics, Specialty Care, Homecare), and Geography (North America, Europe, Asia-Pacific, and More). Forecasts are in Value (USD).

Global Chromoblastomycosis Treatment Market Trends and Insights

Rising Need for Long-Duration Systemic Antifungal Therapy

The chromoblastomycosis treatment market benefits from the extended therapy durations required by most patients. Standard treatments last 8 to 36 months, with itraconazole typically administered at daily doses of 200 to 400 mg. This prolonged regimen results in significant cumulative drug demand for each patient episode. Itraconazole remains the primary agent for mild to severe cases, while terbinafine is frequently used in combination therapies. Cure rates for itraconazole monotherapy range from 15% to 80%, often necessitating extended treatments, second-line therapies, or combined regimens, further driving market demand. This trend ensures a consistent demand profile compared to acute infections, as consumption builds over extended periods.

Growing Use of Combination Therapy for Refractory Lesions

The market is witnessing a shift toward combination therapies for moderate to severe cases. Evidence shows improved outcomes when itraconazole is paired with terbinafine for Fonsecaea pedrosoi infections. DAT therapy, combining debulking, intralesional amphotericin B, and oral terbinafine, has emerged as a curative option for patients unresponsive to standard treatments. Adjunctive photodynamic therapy has demonstrated an 80% to 90% reduction in lesion size after six applications, highlighting the growing role of device-based modalities. Multi-modal approaches, such as combining cryotherapy, itraconazole, and topical 5-fluorouracil, are gaining clinical acceptance, achieving significant lesion clearance within months.

Long Treatment Duration and Poor Adherence

Poor adherence remains a significant challenge in the chromoblastomycosis treatment market. Daily or pulse itraconazole regimens, lasting 8 to 36 months, often face discontinuation due to costs, side effects, and the slow initial response of lesions. Interrupted therapy creates selective pressure, with studies showing higher itraconazole MICs in isolates during treatment, indicating resistance from incomplete cycles. This reduces clinical success and undermines the reliability of first-line therapy. Standard itraconazole's food-dependent absorption adds to challenges in lower-resource settings, while super-bioavailability itraconazole, developed to address this, remains unaffordable in many endemic areas.

Other drivers and restraints analyzed in the detailed report include:

- Persistent Diagnostic Delay in Endemic Rural Care Pathways

- Public Procurement and Donation Models for Itraconazole

- Limited Clinical Trial Evidence and Standardized Guidelines

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, Antifungal Drug Therapy accounted for 58.45% of the chromoblastomycosis treatment market, highlighting the continued reliance on systemic azoles and allylamines for managing various disease severities. This includes itraconazole monotherapy for localized cases and complex oral regimens for chronic or severe lesions. Combination Therapy is projected to grow at a 5.66% CAGR from 2026 to 2031, driven by a shift toward multi-drug and multi-modal approaches when monotherapy proves insufficient.

Published evidence supports improved outcomes in moderate to severe cases when systemic drugs are combined with cryotherapy, laser treatments, or intralesional amphotericin B. Immunomodulatory agents like topical imiquimod are increasingly used alongside systemic azoles for challenging lesions, bridging infectious disease treatment and dermatology. While surgical excision and cryotherapy remain relevant for localized cases, the market is moving toward pharmaceutical-centered combinations, with physical modalities serving as complementary options. Drug-based protocols are expected to dominate the market during the forecast period.

Azoles held a 71.75% share of the chromoblastomycosis treatment market in 2025, reflecting their position as the leading drug class. Itraconazole remains the global first-line treatment, supported by established prescribing patterns in endemic regions. Posaconazole, the primary second-line azole, has regulatory approval for chromoblastomycosis and mycetoma, with case data showing successful outcomes in 9 of 11 patients.

Allylamines, led by terbinafine, are gaining traction due to their effectiveness in combination therapies and select monotherapy cases, with a 66% complete healing rate reported in F. pedrosoi infections over 12 months. Polyenes like amphotericin B are limited to severe cases due to toxicity concerns, while adjunctive agents such as flucytosine and topical imiquimod hold niche relevance. Drug repurposing efforts are identifying compounds with potential synergy with itraconazole, indicating gradual diversification within the market.

Complete Report Scope:

- By Treatment Type

- Antifungal Drug Therapy

- Surgical Excision

- Cryotherapy

- Thermotherapy

- Combination Therapy

- By Drug Class

- Azoles

- Allylamines

- Polyenes

- Adjunctive Antifungal Agents

- By Route Of Administration

- Oral

- Topical

- Parenteral

- By End User

- Hospitals

- Dermatology Clinics

- Specialty Care Centers

- Homecare And Ambulatory Settings

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Geography Analysis

In 2025, North America held a 38.95% share of the chromoblastomycosis treatment market, maintaining its position as the largest regional contributor. The region benefits from advanced dermatology infrastructure, access to branded azoles like posaconazole and voriconazole, and higher adoption of multi-drug combination protocols compared to many endemic low-income markets. The United States drives most of this value due to its academic medical centers specializing in travel-acquired and immigrant-associated cases. Canada and Mexico contribute smaller volumes, with Mexico's northern semi-arid regions showing distinct infection patterns compared to humid-region diseases caused by Fonsecaea pedrosoi. Europe is also seeing a rise in non-endemic cases linked to migration from Africa and Latin America, highlighting challenges in timely diagnosis outside specialized tropical care.

