|

시장보고서

상품코드

2066574

농업용 생물제제 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Agricultural Biologicals - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

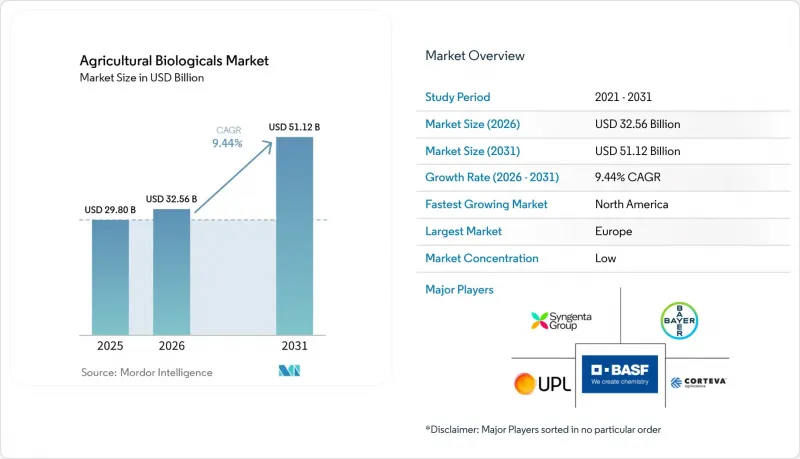

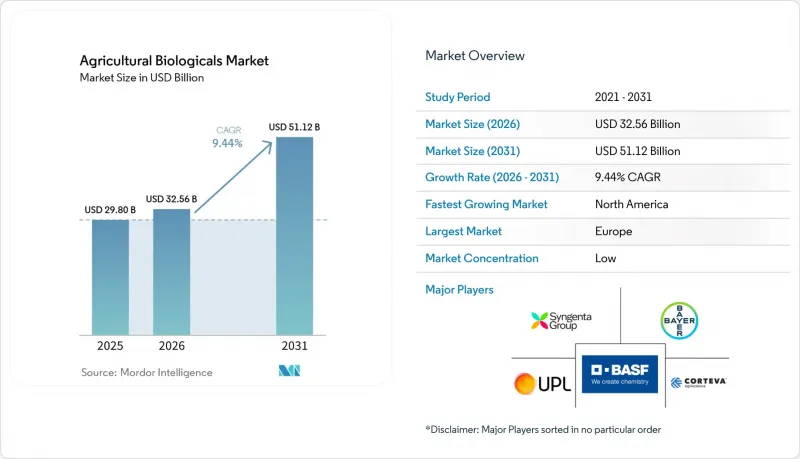

Mordor Intelligence에 의하면, 농업용 생물제제 시장 규모는 2025년 298억 달러로 평가되었습니다. 2026년에는 325억 6,000만 달러, 2031년까지 511억 2,000만 달러에 이를 것으로 예상되며 2026년부터 2031년에 걸쳐 CAGR 9.44%를 기록할 전망입니다.

본 보고서는 기능별(작물 영양 및 작물 보호), 작물 유형별(밭작물, 원예작물, 현금작물), 지역별(북미, 남미, 유럽, 아시아태평양, 중동 및 아프리카)로 분류되어 있습니다. 시장 전망은 금액(달러) 및 수량(미터톤) 단위로 제시되어 있습니다.

세계의 농업용 생물제제 시장 동향 및 인사이트

유기농 및 잔류물 없는 농산물에 대한 수요 증가

주요 생산 지역에서 유기 농업 및 잔류물을 고려한 농업 시스템의 도입이 진행되고 있어, 농업용 생물제제 시장이 성장하고 있습니다. ‘인도의 유기농업 성장’이라는 제목의 조사에 따르면, 인도의 유기농 재배 면적은 2024년에 약 730만 헥타르에 달했습니다. 이는 20년 전의 50만 헥타르에 비해 대폭 증가한 수치이며, 2024년 이 나라에는 230만 명 이상의 유기농 농가가 존재하고 있어, 지속 가능한 농업 관행이 급속히 확대되고 있음을 여실히 보여주었습니다. 이러한 성장은 잔류물이 없는 농업을 촉진하는 생물 유래 작물 보호 및 토양 개량 제품에 대한 수요를 이끌고 있습니다. 또한, 소매업체와 가공업체의 조달 요건에 따라 잔류물이 없는 농산물의 조달 범위가 유기 인증을 받은 유통 경로를 넘어 확대되고 있으며, 기존의 농업 관행에도 생물 유래 자재가 도입되면서 시장 수요가 더욱 확대되고 있습니다.

합성 농약의 잔류물 및 성분에 대한 규제 강화

농업용 생물제제 시장은 기존 살충제 사용에 대한 규제 준수 요건의 강화와 생물제제 승인 절차의 효율화 덕분에 성장세를 보이고 있습니다. 유럽에서는 유럽집행위원회가 2025년 12월, 생물학적 방제 제품에 대한 잠정적인 국내 승인을 통해 개발 기업이 시장 출시 지연으로 인한 손실을 연간 2,200만 유로(2,350만 달러) 절감할 수 있을 것이라고 발표했습니다. 이러한 움직임에 힘입어 농업용 생물제제 시장에서 신제품 출시의 경제적 타당성이 높아지고 있습니다. 이러한 규제 절차가 효율화됨에 따라, 시장 내 투자 결정은 규제상의 장벽을 낮추면서도 보다 신속하게 상품화할 수 있는 생물제제 파이프라인을 점점 더 우선시할 것으로 예측됩니다.

많은 제제에서 나타나는 짧은 유통기한과 콜드체인에 대한 의존도

농업용 생물제제 시장은 많은 미생물 제제와 생체 제제가 부적절한 보관 및 운송 조건으로 인해 효능을 상실하기 때문에 유통 측면에서 현저한 과제에 직면해 있습니다. 2025년 『Journal of Crop Health』에 게재된 연구에 따르면, Aphidius colemani의 부화율은 통제된 조건에서는 84.4%였으나, 96시간 동안 냉장 보관한 후에는 34.8%로 떨어진 것으로 나타났습니다. 마찬가지로, Orius laevigatus 개체군도 168시간 후에 83.97%에서 22.12%로 감소하여 생존 능력이 급격히 저하된 것으로 나타났습니다. 이 문제는 남아시아, 동남아시아, 사하라 이남 아프리카 등의 지역에서 특히 심각합니다. 이러한 지역에서는 농업용 생물제제 시장의 보급 가능성이 높지만, 라스트 마일 단계의 콜드체인 인프라 미비로 인해 그 보급이 저해되고 있습니다.

부문별 분석

2025년, 작물 영양 부문의 농업용 생물제제 시장 점유율은 64.0%로 가장 높은 비중을 차지했습니다. 이는 상업 농업 시스템 전반에 걸쳐 바이오 비료, 바이오 자극제 및 유기 영양 관리 프로그램의 도입이 확대되고 있는 데 힘입은 것입니다. 농가들은 작업 방식을 대폭 변경할 필요 없이 영양분 흡수 효율, 토양 미생물 활성 및 비생물적 스트레스 내성을 높일 수 있기 때문에 기존 농법에 바이오 영양 자재를 점점 더 많이 도입하고 있습니다. 특히, 지속 가능한 농업 관행과 잔여물 관리가 구매 결정에 영향을 미치는 중요한 요소로 작용하는 밭작물 및 원예 생산 분야에서 수요가 견조합니다. 또한, 이러한 제품들이 기존의 비료 프로그램과 호환된다는 점도 대규모 농업 경영에서 더 폭넓은 수용을 촉진하고 있습니다.

작물 보호 부문에서 농업용 생물제제 시장 규모는 2026년부터 2031년까지 9.5%라는 가장 높은 예측 연평균 성장률(CAGR)을 보일 것으로 전망됩니다. 이는 내성 관리나 잔류물에 대한 고려가 필요한 작물 시스템에서 생물학적 솔루션의 활용 확대에 힘입은 결과입니다. 규제 감시가 강화되는 가운데, 생산자들이 합성 화학 물질을 대체할 대안을 모색함에 따라 생물학적 살균제, 생물학적 살충제 및 생물학적 살선충제가 종합 해충 관리 프로그램에 점점 더 많이 도입되고 있습니다. 또한, 일부 생물 유래 제품이 식물의 방어 반응과 스트레스 관리 모두를 지원하기 때문에 작물 영양과 작물 보호 기능 간의 중복도 증가하고 있습니다. 이러한 융합은 농업용 생물제제 업계 전반의 제품 개발 전략, 포트폴리오 포지셔닝 및 상업적 파트너십에 영향을 미치고 있습니다.

지역별 분석

2025년, 유럽은 전 세계 매출의 34%를 차지하며 가장 큰 점유율을 기록했습니다. 이는 더욱 엄격해진 지속가능성 정책, 잔류 기준, 그리고 기존 작물 보호 제품에 대한 규제 압박으로 인해 모든 농업 시스템에서 생물제제의 도입이 지속적으로 촉진되고 있기 때문입니다. 지역적 수요는 지속 가능한 농업의 목표와 식품 공급망의 요건이 일치함으로써 더욱 뒷받침되고 있습니다. 2025년 11월, 유럽의회는 승인 절차의 합리화 및 생물제제에 관한 상호 승인 체계 강화 등을 담은 생물학적 방제제의 등록과 보급을 가속화하는 결의안을 채택했습니다. 이러한 정책 방향은 유럽 농업 전반에서 생물제제의 상용화 기회를 뒷받침하고 있습니다.

북미에서는 생물제제의 등록 확대, 유기농업 전환 이니셔티브, 그리고 기존 작물 재배 프로그램에 생물제제를 통합하는 움직임이 진행되고 있는 것을 배경으로, 2026년부터 2031년에 걸쳐 11.8%라는 가장 높은 연평균 성장률(CAGR)을 달성할 것으로 예측됩니다. 미국은 농가들이 내성 관리, 토양 건강 개선, 잔류물 저감 전략을 위해 생물 유래 자재를 채택하고 있기 때문에 해당 지역에서 계속해서 가장 큰 기여를 하는 국가로 자리매김하고 있습니다. 또한, 통합 해충 관리(IPM) 시스템과의 호환성을 요구하는 특산 작물 및 줄 재배 작물 생산자들 사이에서도 상업적 수요가 증가하고 있습니다. 발효 인프라, 제제 기술 및 대규모 생물 유래 제품 생산에 대한 민간 부문의 강력한 투자가 지역 내 시장 경쟁과 제품의 접근성을 더욱 높이고 있습니다.

남미에서는 특히 브라질과 아르헨티나를 중심으로 대규모 농업 생산 시스템에서 생물 유래 투입제의 도입이 확대되고 있으며, 그 입지를 확고히 다지고 있습니다. 브라질은 여전히 이 지역의 성장 중심지이며, 대두, 옥수수, 사탕수수, 원예작물 재배 프로그램에 생물 유래 자재가 점점 더 많이 도입되고 있습니다. 2025년, 브라질에서는 162종의 생물 유래 자재 제품이 승인되었으며, 이는 해당 국가에서 역대 최다 연간 승인 건수를 기록한 것으로, 농업 분야에서의 생물 유래 솔루션의 급속한 상용화를 입증하는 결과였습니다. 백신 및 생물 유래 작물 보호제의 보급 확대는 광대한 농지를 보유한 농업 시스템 전반에 걸쳐 이러한 제품의 채택을 더욱 촉진하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도와 주요 업계 동향

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.29According to Mordor Intelligence, the agricultural biologicals market size is projected to grow from USD 29.80 billion in 2025 to USD 32.56 billion in 2026 and USD 51.12 billion by 2031, registering a CAGR of 9.44% from 2026 to 2031.

This report is Segmented by Function (Crop Nutrition and Crop Protection), by Crop Type (Row Crops, Horticultural Crops, and Cash Crops), and by Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Value (USD) and Volume (Metric Tons).

Global Agricultural Biologicals Market Trends and Insights

Rising Demand for Organic and Residue-Free Produce

The agricultural biologicals market is growing due to the rising adoption of organic and residue-sensitive farming systems in major production regions. According to the study published in "Growth of Organic Farming in India," the area under organic cultivation in India reached approximately 7.3 million hectares in 2024, compared to 0.5 million hectares two decades ago, and the country had over 2.3 million organic farmers in 2024, highlighting the rapid expansion of sustainable agricultural practices. This growth is driving demand for biological crop protection and soil enhancement products that facilitate residue-free farming. Furthermore, retailer and processor purchasing requirements are extending residue-free sourcing beyond certified organic channels, incorporating biological inputs into conventional farming practices, and broadening market demand.

Stricter Regulations on Synthetic Agrochemical Residues and Ingredients

The agricultural biologicals market is benefiting from stricter compliance regulations on conventional insecticide usage and streamlined approval processes for biological products. In Europe, the European Commission announced in December 2025 that provisional national authorizations for biocontrol products could save developers EUR 22 million (USD 23.5 million) annually in delayed marketing losses . This development enhances the economic feasibility of product launches in the agricultural biologicals market. As these regulatory processes become more efficient, investment decisions within the market are projected to increasingly favor biological pipelines that can be commercialized more rapidly and with reduced regulatory hurdles.

Short Shelf Life and Cold-Chain Dependence of Many Formulations

The agricultural biologicals market faces a notable distribution challenge, as many microbial and living-agent formulations lose effectiveness under suboptimal storage and transportation conditions. Research published in the 2025 Journal of Crop Health indicated that the emergence rates for Aphidius colemani dropped from 84.4% under controlled conditions to 34.8% after 96 hours of refrigeration. Similarly, Orius laevigatus populations declined from 83.97% to 22.12% after 168 hours, demonstrating a rapid loss of viability . This issue is particularly significant in regions such as South Asia, Southeast Asia, and Sub-Saharan Africa, where the agricultural biologicals market has strong adoption potential but is hindered by inadequate cold-chain infrastructure at the last mile.

Other drivers and restraints analyzed in the detailed report include:

- Growing Use of Biologicals in Integrated Pest Management

- Regenerative Agriculture Incentives and Carbon Insetting Programs

- Complex and Non-Harmonized Registration Pathways

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The agricultural biologicals market share for the crop nutrition segment held the largest 64.0% in 2025, supported by the rising adoption of biofertilizers, biostimulants, and organic nutrient management programs across commercial farming systems. Farmers are increasingly integrating biological nutrition inputs into conventional agronomy practices due to their ability to enhance nutrient uptake efficiency, soil microbial activity, and abiotic stress tolerance without requiring significant operational changes. Demand is particularly robust in row crops and horticultural production, where sustainable farming practices and residue management are key factors influencing purchasing decisions. Additionally, the compatibility of these products with existing fertilizer programs supports their broader acceptance in large-scale farming operations.

The agricultural biologicals market size for the crop protection segment recorded the fastest projected CAGR at 9.5% from 2026 to 2031. driven by expanding use of biological solutions in resistance management and residue-sensitive crop systems. Biological fungicides, bioinsecticides, and bionematicides are increasingly incorporated into integrated pest management programs as growers seek alternatives to synthetic chemistries facing tighter regulatory scrutiny. The overlap between crop nutrition and crop protection functions is also increasing, because several biological products support both plant defense responses and stress management. This convergence is influencing product development strategies, portfolio positioning, and commercial partnerships throughout the agricultural biologicals industry.

Geography Analysis

Europe accounted for the largest 34% share of global revenue in 2025 because stricter sustainability policies, residue standards, and regulatory pressure on conventional crop protection products continue encouraging biological adoption across farming systems. Regional demand is further supported by the alignment between sustainable agriculture objectives and food supply chain requirements. In November 2025, the European Parliament adopted a resolution to accelerate the registration and uptake of biological control agents, including streamlined authorization procedures and enhanced mutual recognition frameworks for biological products. This policy direction is bolstering commercialization opportunities for biological inputs across European agriculture.

North America is projected to achieve the fastest CAGR of 11.8% from 2026 to 2031, supported by expanding biological registrations, organic transition initiatives, and increasing integration of biological products into conventional crop programs. The United States remains the largest contributor in the region, as growers adopt biological inputs for resistance management, soil health improvement, and residue reduction strategies. Commercial demand is also increasing among specialty crop and row crop producers seeking compatibility with integrated pest management systems. Strong private-sector investments in fermentation infrastructure, formulation technologies, and large-scale biological manufacturing are further enhancing regional market competitiveness and product availability.

South America continues to solidify its position through the growing adoption of biological inputs in large-scale agricultural production systems, particularly in Brazil and Argentina. Brazil remains the regional growth hub, with biological inputs increasingly integrated into soybean, corn, sugarcane, and horticultural cultivation programs. In 2025, Brazil approved 162 bio-input products, marking the highest annual level recorded in the country and reinforcing the rapid commercialization of biological solutions in agriculture. The wider use of inoculants and biological crop protection products is further driving adoption across large-acre farming systems.

- Corteva Agriscience

- BASF SE

- Bayer AG

- Syngenta Group

- UPL Limited

- Novonesis A/S

- Koppert Biological Systems B.V.

- Valent BioSciences LLC

- FMC Corporation

- Rovensa S.A.

- Certis USA LLC

- Andermatt Biocontrol AG

- Yara International ASA

- Futureco Bioscience S.A.

- Verdesian Life Sciences LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE AND KEY INDUSTRY TRENDS

- 4.1 Area Under Organic Cultivation

- 4.2 Per Capita Spending On Organic Products

- 4.3 Regulatory Framework

- 4.3.1 Argentina

- 4.3.2 Australia

- 4.3.3 Brazil

- 4.3.4 Canada

- 4.3.5 China

- 4.3.6 Egypt

- 4.3.7 France

- 4.3.8 Germany

- 4.3.9 India

- 4.3.10 Indonesia

- 4.3.11 Italy

- 4.3.12 Japan

- 4.3.13 Mexico

- 4.3.14 Netherlands

- 4.3.15 Nigeria

- 4.3.16 Philippines

- 4.3.17 Russia

- 4.3.18 South Africa

- 4.3.19 Spain

- 4.3.20 Thailand

- 4.3.21 Turkey

- 4.3.22 United Kingdom

- 4.3.23 United States

- 4.3.24 Vietnam

- 4.4 Value Chain Analysis and Distribution Channel Analysis

- 4.5 Market Drivers

- 4.5.1 Rising demand for organic and residue-free produce

- 4.5.2 Stricter regulations on synthetic agrochemical residues and ingredients

- 4.5.3 Growing use of biologicals in integrated pest management

- 4.5.4 Regenerative agriculture incentives and carbon insetting programs

- 4.5.5 Artificial intelligence (AI)-enabled microbial strain discovery and formulation optimization

- 4.5.6 Localized fermentation and on-farm bio-input manufacturing models

- 4.6 Market Restraints

- 4.6.1 Short shelf life and cold-chain dependence of many formulations

- 4.6.2 Complex and non-harmonized registration pathways

- 4.6.3 Proliferation of counterfeit and sub-standard products

- 4.6.4 Volatile seaweed and other biological feedstock supply

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

- 5.1 By Function

- 5.1.1 Crop Nutrition

- 5.1.1.1 Biofertilizers

- 5.1.1.1.1 Azospirillum

- 5.1.1.1.2 Azotobacter

- 5.1.1.1.3 Mycorrhiza

- 5.1.1.1.4 Phosphate Solubilizing Bacteria

- 5.1.1.1.5 Rhizobium

- 5.1.1.1.6 Other Biofertilizers

- 5.1.1.2 Biostimulants

- 5.1.1.2.1 Amino Acids

- 5.1.1.2.2 Fulvic Acid

- 5.1.1.2.3 Humic Acid

- 5.1.1.2.4 Protein Hydrolysates

- 5.1.1.2.5 Seaweed Extracts

- 5.1.1.2.6 Other Biostimulants

- 5.1.1.3 Organic Fertilizer

- 5.1.1.3.1 Manure

- 5.1.1.3.2 Meal Based Fertilizers

- 5.1.1.3.3 Oilcakes

- 5.1.1.3.4 Other Organic Fertilizers

- 5.1.1.1 Biofertilizers

- 5.1.2 Crop Protection

- 5.1.2.1 Biocontrol Agents

- 5.1.2.1.1 Macrobials

- 5.1.2.1.2 Microbials

- 5.1.2.2 Biopesticides

- 5.1.2.2.1 Biofungicides

- 5.1.2.2.2 Bioherbicides

- 5.1.2.2.3 Bioinsecticides

- 5.1.2.2.4 Other Biopesticides

- 5.1.2.1 Biocontrol Agents

- 5.1.1 Crop Nutrition

- 5.2 By Crop Type

- 5.2.1 Row Crops

- 5.2.2 Horticultural Crops

- 5.2.3 Cash Crops

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.1.4 Rest of North America

- 5.3.2 South America

- 5.3.2.1 Brazil

- 5.3.2.2 Argentina

- 5.3.2.3 Rest of South America

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Spain

- 5.3.3.5 Italy

- 5.3.3.6 Netherlands

- 5.3.3.7 Russia

- 5.3.3.8 Turkey

- 5.3.3.9 Rest of Europe

- 5.3.4 Asia-Pacific

- 5.3.4.1 China

- 5.3.4.2 India

- 5.3.4.3 Japan

- 5.3.4.4 Australia

- 5.3.4.5 Vietnam

- 5.3.4.6 Thailand

- 5.3.4.7 Indonesia

- 5.3.4.8 Philippines

- 5.3.4.9 Rest of Asia-Pacific

- 5.3.5 Middle East

- 5.3.5.1 Iran

- 5.3.5.2 Saudi Arabia

- 5.3.5.3 Rest of Middle East

- 5.3.6 Africa

- 5.3.6.1 South Africa

- 5.3.6.2 Nigeria

- 5.3.6.3 Egypt

- 5.3.6.4 Rest of Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Corteva Agriscience

- 6.4.2 BASF SE

- 6.4.3 Bayer AG

- 6.4.4 Syngenta Group

- 6.4.5 UPL Limited

- 6.4.6 Novonesis A/S

- 6.4.7 Koppert Biological Systems B.V.

- 6.4.8 Valent BioSciences LLC

- 6.4.9 FMC Corporation

- 6.4.10 Rovensa S.A.

- 6.4.11 Certis USA LLC

- 6.4.12 Andermatt Biocontrol AG

- 6.4.13 Yara International ASA

- 6.4.14 Futureco Bioscience S.A.

- 6.4.15 Verdesian Life Sciences LLC