|

시장보고서

상품코드

2066588

고대역폭 메모리 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)High Bandwidth Memory - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

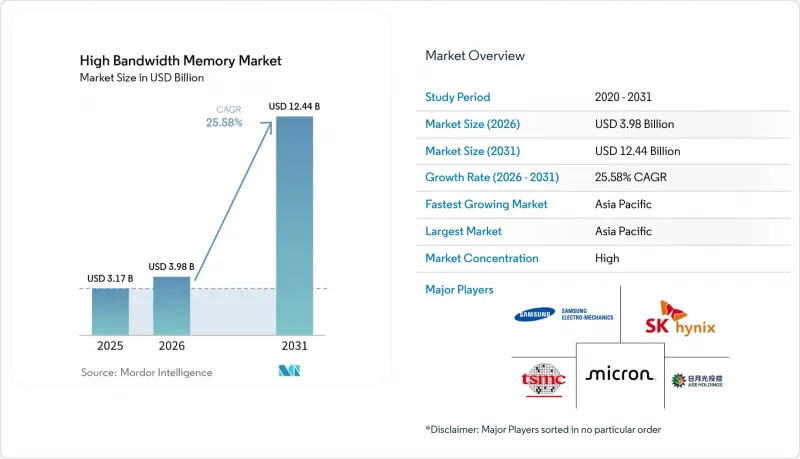

Mordor Intelligence에 의하면, 고대역폭 메모리 시장 규모는 2025년 31억 7,000만 달러에서 2026년에는 39억 8,000만 달러로 확대되어 2031년까지 124억 4,000만 달러에 이를 것으로 예상되고 있어 2026년부터 2031년까지 CAGR 25.58%로 성장할 전망입니다.

본 보고서는 용도별(서버, 네트워크, 고성능 컴퓨팅, 소비자용 전자기기, 자동차 및 운송), 기술별(HBM2, HBM2E, HBM3, HBM3E, HBM4), 스택당 메모리 용량별(4GB, 8 GB, 16GB, 24GB 및 그 이상), 프로세서 인터페이스별(GPU, CPU, AI 가속기/ASIC, FPGA 및 기타 인터페이스), 그리고 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계 고대역폭 메모리 시장 동향 및 분석

AI 서버의 보급과 GPU 탑재율

기업들은 1조 개 이상의 매개변수를 가진 트랜스포머 모델을 처리하기 위해, 노드당 4-8개의 HBM 스택이 필요한 GPU 고밀도 서버로 전환하고 있습니다. 델 테크놀로지스는 2025 회계연도에 AI 최적화 서버 매출이 전년 대비 80% 증가했다고 보고했으며, 이는 기존 OEM 제조업체들이 이러한 전환을 통해 얼마나 큰 이익을 얻고 있는지를 보여줍니다. 비트코인 채굴업체에서 AI 서비스 제공업체로 전환한 IREN과 같은 비전통적인 구매자들은 각각 141GB의 HBM3E를 탑재한 엔비디아 H200 GPU 2만 대를 발주했으며, 이로써 대역폭 수요가 다양한 산업 분야로 확대되고 있음이 확인되었습니다. 모델 규모가 확대됨에 따라 메모리와 연산 비율은 지속적으로 증가하고 있으며, HBM 공급업체 입장에서는 향후 수년에 걸친 수요 전망이 확고해지고 있습니다. HBM2E에서 HBM3E로의 세대 교체로 인해 스택당 대역폭은 50% 향상되었지만, 개발자들은 이미 2027년 출시될 하드웨어에 HBM4를 지정하고 있어 제품 수명 주기가 단축되고, 연구 개발의 중복이 불가피한 상황입니다. 그 결과, DRAM 제조업체들은 GPU 공급업체들이 당초 예상했던 것보다 시스템 부품 원가(BOM)에서 차지하는 비중을 확대되고 있습니다.

데이터센터에서의 DDR5 및 2.5D 패키징으로의 전환

DDR4에서 DDR5로의 전환을 통해, 기판 제조업체와 조립 제조업체는 멀티 기가헤르츠 신호 전송에 익숙해지게 되었으며, HBM 인증과 관련된 인식상의 위험이 감소했습니다. 2025년 말까지 DDR5 모듈은 서버용 DRAM 출하량의 절반 이상을 차지하게 될 것이며, 6.4GT/s 인터페이스의 열 설계에 대한 학습 곡선은 HBM 패키징에 직접적인 이점을 가져다주고 있습니다. TSMC의 ‘Chip-on-Wafer-on-Substrate(COWS)’ 공정에서는 로직 다이와 메모리 다이 사이에 수천 개의 마이크로 범프를 배선하고 있으며, 이 기술은 기존의 2.5-D FPGA(Field-Programmable Gate Array)에서 발전한 것입니다. 제조 기술의 성숙도가 높아짐에 따라 HBM의 가격 프리미엄은 범용 DRAM 대비 10배에서 약 4배로 축소되었으며, 하이퍼스케일 AI를 넘어 고성능 컴퓨팅 및 프리미엄 그래픽 카드 분야로의 채택이 확대되고 있습니다. 표준화 기구는 상호 운용성을 규정하고, 벤더 종속성을 방지하며, 여러 컴퓨팅 분야에서 고대역폭 메모리(HBM)의 보급을 가속화하고 있습니다.

CoWoS/SoIC의 첨단 패키징 생산 능력 제약

TSMC의 CoWoS 및 SoIC 생산 라인은 2025년 말까지 월간 약 12만 장의 웨이퍼 생산 능력에 도달했으나, 2026년 생산량의 절반 이상을 엔비디아(Nvidia)가 단독으로 확보하고 있습니다. ASE, Amkor, JCET가 제시한 단기적인 대안으로 팬아웃(fan-out) 및 실리콘 브리지(silicon bridge) 옵션이 제공되고 있지만, 이러한 공정은 수율 및 고객 인증 측면에서 뒤처져 있어 중견 칩 설계 기업들은 검증 주기의 장기화와 성능 저하를 감수할 수밖에 없는 상황에 처해 있습니다. TSMC는 2026 회계연도에 440억-500억 달러 규모의 설비 투자 중 일부를 애리조나주 내 새로운 패키징 생산 능력 확충에 투입했으나, 단기적인 공급은 여전히 유연성이 부족한 실정입니다. 그 결과, 2028년까지의 고대역폭 메모리(HBM) 시장 성장에 있어 제약 요인은 웨이퍼 투입량이 아니라 패키징 생산 능력이며, 다중 공급원 전략을 채택한 고객들이 우선적인 할당량을 확보하고 있습니다.

부문별 분석

2025년 총 매출액 중 서버가 67.80%를 차지하며, 31억 7,000만 달러에 달하는 고대역폭 메모리 시장 규모를 지탱하는 핵심 요소로 자리 잡고 있습니다. 하이퍼스케일 데이터센터에서는 GPU 1대당 4-8개의 HBM 스택이 도입되어 있으며, 이는 연간 수백 페타바이트 규모의 잠재적 수요에 해당합니다. 800Gb 이더넷 라인 카드 등의 네트워크 장비는 초저지연 요건을 충족하기 위해 HBM을 채택하고 있지만, 매출에서 차지하는 비중은 극히 미미합니다. 고성능 컴퓨팅 센터에서는 메모리 제약이 있는 알고리즘의 솔루션 구현 시간을 단축하기 위해 HBM2E에서 HBM3E로의 전환이 진행되고 있습니다.

자동차용 플랫폼은 가장 빠르게 성장하고 있는 분야로, HBM이 통합된 단일 SoC 상에서 센서 융합 및 경로 계획이 통합됨에 따라 연평균 성장률(CAGR) 26.58%로 확대되고 있습니다. NVIDIA의 ‘Drive Thor’는 패키지에 내장된 HBM을 통해 2,000 TOPS를 구현하며, 시간당 약 1 TB의 센서 데이터를 처리합니다. 프리미엄급 소비자용 그래픽 카드에는 여전히 적층형 DRAM이 채택되고 있지만, 비용 효율을 중시하는 SKU의 경우 게임 워크로드의 대역폭 제약이 비교적 적기 때문에 GDDR이 선호되고 있습니다. 전략적 측면에서 볼 때, 자동차 분야의 설계 채택 기간이 길어지고 엄격한 안전 인증 요건이 더해지면서, 하이퍼스케일 분야의 제품 업데이트 주기가 가져오는 것보다 더 높은 이익률을 창출하고 있다는 것입니다.

HBM3는 고성능 컴퓨팅 및 AI 용도에서의 광범위한 채택에 힘입어 2025년 매출의 45.70%를 차지했습니다. 그러나 공급업체들이 3 TB/s를 초과하는 성능을 갖춘 12층 스택의 인증을 잇달아 진행하고 있는 만큼, HBM3E가 26.43%의 성장률로 시장을 주도할 것으로 예측됩니다. 이러한 첨단 스택은 대역폭을 대폭 향상시켜, 가속기 1대당 필요한 패키지 수를 줄여줍니다. 그 결과, 인터포저의 면적이 최소화되어 전반적인 수율이 향상됩니다. 한편, HBM2 및 HBM2E는 꾸준히 감소하는 추세를 보이고 있으며, 현재 그 사용은 주로 네트워크 및 구형 컴퓨팅 시스템으로 제한되어 있습니다.

HBM4의 샘플 출하는 2025년 초에 시작되어, 메모리 기술 분야에서 중요한 이정표가 되었습니다. SK하이닉스가 최초로 12층 모듈을 출하했고, 삼성도 몇 달 뒤 이를 뒤따랐습니다. HBM4의 사양은 매우 뛰어나며, 핀당 10 Gb/s 이상, 스택 대역폭은 2 TB/s를 초과합니다. 또한, HBM4는 HBM3E에 비해 에너지 효율이 40% 향상되어 차세대 용도에 있어 매우 매력적인 선택지가 되고 있습니다. 2026년부터 양산으로 전환될 것으로 예상되며, 이에 따라 2020년대 말까지 매출 구성비가 HBM4로 이동하는 추세가 가속화될 가능성이 있습니다. 또한, 이러한 발전은 2028년부터 2029년까지 등장할 것으로 예상되는 포토닉스 지원 HBM 변형 제품의 길을 열어줄 것으로 기대되고 있습니다.

지역별 분석

아시아태평양은 2025년에 41.00%의 시장 점유율을 차지하며 고대역폭 메모리 시장을 주도하고 있으며, 2031년까지 연평균 성장률(CAGR) 26.66%로 성장할 전망입니다. 이 지역은 한국이나 일본 등 각국 정부의 보조금 덕분에 큰 혜택을 받고 있으며, 이로 인해 팹 비용이 20-40% 절감되고 있습니다. 이러한 보조금 덕분에 SK하이닉스 등의 기업들은 2026년 1분기 매출액 371억 달러에 대해 72%의 영업이익률을 달성할 수 있었습니다. 또한, 마이크론이 히로시마의 신규 공장에 96억 달러를 투자하는 것은 중국 이외공급 경로를 다각화하고, 보다 안정적인 공급망을 확보하기 위함입니다. 한편, 중국의 국내 DRAM 제조업체들은 2026년까지 HBM3 생산량을 확대하기 위해 노력하고 있지만, 기술 발전 및 생산 능력 면에서는 기존 주요 기업들에 비해 18-24개월 뒤처져 있습니다.

북미는 하이퍼스케일러들의 활발한 수요와 ‘CHIPS법’에 따른 보조금을 통한 정부의 강력한 지원에 힘입어 2위 시장으로 자리매김했습니다. 총액 66억 달러를 넘는 이 보조금은 애리조나주에 위치한 TSMC의 첨단 패키징 거점 개발에 중요한 역할을 해왔습니다. Nvidia, AMD, Broadcom과 같은 미국에 본사를 둔 주요 기업들은 전 세계 HBM 조달량의 70% 이상을 차지하고 있으며, 이 지역공급망은 실리콘밸리의 기술 로드맵과 밀접하게 연계되어 있습니다. 한편, 유럽은 자국 내 DRAM 생산 능력이 제한적이기 때문에 뒤처지고 있습니다. 그러나 특히 자동차용 첨단 운전자 보조 시스템(ADAS)이나 고성능 컴퓨팅(HPC) 센터용 용도 분야에서 여전히 중요한 소비 시장으로 자리 잡고 있습니다.

남미, 중동 및 아프리카는 주로 통신 인프라의 업그레이드와 각국의 AI 개발 이니셔티브에 힘입어 수요가 확대되고 있는 신흥 시장을 총칭합니다. 그러나 이러한 지역에서는 수출 허가 제한이나 현지 포장 능력 부족과 같은 문제에 직면해 있어, 당분간 출하량에 제약을 받고 있습니다. 그 결과, 이러한 시장은 단기적으로는 주요 수익원이라기보다는 미래 성장을 위한 전략적 기회로 현재 간주되고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

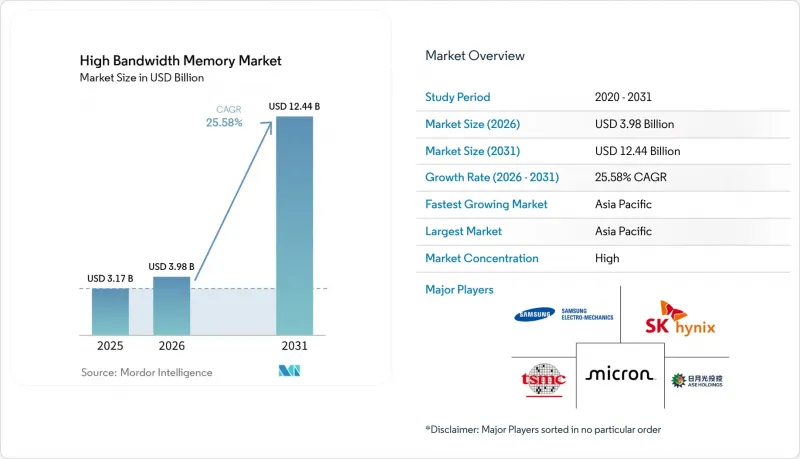

JHS 26.06.29According to Mordor Intelligence, the high bandwidth memory market size is expected to increase from USD 3.17 billion in 2025 to USD 3.98 billion in 2026 and reach USD 12.44 billion by 2031, growing at a CAGR of 25.58% over 2026-2031.

This report is Segmented by Application (Servers, Networking, High-Performance Computing, Consumer Electronics, and Automotive and Transportation), Technology (HBM2, HBM2E, HBM3, HBM3E, and HBM4), Memory Capacity Per Stack (4 GB, 8 GB, 16 GB, 24 GB, and More), Processor Interface (GPU, CPU, AI Accelerator/ASIC, FPGA, and Other Interfaces), and Geography. Market Forecasts are Provided in Terms of Value (USD).

Global High Bandwidth Memory Market Trends and Insights

AI-Server Proliferation and GPU Attach Rates

Enterprises are pivoting toward GPU-dense servers that demand four to eight HBM stacks per node to keep pace with transformer models exceeding one trillion parameters. Dell Technologies reported AI-optimized server revenue up 80% year over year in fiscal 2025, illustrating how traditional OEMs are profiting from this pivot. Non-traditional buyers such as Bitcoin miner-turned-AI provider IREN have ordered 20,000 Nvidia H200 GPUs, each with 141 GB of HBM3E, confirming that bandwidth needs spill across verticals. As model sizes grow, the memory-to-compute ratio continues to climb, locking in multiyear visibility for HBM suppliers. The generational jump from HBM2E to HBM3E raised per-stack bandwidth by 50%, yet developers are already specifying HBM4 for 2027 hardware, compressing product lifecycles and forcing overlapping R&D. Consequently, DRAM makers are capturing a larger share of system bill-of-materials than GPU vendors ever anticipated.

Data-Center Shift to DDR5 and 2.5-D Packaging

Migration from DDR4 to DDR5 has familiarized substrate manufacturers and assembly houses with multi-gigahertz signaling, lowering perceived risk around HBM qualification. By late 2025, DDR5 modules represented over half of server DRAM shipments, and the learning curve in thermal design for 6.4 GT/s interfaces directly benefits HBM packaging. TSMC's Chip-on-Wafer-on-Substrate process routes thousands of micro-bumps between logic and memory dies, a technology that evolved from earlier 2.5-D field-programmable gate arrays. As manufacturing maturity rises, HBM cost premiums have narrowed from 10X to roughly 4X versus commodity DRAM, widening adoption beyond hyperscale AI into high-performance computing and premium graphics cards. Standards bodies have codified interoperability, preventing vendor lock-in and accelerating the diffusion of High Bandwidth Memory across multiple compute domains.

Limited CoWoS/SoIC Advanced-Packaging Capacity

TSMC's CoWoS and SoIC lines reached roughly 120,000 wafers per month by late 2025, but Nvidia alone reserved more than half of that volume for 2026. Short-run alternatives at ASE, Amkor, and JCET offer fan-out or silicon-bridge options, yet these processes lag in yield and customer qualifications, forcing second-tier chip designers to accept longer validation cycles or reduced performance. Although TSMC earmarked part of its USD 44-50 billion in fiscal 2026 capex for new packaging capacity in Arizona, near-term supply remains inelastic. Consequently, packaging capacity, not wafer starts, is the gating factor for High Bandwidth Memory market growth through 2028, and customers with multi-source strategies command premium allocations.

Other drivers and restraints analyzed in the detailed report include:

- Hyperscaler Preference for Silicon Interposers

- Localized Memory Production Subsidies

- Geo-Political Export Controls on AI Accelerators

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Servers accounted for 67.80% of the total 2025 revenue, making them the anchor of the High Bandwidth Memory market size at USD 3.17 billion. Hyperscale data centers deploy four to eight HBM stacks per GPU, translating to hundreds of petabytes of addressable demand annually. Networking equipment, such as 800-Gb Ethernet line cards, uses HBM to meet ultra-low-latency thresholds but accounts for only a modest slice of revenue. High-performance computing centers are transitioning from HBM2E to HBM3E to reduce time-to-solution on memory-bound algorithms.

Automotive platforms represent the fastest-growing slice, advancing at a 26.58% CAGR as centralized compute domains consolidate sensor fusion and path planning on single SoCs that integrate HBM. NVIDIA's Drive Thor delivers 2,000 TOPS with on-package HBM to digest nearly 1 TB of sensor data per hour. Premium consumer graphics cards still leverage stacked DRAM, but cost-sensitive SKUs favor GDDR because gaming workloads are less bandwidth-constrained. The strategic implication is that design-win longevity in automotive, combined with stringent safety certifications, creates thicker margins than hyperscale refresh cycles can offer.

HBM3 accounted for 45.70% of the revenue in 2025, driven by its widespread adoption across high-performance computing and AI applications. However, HBM3E is anticipated to drive growth at 26.43%, as suppliers increasingly qualify 12-layer stacks capable of exceeding 3 TB/s. These advanced stacks offer significantly higher bandwidth, which reduces the number of packages required per accelerator. This, in turn, minimizes interposer area and enhances overall yield. Meanwhile, HBM2 and HBM2E are experiencing a steady decline, with their usage now largely confined to networking and legacy compute systems.

Sampling of HBM4 commenced in early 2025, marking a significant milestone in memory technology. SK Hynix was the first to ship 12-layer modules, with Samsung following closely behind a few months later. The specifications for HBM4 are impressive, featuring more than 10 Gb/s per pin and stack bandwidth exceeding 2 TB/s. Additionally, HBM4 offers a 40% improvement in energy efficiency compared to HBM3E, making it a highly attractive option for next-generation applications. The transition to volume production is expected to begin in 2026, likely accelerating the shift in revenue share toward HBM4 by the end of the decade. This evolution is also expected to pave the way for photonics-ready HBM variants, projected to emerge between 2028 and 2029.

Geography Analysis

Asia-Pacific dominated the High Bandwidth Memory market with 41.00% market share in 2025 and is set to grow at a 26.66% CAGR through 2031. The region benefits significantly from government subsidies in countries like South Korea and Japan, which reduce fab costs by 20-40%. These subsidies have enabled companies like SK hynix to achieve an operating margin of 72% on USD 37.1 billion in Q1-2026 revenue. Additionally, Micron's USD 9.6 billion investment in a new Hiroshima facility aims to diversify non-Chinese supply lines, ensuring a more stable supply chain. Meanwhile, China's domestic DRAM manufacturers are striving to ramp up HBM3 production volumes by 2026, though they remain 18-24 months behind established players in terms of technological advancements and production capabilities.

North America ranks as the second-largest market, driven by strong hyperscaler demand and significant government support through the CHIPS Act grants. These grants, totaling more than USD 6.6 billion, have been instrumental in developing TSMC's advanced packaging hub in Arizona. Major U.S.-based companies such as Nvidia, AMD, and Broadcom collectively account for over 70% of global HBM procurement, aligning the region's supply chain closely with Silicon Valley's technological roadmaps. Europe, on the other hand, lags due to its limited indigenous DRAM production capacity. However, it remains a critical consumer market, particularly for applications in automotive advanced driver-assistance systems (ADAS) and high-performance computing (HPC) centers.

South America, the Middle East, and Africa collectively represent emerging markets with growing demand, primarily driven by telecommunications infrastructure upgrades and national AI development initiatives. However, these regions face challenges, such as export licensing restrictions and limited local packaging capabilities, which constrain immediate shipment volumes. As a result, these markets are currently viewed as strategic opportunities for future growth rather than primary revenue contributors in the near term.

- Samsung Electronics Co., Ltd.

- SK hynix Inc.

- Micron Technology, Inc.

- Intel Corporation

- Advanced Micro Devices, Inc.

- Nvidia Corporation

- Taiwan Semiconductor Manufacturing Company Limited

- ASE Technology Holding Co., Ltd.

- Amkor Technology, Inc.

- Powertech Technology Inc.

- United Microelectronics Corporation

- GlobalFoundries Inc.

- Applied Materials Inc.

- Marvell Technology, Inc.

- Rambus Inc.

- Cadence Design Systems, Inc.

- Synopsys, Inc.

- Siliconware Precision Industries Co., Ltd.

- JCET Group Co., Ltd.

- Chipbond Technology Corporation

- Cadence Design Systems Inc.

- Broadcom Inc.

- Celestial AI

- ASE-SPIL (Silicon Products)

- Graphcore Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 AI-Server Proliferation and GPU Attach Rates

- 4.2.2 Data-Center Shift to DDR5 and 2.5-D Packaging

- 4.2.3 Edge-AI Inference in Automotive ADAS

- 4.2.4 Hyperscaler Preference for Silicon Interposer Stacks

- 4.2.5 Localized Memory Production Subsidies (KR, US, JP)

- 4.2.6 Photonics-Ready HBM Road-Maps (HBM-P)

- 4.3 Market Restraints

- 4.3.1 TSV Yield Losses Above 12-Layer Stacks

- 4.3.2 Limited CoWoS/SoIC Advanced-Packaging Capacity

- 4.3.3 Thermal Throttling in >1 TB/s Bandwidth Devices

- 4.3.4 Geo-Political Export Controls on AI Accelerators

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 DRAM Market Analysis

- 4.8.1 DRAM Revenue and Demand Forecast

- 4.8.2 DRAM Revenue by Geography

- 4.8.3 Current Pricing of DDR5 Products

- 4.8.4 List of DDR5 Product Manufacturers

- 4.9 Impact of Macroeconomic Factors

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Application

- 5.1.1 Servers

- 5.1.2 Networking

- 5.1.3 High-Performance Computing

- 5.1.4 Consumer Electronics

- 5.1.5 Automotive and Transportation

- 5.2 By Technology

- 5.2.1 HBM2

- 5.2.2 HBM2E

- 5.2.3 HBM3

- 5.2.4 HBM3E

- 5.2.5 HBM4

- 5.3 By Memory Capacity per Stack

- 5.3.1 4 GB

- 5.3.2 8 GB

- 5.3.3 16 GB

- 5.3.4 24 GB

- 5.3.5 32 GB and Above

- 5.4 By Processor Interface

- 5.4.1 GPU

- 5.4.2 CPU

- 5.4.3 AI Accelerator / ASIC

- 5.4.4 FPGA

- 5.4.5 Others

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 France

- 5.5.3.3 United Kingdom

- 5.5.3.4 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Samsung Electronics Co., Ltd.

- 6.4.2 SK hynix Inc.

- 6.4.3 Micron Technology, Inc.

- 6.4.4 Intel Corporation

- 6.4.5 Advanced Micro Devices, Inc.

- 6.4.6 Nvidia Corporation

- 6.4.7 Taiwan Semiconductor Manufacturing Company Limited

- 6.4.8 ASE Technology Holding Co., Ltd.

- 6.4.9 Amkor Technology, Inc.

- 6.4.10 Powertech Technology Inc.

- 6.4.11 United Microelectronics Corporation

- 6.4.12 GlobalFoundries Inc.

- 6.4.13 Applied Materials Inc.

- 6.4.14 Marvell Technology, Inc.

- 6.4.15 Rambus Inc.

- 6.4.16 Cadence Design Systems, Inc.

- 6.4.17 Synopsys, Inc.

- 6.4.18 Siliconware Precision Industries Co., Ltd.

- 6.4.19 JCET Group Co., Ltd.

- 6.4.20 Chipbond Technology Corporation

- 6.4.21 Cadence Design Systems Inc.

- 6.4.22 Broadcom Inc.

- 6.4.23 Celestial AI

- 6.4.24 ASE-SPIL (Silicon Products)

- 6.4.25 Graphcore Limited

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-need Assessment