Asia-Pacific is projected to grow at a 7.88% CAGR from 2026 to 2031, making it the fastest-growing region in the chromoblastomycosis treatment market. Improved case detection in India, China, South Korea, and Southeast Asia is addressing underreported cases. WHO data recorded 1,394 cases in Asia through 2024, including 169 in India and 71 in Japan, though the actual burden is likely higher due to incomplete surveillance. A 2026 study from Kerala identified F. nubica as the predominant species, emphasizing the need for region-specific treatment approaches. India's strong generic pharmaceutical sector provides a cost-effective supply of itraconazole and terbinafine as diagnoses increase.

Latin America remains the primary disease-burden center in the chromoblastomycosis treatment market, with Brazil accounting for one of the largest national caseloads globally. Brazil's public provision of itraconazole through a dedicated implantation mycoses program offers suppliers better volume visibility but limits premium pricing. Fonsecaea pedrosoi caused 84.1% of registered cases in Latin America and the Caribbean, enabling more standardized treatment protocols compared to Asia or Africa.

- Astellas Pharma

- Aurobindo Pharma

- Bayer

- Cipla

- Dr. Reddys Laboratories Limited

- Gilead Sciences

- Glenmark Pharmaceuticals

- GlaxoSmithKline

- Hikma Pharmaceuticals

- Johnson & Johnson

- Merck

- Mycovia Pharmaceuticals

- Novartis

- Pfizer

- Sanofi

- SCYNEXIS

- Sun Pharmaceuticals Industries

- Teva Pharmaceutical Industries

- Viatris

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Need for Long-Duration Systemic Antifungal Therapy

- 4.2.2 Persistent Diagnostic Delay in Endemic Rural Care Pathways

- 4.2.3 Public Procurement and Donation Models for Itraconazole Access

- 4.2.4 Growing Use of Combination Therapy for Refractory Lesions

- 4.2.5 Underuse of Species-Level Identification and Antifungal Susceptibility Testing

- 4.2.6 Scarcity of Affordable Newer Triazoles in Endemic Markets

- 4.3 Market Restraints

- 4.3.1 Long Treatment Duration and Poor Adherence

- 4.3.2 Limited Clinical Trial Evidence and Standardized Guidance

- 4.3.3 Low Commercial Incentive Due to Disease Neglect and Regional Concentration

- 4.3.4 Limited Access to Diagnostics and Specialist Dermatology Care

- 4.4 Value/Supply Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE, USD)

- 5.1 By Treatment Type

- 5.1.1 Antifungal Drug Therapy

- 5.1.2 Surgical Excision

- 5.1.3 Cryotherapy

- 5.1.4 Thermotherapy

- 5.1.5 Combination Therapy

- 5.2 By Drug Class

- 5.2.1 Azoles

- 5.2.2 Allylamines

- 5.2.3 Polyenes

- 5.2.4 Adjunctive Antifungal Agents

- 5.3 By Route Of Administration

- 5.3.1 Oral

- 5.3.2 Topical

- 5.3.3 Parenteral

- 5.4 By End User

- 5.4.1 Hospitals

- 5.4.2 Dermatology Clinics

- 5.4.3 Specialty Care Centers

- 5.4.4 Homecare And Ambulatory Settings

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.3.1 Astellas Pharma Inc.

- 6.3.2 Aurobindo Pharma Limited

- 6.3.3 Bayer AG

- 6.3.4 Cipla Limited

- 6.3.5 Dr. Reddys Laboratories Limited

- 6.3.6 Gilead Sciences, Inc.

- 6.3.7 Glenmark Pharmaceuticals Limited

- 6.3.8 GSK plc

- 6.3.9 Hikma Pharmaceuticals PLC

- 6.3.10 Johnson & Johnson

- 6.3.11 Merck & Co., Inc.

- 6.3.12 Mycovia Pharmaceuticals, Inc.

- 6.3.13 Novartis AG

- 6.3.14 Pfizer Inc.

- 6.3.15 Sanofi

- 6.3.16 SCYNEXIS, Inc.

- 6.3.17 Sun Pharmaceutical Industries Limited

- 6.3.18 Teva Pharmaceutical Industries Limited

- 6.3.19 Viatris Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment